Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13 Principles of Finance 6e

Besley/Brigham

g. (1) The net present value (NPV) is simply the sum of the present values of a project’s cash

flows:

( )

n

t

t

t0

ˆ

CF

1r

=

We refer to the completed cash flow time line and explain how each of the indicators is

calculated. We base our explanation on financial calculators, but it would be equally easy

to explain using a regular calculator. The cash flow time line and the NPV computation are:

(2) The rationale behind the NPV method is straightforward: If a project has NPV = $0, then

the project generates exactly enough cash flows (1) to recover the cost of the investment

h. (1) The internal rate of return (IRR) is the discount rate that forces the NPV of a project to

equal zero; it is the rate of return the project is expected to generate:

(260.00) 79.7 91.2 62.4 89.7

72.45

75.37

46.88

61.27

( 4.03)

0 1 2 3 4

10%

Principles of Finance 6e Chapter 13

Besley/Brigham

Expressed as an equation, we have:

( )

=

+

0t t

IRR1

Note that the IRR equation is the same as the NPV equation, except that to find the

IRR, the equation is solved for the particular discount rate that forces the project’s NPV

to equal zero (the IRR) rather than using the cost of capital (k) in the denominator and

(2) The IRR is to a capital project what the YTM is to a bond—it is the expected rate of return

on the project, just as the YTM is the promised rate of return on a bond.

(3) IRR measures a project’s profitability in the rate of return sense: If a project’s IRR equals

its required rate of return, then its cash flows are just sufficient to provide investors with

(4) The IRR is independent of the required rate of return. Therefore, the IRR would not change

(260.00) 79.7 91.2 62.4 89.7

PV of CF1

PV of CF2

PV of CF3

PV of CF4

NPV= 0

0 1 2 3 4

IRR

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-38

i. (1) The MIRR is the rate of return that equates a project’s terminal value to the present value

of its cash outflows. Cash inflows are compounded to the end of the project’s life at the

firm’s required rate of return, cash outflows are discounted at the firm’s required rate of

return, and then the rate at which these two value are equal is the MIRR. To compute the

MIRR, solve this equation:

n

n

)MIRR1(

TV

+

=

outflows cash of PV

(2) The modified IRR has a significant advantage over the traditional IRR measure. MIRR

assumes that cash flows are reinvested at the required rate of return, whereas the

(3) The cash outflows are discounted at the firm’s required rate of return, and the cash

