Principles of Finance 6e Chapter 8

Besley/Brigham

8-1

CHAPTER 8

ANSWERS

8-2 a. +

b. – The firm needs less manufacturing facilities, raw materials, and work in process.

8-3 Breakeven analysis, whether operating or financial, shows:

(a) profit planning in relationship to its main determinants.

(b) the effects of leverage on profitability.

8-4 The selling price per unit, the variable cost per unit, and total fixed costs are necessary to construct

8-5 Operating leverage is the presence of fixed costs in the operation of a firm. Operating profits

8-6 Financial leverage exists when fixed financing costs exist. The amount of earnings that can be

8-2

8-7 Firms that have higher degrees of leverage, no matter the type, are perceived as having greater

8-8 The operating breakeven point will be affected as follows:

a. An increase in the sales price –

8-9 It is generally not possible to specify an optimum planning period. The optimum length of time over

8-10 A cash budget is used to project the cash inflows and cash outflows during a specified time period.

________________________________________________________________

SOLUTIONS

8-1 a. Sales = 10,000 x $50 $500,000

Variable costs = 10,000 x $30 (300,000)

30$50$

−

c.

=== 5.2

000,80$

000,200$

NOI

tGrossprofi

DOL

Principles of Finance 6e Chapter 8

Besley/Brigham

8-3

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

8-2

units200

750,1$500,2$

000,150$

QOpBEP =

−

=

8-3 DOL = 4.0x, so EBIT will change in the same direction by 4 percent for every 1 percent change in

sales.

%0.1010.0

000,800$

000,800$000,720$

%−=−=

−

=

8-5 a. 125,000 units 175,000 units

Sales ($15/unit) $1,875,000 $2,625,000

b.

