Principles of Finance 6e Chapter 5

Besley/Brigham

5-1

CHAPTER 5

ANSWERS

5-1 The return associated with any investment is based on the change in the investor’s wealth. Any

5-2 a. Regional mortgage rate differentials do exist, depending on supply/demand conditions in

the different regions. However, relatively high rates in one region would attract capital from

other regions, and the end result would be a differential that was just sufficient to cover the

5-3 Short-term rates are more volatile because (1) the Federal Reserve operates mainly in the

5-4 A significant increase in productivity would raise the rate of return on producers’ investments,

5-5 a. The immediate effect on the yield curve would be to lower interest rates in the short-term

end of the market, because the Fed deals primarily in that market segment. However,

5-6 Treasury bonds, along with all other bonds, are available to investors as an alternative

investment to common stocks. An increase in the return on Treasury bonds would increase the

5-7 The open market operations of the Federal Reserve are carried out by buying and selling

Chapter 5 Principles of Finance 6e

5-2

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

deposits in the banking system, and hence it affects the money supply. If the Fed wants to lower

interest rates, it would increase the money supply by purchasing government securities, and

vice versa.

5-8 When an interest rate change occurs, the value of a financial asset changes in an opposite

direction—that is, when the rate increases, the value decreases, and vice versa. This is a

5-9 If investors are convinced that interest rates will increase in the future, they will not want to “lock

5-10 Reinvestment rate risk has a greater impact on short-term investments than long-term

investments. For any investment, an investor has the opportunity to reinvest the funds that are

───────────────────────────────────────────────────────

SOLUTIONS

5-1

%1.57571.0

500,10$

000,6$

500,10$

)000,1($4)500,10$500,12($

HPY ===

+−

=

over the four-year period

000,1$

)20($50

5-3 a.

1,000[($45 $50) 8($0.50)] $1

Return 0.02 2.0%

1,000($50) $50

− + −

= = =− =−

Year 2 1,000[($45 $45) 4($0.50)] $2

1,000($45) $45

5-3

5-4 a. rRF1 = 5%, and

.5%7 =

2

2) Yearin r( + %5

=

rRF

2RF

Solving for rRF in Year 2, we obtain

rRF in Year 2 = (7.5% x 2) – 5% = 10%.

b. For riskless bonds under the expectations theory, the interest rate for a bond of any

maturity is rRF = r* + average inflation over n years. If r* = 3%, we can solve for IPn:

Year 1: rRF1 = 3% + Infl1 = 5%;

Infl1 = Year 1 expected inflation = 5% – 3% = 2%.

5-5 r* = 4%; MRP = 0%; rRF1 = 11%; rRF2 = 13%

RF1 RF RF

RF2

r +( r in Year 2) 11% + (r in Year 2)

r = 13% =

22

Chapter 5 Principles of Finance 6e

5-4

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

The average interest rate during the two-year period differs from the one-year interest rate

expected for Year 2 because of the inflation rates reflected in the two interest rates. The

inflation rate reflected in the interest rate on any security is the average rate of inflation

expected over the security’s life.

5-6 Basic relevant equations:

rt = r* + IPt + DRPt + MRPt + LPt.

But here IP is the only premium, so rt = r* + IPt.

IPt = Avg. inflation = (Infl1 + Infl2 + … + Infln)/n

We can set up this table:

r* I Average I = IPt r = r* + IPt

1 2% 3% 3%/1 = 3% 5%

5-7 rRF = 2.2% in Year 1; IP1 = rRF – r* = 2.2% – 2.0% = 0.2% = Infl1

rRF averages 3.0% for two years. Thus, rRF in Year 2 is:

5-8 Because the only difference between Bond A and Bond B is the term to maturity, the difference

in the yields of these two bonds must be the result of their MRPs. Thus,

Principles of Finance 6e Chapter 5

Besley/Brigham

5-5

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

MRP = (8% – 7.5%)/5 = 0.1% per year

If the yields for Bond A and Bond B are deflated by the MRPs, then the interest rate on the risky

bonds is 7 percent:

Bond A yield = 8.0% = rRF + MRP + DRP = (5.5% + DRP) + 0.1%(10) = (5.5% + DRP) + 1.0%.

