Principles of Finance 5e Chapter 12

Besley/Brigham

12–15

c. Rate of return, r1:

−

=+

r

1

401,155$000,675$

8

)r1(

1

d.

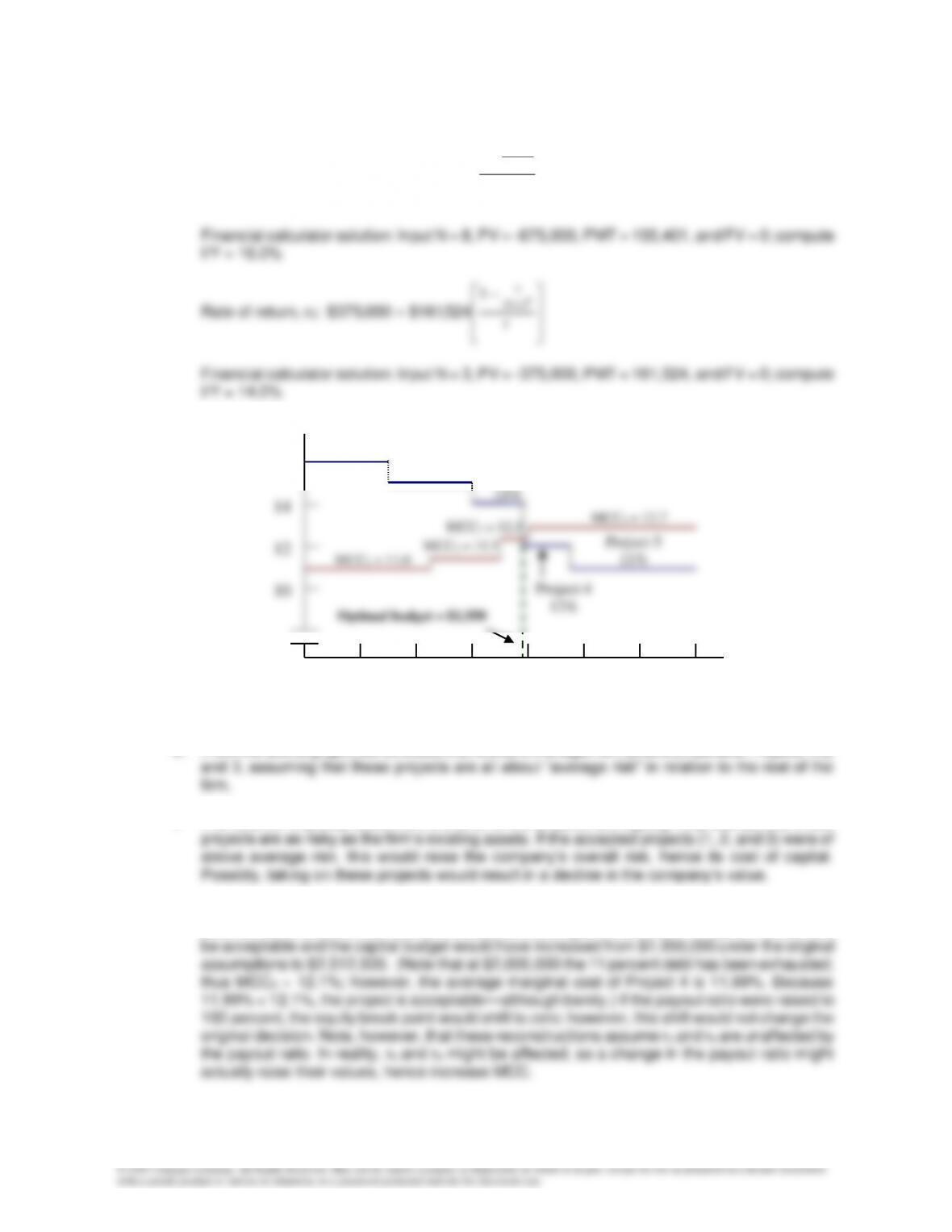

10

12

14

Project 4

12%

Project 5

11%

e. From the above graph, we conclude that Ezzell’s management should undertake Projects 1, 2,

f. The solution implicitly assumes (1) that all of the projects are equally risky and (2) that these

g. If the payout ratio were lowered to zero, this would shift the equity break point to the right, from

$1,818,182, to $4,545,455. This shift would have changed the decision—Project 4 would now

12–30 Integrative Problem

16

%

500

1,000

1,500

2,000

2,500

3,000

3,500

Capital Expenditure/Financing

($ thousands)

