Principles of Finance 6e Chapter 13

Besley/Brigham

13–21

10%

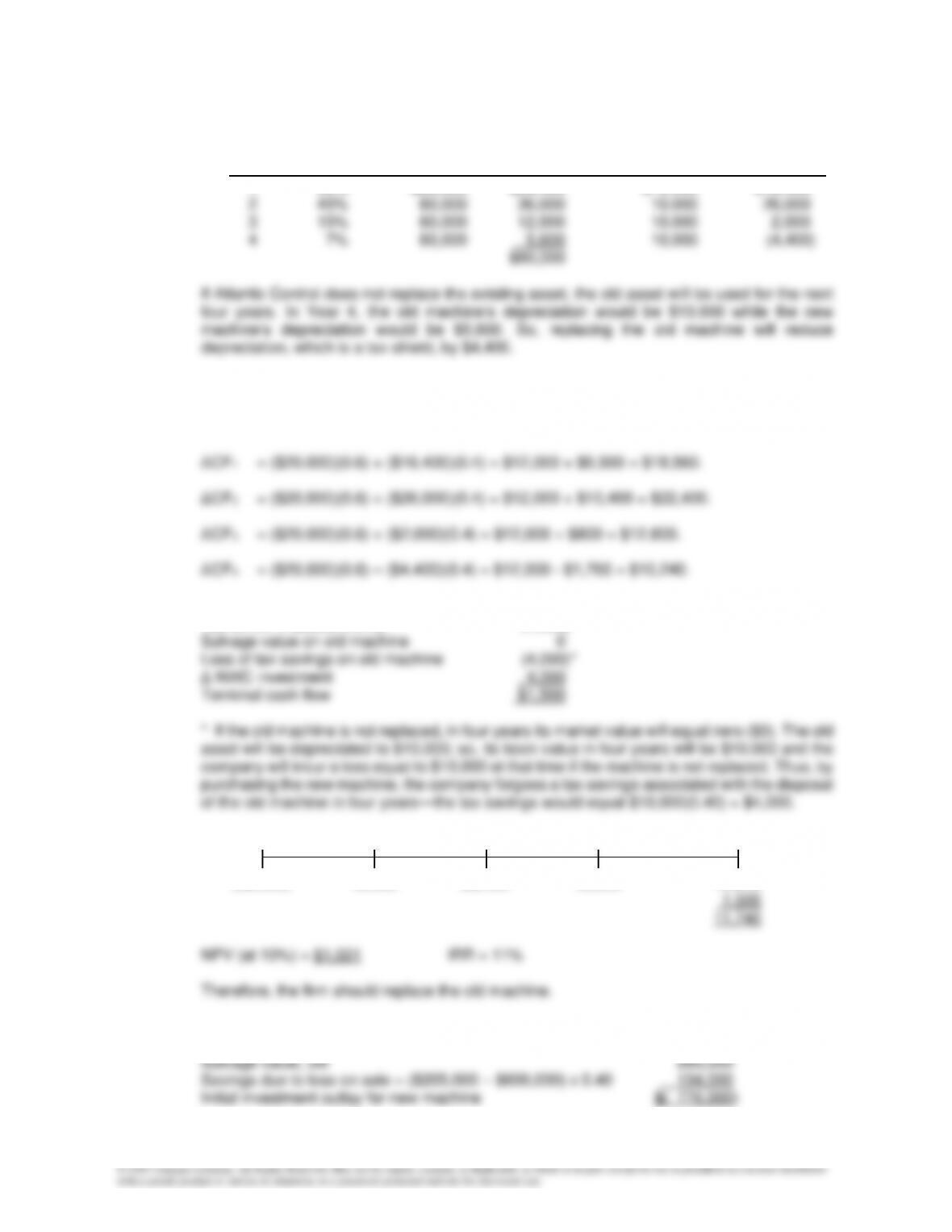

b. Recovery Depreciable Depreciation Depreciation Change in

Year Percentage Basis Allowance, New Allowance, Old Depreciation

1 33% $80,000 $26,400 $10,000 $16,400

Supplemental operating cash flows:

ΔCFt = ΔOperating(1 ─ T) + (ΔDepreciation)(T)

c. Salvage value on new machine $2,500

Tax on SV = $2,500 x 0.40 (1,000)

d. 0 1 2 3 4

(52,000) 18,560 22,400 12,800 10,240

13-28 a. Cost of new machine $(1,175,000)

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–22

b. Recovery Depreciable Depreciation Depreciation Change in

Year Percentage Basis Allowance, New Allowance, Old Depreciation

1 20% $1,175,000 $ 235,000 $120,000 $115,000

c. Supplemental operating cash flows:

ΔCFt = (ΔOperating expenses)(1 – T) + (ΔDepreciation)(T).

d. Book value in Year 5 = $1,175,000(0.06) = $70,500.

e. A time line of the cash flows looks like this:

0 1 2 3 4 5

(776,000) 199,000 255,400 194,300 161,400 156,700

f. (1) If the expected life of the old machine decreases, the new machine will look better as cash

12%

Principles of Finance 6e Chapter 13

Besley/Brigham

13–23

13-29 a. βGoodtread = wTDβTD + wRDβRD = (0.75)1.5 + (0.25)0.5 = 1.25.

b. Apparently, investments are made either in the Tire Division (TD) or in the Recap Division (RD).

The required rate of return for each division is:

The project described in the problem would have a positive NPV if it is an average risk project

in the Recap Division, but a negative NPV if it is in the Tire Division:

0 1 2 3 5

13–30 If the actual life is five years:

The cash flow time line is:

0 1 2 3 4 5

(72,000) 20,160 20,160 20,160 20,160 20,160

…

10%

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–24

If the actual life is four years:

The cash flow time line is:

0 1 2 3 4

(72,000) 20,160 20,160 20,160 20,160

The cash flow time line is:

0 1 2 5 6 7 8

(72,000) 20,160 20,160 20,160 14,400 14,400 14,400

10%

10%

Principles of Finance 6e Chapter 13

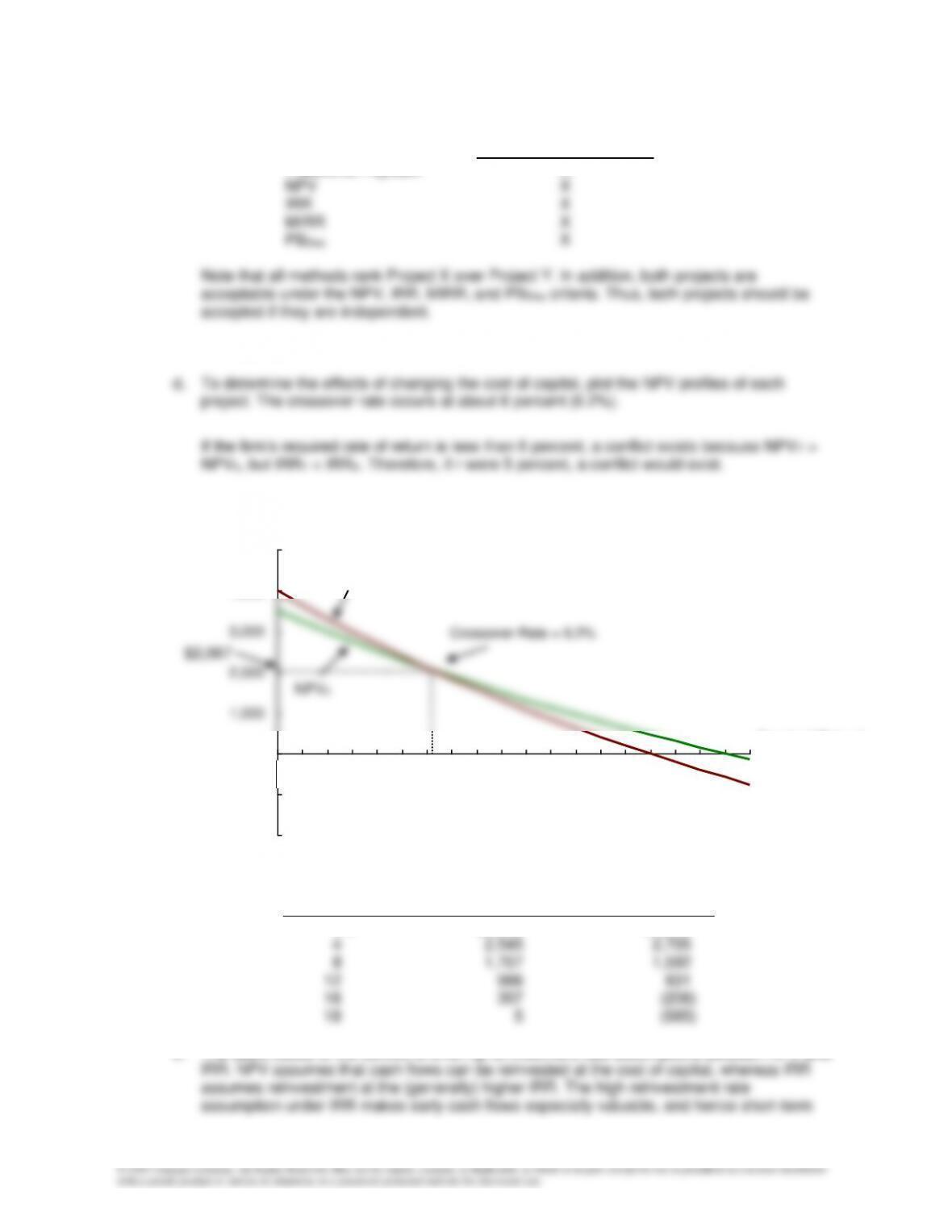

13-31 a. Compute the values for NPV at different required rates of return, r, by entering the cash flows

for each project in the CF register of your calculator, then change the value for I and compute

the NPV each time.

r NPVA NPVB

0% $970 $399

10 297 179

The NPV profiles look like the following:

NPV ($ millions)

r%

Crossover

14.5

Project A

Project B

17.8

0.4

0.6

0.8

1.0

0.2

0

-0.2

4812 16 20 24 28

IRRA

IRRB

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–26

b. For Project A, solve the following:

)IRR1(

500$

)IRR1(

100$

)IRR1(

193$

)IRR1(

387$

300$NPV

4321

A

+

+

+

−

+

+

−

+

+

−

+−=

c. At r = 12%, Project A has the greater NPV, specifically $206.77 as compared to Project B’s

d. Looking at the NPV profile developed in Part a, the crossover rate is between 14 and 15

percent, or approximately 14.5%. To determine exactly where the crossover rate is, proceed as

follows: Construct a Project Δ, which is the difference in the two projects’ cash flows:

Project Δ =

Year CFA – CFB

1 (521)

13–32 a. Payback:

To determine the payback, construct the cumulative cash flows for each project:

Principles of Finance 6e Chapter 13

Besley/Brigham

13–27

Project X Project Y

Year Cash Flows Cumulative CF Cash Flows Cumulative CF

0 ($10,000) ($10,000) ($10,000) ($10,000)

years2.86

$3,500

$3,000

2Payback

Y

=+=

Net present value (NPV):

(1.12)

$1,000

(1.12)

$3,000

(1.12)

$3,000

(1.12)

$6,500

$10,000NPV 4321

X

++++−=

Internal rate of return (IRR):

To solve for each project’s IRR, find the discount rates that equate each NPV to zero:

Modified Internal rate of return (MIRR):

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–28

3 2 1 0

4

X

4

X

4

X

1/4

X

$6,500(1.12) $3,000(1.12) $3,000(1.12) $1,000(1.12)

$10,000 (1 MIRR )

$17,255.23

$10,000 (1 MIRR )

$17,255.23

(1 MIRR ) 1.725523

$10,000

MIRR (1.725523) 1.0

0.1461 14.61%

+ + +

=+

=+

+ = =

=−

==

13.73%0.1373

1.0(1.672765)MIRR

1.672765

$10,000

$16,727.65

)MIRR(1

)MIRR(1

$16,727.65

$10,000

)MIRR(1

2)$3,500(1.12)$3,500(1.12)$3,500(1.12)$3,500(1.1

$10,000

1/4

Y

4

Y

4

Y

4

Y

0123

==

−=

==+

+

=

+

+++

=

Discounted Payback Period (PBDisc):

