Chapter 14 Principles of Finance 6e

Besley/Brigham

14–20

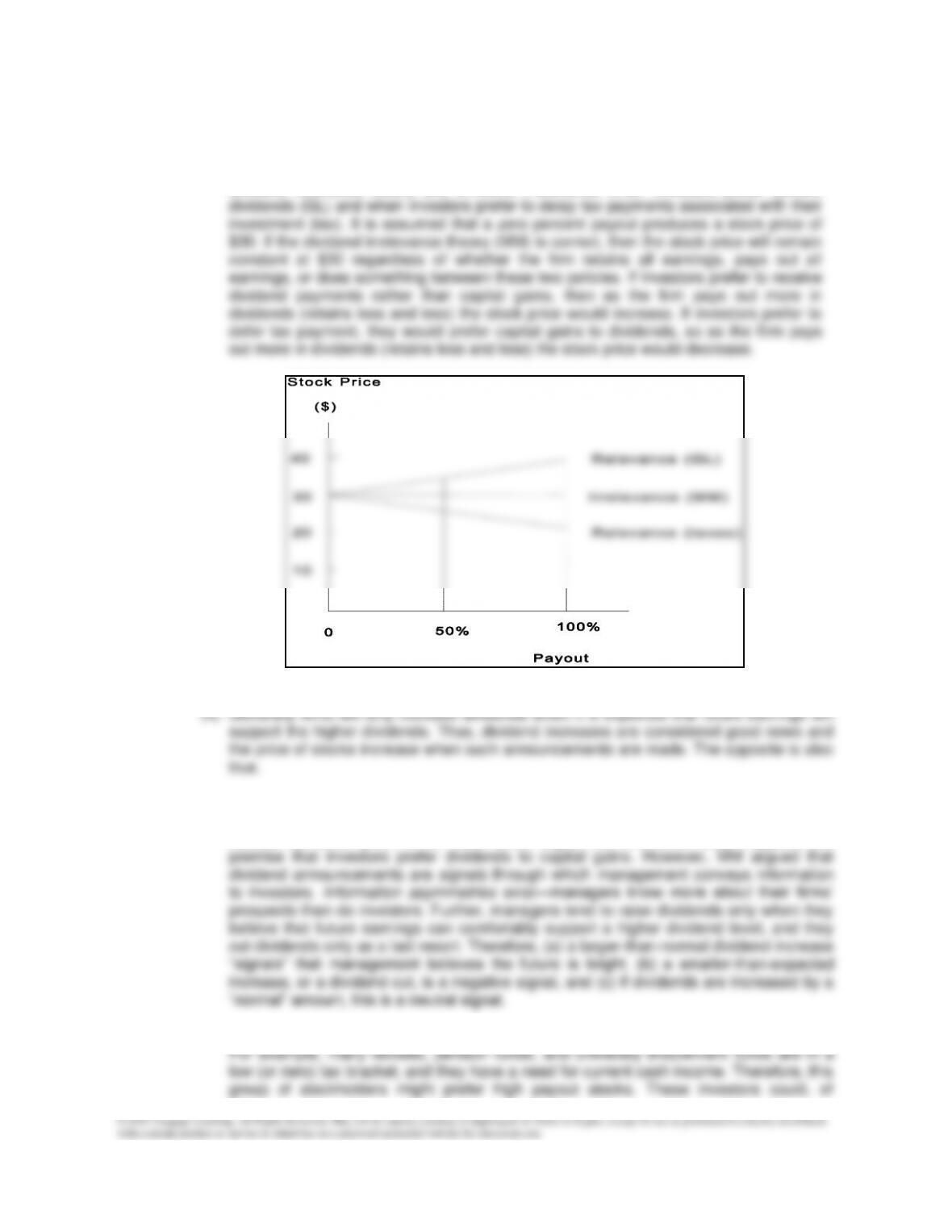

(3) In the graph given here, we plot stock price versus dividend policy (payout) under the

dividend relevance theory and dividend irrelevance when investors prefer current

b. (1) It has long been recognized that the announcement of a dividend increase often results

in an increase in the stock price, whereas an announcement of a dividend cut typically

causes the stock price to fall. One could argue that this observation supports the

(2) Different groups, or clienteles, of stockholders prefer different dividend payout policies.