Project 1

16%

Project 3

14%

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–16

a. (1) The WACC is used primarily for making long-term capital investment decisions—that is, for

capital budgeting. Thus, the WACC should include the types of capital used to pay for long-

(2) Stockholders are concerned primarily with those corporate cash flows that are available for

(3) In financial management, the cost of capital is used primarily to make decisions that involve

b. Coleman’s 12 percent bond with 15 years to maturity currently is selling for $1,153.72. Thus, its

yield to maturity is 10 percent:

c. (1) Because the preferred issue is perpetual, its cost is estimated as follows:

9.0% = 0.09 =

$2.00 – $113.10

0.1($100)

=

NP

D

= r ps

ps

Note that (1) flotation costs for preferred are significant, so they are included here, (2)

because preferred dividends are not deductible to the issuer, there is no need for a tax

adjustment, and (3) we could have estimated the effective annual cost of the preferred, but

as in the case of debt, the simple cost is generally used.

(2) Corporate investors own most preferred stock, because 70 percent of preferred dividends

0 1 2 3 29 30

…

-1,153.70 60 60 60 60 60

1,000

rd = ?

Principles of Finance 5e Chapter 12

Besley/Brigham

12–17

d. (1) Coleman’s earnings can either be retained and reinvested in the business or paid out as

dividends. If earnings are retained, Coleman’s shareholders forego the opportunity to

(2) The CAPM estimate for Coleman’s cost of retained earnings is 14.2 percent:

e. Because Coleman is a constant growth stock, the constant growth model can be used:

50$

$50

P

P

0

0

f. The bond-yield-plus-risk-premium estimate is 14 percent:

g. The following table summarizes the rs estimates:

Method Estimate

CAPM 14.2%

h. The DCF method produced an estimate for the cost of retained earnings of rs = 13.8% (see the

computations given earlier). However, flotation costs of F = 15% must be incurred when new

common stock is sold, and that increases the cost of equity to 15.4%:

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–18

Thus, flotation costs increase the cost of equity by 1.6 percentage points for up to $300,000 of

new common stock:

Flotation adjustment1 = 15.4% – 13.8% = 1.6%.

i. The company is raising money in order to make an investment. The money has a cost, and this

j. (1) Coleman’s WACC is 11.1 percent when retained earnings are used as the equity

component (at 14 percent):

Up to $300,000 of equity as RE at rs = 14%:

Capital Structure Component

Weights x costs = WACC

0.3 6.0% 1.8%

(2) When up to $300,000 of new common stock is sold, the WACC increases from 11.1

percent to WACC2 = 12.1 percent:

Principles of Finance 5e Chapter 12

Besley/Brigham

12–19

Capital Structure Component

Weights x costs = WACC

0.3 6.0% 1.8%

(3) When more than $300,000 of new common stock is sold, the WACC increases to 12.8

percent:

k. (1) The dollar amount of total new capital at which Coleman uses up its retained earnings and

must resort to selling new common stock will consist of the retained earnings plus debt and

preferred supported by the retained earnings, and the point is called the retained earnings

break point:

$500,000 =

0.60

$300,000

equity of proportion Target

earnings retained of ollarsD

BPRE ==

(2)