Deflating the yield on Bond A by MRP = 1.0%, gives 7.0% = 5.5% + DRP.

Thus, DRP = 7.0% – 5.5% = 1.5%

Bond B yield = 7.5% = rRF + MRP + DRP = (5.5% + DRP) + 0.1%(5) = (5.5% + DRP) + 0.5%.

Deflating the yield on Bond B by MRP = 0.5%, gives 7.0% = 5.5% + DRP.

Thus, DRP = 7.0% – 5.5% = 1.5%

5-9 We know the following:

r3-year bond = 6%

Year Annual Rate

2018 5%

2019 4

2020 3

5-10 We know the following:

r4-year bond = 2.5%

Year Annual Rate

2019 4.5%

5-11 Maturity Yield

1 year 5.0%

2 years 5.5

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-6

Year Rate in Year t

1 5.0%

In one year, the bond that matures in one year will mature (die), and the other bonds will have

one less year to maturity. Given the one-year interest rates computed above, the yields on the

three remaining bonds will be:

Original Maturity Maturity after 1 Year New Yield

1 year Matured —

Following the same logic for the next two years, we have:

Original Maturity Maturity after 2 Years New Yield

1 year Matured —

Original Maturity Maturity after 3 Year New Yield

1 year Matured —

5-12 Maturity Yield

5 years 3.1%

6 years 2.9

5-7

5-13 a. Real

Years to Risk-Free

Maturity Rate (r*) IP** MRP rT = r* + IP + MRP

1 2% 7.0% 0.2% 9.2%

2 2 6.0 0.4 8.4

**The computation of the inflation premium is as follows:

Expected Average

Year Inflation Expected Inflation

1 7% 7.0%

2 5 6.0 = (7 + 5)/2

Thus, the yield curve would be as follows:

b. The interest rate on the IBM bonds has the same components as the Treasury

securities, except that the IBM bonds have default risk, so a default risk premium must

be included. Therefore,

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

0

2

4

6

8

10

12

14

16

18

20

Years to maturity

Yield

(%)

T-Bonds

IBM

LILCO

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-8

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

For a strong company such as IBM, the default risk premium is virtually zero for

short-term bonds. However, as time to maturity increases, the probability of default,

although still small, is sufficient to warrant a default premium. Thus, the yield risk curve

for the IBM bonds will rise above the yield curve for the Treasury securities. In the graph,

the default risk premium was assumed to be 1.2 percentage points on the 20-year IBM

bonds. The return should equal 6.3% + 1.2% = 7.5%.

c. LILCO bonds would have significantly more default risk than either Treasury securities or

5-14 a. – c.

Arithmetic

1-Year Average Maturity Estimated

Expected Expected Risk Interest

Year Inflation Inflation r* Premium Rates

1 3% 3.0% 3% 0.0% 6.0%

2 5 4.0 3 0.2 7.2

3 4 4.0 3 0.4 7.4

e. Yield curve:

5-15 a. MRP for 10-year T-bond = 6.5% – 3.5% = 3.0%

5.0

5.5

8.5

9.0

0

2

4

6

8

10

12

14

16

18

20

Principles of Finance 6e Chapter 5

Besley/Brigham

5-9

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

MRP per year = 3.0%/10 = 0.3%

b. DRPNextel = 7.5% – (rRF + MRP) = 7.5% – [3.5 + 0.3%(6)] = 2.2%

c. r* = 3.5% – IP = 3.5% – 2.0% = 1.5%

5-16 a. Dollar return = $120

Yield = $120/$1,080 = 0.1111 = 11.11%

5-17 Term Rate

6 months 0.17%

1 year 0.26

The yield curve is as follows:

5-18 a. The average rate of inflation for the 5-year period is calculated as:

Yield (%)

Maturity

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-10

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

b. r5-yr = r* + IPAvg. = 2% + 4.8% = 6.8%.

c. Here is the general situation:

Arithmetic

One-Year Average Maturity Estimated

Expected Expected Risk Interest

Year Inflation Inflation r* Premium Rates

1 4% 4.00% 2% 0.1% 6.10%

2 5 4.50 2 0.2 6.70

3 7 5.33 2 0.3 7.63

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

0 2 4 6 8 10 12 14 16 18 20

Years to Maturity

Yield (%)

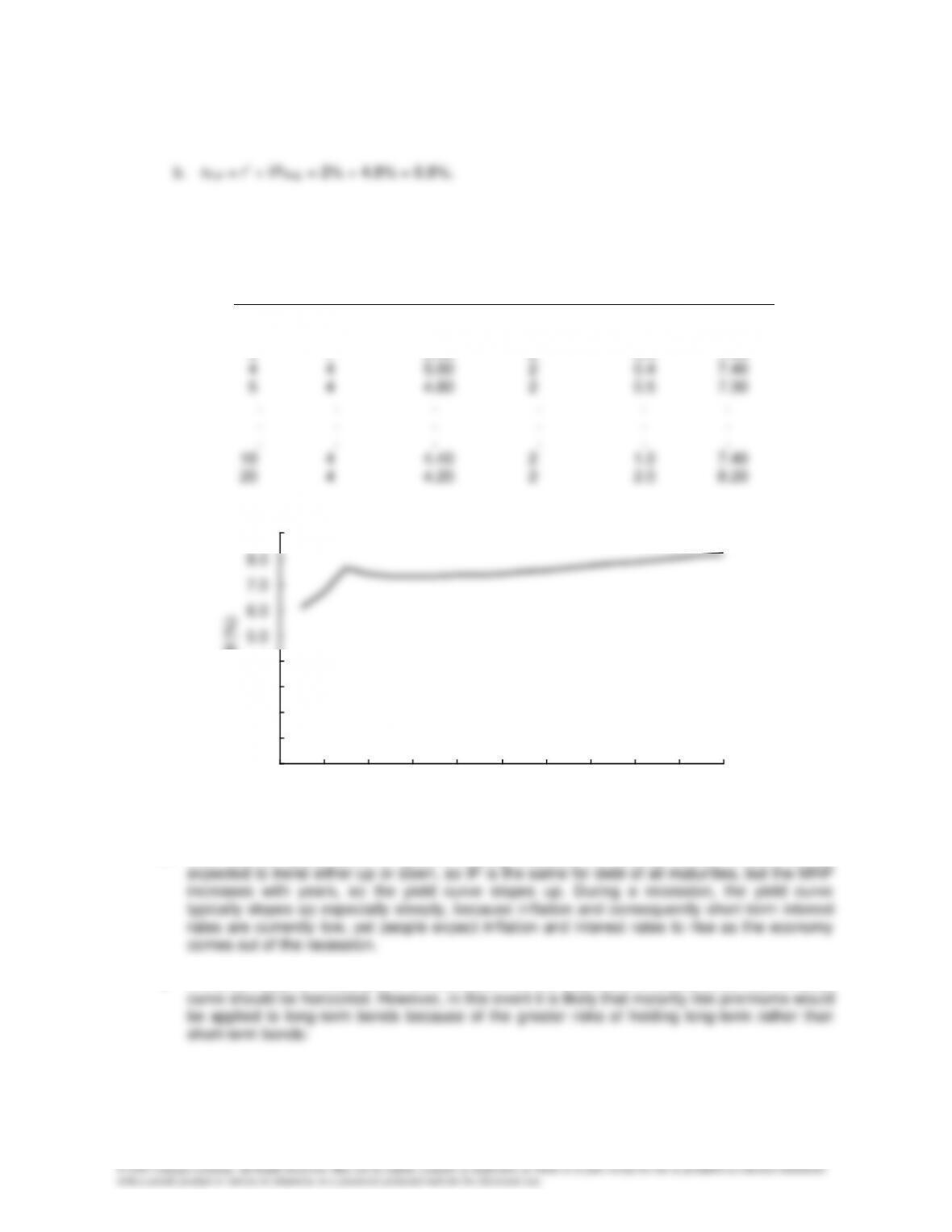

d. The “normal” yield curve is upward sloping because, in “normal” times, inflation is not

e. If inflation rates are expected to be constant, then the expectations theory holds that the yield

Principles of Finance 6e Chapter 5

Besley/Brigham

If maturity risk premiums were added to the yield curve in part e above, then the yield curve would be

more nearly normal—that is, the long-term end of the curve would be raised.

5-19 Integrative Problem

a. The dollar return is the amount in dollars that an investor would be paid if an investment is

liquidated at a particular period. For example, If you buy a stock for $40 today, you are paid

a $5 dividend during the year, and you sell the stock for $50 at the end of the year, the total

Return (Yield) = Dollar return

Original investment value

b. Total dollar return = ($240 – $250) + $25 = $15

c. The interest rate is the price paid for borrowed capital, while the return on equity capital

comes in the form of dividends plus capital gains. The return that investors require on

capital depends on (1) production opportunities, (2) time preferences for consumption, (3)

risk, and (4) inflation.

Pure expectations yield curve

Maturity risk

premium

Actual yield curve

Years to Maturity

Yield (%)

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-12

Risk, in a money and capital market context, refers to the chance that a loan will not be

repaid as promised—the higher the perceived default risk, the higher the required rate of

return.

d. Keep these equations in mind as we discuss interest rates. We will define the terms as we

go along:

r = r* + IP + DRP + LP + MRP.

rRF = r* + IP.

e. The inflation premium (IP) is a premium added to the real risk-free rate of interest to

compensate for expected inflation.

The default risk premium (DRP) is a premium based on the probability that the issuer will

default on the loan, and it is measured by the difference between the interest rate on a U.S.

Treasury bond and a corporate bond of equal maturity and marketability.

Principles of Finance 6e Chapter 5

Besley/Brigham

5-13

f. The term structure of interest rates is the relationship between interest rates, or yields, and

the maturities of securities. When this relationship is graphed, the resulting curve is called a

yield curve. The yield curve normally slopes upward, indicating that short-term interest

rates are lower than long-term interest rates.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Years to Maturity

