Principles of Finance 6e Chapter 14

Besley/Brigham

4-1

CHAPTER 14

ANSWERS

14-1 If sales tend to fluctuate widely, then cash flows and the ability to service fixed charges also will

14-2 The tax benefits from debt increase linearly, which causes a continuous increase in the firm’s

14-3 Expected EPS generally is measured as EPS for the coming years, and we typically do not

14-4 EBIT depends on sales and operating costs that generally are not affected by the firm’s use of

14-7 With increased competition after the breakup of AT&T, the new AT&T and the seven Bell

operating companies’ business risk increased. With this component of total company risk

14-8 Several possibilities exist for the firm, but trying to match the length of the project with the

maturity of the financing plan seems to be the best approach. The firm might want to finance the

Chapter 14 Principles of Finance 6e

14-2

14-9 The way this question is worded, the decision would have to be made on an individual basis. In

our opinion, investors who intend to invest in companies that maintain a relatively high payout

probably are seeking income and would prefer to receive a stable, or predictably increasing,

14–10 a. From the stockholders’ point of view, if the capital gains tax rate stays constant, an increase

in the personal income tax rate would make it more desirable for a firm to retain and

reinvest earnings. Consequently, an increase in personal tax rates should lower the

aggregate payout ratio.

14–11 While it is true that the cost of outside equity is higher than that of retained earnings, it is not

14–12 Logic suggests that stockholders like stable dividends—many of them depend on dividend

Principles of Finance 6e Chapter 14

4-3

14–13 a. The residual dividend policy is based on the premise that, because new common stock is

more costly than retained earnings, a firm should use all the retained earnings it can to

14-14 The difference is largely one of accounting. In the case of a split, the firm simply increases the

number of shares and simultaneously reduces the par or stated value per share. In the case of

14–15 If outside investors have the same information as the executives who run the company, then

14–16 If investors do not have the same information as the executives who run the company and the

SOLUTIONS

14-1 a. LL: D/TA = 30%; Debt = 0.3($20 million) = $6 million

EBIT $4,000,000

Chapter 14 Principles of Finance 6e

Besley/Brigham

14-4

b. LL: D/TA = 60%; debt = 0.6($20 million) = $12 million

EBIT $4,000,000

14-2 Equity financing = 0.5($120,000) = $60,000

14-3 Retention ratio = $400,000/$1,000,000 = 0.40 = 40.0%

14-4 Dividend payout ratio = $6,000,000/$15,000,000 = 0.4 = 40.0%

14-5 a. Price = $3 x 3.0 = $9

Principles of Finance 6e Chapter 14

Besley/Brigham

4-5

14-6 DPS after split = $0.75.

14-7 Retained earnings = Net income (1 – Payout ratio) = $5,000,000(0.55) = $2,750,000

External equity needed:

14-8 Equity financing = $12,000,000(0.60) = $7,200,000

14-9 Break point if all earnings retained = NI/Equity ratio = $7,287,500/0.5 = $14,575,000

10

14

18

%

15

5

10

20

$

A

B

C

WACC2

WACC1

Optimal Capital Budget

Chapter 14 Principles of Finance 6e

Besley/Brigham

14-6

14-10 No leverage: D = 0 (debt); E = $14,000,000 (equity)

Net Income = ROE =

State Pr EBIT (EBIT – rdD)(1 – T) NI/S Pr x (ROE) Pr(ROE –

ROE

)2

1 0.2 $4,200,000 $2,520,000 0.18 0.036 0.00113

Net Income = ROE =

State Pr EBIT (EBIT – rdD)(1 – T) NI/S Pr x (ROE) Pr(ROE –

ROE

)2

1 0.2 $4,200,000 $2,444,400 0.194 0.039 0.00138

Net Income = ROE =

State Pr EBIT (EBIT – rdD)(1 – T) NI/S Pr x (ROE) Pr(ROE –

ROE

)2

1 0.2 $4,200,000 $2,058,000 0.294 0.059 0.00450

Principles of Finance 6e Chapter 14

Besley/Brigham

4-7

Net Income = ROE =

State Pr EBIT (EBIT – rdD)(1 – T) NI/S Pr x (ROE) Pr(ROE –

ROE

)2

1 0.2 $4,200,000 $1,814,400 0.324 0.065 0.00699

14–11 a. Expected EPS for Firm C:

b. According to the standard deviations of EPS, Firm B is the least risky, while Firm C is the

riskiest. However, this analysis does not take account of portfolio effects—if Firm C’s

earnings go up when most other companies’ decline (that is, its beta is low), its apparent

riskiness would be reduced when combined with other assets. Also, standard deviation is

related to size, or scale, and to correct for scale we could calculate a coefficient of variation

(σ/mean):

E(EPS) σ CV = σ/E(EPS)

A $5.10 $3.61 0.71

14–12 a. Without new investment

Sales $12,960,000 = $288 × 45,000 units

1. EPSOld = $489,600/240,000 = $2.04.

Chapter 14 Principles of Finance 6e

Besley/Brigham

With new investment Debt Stock

Sales $12,960,000 $12,960,000

b.