Principles of Finance 6e Chapter 14

4-21

(3) Investors expect financial managers to make decisions that help maximize the value of

the firm. If positive net present value capital budgeting projects are available for current

investment, the firm should invest in these projects. Thus, if investors want wealth

c. (1) Draw the WACC graph assuming no dividends are paid. The graph shows that the

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–22

Given the optimal capital budget and the target capital structure, we must now

0.4($800,000) = $320,000 must be raised as debt if we are to maintain the optimal

capital structure:

If a residual exists, that is, if net income exceeds the amount of equity the company

needs, then it should pay the residual amount out in dividends. Because $600,000 of

However, if it were applied exactly, the residual policy would result in dividend

payments that fluctuated significantly from year to year as capital requirements and

1,000

Cost of Capital

(%)

CAPITAL RAISED

(THOUSANDS $)

800

IOS

0

Principles of Finance 6e Chapter 14

Besley/Brigham

4-23

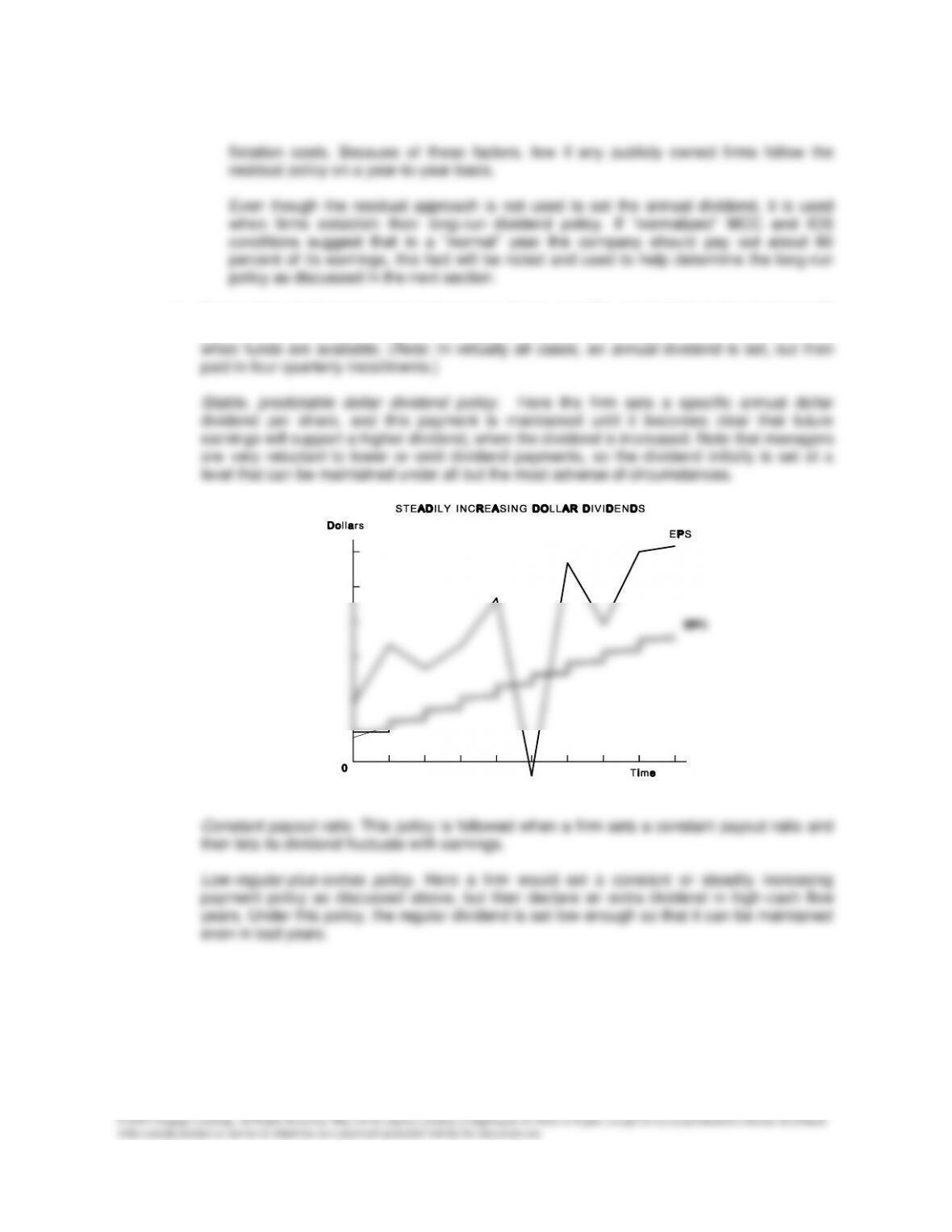

d. Three other dividend payment policies are (1) pay a stable, predictable dollar dividend, (2)

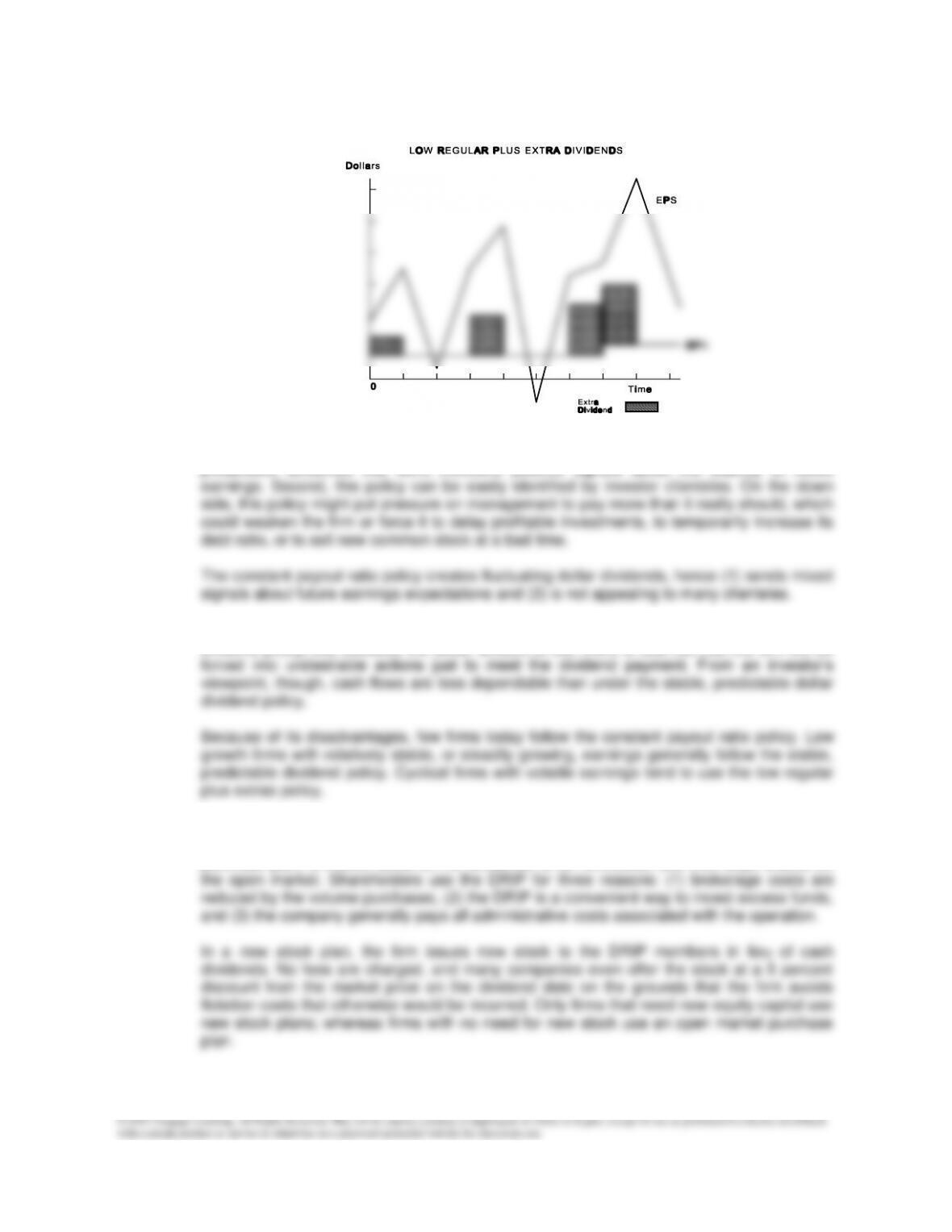

pay out a constant percentage of earnings, and (3) pay a low regular dividend plus an extra