Yield

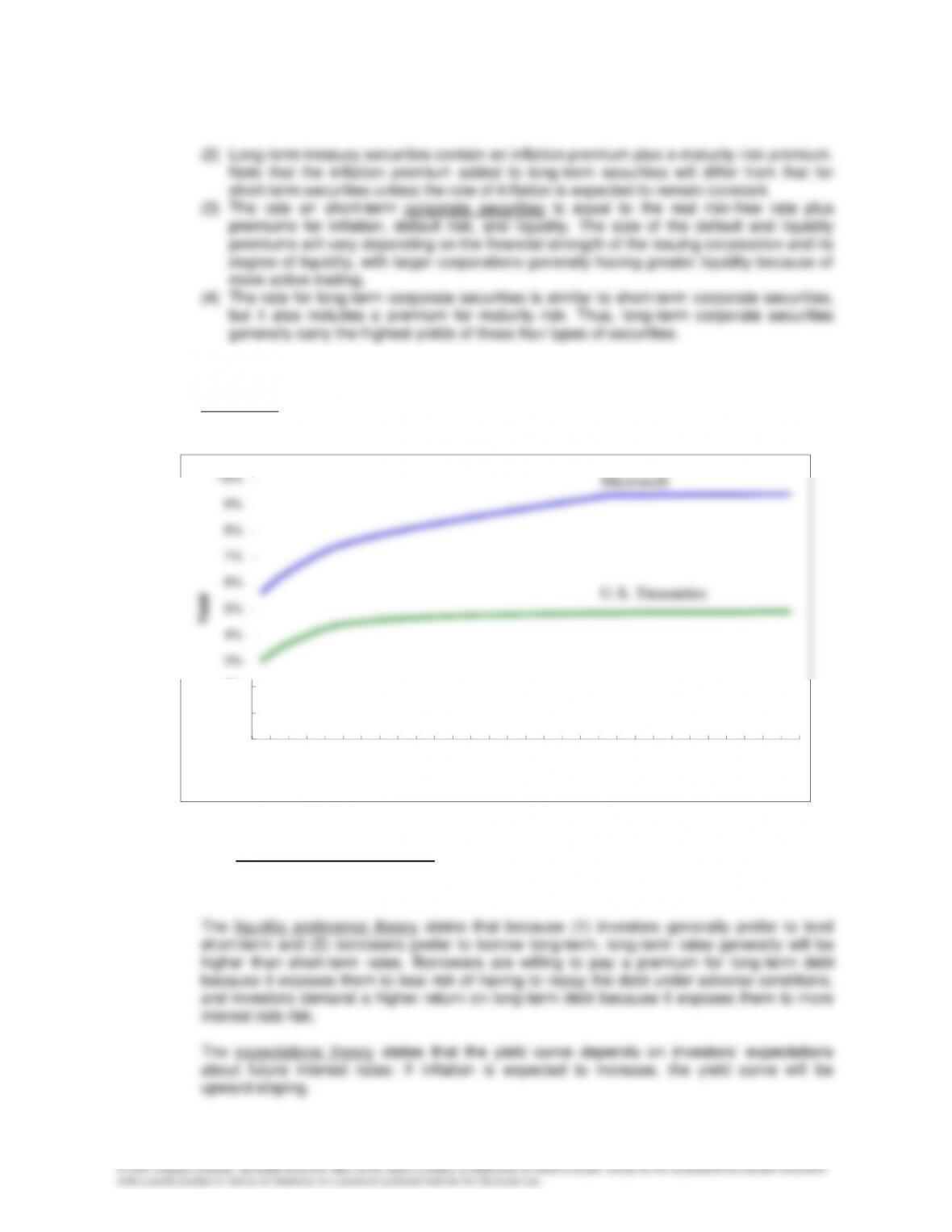

g. The market segmentation theory states that each borrower and lender has a preferred

maturity, and that the slope of the yield curve depends on the supply of and demand for

funds in the long-term market relative to the situation in the short-term market.