units 140,000 =

$10 – $15

$700,000

=

V– P

F

=

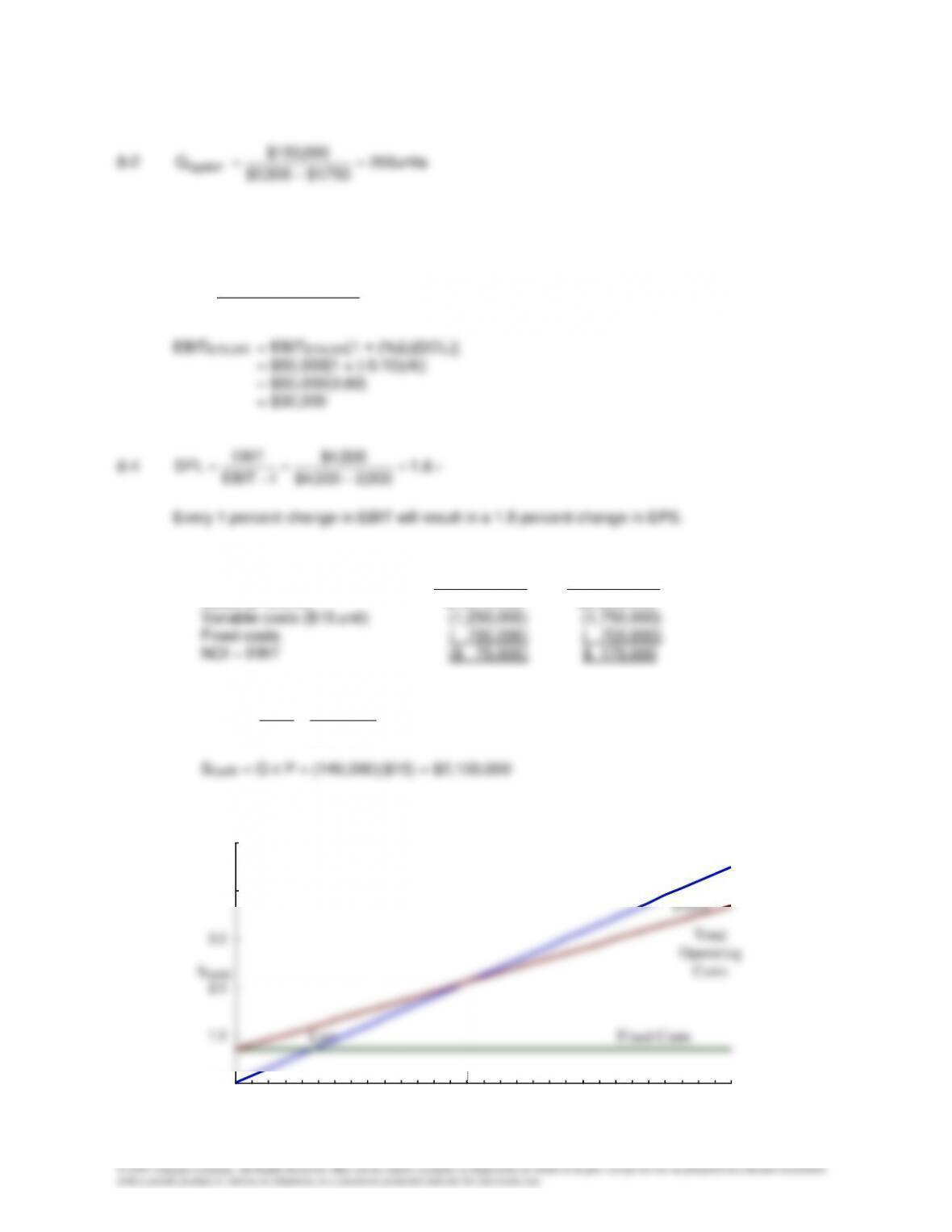

QOpBE

Fixed Costs

($ millions)

Revenues

QOpBE

Output (thousands)

0.0

4.0

5.0

050 100 150 200 250 300

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-4

c. Using Equation 8-4, the DOLs are:

5.0=

$700,000 – )175,000($5

)175,000($5

=

DOL

15.0 =

$700,000 – )150,000($5

)150,000($5

=

DOL

units 175,000

units 150,000

8-6 a. Total assets = Total liabilities & equity

= Accounts payable + Long-term debt + Common stock + Retained earnings

$1,200,000 = $375,000 + Long-term debt + $425,000 + $295,000

b. Using the projected balance sheet:

Additions (New

2015 (1 + g) Financing, R/E) Pro Forma

Total assets $1,200,000 (1.25) $1,500,000

Current liabilities $ 375,000 (1.25) $ 468,750

Long-term debt 105,000 105,000

Principles of Finance 6e Chapter 8

Besley/Brigham

8-5

8-7 a.

units 40,000 =

0.75) – $5(1

$50,000

=

QOpBE

b. At operating BEP, EBIT = 0, so the financing section of Straight Arrow’s income statement

would be:

EBIT $ 0

Interest ($10,000)

c. If sales equal $300,000, the income statement would be:

Sales $300,000

Variable costs (0.75) (225,000)

Gross profit 75,000

===

===

1.67

$10,000 – $25,000

$25,000

I – EBIT

EBIT

DFL

3.0

$25,000

$75,000

EBIT

profit Gross

DOL

$300,000

EPS$270,000 = $0.45[1 + (-0.10)(5.0)] = $0.225

8-6

8-8 Cash 100.00 x 2 = 200.00

Accounts receivable 200.00 x 2 = 400.00

Long-term debt 400.00 400.00

Common stock 100.00 100.00

8-9 a. Craig Computers

Pro Forma Balance Sheet

December 31, 2016

($ millions)

Pro Forma

After

2015 (1 + g) Additions Pro Forma Financing Financing

Cash $ 3.5 (1.2) $ 4.20 $ 4.20

Receivables 26.0 (1.2) 31.20 31.20

Mortgage loan 6.0 6.00 6.00

Common stock 15.0 15.00 15.00

*Profit margin = $10.5/$350 = 3%.

Principles of Finance 6e Chapter 8

Besley/Brigham

8-7

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

Addition to RE = NI – DIV = $12.6 – 0.4($12.6) = 0.6($12.6) = $7.56.

b. Current ratio = $105/$52.44 = 2.00x

The current ratio is poor compared to 2.5x in 2015 and the industry average of 3x.

c. (1) Craig Computers

Pro Forma Balance Sheet

December 31, 2020

($ millions)

Pro Forma

After

2015 (1 + g) Additions Pro Forma Financing Financing

Total curr. assets $ 87.50 (1.2) $105.00 $105.00

Total current liabilities $ 35.50 $ 39.00 $ 24.72

Mortgage loans 6.00 6.00 6.00

AFN = <14.28>

*PM = 3%; Payout = 40%.