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–24

The stable, predictable dollar policy has two advantages. First, it provides stable,

predictable dividends that send investors positive signals about the stability of future

The low regular plus extras policy has advantages similar to the stable, predictable dollar

dividend policy, but, because the dollar amount is low, there is less risk that the firm will be

e. Under a dividend reinvestment plan (DRIP), shareholders have the option of automatically

reinvesting their dividends in shares of the firm’s common stock. In an open market

purchase plan, a trustee pools all the dividends to be reinvested and then buys shares on

4-25

14-18 Computer-Related Problem

a. If the outstanding debt has to be refunded at the new higher interest rate, expected EPS

would decline under either financing plan. However, EPS would decline more if debt

financing were used. Therefore, debt financing has become relatively less attractive than

stock financing. The output generated by the model is:

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $60 Expected EPS $5.60

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Accounts payable: $172.50

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Chapter 14 Principles of Finance 6e

Besley/Brigham

Sales $2,250 $2,700 $3,150

ANALYSIS IF STOCK FINANCING IS USED:

Sales $2,250 $2,700 $3,150

EBIT 225 270 315

b. We can see from the output given below that the lower the interest rate, the better debt

financing looks. At a long-term interest rate of 5 percent, the expected EPS is significantly

LONG-TERM INTEREST RATE = 5 PERCENT

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $60 Expected EPS $6.80

© 2015 South-Western/Cengage Learning

14–27

Annual Sales Prob.

$2,250 0.30 Using Equity financing:

Amount financed $270

Tax rate 40%

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Sales $2,250 $2,700 $3,150

Expected EPS,

using debt: $6.80 Std. Dev. of EPS: $1.05

Chapter 14 Principles of Finance 6e

14–28

EBIT 225 270 315

Interest on S-T debt (15) (15) (15)

Interest on L-T debt (15) (15) (15)

EBT $ 195 $ 240 $ 285

Taxes (78) (96) (114)

Net income $ 117 $ 144 $ 171

EPS $ 4.78 $ 5.88 $ 6.98

TIE 7.50 9.00 10.50

Expected EPS,

using stock: $ 5.88 Std. Dev. of EPS: $0.85

Expected TIE 9.00

LONG-TERM INTEREST RATE = 20 PERCENT

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $60 Expected EPS $4.23

Standard Deviation 1.05

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Accounts payable: $172.50

© 2015 South-Western/Cengage Learning

14–29

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Sales $2,250 $2,700 $3,150

ANALYSIS IF STOCK FINANCING IS USED:

Sales $2,250 $2,700 $3,150

EBIT 225 270 315

c. This analysis shows that at the higher stock price, equity financing looks better. At very high

STOCK PRICE = $105:

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

14–30

Debt ratio 75.46%

Annual Sales Prob.

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Initial income statement data:

Sales $2,475.00

EBIT $247.50

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Sales $2,250 $2,700 $3,150

ANALYSIS IF STOCK FINANCING IS USED:

© 2015 South-Western/Cengage Learning

14–31

Sales $2,250 $2,700 $3,150

EBIT 225 270 315

STOCK PRICE = $30:

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $30 Expected EPS $5.60

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Accounts payable: $172.50

14–32

Taxes $81.00

Net income $ 121.50

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Sales $2,250 $2,700 $3,150

ANALYSIS IF STOCK FINANCING IS USED:

Sales $2,250 $2,700 $3,150

EBIT 225 270 315

Interest on S-T debt (15) (15) (15)

d. These results indicate that debt financing is relatively better than equity financing if the