U.S. Treasuries

Microsoft

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-14

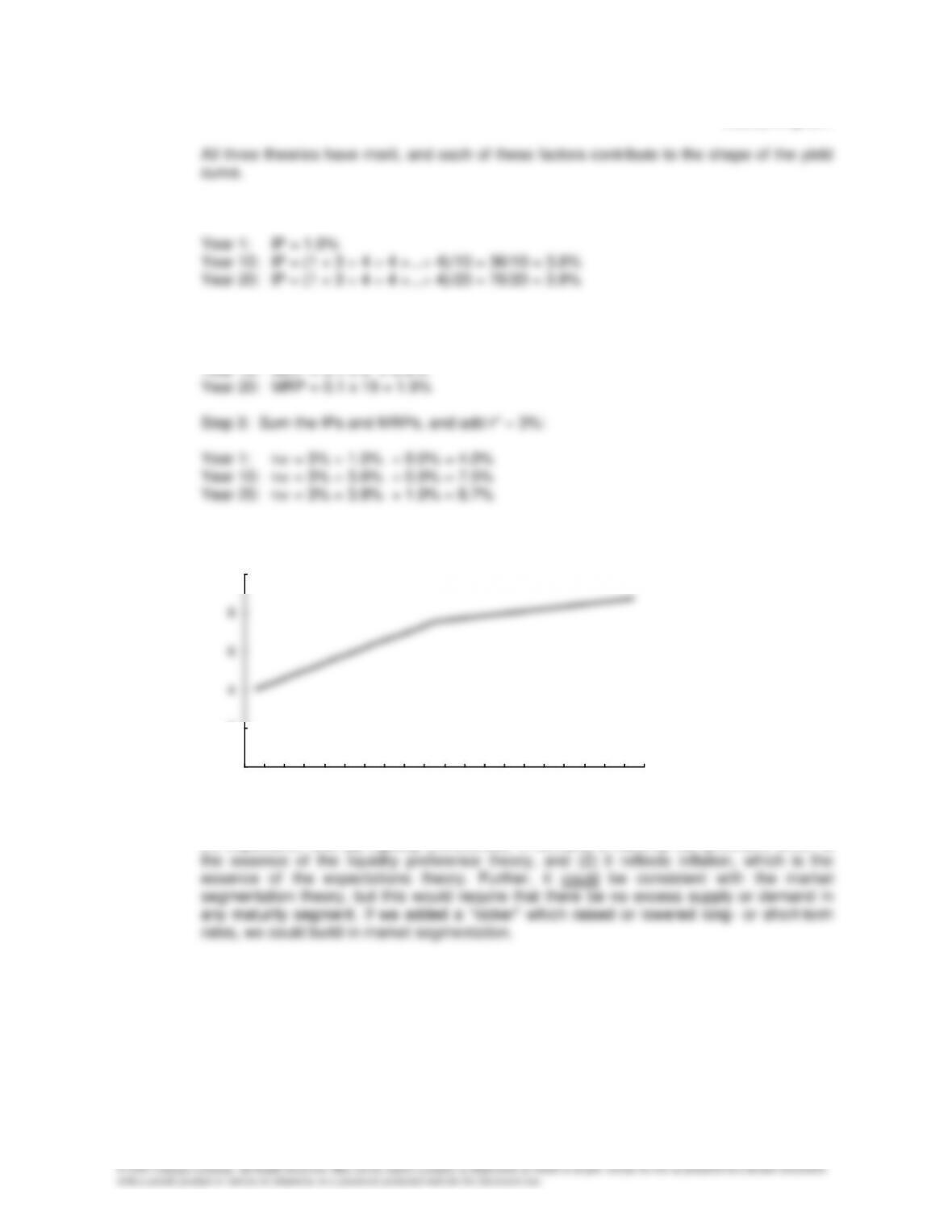

h. Step 1: find the average expected inflation rate over years 1 to 20:

Year 1: IP = 1.0%

Step 2: Find the maturity premium in each year:

Year 1: MRP = 0.0%

The yield curve is based directly on, hence is consistent with, at least two of the theories:

(1) expectation and (2) liquidity preferences. It contains a maturity risk premium, which is

Years to Maturity

Interest

(%)