(2) Current ratio = $105/$24.72 = 4.25x (good).

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-8

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

**The rate of return declines because of the decrease in the debt/assets ratio. The firm might,

with this slow growth, consider a dividend increase. A dividend increase would reduce future

increases in retained earnings, and in turn, common equity, which would help boost the ROE.

d. Craig probably could carry out either the slow growth or fast growth plan, but under the fast

growth plan (20 percent per year), the risk ratios would deteriorate, indicating that the company

might have trouble with its bankers and would be increasing the odds of bankruptcy.

8-10 a. Noso Textiles

Pro Forma Income Statement

December 31, 2016

($ thousands)

2015 (1 + g) Pro Forma

Sales $36,000 (1.15) $41,400

Operating costs (32,440) (1.15) (37,306)

EBIT $ 3,560 $ 4,094

Noso Textiles

Pro Forma Balance Sheet

December 31, 2015

($ thousands)

Pro Forma

After

2015 (1 + g) Additions Pro Forma Financing Financing

Cash $ 1,080 (1.15) $ 1,242 $ 1,242

Accounts receivable 6,480 (1.15) 7,452 7,452

Long-term debt 3,500 3,500 3,500

Total debt $12,800 $13,880 $16,008

Common stock 3,500 3,500 3,500

Principles of Finance 6e Chapter 8

Besley/Brigham

8-9

b. Δ interest expense = $2,128 x 0.10 = $213.

1st Pass Financing 2nd Pass

2016 Feedback 2016

Sales $41,400 $41,400

1st Pass Financing 2nd Pass

2016 Feedback 2016

Total assets $33,534 $33,534

Accounts payable $ 4,968 $ 4,968

8-11 a.

=== 5.2

320,4$

800,10$

EBIT

profit Gross

DOL

320,4$

320,4$

EBIT

−

440,1$

880,2$320,4$

I–EBIT

b. DOL = 2.5; so for every 1 percent change in sales, EBIT will change by 2.5 percent. DFL = 3.0;

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-10

c. Van Auken can reduce its total leverage by reducing the degree of operating leverage, the

8-12 a., b., & c. Woods Company

Pro Forma Income Statement

December 31, 2016

($ thousands)

AFN

2015 (1 + g) 1st Pass Effects 2nd Pass

Sales $8,000 (1.2) $9,600 $9,600

Operating costs (7,450) (1.2) (8,940) (8,940)

EBIT $ 550 $ 660 $ 660

Woods Company

Pro Forma Balance Sheet

December 31, 2016

($ thousands)

AFN

2015 (1 + g) 1st Pass Effects 2nd Pass

Cash $ 80 (1.2) $ 96 $ 96

Principles of Finance 6e Chapter 8

Besley/Brigham

8-11

Accounts payable $ 160 (1.2) $ 192 $ 192

Accruals 40 (1.2) 48 48

*See income statement, 1st pass.

**2015 CA/CL = $1.040/$452 = 2.3; D/A = ($452 + $1,244)/$4,240 = 40%; to keep these ratios the

same, the following would exist:

Maximum total debt = 0.4 x $5,088 = $2,035

8-13 a. 8,000 units 18,000 units

Sales ($25/watch) $200,000 $450,000

Chapter 8 Principles of Finance 6e

Besley/Brigham

8-12

c.

1.33– =

$60,000–

$80,000

=

$140,000 – $15) – 8,000($25

$15) – 8,000($25

=

DOL units 8,000

d. If the selling price rises to $31, while the variable cost per unit remains fixed, P – V increases to

$16.

$140,000

F

e. If the selling price rises to $31 and the variable cost per unit rises to $23, P – V falls to $8.