Principles of Finance 6e Chapter 13

Besley/Brigham

13-39

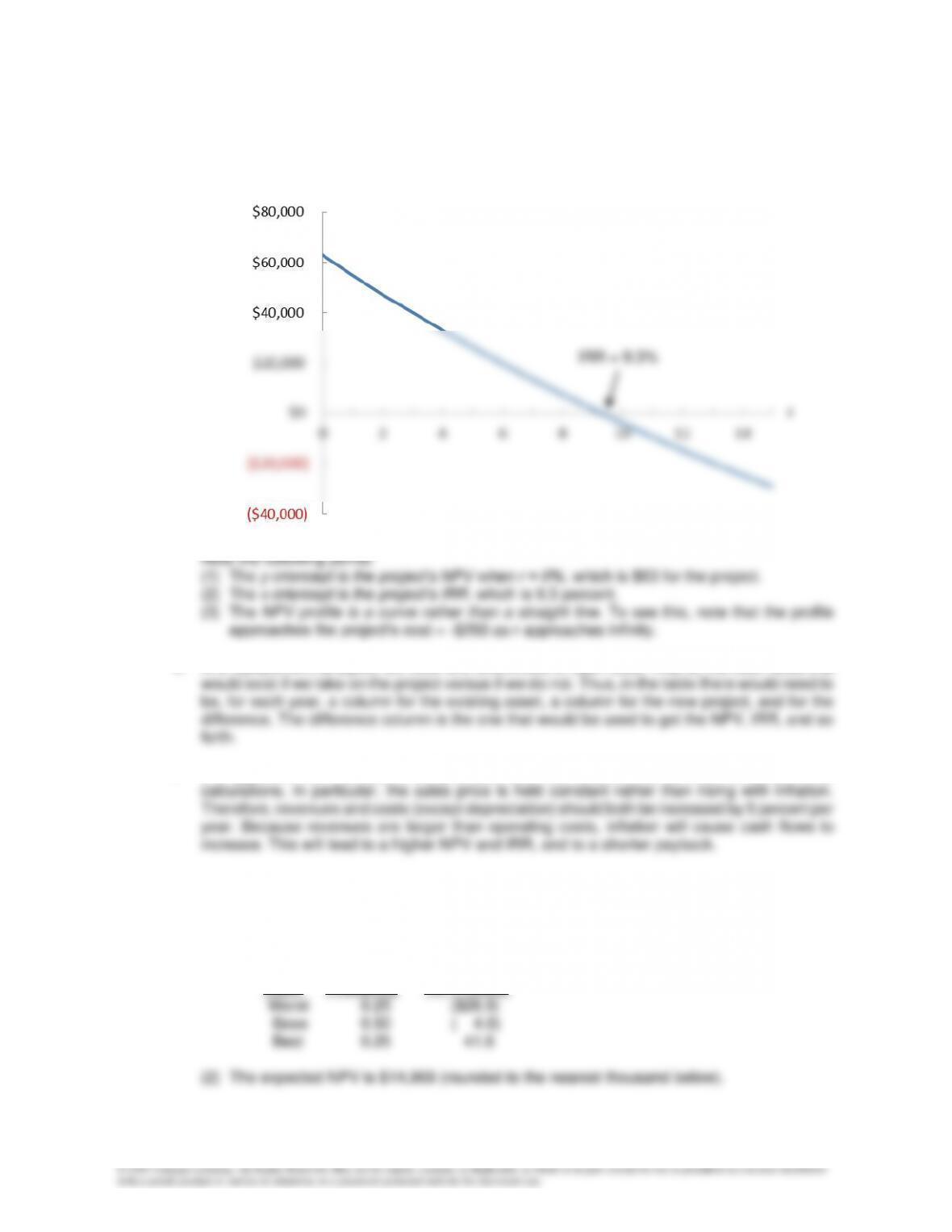

j. The NPV profile is plotted in the figure below.

k. In a replacement analysis, we must find differences in cash flows—that is, the cash flows that

l. It is apparent from the data in the previous table that inflation has not been reflected in the

13-36 Integrative Problem

a. (1) We used a spreadsheet model to develop the scenarios (in thousands of dollars), which

are summarized below:

Case Probability NPV (000s)

NPV

r

IRR = 9.3%

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-40

( )

NPV

E NPV $1.7

b. (1) The project has a CV of 14.6, which is much higher than the average range of 2.0 to 3.0,

(2) It is reasonable to assume that if the economy is strong and people are buying a lot of

(3) If the project’s cash flows are highly correlated with the firm’s aggregate cash flows, which

generally is a reasonable assumption, then the project would have high corporate risk.

c. (1) Because the project is judged to have above-average risk, its differential risk-adjusted, or

(2) A numerical analysis such as this one might not capture all of the risk factors inherent in

d. The SML can be used to estimate the project’s required rate of return on equity:

13-41

13-37 Computer-Related Problem

a. & b.

INPUT DATA: KEY OUTPUT:

Expected Cash Flows

Year Proj. A Proj. B Proj. A Proj. B

0 (45,000) (50,000) NPV 2,600 2,758

MODEL-GENERATED DATA:

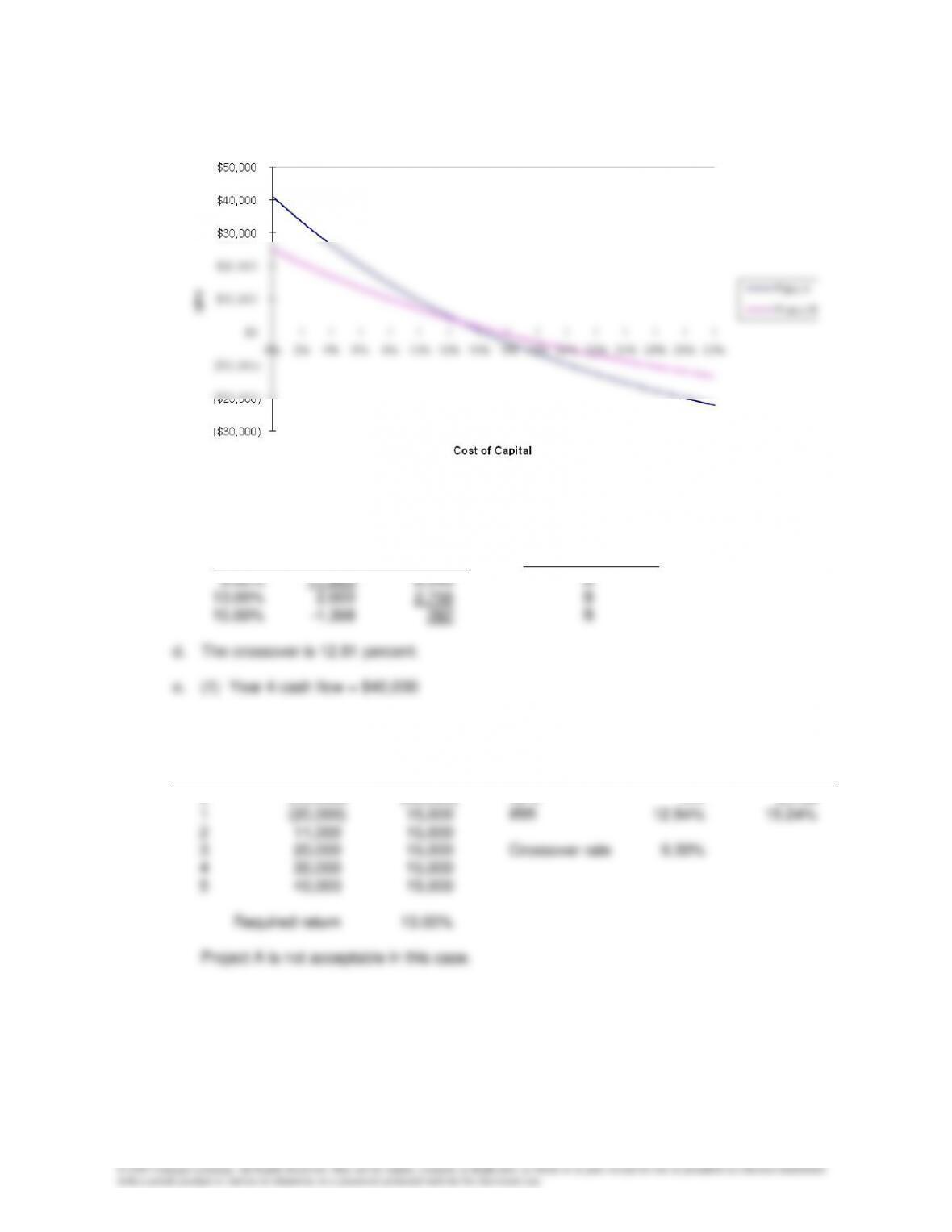

NPV profile:

Proj. A Proj. B

r NPV NPV

0.00% 41,000 25,000

Crossover rate calculation:

Delta's Required NPV of

Year CFs Return Delta

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-42

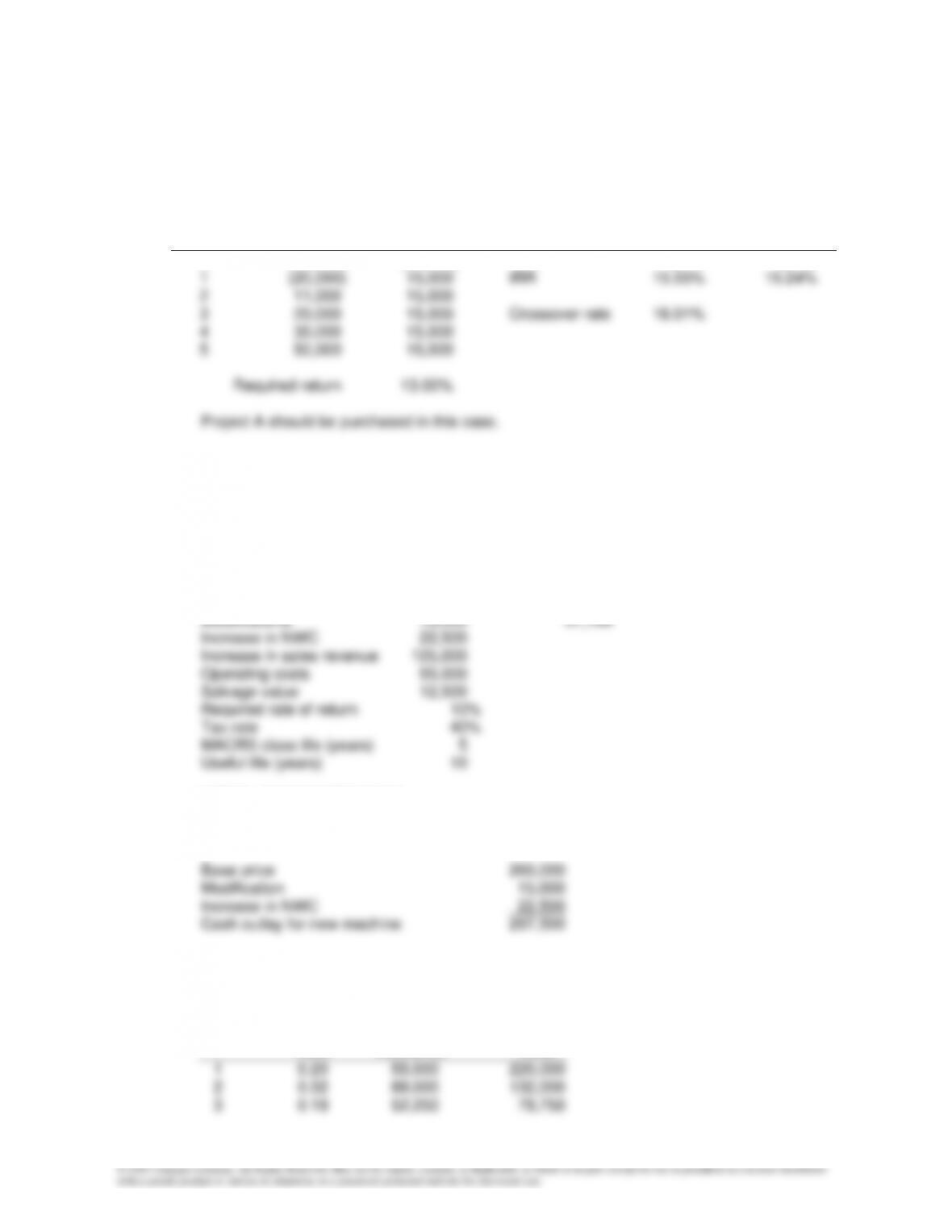

c. Because the projects are mutually exclusive, only one can be chosen. Following are the

NPVs for the two projects at the different required rates of return:

r NPVA NPVB Project to Purchase

INPUT DATA: KEY OUTPUT:

Expected Cash Flows

Year Proj. A Proj. B Proj. A Proj. B

0 (45,000) (50,000) NPV -114 2,758

Principles of Finance 6e Chapter 13

Besley/Brigham

13-43

e. (2) Year 4 cash flow = $50,000

INPUT DATA: KEY OUTPUT:

Expected Cash Flows

Year Proj. A Proj. B Proj. A Proj. B

0 (45,000) (50,000) NPV 5,314 2,758

13-38 Computer-Related Problem

a. The NPV of the project is positive (NPV = $57,186), so Golden State should purchase the

machine and expand its operations.

INPUT DATA: KEY OUTPUT:

Base price 260,000 NPV

MODEL-GENERATED DATA:

1.Cost of investment at t=0:

Depreciation schedule:

Basis = 275,000

Ending

Year MACRS Depreciation Book

Rate Allowance Value

13-44

Annual cash flows:

0 1 2 3 4 5 6 7 8 9 10

Cash Outlay -297,500

Depr. tax savings 22,000 35,200 20,900 13,200 12,100 6,600 0 0 0 0

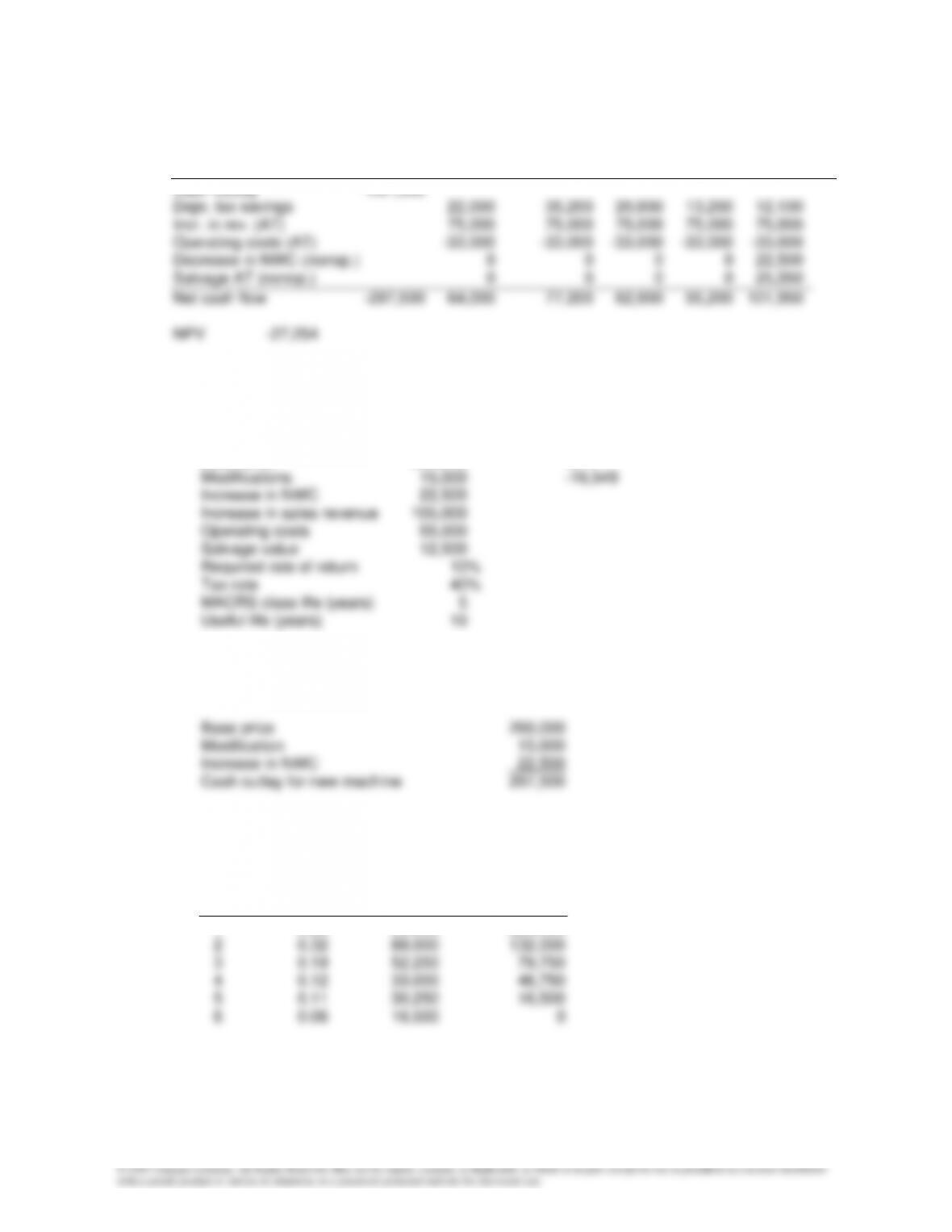

b. The NPV of the project is negative (NPV = -27,254), so Golden State should not purchase the

machine and expand its operations.

INPUT DATA: KEY OUTPUT:

Base price 260,000 NPV

Modifications 15,000 -27,254

MODEL-GENERATED DATA:

1.Cost of investment at t=0:

Depreciation schedule:

Ending

Year MACRS Depreciation Book

Rate Allowance Value

1 0.20 55,000 220,000

Principles of Finance 6e Chapter 13

Besley/Brigham

13-45

Annual cash flows:

0 1 2 3 4 5

Cash Outlay -297,500

c. The NPV of the project is negative (NPV = -16,549), so Golden State should not purchase the

machine and expand its operations.

