Chapter 8 Principles of Finance 6e

Besley/Brigham

8-14

December January February

Cash Receipts:

Receipts from sales $160,000 $40,000

Cash Disbursements:

Payments for purchases 40,000 40,000

Net cash flow for the month $113,200 $( 6,800)

8-16 a. (1) Determine the variable cost per unit at present, using the following definitions and

equations:

Q = units of output (sales) = 5,000.

P = average sales price per unit of output = $100.

(2) Determine the new EBIT level if the change is made:

(3) Determine the incremental EBIT:

ΔEBIT = $135,000 – $50,000 = $85,000.

(4) Estimate the approximate rate of return on the new investment:

21.25%0.2125

$400,000

$85,000

Investment

ΔEBIT

ΔROA ====

Because the ROA exceeds Olinde’s average cost of funds, this analysis suggests that

Olinde should go ahead and make the investment.

Principles of Finance 6e Chapter 8

Besley/Brigham

b.

FV)Q(P

V)Q(P

DOL −−

−

=

units 4,000

$50$100

$200,000

VP

F

Q

OpBE

=

−

=

−

=

:Old

8-17 a. Carol’s Fashion Designs, Inc.

Cash Budget, July-December 2016

I. Collections and Payments:

May June July August September October November December

Credit Sales $180,000 $180,000 $360,000 $540,000 $720,000 $360,000 $360,000 $ 90,000

Labor/Materials 90,000 90,000 126,000 882,000 306,000 234,000 162,000 90,000

Cash Receipts:

From this month’s sales (10%) 36,000 54,000 72,000 36,000 36,000 9,000

Cash Disbursements:

Labor/raw materials (1 month lag) 90,000 126,000 882,000 306,000 234,000 162,000

Administrative salaries 27,000 27,000 27,000 27,000 27,000 27,000

Lease payment 9,000 9,000 9,000 9,000 9,000 9,000

b. The cash budget indicates that Carol will have surplus funds available during July, August,

c. In a situation such as this, where inflows and outflows are not synchronized during the month, it

might not be possible to use a cash budget centered on the end of the month. The cash budget