$140,000

F

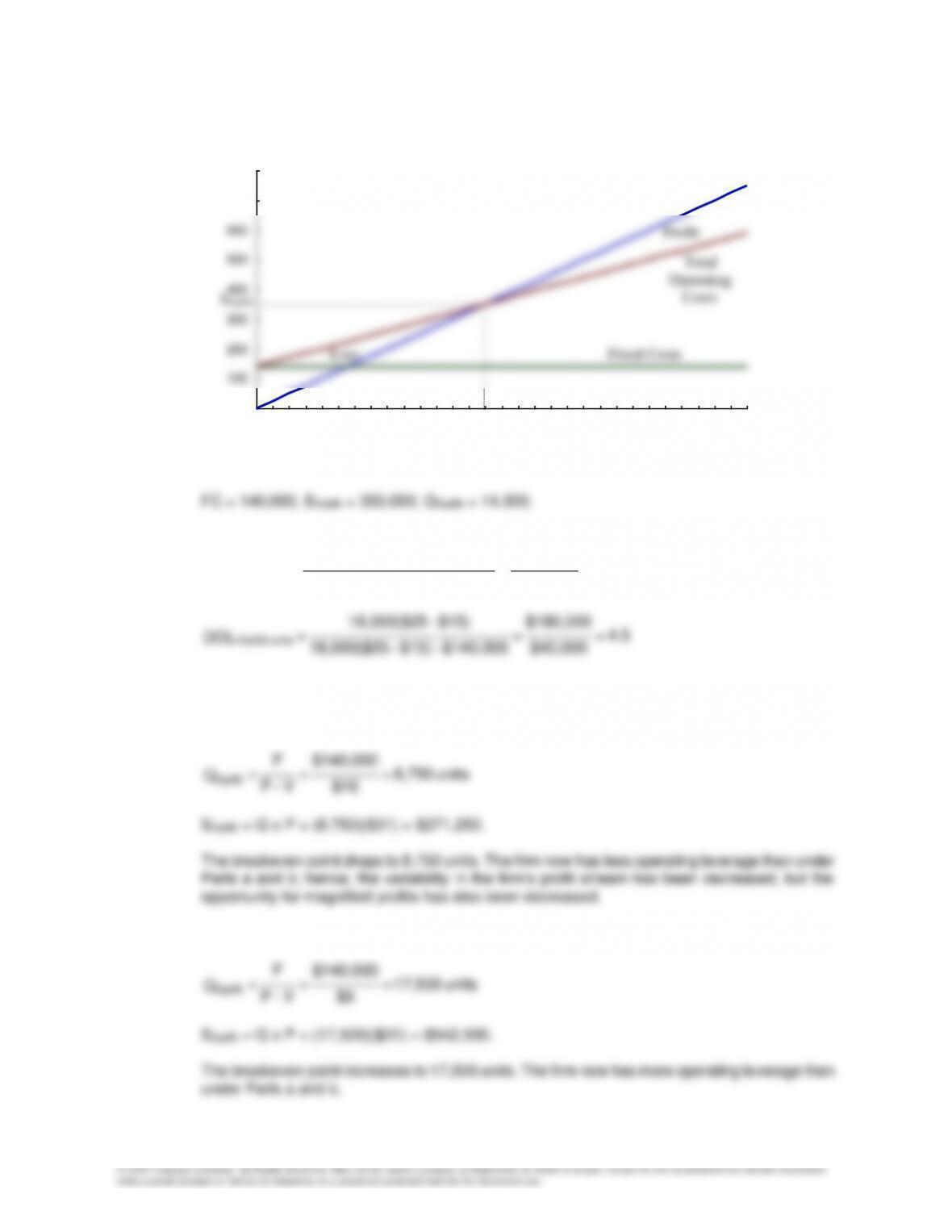

Revenues

Total

Operating

Costs

Fixed Costs

SOpBE

QOpBE

Profit

Loss

($ thousands)

Output (thousands)

0

100

200

300

400

500

600

700

800

0 5 10 15 20 25 30

8-14 a. 5,000 units 12,000 units

Income ($45/unit) $225,000 $540,000

b.

OpBE

F $175,000

= = = 7,000 units

QP – V $45 $20

−

8-15 a. December January February

Cash sales $160,000 $40,000 $60,000

Credit purchases 40,000 40,000 40,000

Cash Receipts:

Net cash flow for the month $ 1,200 $( 6,800) $13,200

Beginning cash balance 400 1,600 (5,200)

b. If the company began selling on credit on December 1, then it would have zero receipts during

December, down from $160,000. Thus, it would have to borrow an additional $160,000, so its