To determine the discounted payback, construct the cumulative discounted cash flows for

each project:

Project X Project Y

Year PV CF @ 12% Cumulative CF PV CF @ 12% Cumulative CF

0 ($10,000.00) ($10,000.00) ($10,000.00) ($10,000.00)

Principles of Finance 6e Chapter 13

Besley/Brigham

13–29

Project that Ranks Higher

Traditional Payback X

c. In this case, we would choose the project with the higher NPV at r = 12%, or Project X.

Required Rate

of Return NPVX NPVY

0% $3,500 $4,000

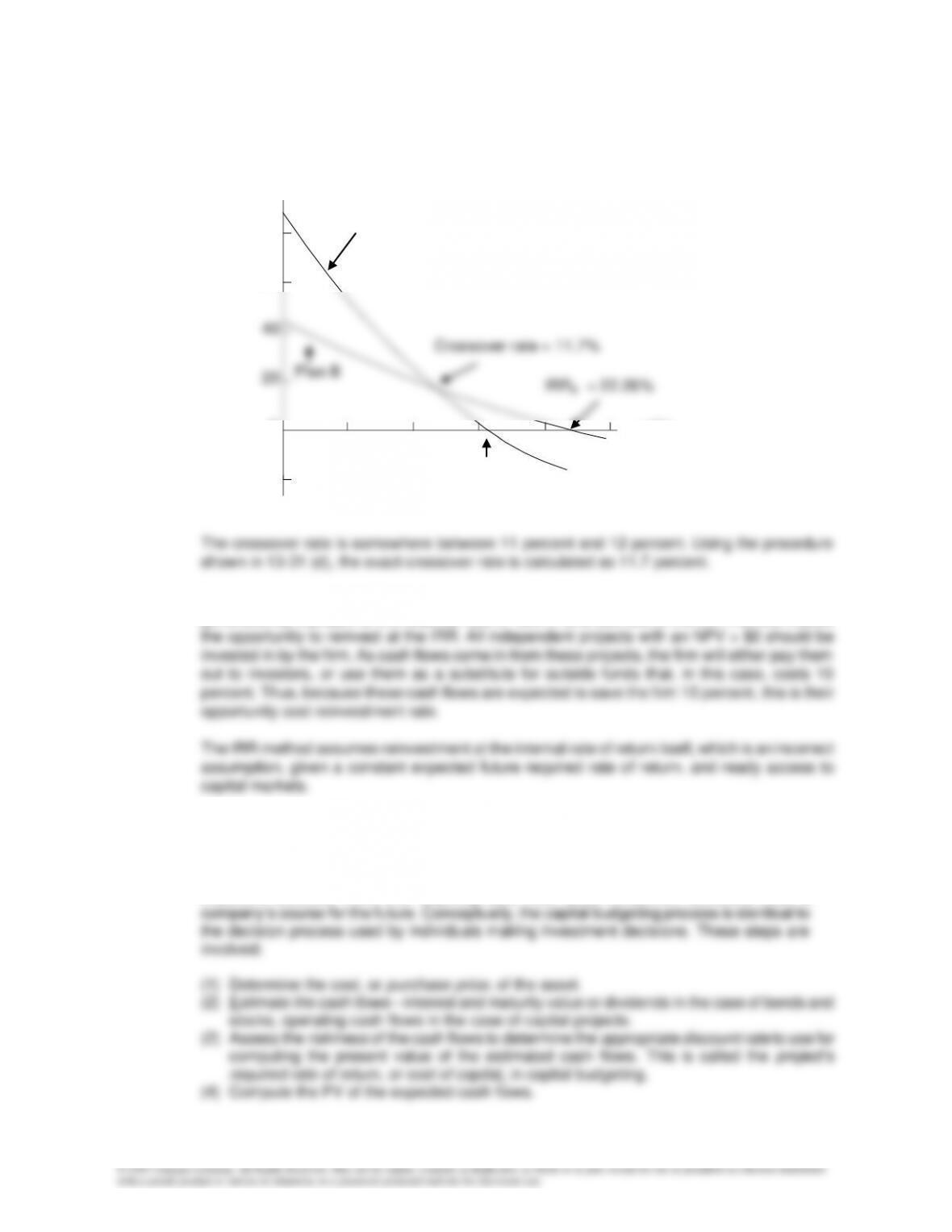

e. The basic cause of the conflict is differing reinvestment rate assumptions between NPV and