7/2 7/4 7/5 7/6 7/14 7/30

Beginning cash balance $132,000 $132,000 $132,000 $132,000 $132,000 $132,000

Cumulative inflows

[1/30xreceiptsx(# days)] 13,200 26,400 33,000 39,600 92,400 198,000

Principles of Finance 6e Chapter 8

Besley/Brigham

8-17

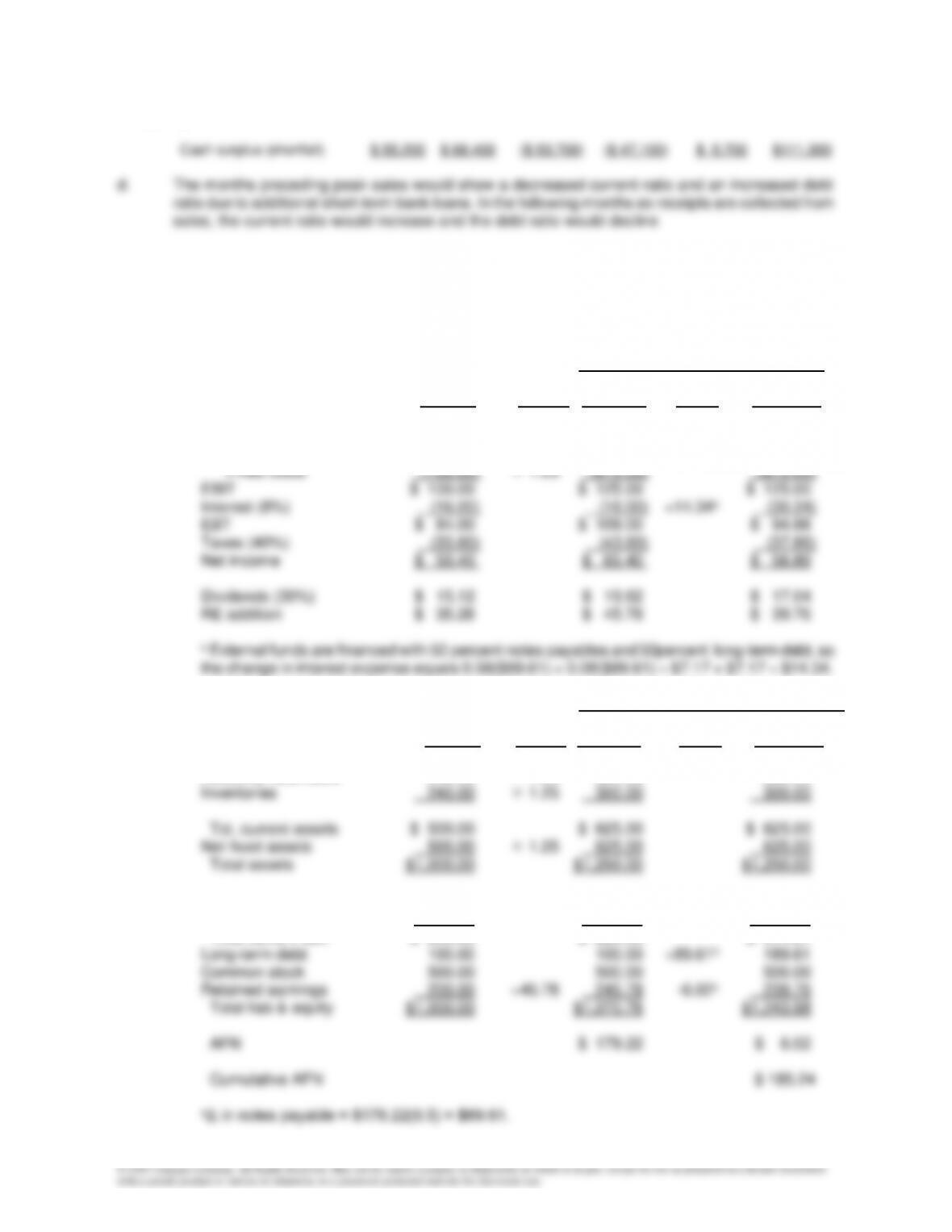

8-18 Integrative Problem

PART I

a. Income Statement:

2016 Forecast

2015 Forecast Feed-

Actual Basis 1st Pass Back 2nd Pass

Sales $2,000.00 1.25 $2,500.00 $2,500.00

Less: Var. costs (60%) (1,200.00) 1.25 (1,500.00) 1,500.00

Balance Sheet: 2016 Forecast

2015 Forecast Feed-

Actual Basis 1st Pass Back 2nd Pass

Cash & securities $ 20.00 1.25 $ 25.00 $ 25.00

Accounts receivable 240.00 1.25 300.00 300.00

A/P and accruals $ 100.00 1.25 $ 125.00 $ 125.00

Notes payable 100.00 100.00 +89.61a 189.61

Total current liab. $ 200.00 $ 225.00 $ 314.61

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-18

b. Key ratios NWC

2015 2016 Industry

Actual 2nd pass 2015

Profit margin 2.52% 2.27% 4.00%

ROE 7.20% 7.68% 15.60%

Days sales outstanding (DSO) 43.20 days 43.20 days 32.00 days

c. (1)

667,2$

75.0

000,2$

operated were assets fixed

which at capacity of Percent

sales Actual

sales

capacity Full ==

=

(2) We had previously found an AFN of $185.24 using two passes through the balance sheet

d. We would expect almost all the ratios to improve. With less financing, interest expense would

Principles of Finance 6e Chapter 8

Besley/Brigham

8-19

Without question, the company’s financial position would be better. One cannot tell exactly how

large the improvement will be without working out the numbers, but when we worked them out

(with a spreadsheet model that requires just one change, a change in capacity utilization from

100 percent to 75 percent), we obtained the following figures:

2016, 2nd Pass

2015 If 2015 Was At

Key Ratios Actual 75% Cap. 100% Cap.

Profit Margin 2.52% 2.51% 2.27%

Roe 7.20% 8.44% 7.68%

e. The DSO and inventory turnover ratio indicate that NWC has excessive inventories and

receivables. The effect of improvements here would be similar to that associated with excess

capacity in fixed assets. Sales could be expanded without proportionate increases in current

f. (1) If the payout ratio were reduced, then more earnings would be retained, and this would

reduce the need for external financing, or AFN.

PART II

a. The computation for operating breakeven is:

units million 15

0.6)–$10(1

million 60$

VP

F

QOpBE ==

−

=

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-20

b. The breakeven chart is:

c. At 20 million units of sales, the operating section of NWC’s income statement would be:

Sales (20 million units @ $10) $200,000,000

Variable costs (60%, or $6) (120,000,000)

000,000,20$

EBIT

The DOL for this level of sales indicates that for every 1 percent change in sales, NOI, or EBIT,

will change by 4 percent. Therefore, if sales actually were 10 percent higher than expected,

EBIT would be 40 percent higher than expected. To show that this is correct, consider the what

the operating section of the income statement would look like if NWC’s sales actually were

$200,000,000(1.10) = $220,000,000:

Sales (22 million units @ $10) $220,000,000

d. At 20 million units of sales, the financing section of NWC’s income statement would be:

0

50

100

150

200

250

300

350

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30

Units (millions)

$ millions

QOpBE = 15

SOpBE = $150

Fixed costs

Total operating costs

Total sales revenues

Principles of Finance 6e Chapter 8

Besley/Brigham

8-21

Net operating income (EBIT) $20,000,000

Interest (16,000,000)

e. Breakeven analysis can be used to help determine the feasibility of the proposal. As the above

analyses show, NWC would have to sell at least 15 million units of the chemical before the

expected. To see this, the income statement for sales units equal to 19 million = 20 million x

0.95 is given below:

Sales (19 million units @ $10) $190,000,000

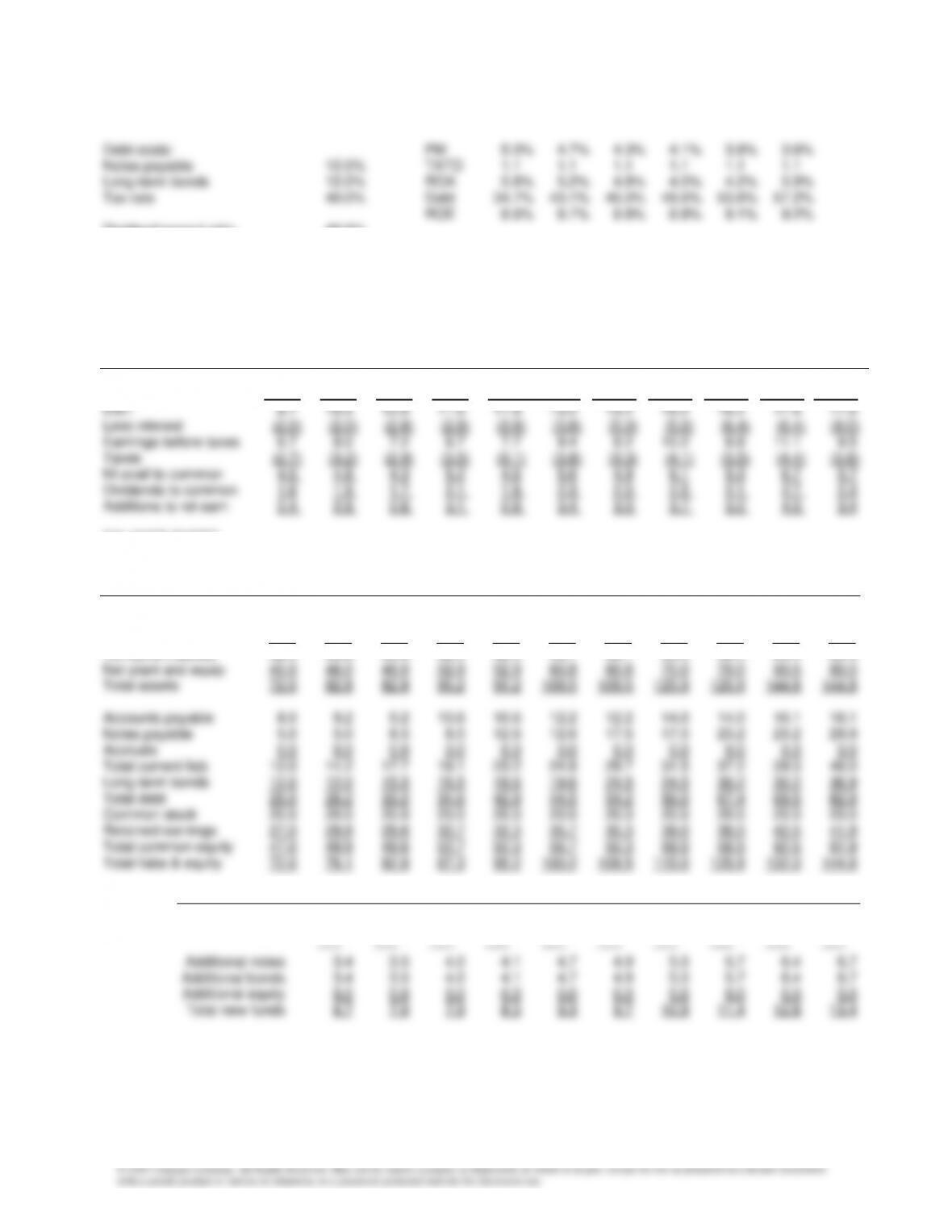

8-19 Computer-Related Problem

a.