SALES LEVEL KNOWN WITH CERTAINTY

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $60 Expected EPS $5.60

© 2015 South-Western/Cengage Learning

14–33

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Accounts payable: $172.50

Initial income statement data:

Sales $2,475.00

EBIT $247.50

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.0 1.0 0.0

Sales $2,250 $2,700 $3,150

ANALYSIS IF STOCK FINANCING IS USED:

14–34

Sales $2,250 $2,700 $3,150

EBIT 225 270 315

SALES LEVEL UNCERTAIN

INPUT DATA: KEY OUTPUT:

Financing alternatives: Using Debt financing:

Stock – Price per share $60 Expected EPS $7.49

Standard Deviation 8.85

Initial balance sheet data:

Current assets: $900.00

Net fixed assets: $450.00

Accounts payable: $172.50

© 2015 South-Western/Cengage Learning

14–35

MODEL-GENERATED DATA:

ANALYSIS IF DEBT FINANCING IS USED:

Probability 0.3 0.4 0.3

Sales $0 $2,700 $7,500

ANALYSIS IF STOCK FINANCING IS USED:

Sales $0 $2,700 $7,500

EBIT 0 270 750

14–19 a. With the proposed increase in the debt ratio, the marginal cost of capital before the break

INPUT DATA: KEY OUTPUTS:

Previous dividend: $3.00 Expected payout: 63.16%

14–36

Debt ratio: 60.00%

Cost of new debt: 12.00% Optimal capital budget:

Net price new stock $51.25 Project IRR Cost

Investment:

Project Cost IRR Cum. Cost

MODEL-GENERATED DATA:

With proposed dividend:

Earnings 14,250,000

Marginal cost of capital up to break point:

After-Tax Weighted

Component Percent Cost Cost

After-Tax Weighted

Component Percent Cost Cost

Capital cost:

Range of financing Capital cost

Optimal capital budget:

Project IRR Cost

b. If rs rose to 16 percent, the MCC above the break would rise to 10.93 percent, which would

Principles of Finance 6e Chapter 14

© 2015 South-Western/Cengage Learning

14–37

INPUT DATA: KEY OUTPUTS:

Previous dividend: $3.00 Expected payout: 63.16%

c. No, the project selection would not be affected by a change in the dividend. The low return

INPUT DATA: KEY OUTPUTS:

Previous dividend: $3.00 Expected payout: 39.58%

Proposed dividend: $1.88 WACC before break: 10.72%

ETHICAL DILEMMA

A Bond Is a Bond … Is a Stock … Is a Bondock?

Ethical dilemma:

Wally is evaluating whether to use a new (to the United States) financial instrument to raise funds to

finance Ohio Rubber & Tire’s (ORT) expansion plans. The new instrument, which is called a bondock,

has some characteristics of traditional debt and some characteristics that are similar to common equity.

The cost of capital associated with bondocks is slightly higher than traditional debt, but significantly

lower than common equity. If ORT’s expansion plans are successful, both its bondholders and its

stockholders will receive handsome returns. However, if the expansion plans are not successful, then it

appears that stockholders can still benefit but at the expense of bondholders. ORT’s executives are

some of the company’s major stockholders, so it appears that they would be in favor of issuing

bondocks.

Discussion questions:

Chapter 14 Principles of Finance 6e

© 2015 South-Western/Cengage Learning

14–38

• Is there an ethical problem? If so, what is it?

The question here is whether it is appropriate to use a new financial instrument called a bondock to

raise funds needed for expansion. Because the cost of capital associated with a bondock is slightly

• Is it appropriate for ORT to use bondocks to raise funds that are needed for expansion?

Is there an ethical dilemma here? Maybe not. Remember that investors take risks when purchasing

• What would you do if you were Wally?

It seems that the best solution is for Wally to try to get more information about the new financial

References:

The following articles might be assigned for background material:

Emily Thornton, “Gluttons at the Gate,” BusinessWeek, October 30, 2006, pp. 58-66.

David Henry, “Cross–Dressing Securities,” BusinessWeek, March 13, 2006, pp. 58-59.