Principles of Finance 6e Chapter 9

Besley/Brigham

9-21

9-32 With a calculator, enter N = 10 x 2 = 20, I/Y= 10/2 = 5, and PV = –10,000, and press PMT to get

PMT = $802.43. Or

43.802

46221.12

000,10

PMT

)46221.12(PMT

05.0

PMT000,10

20

)05.1(

==

=

=

Set up an amortization table for Year 1:

Pmt of

Period Beg Bal Payment Interest* Principal End Bal

1 $10,000.00 $802.43 $500.00 $302.43 $9,697.57

9-33 a. Using a financial calculator, enter N = 5, I/Y= 10, PV = 25,000, and FV = 0; compute PMT =

-6,594.94.

r

1

PMTPVA

n

)r1(

1

−

=+

Set up an amortization schedule as described in the appendix to Chapter 9.

Beginning Repayment Remaining

Year Balance Payment Interest* of Principal Balance

1 $25,000.00 $ 6,594.94 $2,500.00 $ 4,094.94 $20,905.06

Chapter 9 Principles of Finance 6e

Besley/Brigham

b. Here the loan size is doubled, so the payments also double in size to $13,189.87.

c. Using a financial calculator, enter N = 10, I/Y= 10, PV = 50,000, and FV = 0; compute PMT

= –8,137.27.

9-34 0 1 2 3 4 5 6 7 8 9 10

Z: –422.410 0 0 0 0 0 0 0 0 1,000.00

B: -500.00 74.50 74.50 74.50 74.50 74.50 74.50 74.50 74.50 74.50 74.50

a. Security Z:

Security B:

r

1

50.74500

10

)r1(

1

−

=

+

r = ?

Principles of Finance 6e Chapter 9

Besley/Brigham

9-23

b. Using a calculator, for Security Z, enter N = 10, I/Y= 6, PMT = 0, and FV = 1,000; compute PV

c. The value of Security Z would fall from $422.41 to $321.97, so a loss of $100.44, or 23.8

percent, would be incurred. The value of Security B would fall to $420.94, so the loss here

9-35 a. If Jason makes his first withdrawal today, this is an annuity due:

0 1 2 3 4 5 45 46 47 48 Months

10,000

PMT PMT PMT PMT PMT PMT PMT PMT PMT

73.260

35370.38

000,10

PMT

)35370.38(PMT01.1

01.0

PMT000,10

48

)01.1(

==

=

=

b. If Jason makes his first withdrawal in one month, then this is an ordinary annuity:

0 1 2 3 4 5 45 46 47 48 Months

10,000

PMT PMT PMT PMT PMT PMT PMT PMT PMT

…

r = 1%

…

r=1%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-24

34.263

97396.37

000,10

PMT

)97396.37(PMT

01.0

1

PMT000,10

r

1

PMTPVA

48

n

)01.1(

1

)r1(

1

==

=

−

=

−

=+

9-36 Here we want to have the same effective annual rate (rEAR) on the credit extended as on the bank

loan that will be used to finance the credit extension.

First, we must find the EAR of the bank loan:

rEAR = (1 + 0.15/12)12 – 1 = (1.0125)12 – 1 = 16.075%

9-37 Set the calculator to BGN mode.

a. Calculator solution: I/Y= 18/12 = 1.5, PV = 3,310, PMT = -150, and FV = 0; N = ? = 26.51

months, or 2.2 years.

9-38 a. Calculator solution: N = 240, I/Y= 0.75, PV = 95,000, and FV = 0; PMT = ? = -854.74

Principles of Finance 6e Chapter 9

Besley/Brigham

9-25

74.854

144954.111

000,95

PMT

)144954.111(PMT

0075.0

1

PMT000,95

r

1

PMTPVA

240

n

)0075.1(

1

)r1(

1

==

=

−

=

−

=+

b. Calculator solution: N = 120, I/Y= 0.75, PV = 95,000, and FV = 0; PMT = ? = -1,203.42

42.203,1

94169.78

000,95

PMT

==

c. Calculator solution: I/Y= 0.75, PV = 95,000, PMT = -985, and FV = 0; N = ? = 171.98 months,

or 14.3 years.