Required Rate of

Return, r (%)

Crossover Rate = 6.2%

NPVY

NPVX

NPV ($)

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

0 2 4 6 8 10 12 14 16 18

$2,067

Chapter 13 Principles of Finance 6e

Besley/Brigham

13-33 a. r NPVA NPVB

0 2,400,000 30,000,000

5 1,714,286 14,170,642

b. Yes. Assuming (1) equal risk among projects, and (2) that the required rate of return is a

c. Plan A:

1

0

)MIRR1(

)12.1(000,400,14$

000,000,12$+

=

k (%)

510 15 20 25

(Millions of

Dollars)

NPV

Plan B

Plan A

Crossover rate = 16.07%

0

2.4

6

12

18

24

30

IRRA = 20.0%

IRRB = 16.7%

r (%)

Principles of Finance 6e Chapter 13

Besley/Brigham

MIRRA

13-34 a. Using a financial calculator, we get:

NPVA = $14,486,808.

NPVB = $11,156,893.

20

60.998,787,155$

10.0

1)10.1(

000,720,2$

−

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–32

b.

c. The NPV method implicitly assumes that the opportunity exists to reinvest the cash flows

generated by a project at the required rate of return, whereas use of the IRR method implies

13-35 Integrative Problem

a. Capital budgeting is the process of analyzing additions to fixed assets. Capital budgeting is

important because, more than anything else, fixed asset investment decisions chart a

k (%)

NPV

(Millions of

Dollars)

80

60

0

–20

510 15 20 25

IRRA = 15.03%

Plan A

r (%)

Principles of Finance 6e Chapter 13

Besley/Brigham

13–33

b. Projects are independent if the cash flows of one are not affected by the acceptance of the

other. Conversely, two projects are mutually exclusive if acceptance of one impacts adversely

Projects that have conventional cash flows have outflows, or costs, in the first year (or years)

followed by a series of inflows. Projects with unconventional cash flows have one or more

outflows after the inflow stream has begun. Here are some examples:

inflow (+) or outflow (-) in year

0 1 2 3 4 5

conventional – + + + + +

c. You may want to begin discussion differentiating between cash flow versus accounting income.

0 1 2 3 4

CF0

1

CF

2

CF

3

CF

4

CF

d. (1) – (4)

The only thing that requires explanation here is the use of the depreciation tables in

Appendix 13A. Here are the rates for 3-year property; they are multiplied by the depreciable

basis, $240,000, to get the annual depreciation allowances:

($ Thousands)

Chapter 13 Principles of Finance 6e

Besley/Brigham

13–34

End of Year: 0 1 2 3 4

Unit sales (thousands) 100 100 100 100

Price/unit $2.00 $2.00 $2.00 $2.00

Total revenues $200.0 $200.0 $200.0 $200.0

Cash flow timeline:

0 1 2 3 4

(260,0) 79.7 91.2 62.4 89.7

Principles of Finance 6e Chapter 13

Besley/Brigham

13–35

f. (1) Notice from Table IP13.1 that the “Cumulative CF for payback” is negative until Year 4;

thus, the regular payback occurs sometime in Year 4:

To compute the discounted payback period, we need to discount each of the annual cash

flows using the required rate of return. The following table shows the discounted payback

period:

r = 10%

Non-Discounted Discounted Cumulative CF

Year Cash Flow Cash Flow for Payback

(2) Payback represents a type of “breakeven” analysis: The payback period tells us when the

(3) Discounted payback is similar to payback except that discounted rather than

nondiscounted cash flows are used.

(4) Regular payback has two critical deficiencies: (1) it ignores the time value of money, and