Principles of Finance 6e Chapter 17

Besley/Brigham

17-1

CHAPTER 17

ANSWERS

17-1 Fundamental analysts evaluate a company’s financial statements and other information about the

17-2 Economic variable Type of indicator

a. New building permits leading

17-3 The Federal Reserve manages the money supply by affecting the reserves of banks through its

17-4 Economists who believe deficit spending artificially inflates prices and interest rates contend that

17-5 Industry Classification

a. Automobile manufacturing Cyclical

b. Debt collection services Defensive

17-2

17-6 Circumstance Life-cycle stage

a. Supplement retirement income Mature

Income would be more important than growth in value.

d. Prefer stocks with dividends and

high expected growth in the future Expansion

17-7 The dividend discount model is based on the principle that the value of the stock is simply the

present value of the cash flows investors expect to receive in the future. The cash flows generated

by a stock are in the form of dividends. When one investor sells a stock to another investor, he or

she is selling the right to receive the dividends paid by the company from that date on. This

17-3

17-8 Technical analysts try to determine when values will change by examining the supply/demand

17-9 The common factors include: (a) don’t flip flop with your investment decisions—be disciplined and

17–10 Even if the financial markets were strong form efficient, there still would be a need for investors to

───────────────────────────────────────────────

SOLUTIONS

17-1

gr

D

ˆ

P

s

1

0−

=

P

D

ˆ

rg

1

s

−=

17-2

1

0s

ˆ$2.20(1.05) $2.31

D

= = = = $21

P – g 0.16 – 0.05 0.11

r

17-3 a. Recognize that once the dividend payments begin, the cash flow stream represents a

perpetuity. Therefore,

Chapter 17 Principles of Finance 6e

Besley/Brigham

17-4

b.

11

10 s

ˆ

D$25 $25

P $250.00

r g 0.16 0.06 0.10

= = = =

−−

011 11

s

(1 r ) (1.16)

+

17-4 EVAAgribusiness = EBIT(1 – T) – (WACC x Invested capital)

17-5 a. EPS0 = $122.40/24 = $5.10

0

$122.40 $122.40

P

17-6 a. Net income = $65,000 = Taxable income(1 – T)

Taxable income = ($65,000)/(1 – 0.35) = $100,000

= EBIT – Interest

Principles of Finance 6e Chapter 17

17-5

17-7 a. D0 = $2.50

(1)

$16.67 =

0.15

$2.50

=

0.00 – 0.15

$2.50(1.0)

=

g – r

D

ˆ

=

P1

0

17-8 a. CAPM: rCFT = rRF + (rM – rRF)βCFT

b. (1) The dividends for the periods of nonconstant growth (i.e., the next eight years) are:

Year Growth Dividend PVIF18%,n PV of dividend

0 $ 2.4000 — —

1 30% 3.1200 0.84746 $ 2.6441

(2) Once CFT’s nonconstant growth ends, we can use the constant growth dividend discount

model to compute the price of the stock. Because nonconstant growth ends after Year 8,

we can apply the constant growth model as follows to compute P8:

(3) P0 = PV of dividends + PV of P8

Chapter 17 Principles of Finance 6e

17-6

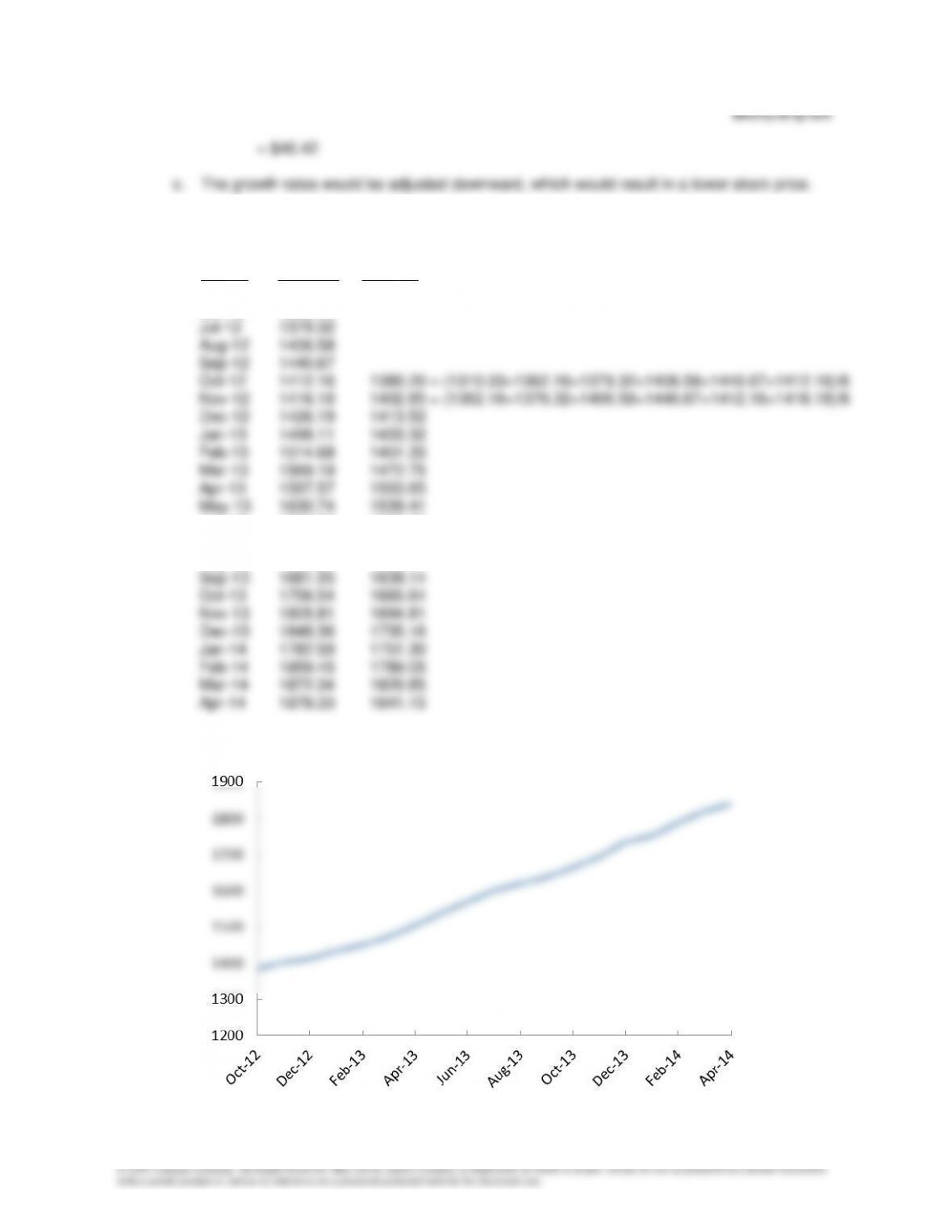

17-9 a. 6-month

moving

Month S&P 500 average

May–12 1310.33

Jun-12 1362.16

Jun-13 1606.28 1569.43

Jul-13 1685.73 1600.70

Aug-13 1632.97 1620.41

b. The general trend is upward.

Principles of Finance 6e Chapter 17

17-7

17–10 a. P/E = 20x = P0/EPS0

EPS0 = P0/20x = $70/20 = $3.50

d. P0 = EPS x P/E

17–11 a. WACCA = [14.0%(1 – 0.35)](0.80) + 26.0%(0.20) = 12.48%

b. EVA = EBIT(1 – T) – (WACC x Invested capital)

EVAA = $25,000(1 – 0.35) – (0.1248 x $100,000)

Chapter 17 Principles of Finance 6e

Besley/Brigham

c. EVAA > EVAB > EVAC; Thus, Firm A would be considered the best investment. The result

d. Firm A Firm B Firm C

EBIT $25,000 $25,000 $25,000

Interesta (11,200) ( 6,000) ( 2,000)

Taxable income 13,800 19,000 23,000

17–12 a. Net income = $1.2 million = Taxable income(1 – 0.40)

Taxable income = ($1.2 million)/(1 – 0.40) = $2.0 million

b. EVA = EBIT(1 – T) – (WACC x Invested capital)

17-13 a. D0 = $72,000/100,000 = $0.72

17-9

b.

$18.00– =

0.25 – 0.20

$0.90

=

g –

r

D

ˆ

=

Ps

1

0

17-14 Integrative Problem

a. Fundamental analysts examine information contained in financial statements, industry reports,

c. Investors try to forecast business cycles using a variety of methods; some are very quantitative,

others are not. In the chapter, we discuss two methods: (1) examining economic indicators and

d. The Federal Reserve implements the nation’s monetary policy through its open market

e. Industry analysis is important because (1) all industries do not perform the same during

business cycles and (2) future growth, thus risk, might be significantly different depending on

the stage of the life cycle in which the industry is operating. Some firms are members of

Chapter 17 Principles of Finance 6e

Besley/Brigham

17–10

f. When making investment decisions it is important to know and understand in what stage of the

life cycle an industry is operating. Everything else equal, investment risk differs significantly for

industries that are in the introductory stage compared to those that are in the mature stage. The

g. An investor examines the financial position of a firm primarily to form expectations about the

h. The valuation techniques discussed in the chapter are:

(1) Dividend discount models (DDM) apply the basic valuation principle—find the present

value of the future cash flows. The general format of a DDM is:

)

r + (1

P

ˆ

+

D

ˆ

+ … +

)

r + (1

D

ˆ

+

)

r + (1

D

ˆ

=

P

ˆN

s

NN

2

s

2

1

s

1

0

(2) P/E ratios can be used when it is felt that there generally exists a defined relationship

17–11

(3) Economic value added (EVA) considers whether the firm has generated funds sufficient to

i. (1) rs = 18.0%

Present

Year Growth Dividend PV if @ 18% Value

1 — $0.0000 0.8475 $0.0000

2 — 0.0000 0.7182 0.0000

16

15 sn

ˆ$17.4302(1.05) $18.3017

D

P – 0.18 – 0.05 0.13

g

r

0 15

15

ˆˆ

P = PV of dividends + PV of P

$140.7825

= $20.0628 + = $20.0628 + $11.7576 = $31.8204 $31.82

(1.18)

To solve for

0

P

ˆ

using the cash flow register on your computer, input CF0 = 0, and then

the dividends given in the above table for CF1 =

1

D

ˆ

, CF2 =

2

D

ˆ

, …, CF14 =

14

D

ˆ

,CF15 =

1515 P

ˆ

D

ˆ+

= $17.4302 + $140.7825 = $158.2127; input I = 18; and then compute the

NPV. The result is 31.8204.

(2) EBIT $110,000

Interest ( 17,600) = 0.08[$550,000(0.40)]

Chapter 17 Principles of Finance 6e

17–12

0

P

ˆ

= $1.5015 x 25 = $37.5375 ≈ $37.54

(3) EVA = EBIT(1 – T) – (WACC x Invested capital)

WACC = [8.0%(1 – 0.35)] x 0.40 + 18% x (1 – 0.40) = 12.88%

j. The results in part (i) differ because the computations are based on different assumptions.

k. It might be helpful to use a trend line or moving averages to determine the general tendency of

l. Table 17–4 can be summarized as follows:

(1) Be disciplined with your investment approach—give a particular strategy a chance to work;

m. Informational efficiency refers to how well the financial markets incorporate new information into

the prices of financial assets. The quicker prices adjust to new information, the more efficient