strucure capital the in capital of type this of roportionP

type given a of capital cost lower of amount otalT

=

intoP

reakB

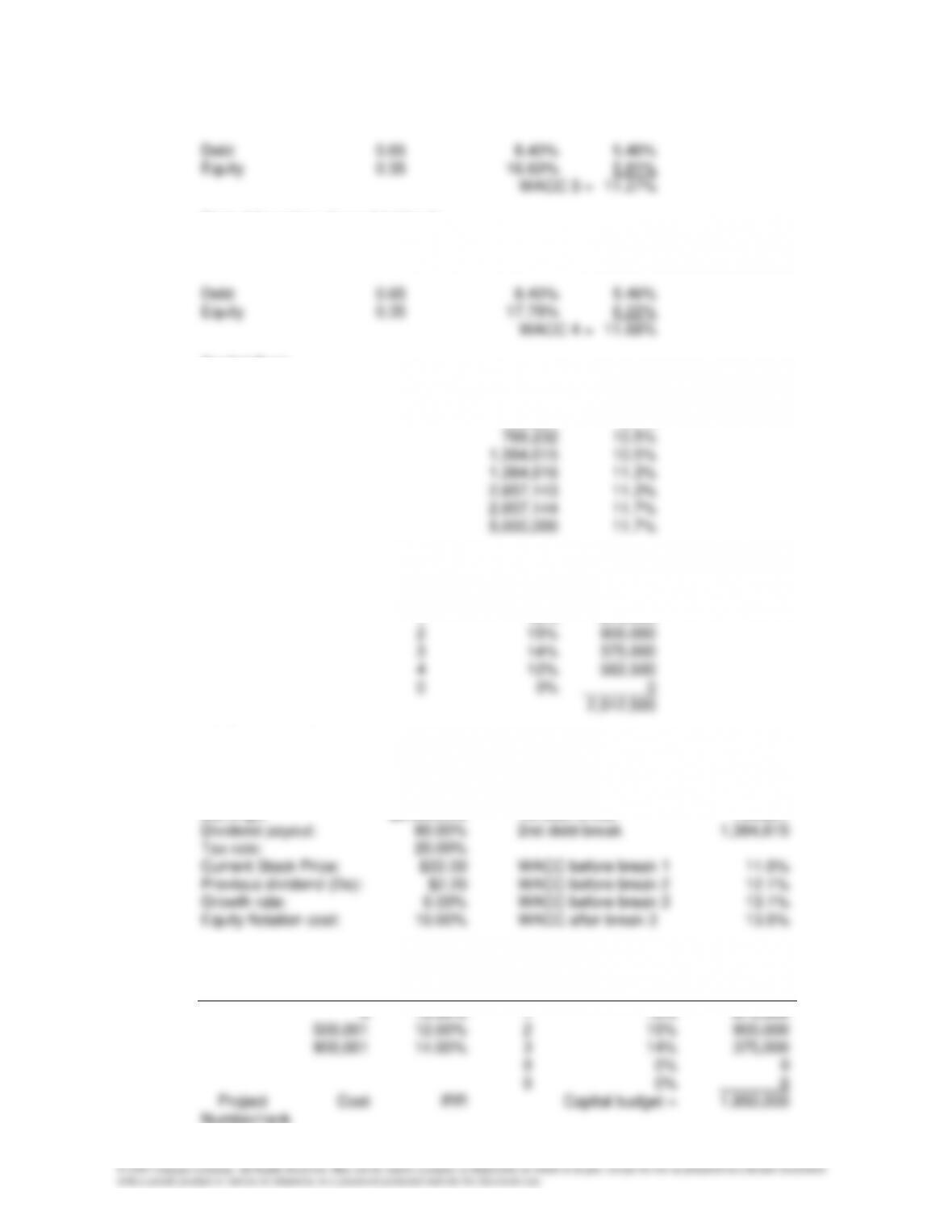

(3) A marginal cost of capital (MCC) schedule is simply a plot of the firm’s WACC versus

dollars of new capital raised. Here is Coleman’s MCC schedule:

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–20

20

15

10

500 1,000 1,500 2,000

WACC3 = 12.8%

WACC2 = 12.1%

WACC2 = 11.1%

MCC

Percent

New Capital

($ thousands)

l. (1) The IOS schedule is a plot of the projects being considered by cost and in descending

order of IRR. Note that Coleman actually faces two IOS schedules—one with Projects A, B,

and C, and another with Projects A, B*, and C.

20

15

10

500 1,000 1,500 2,000

A = 17%

B = 16%

B’ = 15%

C = 11.5%

WACC3 = 12.8%

WACC2 = 12.1%

WACC2 = 11.1%

MCC

IOS

1,200

Optimal Capital

Budget

Percent

New Capital

($ Thousands)

Principles of Finance 5e Chapter 12

Besley/Brigham

12–21

(3) As more and more new capital is required in any year, Coleman’s WACC would eventually

begin to rise above 12.8 percent. The company would have to find new buyers for its debt,

(3) In this situation, the MCC curve would cut through Projects B and B*, meaning that those

m. If Coleman could only raise $200,000 of debt at a 10 percent cost and the remaining debt

The WACCs at these intervals would be:

A. Between $1 and $500,000: WACC1 = 11.1%. (just as before.)

B. Between $500,000 and $666,667: WACC2 = 12.1%. (just as before.)

12-31 Computer-Related Problem

a. Under this scenario, the MCC schedule has moved down because all of the WACCs have

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–22

INPUT DATA: KEY OUTPUT:

Debt ratio: 65.00% Ret. earnings break 2,857,143

Earnings: $2,500,000 1st debt break 769,231

Accepted

Beginning of Projects Project

New debt cost: Range rd (non-zero) IRR Cost

0 10.00% 1 16% 675,000

MODEL-GENERATED DATA:

Breaks in the MCC schedule:

Cost of financing below first break:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between first and second breaks:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between second and third breaks:

After-tax Weighted

Component Weight Cost Cost

Principles of Finance 5e Chapter 12

Besley/Brigham

12–23

Cost of financing above third break:

After-tax Weighted

Component Weight Cost Cost

Capital Cost:

Range of financing Capital cost

1 9.7%

769,231 9.7%

Optimal capital budget:

Project ROR Project

Number/rank Cost

1 16% 675,000

b. (1) Tax rate = 20%

INPUT DATA: KEY OUTPUT:

Debt ratio: 65.00% Ret. earnings break 2,857,143

Earnings: $2,500,000 1st debt break 769,231

Accepted

Beginning of Projects Project

New debt cost: Range rd (non-zero) IRR Cost

Number/rank

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–24

MODEL-GENERATED DATA:

Breaks in the MCC schedule:

Cost of financing below first break:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between first and second breaks:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between second and third breaks:

After-tax Weighted

Component Weight Cost Cost

Cost of financing above third break:

After-tax Weighted

Component Weight Cost Cost

Capital Cost:

Range of financing Capital cost

1 11.0%

769,231 11.0%

Principles of Finance 5e Chapter 12

Besley/Brigham

12–25

Optimal capital budget:

Project ROR Project

Number/rank Cost

1 16% 675,000

b. (1) Tax rate = 0%

INPUT DATA: KEY OUTPUT:

Debt ratio: 65.00% Ret. earnings break 2,857,143

Accepted

Beginning of Projects Project

New debt cost: Range rd (non-zero) IRR Cost

0 10.00% 1 16% 675,000

MODEL-GENERATED DATA:

Breaks in the MCC schedule:

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–26

Cost of financing below first break:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between first and second breaks:

After-tax Weighted

Component Weight Cost Cost

Cost of financing between second and third breaks:

After-tax Weighted

Component Weight Cost Cost

Cost of financing above third break:

After-tax Weighted

Component Weight Cost Cost

Capital Cost:

Range of financing Capital cost

1 12.3%

769,231 12.3%

Optimal capital budget:

Project ROR Project

Number/rank Cost

1 16% 675,000

Principles of Finance 5e Chapter 12

Besley/Brigham

12–27

ETHICAL DILEMMA

How Much Should You Pay to Be “Green”?

Ethical dilemma:

SS is evaluating a project that might help the firm to increase its presence in the “green” industry by

propelling the company into the leadership role in the country’s quest to clean up and protect the

environment. Although Tracey is not evaluating the project’s acceptability, it is her responsibility to

establish the hurdle rate, or weighted average cost of capital (WACC), that is used by those who

conduct capital budgeting analyses. Tracey, who is a compassionate environmentalist, would like to see

SS invest in the project. But, Manual, who works in the capital budgeting department, has told Tracey

that preliminary analysis of the project suggests that its internal rate of return (IRR) is less than the

firm’s WACC, which would mean that the project is not an acceptable investment. Because Tracey feels

the company should purchase the project, she is considering changing the method that she currently

uses to compute the firm’s WACC. If she makes the change, the hurdle rate used to evaluate the

“green” project will be lower than it is currently, and thus the project might turn out to be acceptable.

However, if SS bases its decision on a hurdle rate that is too low and invests a substantial amount in the

project, in the future it might discover that the project actually should have been rejected. It is possible

that this discovery comes too late for the firm to correct its mistake, in which case the firm might find

itself in serious financial trouble.

Discussion questions:

• Is there an ethical problem? If so, what is it?

The question here is whether Tracey should change the weights that she currently uses to compute

• Is it appropriate for Tracey to change the hurdle rate used to evaluate capital budgeting projects?

Maybe. If Tracey can justify using book values rather than market values to weight the component costs

of capital, then it seems that she is making a rational, justifiable change. In fact, the change should be

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–28

• What would you do if you were Tracey?

Perhaps the best solution is to compute the firm’s WACC using both book values and market values to

determine the weights for component costs of capital. Before changing the methods that the firm

currently uses for the WACC computation, Tracey should get approval. If she can show that using book

References:

The following articles might be assigned for background material:

Pete Engardio, “Beyond the Green Corporation,” BusinessWeek, January 29, 2007, pp. 50–64.

John Carey, “Hugging the Tree-Huggers—Why So Many Companies are Suddenly Linking Up with ECO

Groups. Hint: Smart Business,” BusinessWeek, March 12, 2007, pp. 66-68.

Ian Ayes and Barry Nalebuff, “Environmental Atonement: Why Not,” Forbes, December 25, 2006, p. 134.

Emily Thornton, “Who Says It’s Not Easy Being Green,” BusinessWeek, December 25, 2006, p. 76.