9-39 a. Car price, excluding rebates = $24,000 = price if 0 percent financing is taken

b. Car price with rebate = $24,000 – $3,000 = $21,000 = price if credit union loan is used

( )

+

−

=

m

r

1

1

1

PMTPVA m

r

c. Based only on the monthly payment, the car should be purchased using the credit union loan;

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-26

d. Three years remain on the loans:

0% financing balance = (2 x 12) x $500 = $12,000

( )

1

1

1

24

12

06.0

+

−

9-40 a. First, determine the annual cost of college. The current cost is $12,500 per year, which will

escalate at a 5 percent inflation rate:

College Current Years Inflation Cash

Year Cost from Now Adjustment Required

1 $12,500 5 (1.05)5 $15,954

Now put these costs on a cash flow time line and find the PV at the time the daughter starts

college—that is, when she turns 18:

0 1 2 3 Year of College

18 19 20 21 Age

b. The daughter has $7,500 now (age 13) to help achieve the educational goal. Five years hence

the $7,500, when invested at 8 percent, will be worth $11,020:

13 14 15 16 17 18

7,500 FV = ?

8%

8%

Principles of Finance 6e Chapter 9

Besley/Brigham

9-27

c. The father needs to accumulate only $61,204 – $11,020 = $50,184. The key to completing the

problem at this point is to realize the series of deposits represent an ordinary annuity rather

than an annuity due, despite the fact the first payment is made at the beginning of the first year.

The reason it is not an annuity due is because there is no interest paid on the last payment,

which occurs when the daughter is 18. Thus,

0 1 2 3 4 5 Year

13 14 15 16 17 18 Age

PMT PMT PMT PMT PMT PMT

FVA = 50,184

1)08.1(

PMT)r1(

r

1)r1(

PMTFVA

5

n

−

+

+

−+

=

9-41 a. 0 1 2 29 30 Years

0 1 2 3 4 58 59 60 Periods

–500 –500 –500 –500 –500 –500 –500

FVA60 = ?

…

5%

8%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-28

( )

( )

792,176)58372.353(500

05.0

1)05.1(

500

m

r

1

m

r

1

PMTFVA

60

mn

==

−

=

−+

=

Using a calculator, enter N = 30 x 2 = 60, I/Y= 10/2 = 5, and PMT = -500; compute FV =

$176,792.

b. To solve this problem, we have to recognize that the answer given in part a is too high by the

$10,000 withdrawal plus the interest the $10,000 would have earned for 10 years. The $10,000

withdrawal made 10 years before Kay’s retirement would have been worth the following amount

at retirement:

9-42 0 1 4 5 Years

0 1 2 3 4 16 17 18 19 20 Periods

(1) Dealer’s “special financing package”

1

20

(1.01)

1

PVA 1,200 1,200(18.04555) 21,654.66

0.01

−

= = =

(2) Bank loan

1

20

(1.03)

1

PVA 1,200 1,200(14.8875) 17,852.97

0.03

−

= = =

…

Principles of Finance 6e Chapter 9

9-29

9-43 Information given:

2. When she retires, Janet wants to take a trip around the world at a cost of $120,000.

The cash flow time line for Janet is:

25 26 27 28 65 66 67 84 85 Janet’s age

0 1 2 3 20 Payments

0 1 2 19 20 Withdrawals

-PMT -PMT -PMT -PMT

120,000 Trip cost

70,000 70,000 70,000 Ret. inc.

05.0

So, at retirement, including the cost of the trip around the world, Janet needs a total of

$992,355 = $872,355 + $120,000. Thus, the cash flow time line for Janet today, when she is

planning her retirement and wants to determine the amount she needs to contribute to the

retirement fund, is as follows:

The cash flow time line for Janet is:

25 26 27 28 63 64 65 Janet’s age

0 1 2 3 18 19 20 Payments to retirement fund

-PMT -PMT –PMT -PMT -PMT -PMT

7%

5%

7%

…

…

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-30

9-44 Integrative Problem

a. Discuss basic time value concepts, terminology, and solution methods. A cash flow time line is

a graphical representation that is used to show the timing of cash flows. The tick marks

represent end of periods (often years), so time 0 is today; time 1 is the end of the first year, or 1

year from today; and so on.

LUMP-SUM AMOUNT—a single flow; for example, a $100 inflow in Year 2:

0 1 2 3 Year

100 Cash flow

r%

b. (1) Show dollars corresponding to question mark, calculated as follows:

0 1 2 3

100 FV = ?

r%

10%

Principles of Finance 6e Chapter 9

Besley/Brigham

9-31

After 1 year:

FV1 = PV + INT1 = PV + PV(r) = PV(1 + r) = $100(1.10) = $110.00.