0

2

4

6

8

10

1 6 11 16

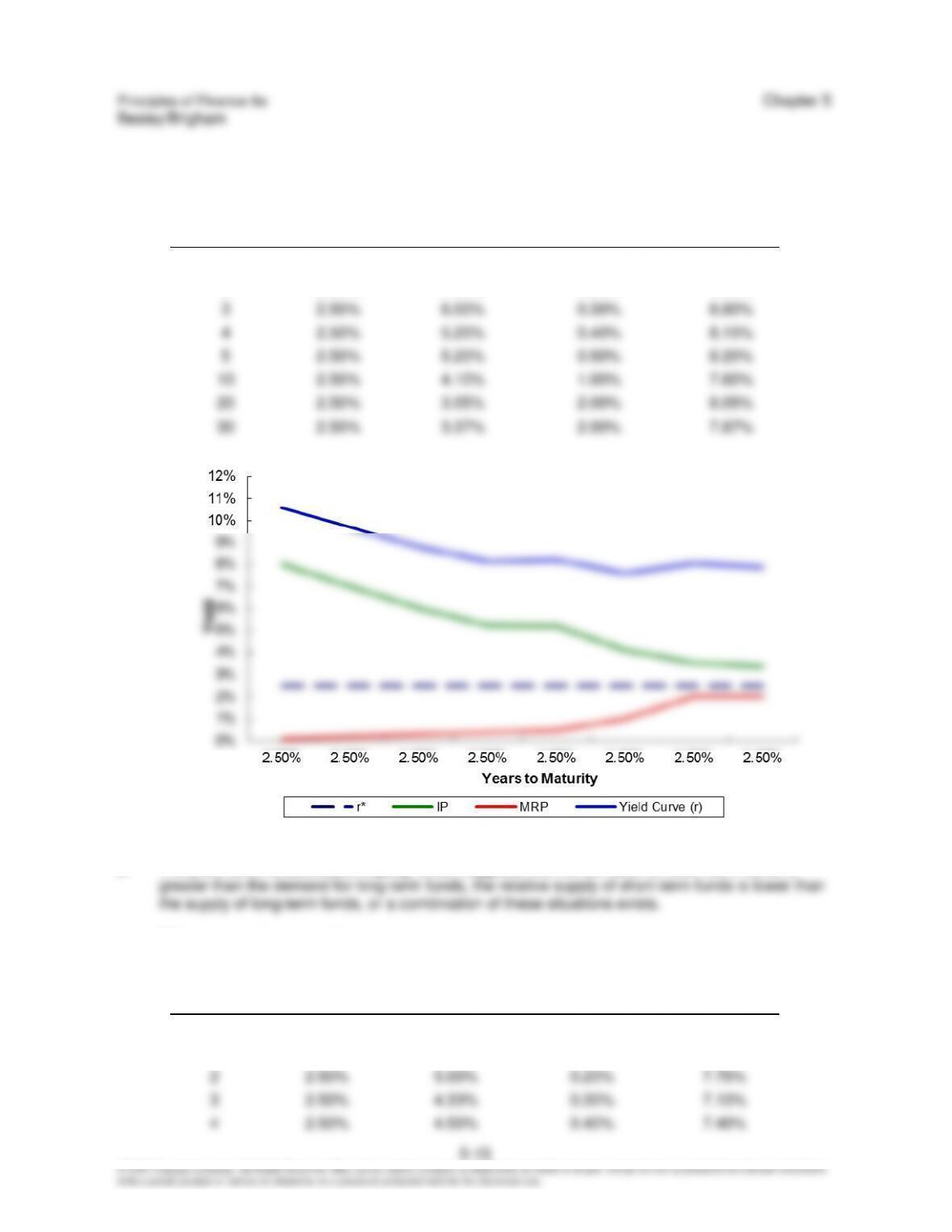

5-20 Computer-Related Problem

a.

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

1

2.50%

8.00%

0.10%

10.60%

2

2.50%

7.00%

0.20%

9.70%

3

2.50%

6.00%

0.30%

8.80%

4

2.50%

5.25%

0.40%

8.15%

5

2.50%

5.20%

0.50%

8.20%

10

2.50%

4.10%

1.00%

7.60%

20

2.50%

3.55%

2.00%

8.05%

30

2.50%

3.37%

2.00%

7.87%

b. The yield curve is downward sloping, which suggests that the demand for short-term funds is

c. After one year has passed:

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

0

1

2.50%

6.00%

0.10%

8.60%

2

2.50%

5.00%

0.20%

7.70%

3

2.50%

4.33%

0.30%

7.13%

4

2.50%

4.50%

0.40%

7.40%

Chapter 5 Principles of Finance 6e

Besley/Brigham

5-16

9

2.50%

3.67%

0.90%

7.07%

19

2.50%

3.32%

1.90%

7.72%

29

2.50%

3.21%

2.00%

7.71%

After two years have passed:

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

-1

0

1

2.50%

4.00%

0.10%

6.60%

2

2.50%

3.50%

0.20%

6.20%

3

2.50%

4.00%

0.30%

6.80%

8

2.50%

3.38%

0.80%

6.68%

18

2.50%

3.17%

1.80%

7.47%

28

2.50%

3.11%

2.00%

7.61%

After three years have passed:

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

-2

-1

0

1

2.50%

3.00%

0.10%

5.60%

2

2.50%

4.00%

0.20%

6.70%

7

2.50%

3.29%

0.70%

6.49%

17

2.50%

3.12%

1.70%

7.32%

27

2.50%

3.07%

2.00%

7.57%

After four years have passed:

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

-3

-2

-1

0

1

2.50%

5.00%

0.10%

7.60%

6

2.50%

3.33%

0.60%

6.43%

16

2.50%

3.13%

1.60%

7.23%

Principles of Finance 6e Chapter 5

Besley/Brigham

5-17

26

2.50%

3.08%

2.00%

7.58%

After five years have passed:

Years to

Real risk-free

Inflation

Maturity Risk

Treasury

Maturity

rate (r*)

Premium (IP)

Premium (MRP)

Yield

-4

-3

-2

-1

0

5

2.50%

3.00%

0.50%

6.00%

15

2.50%

3.00%

1.50%

7.00%

25

2.50%

3.00%

2.00%

7.50%

d. Yields on AAA-rated bonds and B-rated bonds:

Years to

Maturity

Real Risk-

Free Rate

Inflation

Premium (IP)

Maturity Risk

Premium

(MRP)

Treasury

Yield

AAA

Rating

DRP

AAA-

Rated

Bond

Yield

B-

Rating

DRP

B-Rated

Bond

Yield

1

2.50%

8.00%

0.10%

10.60%

1.50%

12.10%

4.00%

14.60%

2

2.50%

7.00%

0.20%

9.70%

1.53%

11.23%

4.08%

13.78%

3

2.50%

6.00%

0.30%

8.80%

1.56%

10.36%

4.16%

12.96%

4

2.50%

5.25%

0.40%

8.15%

1.59%

9.74%

4.24%

12.39%

5

2.50%

5.20%

0.50%

8.20%

1.62%

9.82%

4.33%

12.53%

10

2.50%

4.10%

1.00%

7.60%

1.79%

9.39%

4.78%

12.38%

20

2.50%

3.55%

2.00%

8.05%

2.19%

10.24%

5.83%

13.88%

30

2.50%

3.37%

2.00%

7.87%

2.66%

10.53%

7.10%

14.97%

ETHICAL DILEMMA

Unadvertised Special: Is It a “Shark”?

Ethical dilemma:

Skip Stephens is trying to decide whether it would be wise to consolidate his debt by borrowing funds

from Syndicated Lending, a firm that he doesn’t know much about. Syndicated is an Internet lender that

doesn’t post much information about the costs of the loans it offers. Some of the additional information

Skip has gathered from various sources suggests the Syndicated might use such unethical practices as

“bait and switch” to attract customers.

5-18

Discussion questions:

• Is there an ethical problem? If so, what is it?

In this case, the ethical situation would be the manner in which Syndicated conducts business.

• What are the implications if Skip borrows from Syndicated?

This is a tough question. Skip might end up paying much more for his debt if he borrows from

• Should Skip borrow from Syndicated?

Before he makes a decision, Skip should dig deeper to determine (estimate) the cost of borrowing

References:

The following articles might be assigned for background material:

James R. Hagerty, “Mortgage Brokers: Friends or Foes?” The Wall Street Journal Online, May 24, 2007.