Shares

)T1](IF)VP(Q[

EPS −−−−

=

33.181$

000,45

000,160,8$

V==

000,240

)4.01](000,104,1$000,800,1$Q)33.181$00.288[($

EPSDebt

−−−−

=

Principles of Finance 6e Chapter 14

Besley/Brigham

4-9

c. VOld = $10,200,000/45,000 = $226.67

units 475,20Q

=

d. At the expected sales level, 45,000 units, we have these EPS values:

EPSOld Setup = $2.04.

000,240

60.0$

000,480

)4.01](000,384$000,800,1$000,25)33.181$00.288[($

EPSStock =

−−−−

=

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–10

14–13 Use of debt ($ millions):

Probability 0.3 0.4 0.3

Sales $2,250.0 $2,700.0 $3,150.0

Use of stock (Millions of dollars):

Probability 0.3 0.4 0.3

Sales $2,250.0 $2,700.0 $3,150.0

Principles of Finance 6e Chapter 14

Besley/Brigham

4-11

14–14 a. 1. 2016 Dividends = (1.10)(2015 Dividends) = (1.10)($3,600,000) = $3,960,000

3. Equity financing = $8,400,000(0.60) = $5,040,000.

4. The regular dividends would be 10 percent above the 2015 dividends:

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–12

b. Policy 4, based on the regular dividend with an extra, seems most logical. Implemented

14–15 a. Payout = ($3.00 x 3,000,000)/($14,250,000) = 63.16%.

With a $3.00 dividend:

million 55.9$

55.0

million 25.5$

BPRE ==

Marginal cost up to $9.55 million:

After-Tax Weighted

Component Percent Cost Cost

Debt 0.45 0.0660 0.0297

Marginal cost above $9.55 million:

After-Tax Weighted

Component Percent Cost Cost

Debt 0.45 0.0660 0.0297

$51.25

With no dividend:

Principles of Finance 6e Chapter 14

4-13

million 25.14$

b. Ybor’s capital budget should be $15 million, because only the growth project’s return

exceeds the marginal cost of capital.

c. Ybor’s management should expect that its intended policy of moving into new growth fields

will open up better investment opportunities, which presumably will require more funds than

Assuming the $3.00 dividend, financing should be as follows:

Capital budget: $15,000,000

New debt = 0.45($15,000,000): (6,750,000)

d. Generally, new areas of business involve greater-than-average risk as well as greater-than-

average expected returns. The new growth aspects of Ybor City Tobacco might cause

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–14

Principles of Finance 6e Chapter 14

Besley/Brigham

4-15

(2) Conclusions from the analysis:

(i) Firm L has the higher expected ROE:

(ii) Firm L has a wider range of ROEs, and a higher standard deviation of ROE,

indicating that its higher expected return is accompanied by higher risk. To be

precise:

(iv) Leverage will boost expected ROE if the expected unlevered ROA exceeds the

d. (1) The optimal capital structure is the capital structure at which the tax-related benefits of

(2) Here is the sequence of events:

Chapter 14 Principles of Finance 6e

Besley/Brigham

14–16

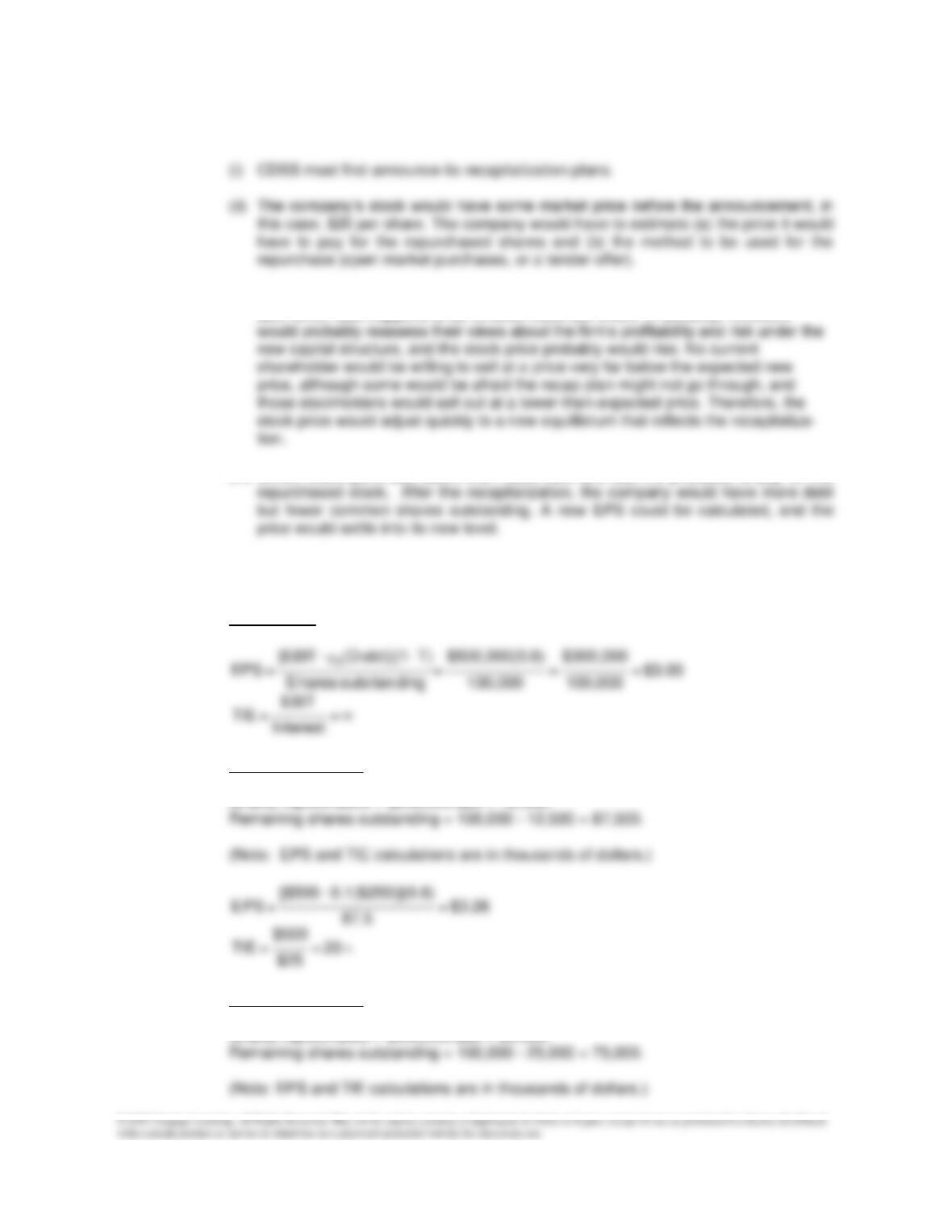

(iii) For simplicity, we assume that the firm could repurchase stock at its current price,

$20, which also happens to be its book value per share. In actuality, investors

(iv) CDSS would purchase stock, then issue debt and use the proceeds to pay for the

(3) The analysis for the debt levels being considered (in thousands of dollars and shares) is

shown below:

At Debt = $0:

=

nterestI

EBIT

= TIE

At Debt = $250,000:

Shares repurchased = $250,000/$20 = 12,500.

20 =

$25

$500

= TIE

At Debt = $500,000:

Shares repurchased = $500,000/$20 = 25,000.

4-17

5.1 =

$97.5

$500

= TIE

At Debt = $1,000,000:

Shares repurchased = $1,000,000/$20 = 50,000.

3.1 =

$160

$500

= TIE

(4) We can calculate the price of a constant growth stock as DPS divided by rs minus g,

where g is the expected growth rate in dividends:

Because in this case all earnings are paid out to the stockholders, DPS = EPS. Further,

because no earnings are plowed back, the firm’s EBIT is not expected to grow, so g =

0. Here are the results:

Debt Level DPS rs Stock Price

$ 0 $3.00 15.0% $20.00

14–18

(7) Currently, Debt/Total assets = 0%, so total assets = initial equity = $20 x 100,000

shares = $2,000,000.

e. If the firm had higher business risk, then, at any debt level, its probability of financial

f. Because it is difficult to quantify the capital structure decision, managers consider the

following judgmental factors when making capital structure decisions:

(1) The average debt ratio for firms in their industry.

g. The asymmetric information concept is based on the premise that management’s choice of

financing gives signals to investors. Firms with good investment opportunities will not want

h. When it uses a stock dividend, a firm issues new shares in lieu of paying a cash dividend.

For example, in a 5 percent stock dividend, the holder of 100 shares would receive an

Principles of Finance 6e Chapter 14

Besley/Brigham

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed

with a certain product or service or otherwise on a password-protected website for classroom use.

4-19

Both stock dividends and stock splits increase the number of shares outstanding and, in

effect, cut the pie into more, but smaller, pieces. If the dividend or split does not occur at the

same time as some other event that would alter perceptions about future cash flows, such

as an announcement of higher earnings, then one would expect the price of the stock to

adjust such that each investor’s wealth remains unchanged. For example, a 2–for-1 split of a

stock selling for $50 would result in the stock price being cut in half, to $25.

It is hard to come up with a convincing rationale for small stock dividends, like 5 percent or

10 percent. No economic value is being created or distributed, yet stockholders have to

bear the administrative costs of the distribution. Further, it is inconvenient to own an odd

number of shares as can result after a small stock dividend. Thus, most companies today

avoid small stock dividends.

On the other hand, there is a good reason for stock splits or large stock dividends.

Specifically, there is a widespread belief that an optimal price range exists for stocks. The

argument goes as follows: if a stock sells for about $20-$80, then it can be purchased in

14-17 Integrative Problem

a. (1) Dividend policy is defined as the firm’s policy with regard to paying out earnings as

(2) Dividend irrelevance refers to the theory that investors are indifferent between

dividends and capital gains, making dividend policy irrelevant with regard to its effect

on the value of the firm. On the other hand, according to the dividend relevance