INPUT DATA: KEY OUTPUT:

Forecasted sales growth:

2016 15.0% 2016 AFN $7.0

Cumulative AFN $49.8

AFN financing percentages:

Notes payable 50.0%

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-22

Dividend payout ratio 40.0%

MODEL-GENERATED DATA:

INCOME STATEMENT

(IN MILLIONS)

Projected

Historical Initial Final Initial Final Initial Final Initial Final Initial Final

2015 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020

Sales 80.0 92.0 92.0 105.8 105.8 121.7 121.7 139.9 139.9 160.9 160.9

Operating costs (71.3) (82.0) (82.0) (94.3) (94.3) (108.4) (108.4) (124.7) (124.7) (143.4) (143.4)

BALANCE SHEET

Projected

Historical Initial Final Initial Final Initial Final Initial Final Initial Final

2015 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020

Cash 4.0 4.6 4.6 5.3 5.3 6.1 6.1 7.0 7.0 8.0 8.0

Accounts receivable 12.0 13.8 13.8 15.9 15.9 18.3 18.3 21.0 21.0 24.1 24.1

Inventories 16.0 18.4 18.4 21.2 21.2 24.3 24.3 28.0 28.0 32.2 32.2

Tot current assets 32.0 36.8 36.8 42.3 42.3 48.7 48.7 56.0 56.0 64.4 64.4

Initial Final Initial Final Initial Final Initial Final Initial Final

Additional Funds 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020

AFN 6.7 0.3 7.9 0.4 9.3 0.5 10.9 0.6 12.8 0.0

b. (1) growth = 20%

INPUT DATA: KEY OUTPUT:

Forecasted sales growth:

2016 20.0% 2016 AFN $10.2

8-23

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-24

c. (2) dividend payout = 20%

INPUT DATA: KEY OUTPUT:

Forecasted sales growth:

2016 15.0% 2016 AFN $6.1

2017 15.0% 2017 AFN $7.2

AFN financing percentages:

Notes payable 50.0%

Long-term bonds 50.0% Ratios: 2015 2016 2017 2018 2019 2020

Common stock 0.0% Cur 2.5 2.1 1.9 1.7 1.6 1.5

ETHICAL DILEMMA

Competition-Based Planning—Promotion or Payoff?

Ethical dilemma:

Republic Communications Corporation (RCC) has offered you an attractive position in its financial planning

division. The new position would constitute a promotion with a $30,000 increase in salary compared to the

job you now have at National Telecommunications, Inc. (NTI). The problem is that RCC wants you to bring

the rate-setting software you developed at NTI, along with some rate data, with you to the new job. Even

though NTI sells its software to other companies and information concerning telephone rates is available to

the public, you know that such knowledge will help RCC significantly in its attempt to redesign its rate–

setting system. In fact, according to the situation presented in the text, a new and improved rate-setting

program could be worth as much as $200 million per year for RCC. Therefore, the question is whether the

information RCC wants you to take with you to your new job is proprietary to NTI. Should the rate-setting

program and the rate data be considered NTI’s privileged information?

Discussion questions:

• What is the ethical dilemma?

Principles of Finance 6e Chapter 8

Besley/Brigham

8-25

Discussion can be generated by asking the students who they think owns NTI’s rate-setting program.

Does the program belong to the person who developed it, or does it belong to the company? In addition,

ask the students to indicate what information they believe ethically can be taken from one job to

another. Does it matter if the new job is with a company that is in direct competition with the company

you are leaving? Why?

• Should you take the new job? If so, should you take the rate-setting program and the rate data with you

to RCC?

It probably is easier to answer the second question first. The answer to this question is based on

whether the information actually is in the public domain—if it is, then there should not be a problem. For

public utilities that are regulated by states’ public utilities commissions, rate information is available

• What should RCC do?

References:

The situation presented here parallels a case involving American Airlines and Northwest Airlines. According

to a Wall Street Journal article, American alleged that Northwest attempted to steal fare-setting computer

programs by hiring top managers and those involved with computerized planning at significant salary

increases, and asking them to bring some of their work with them to their new jobs. It was after its attempts

to purchase the program from American were refused that Northwest began hiring American managers and

experts. One of the former American employees admitted that, before she left American for a position with

Northwest, she sent some information concerning American’s fare–setting and planning system to a top

manager at Northwest, who also formerly worked for American. American sued Northwest to bar the airline

from using its planning system and to recover financial damages. Northwest found the person who originally

wrote the equations used in American’s planning system; it was discovered that his concepts came from

public sources.

For more information concerning this situation, see the following article:

“Fare Game: Did Northwest Steal American’s Systems? The Court Will Decide,” The Wall Street Journal,