INPUT DATA: KEY OUTPUT:

Base price 260,000 NPV

MODEL-GENERATED DATA:

1.Cost of investment at t=0:

Depreciation schedule:

Basis = 275,000

Ending

Year MACRS Depreciation Book

Rate Allowance Value

1 0.20 55,000 220,000

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-46

Annual cash flows:

0 1 2 3 4 5 6 7 8 9 10

Cash Outlay -297,500

Depr. tax savings 22,000 35,200 20,900 13,200 12,100 6,600 0 0 0 0

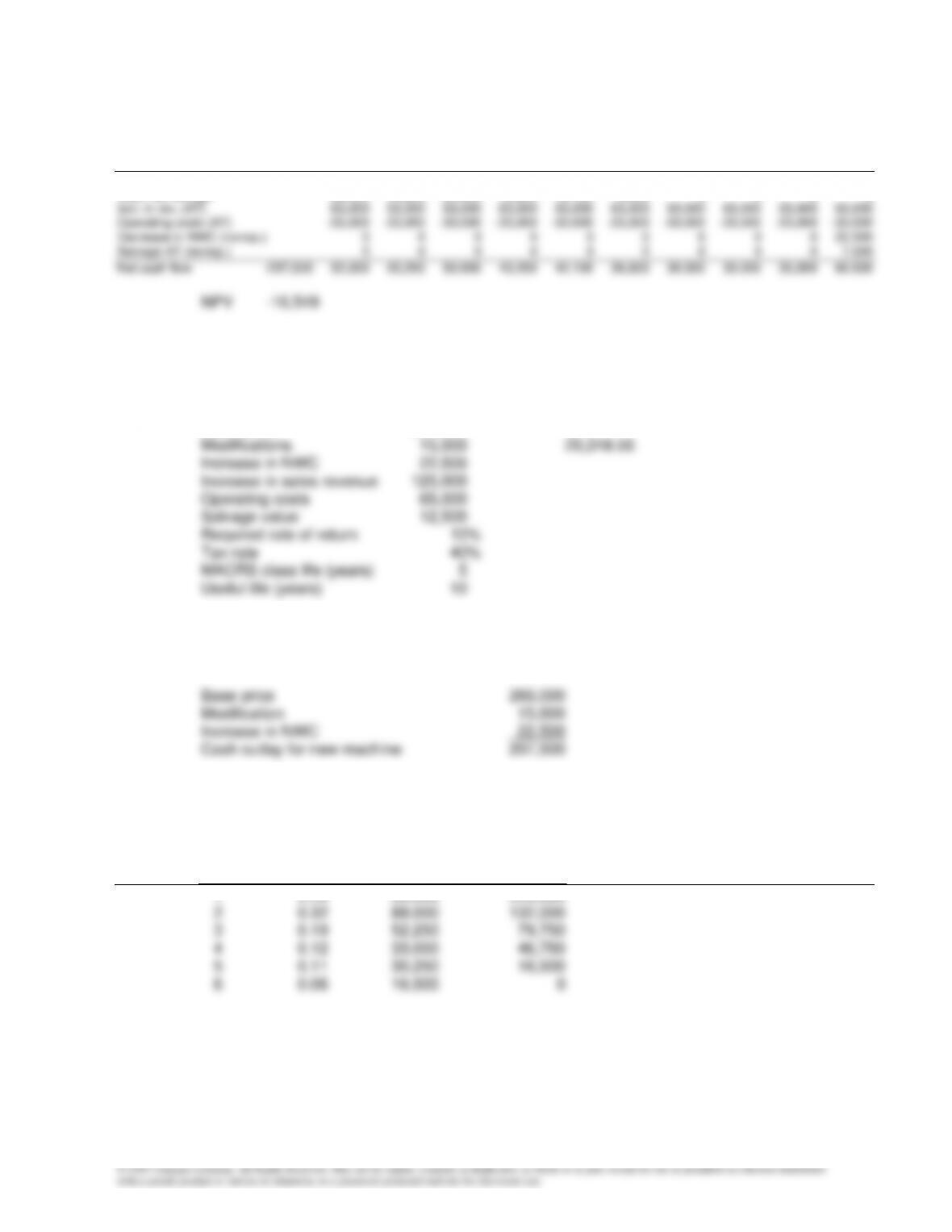

d. The NPV of the project is negative (NPV = 20,318.56), so Golden State should not purchase

the machine and expand its operations.