Similarly:

Finding future values (moving to the right along the time line) is called compounding. Note

we generally find FV using one of these methods:

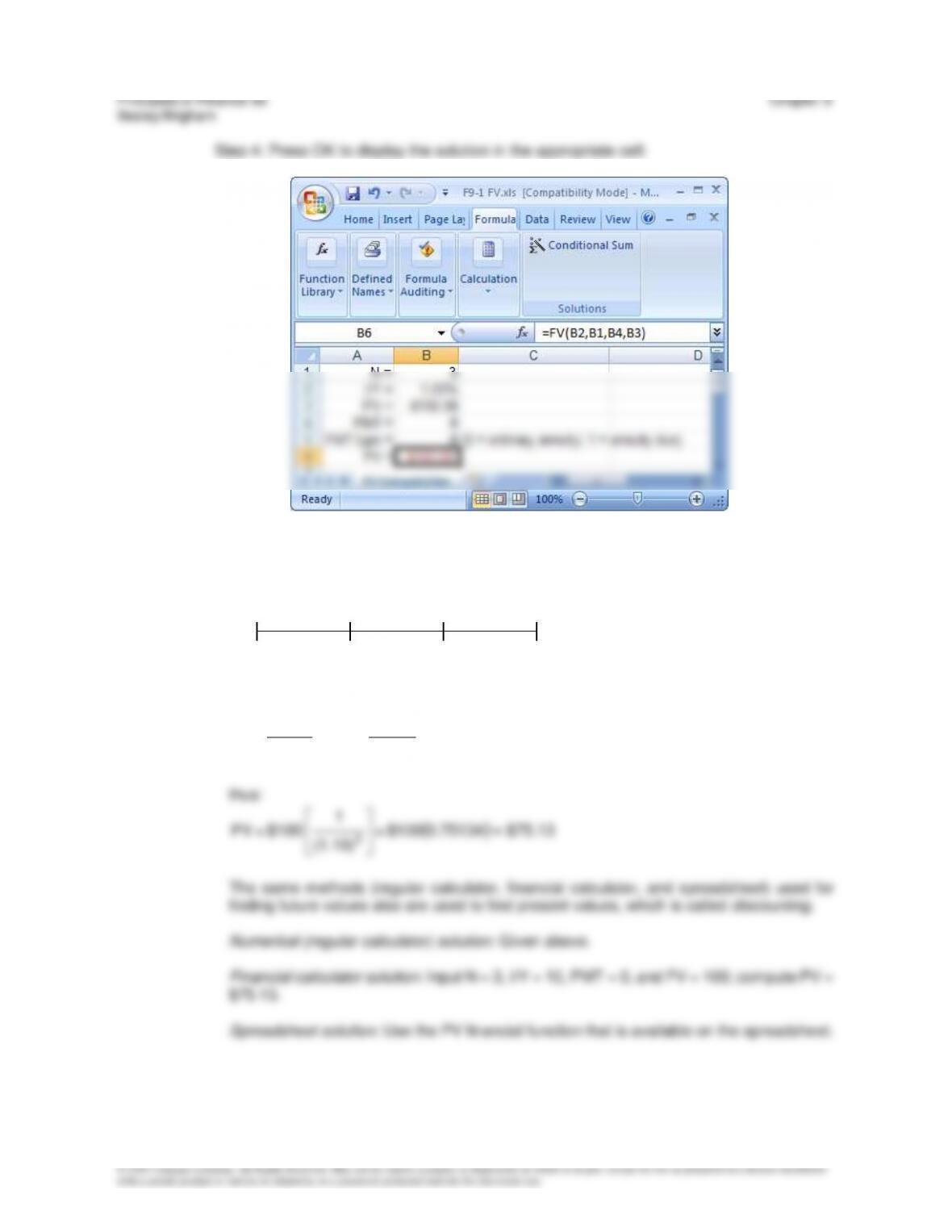

(i) Numerical approach—use a regular calculator to solve: FV3 = $100(1.10)3 = $133.10.