17–13

17-15 Computer-Related Problem

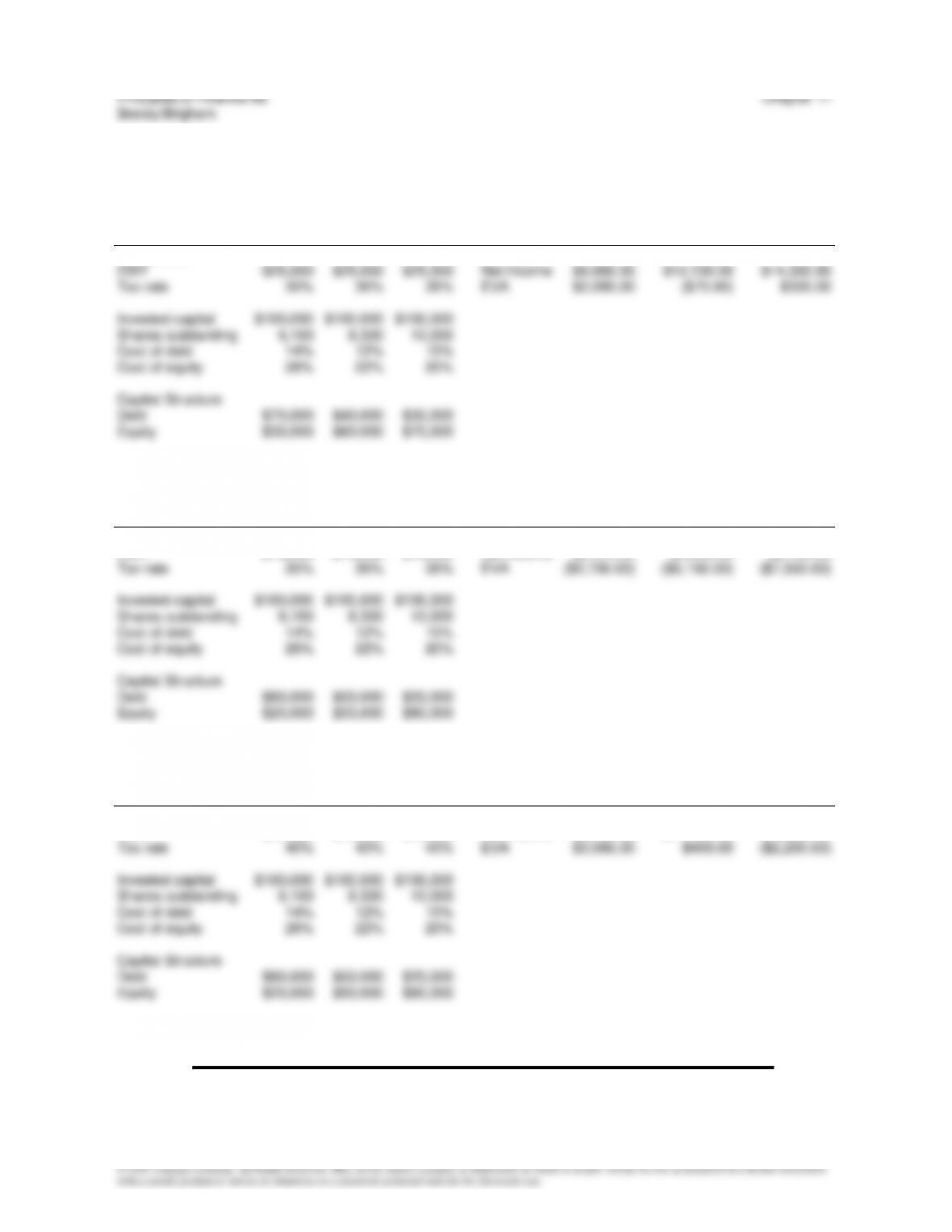

a. D/AA = 70%, D/AB = 40%, D/AC = 30%

INPUT DATA: KEY OUTPUT:

Firm A Firm B Firm C Firm A Firm B Firm C

Debt/assets 70% 40% 30% WACC 14.17% 16.32% 15.95%

b. EBIT = $15,000

INPUT DATA: KEY OUTPUT:

Firm A Firm B Firm C Firm A Firm B Firm C

Debt/assets 80% 50% 20% WACC 12.48% 14.90% 17.30%

EBIT $15,000 $15,000 $15,000 Net income $2,470.00 $5,850.00 $8,450.00

c. T = 40%

INPUT DATA: KEY OUTPUT:

Firm A Firm B Firm C Firm A Firm B Firm C

Debt/assets 80% 50% 20% WACC 11.92% 14.60% 17.20%

EBIT $25,000 $25,000 $25,000 Net income $8,280.00 $11,400.00 $13,800.00

Chapter 17 Principles of Finance 6e

Besley/Brigham

17–14

ETHICAL DILEMMA

Mary Mary Quite Contrary, What Makes Your Sales Forecasts Grow?

Ethical dilemma:

SMS is evaluating a new synthetic steel to determine whether the company should invest in its

producuion, and Mary is in charge of estimating the cash flows that the project will produce. Mary finds

herself in a situation that is not uncommon in business; her boss seems to think that SMS should invest in

the synthetic steel, and he told Mary that he doesn’t like her original cash flow estimates. As a result, Mary’s

boss asked her to reconsider her forecasts. Mary decided to change her numbers to accommodate the

boss, even though she believes that the growth rate needed to attain the revised cash flows is unrealistic. It

appears that when the revised cash flows are used in the final investment analysis, the project’s NPV and

IRR will indicate that SMS should invest in the synthetic steel production process. However, if SMS bases

its decision on “bad numbers” and invests the billions of dollars that are necessary, in the future it will

discover that the project actually should have been rejected. And, it is possible that this discovery will

come too late for the firm to correct its mistake, in which case the firm might find itself in serious financial

trouble.

Discussion questions:

• Is there an ethical problem? If so, what is it?

The question here is whether Mary should have changed her cash blow estimates just because her

• Was it appropriate for Mary’s boss do request that she change her cash flow estimates?

Mary’s boss is the investment officer, who is charged with making investment decisions. It is his

• Was it appropriate for Mary to change her cash flow estimates?

Mary must provide realistic cash flow estimates; otherwise SMS might make bad investments. If Mary

• What would do if you were Mary?

Perhaps the best solution is to provide the investment officer with two or three alternative scenarios,

Principles of Finance 6e Chapter 17

Besley/Brigham

17–15

References:

Many articles appear in business publications, such as The Wall Street Journal, BusinessWeek, and

Fortune, Forbes, to name a few, that relate to the topic of this Ethical Dilemma.

Shawn Tully, “The (Second) Worst Deal Ever,” Fortune, October 16, 2006, 102-119.

Colin Barr, “Lehman’s Costly Bad Bank Plan,” Fortune (online), September 4, 2008,

http://dailybriefing.blogs.fortune.cnn.com/2008/09/04/lehmans-costly-bad-bank-plan/