INPUT DATA: KEY OUTPUT:

Base price 260,000 NPV

MODEL-GENERATED DATA:

1.Cost of investment at t=0:

Depreciation schedule:

Basis = 275,000

Ending

Year MACRS Depreciation Book

Rate Allowance Value

1 0.20 55,000 220,000

Principles of Finance 6e Chapter 13

Besley/Brigham

13-47

Annual cash flows:

0 1 2 3 4 5 6 7 8 9 10

Cash Outlay -297,500

Depr. tax savings 22,000 35,200 20,900 13,200 12,100 6,600 0 0 0 0

Solutions to Appendix Problem

13A-1 MACRS MACRS Straight-Line Difference in PV of

Year Rate Depreciation Depreciation Depreciation Tax Savings Savings

1 0.10 $ 10,000,000 $ 10,000,000 $ 0 $ 0 $ 0

2 0.18 18,000,000 10,000,000 8,000,000 2,720,000 2,289,370

ETHICAL DILEMMA

This Is a Good Investment—Be Sure the Numbers Show that It Is!

Ethical dilemma:

Oliver Greene is a relatively recent college graduate whose primary responsibility with Cybercomp, Inc. is to

evaluate capital budgeting projects and make recommendations to the board of directors. He is paid very

well in his current position. Oliver finds himself in a situation where the CEO of Cybercomp, Nadine Wilson,

insists that the proposal to purchase Netware Products be made to look good. Netware manufactures

circuitry that complements Cybercomp's products. A preliminary appraisal report given to Oliver suggests

the purchase might not be very judicious; the report was completed two years ago. Nadine has made it clear

to Oliver that she wants his analysis to recommend that Netware be purchased by Cybercomp. To make

matters worse, the gossip at Cybercomp is that Mrs. Wilson is tied to the owners of Netware either through

friendship, ownership, or both. The suggestion is that a conflict of interest exists for Mrs. Wilson. Also, Oliver

has the impression that he could lose his job if he doesn't make the "right" decision.

Discussion questions:

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-48

• What is the ethical dilemma? Is there an ethical dilemma?

On the surface, it appears the ethical dilemma is that Mrs. Wilson, the CEO of Cybercomp, is pressuring

Oliver Greene to provide a favorable analysis of Netware Products so Cybercomp's board of directors

• What should Oliver do?

Oliver should complete his analysis of Netware Products in an unbiased manner; he should disregard

any rumors and try not to let Mrs. Wilson's comments influence his initial analysis. Perhaps Oliver's

• Should rumors and innuendos be considered in the capital budgeting analysis?

• If Oliver was certain his job hinged on this capital budgeting decision, should he produce the results

requested by the CEO?

Ask the students what they would do in this situation. Oliver is in a position that pays very well, perhaps

Principles of Finance 6e Chapter 13

Besley/Brigham

13-49

References:

Certainly there are countless examples of the situation described in this Ethical Dilemma, but, few, if any are

made public. An example of a capital budgeting project that parallels this scenario is described in the

Managerial Perspective in Chapter 10. RJR Nabisco invested in the smokeless cigarette because it was the

pet project of some top managers. Even though there is no indication that top managers pressured RJR's

capital budgeting analysts to "manipulate" the results so a favorable decision could be reached, it is thought

that the company knew the project had serious flaws and many were afraid to voice their concerns because

they didn't want to offend top management. The smokeless cigarette turned out to be a $300 million disaster

that lasted less than one year.

Interestingly, RJR currently is testing whether a new smokeless cigarette can be marketed under different

conditions. For more information about RJR's smokeless cigarette projects, see the following articles:

"RJR Is Testing a 'Smokeless Cigarette' After Attempt Failed Five Years Ago," The Wall Street Journal,

November 28, 1994, p. A5.

"RJR Smokeless Cigarette Test Is Snuffed Out," Los Angeles Times, March 1, 1989, p. 1+.

"Fire Without Smoke," The Economist, September 17, 1988, p. 33+.

For examples of some product ideas that were flops, see the following articles:1

“Ford’s Edsel Drives Pack of Marketing Misses: A Look at the Century’s Hyped Products,” Chicago Tribune,

June 13, 1999, p. 12.

“The Museum of Dumb Ideas,” National Post, July 1, 1999, p. 10.

1 The fact that a product flops does not mean that the firm did not conduct a proper capital budgeting analysis.