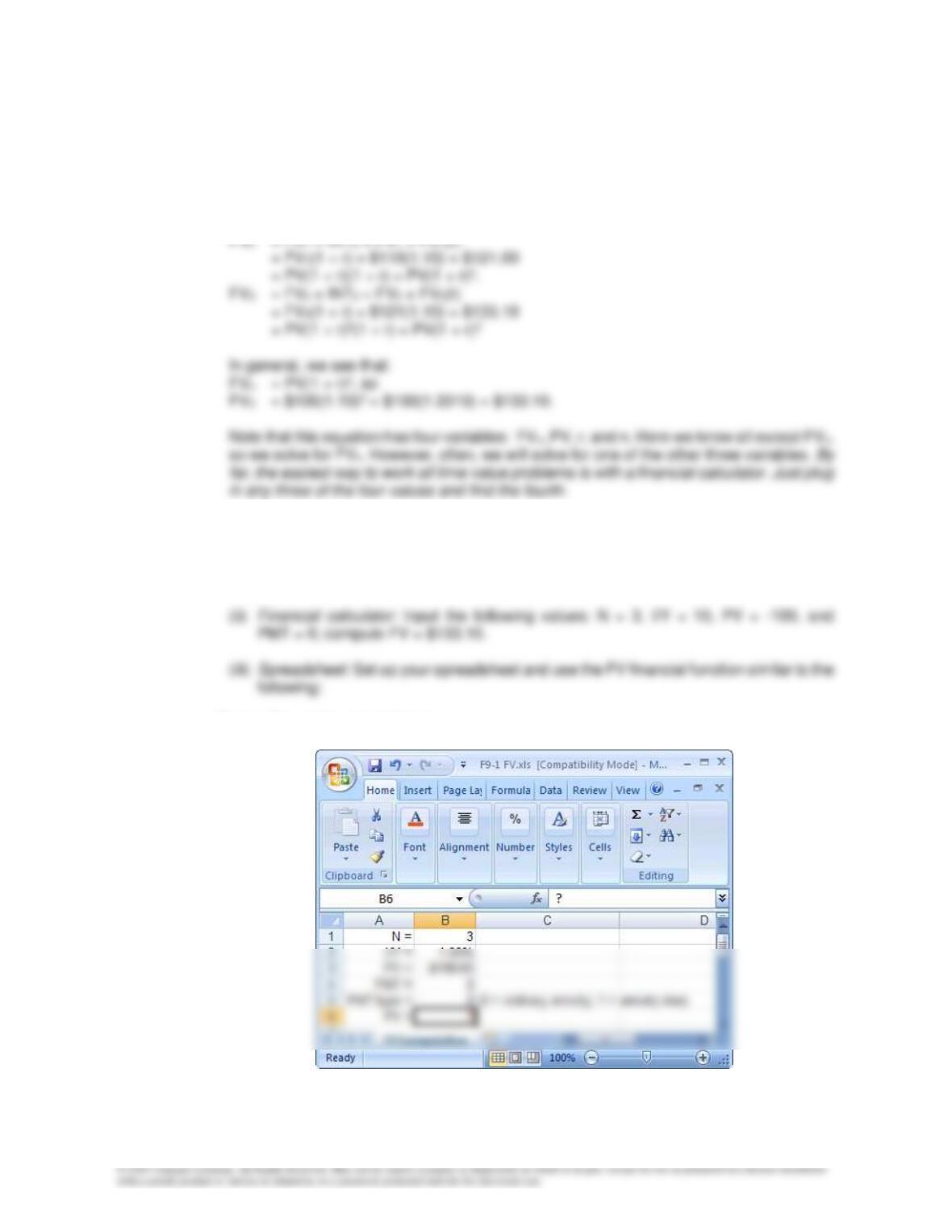

Step 1: Set up the spreadsheet:

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-32

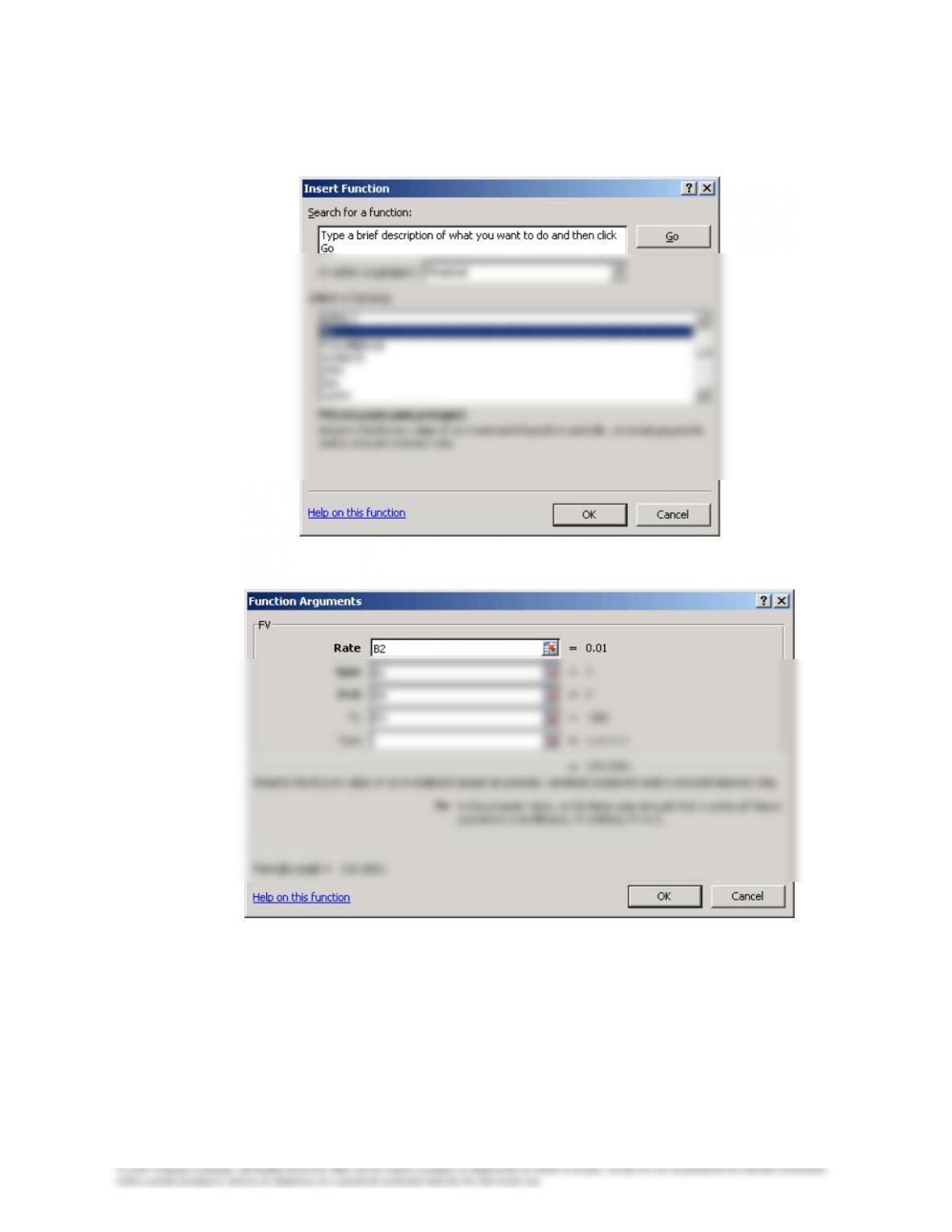

Step 2: Select FV in the financial function category:

Step 3: Input the cell locations of the data:

9-33

(2) Finding present values, or discounting (moving to the left along the time line), is the reverse

of compounding, and the basic present value equation is the reciprocal of the compounding

equation:

0 1 2 3

PV = ? 100

FVn = PV(1 + r)n transforms to:

)

r + (1

1

FV

=

)r + (1

FV

=PV n

n

n

n

10%

Chapter 9 Principles of Finance 6e

Besley/Brigham

9-34

c. We have this situation in time line format:

0 1 2 3 n = ?

-1 3

If we want to find out how long it will take us to triple our money at an interest rate of 20

percent, we can use any numbers, say, $1 and $3, with this equation:

Numerical (regular calculator) solution: Use a trial-and-error method, substituting values in for n

until the right side of the equation equals 3. Or, using more complex mathematics, we can solve

the above equation as follows:

)20.1(13

n

=

d. 0 1 2 3

100 100 100

e. (1) 0 1 2 3

100 100 100

One approach would be to treat each annuity flow as a lump sum as in the time line. Here

we have:

20%

…

10%

10%