Principles of Finance 5e Chapter 12

Besley/Brigham

12-1

CHAPTER 12

ANSWERS

12-1 This point is demonstrated in Table 12-1 and Figures 12-2 and 12-3 in the textbook. The marginal

12-2 This statement is not valid, because the cost of retained earnings is equal to the cost of common

12-3 Probable Effect on

rdT rs WACC

a. The corporate tax rate is lowered. + 0 +

b. The Federal Reserve tightens credit. + + +

g. The firm merges with another firm whose earnings

are countercyclical both to those of the first firm and

to the stock market. – – –

12-4 Assuming that all projects are equally risky, the capital budget should be evaluated at the cost of

12-6 Inflation expectations are “built into” the market rates that investors require. As a result, if inflation

12-7 rs < re because the firm incurs flotation costs when it issues new common stock. This point can be

Chapter 12 Principles of Finance 6e

12-2

P

0

)F1(P

0

−

12-8 If the firm invests in projects that are much riskier than its existing assets, the cost of capital will

12-9 Because the WACC represents the cost of raising funds and the firm must cover this cost to “make

12–10 Common stockholders will permit a firm to retain earnings that could be paid as dividends only if

_____________________________________________________________

SOLUTIONS

12-1

+

+

+

−

=60

60

)YTM1(

1

000,1

YTM

)YTM1(

1

1

7064.353,1

12-3

+

+

+

−

=16

16

)YTM1(

1

000,1

YTM

)YTM1(

1

1

3081.902

$92.15

0.05) $97(1

Principles of Finance 5e Chapter 12

Besley/Brigham

12-5

%37.12=

25.121$

5$1

=

)30.0 (1125$

5$1

=

rps −

5$

Chapter 12 Principles of Finance 6e

Besley/Brigham

common stock, whose cost will be:

0.25) – $30(1

000,60$

Principles of Finance 5e Chapter 12

Besley/Brigham

12-5

12–16 rdT = 5%

rs = 10% and re = 13%

12–17 Capital Sources Amount Percent of Capital Structure

Long-term debt $1,152 40.0

12–18 The break points are calculated as follows:

BPRE = $3,000,000/0.5 = $6,000,000

BPDebt = $5,000,000/0.5 = $10,000,000

Chapter 12 Principles of Finance 6e

Besley/Brigham

12-6

12–19 Retained earnings are forecast to be $7,500(1 – 0.3) = $5,250. RE breakpoint = $5,250/0.6 =

$8,750. The cost of retained earnings is:

%016.0 = 0.05 +

$8.59

)$0.90(1.05

= g +

P

g) + (1

D

= r

0

0

s

The cost of new equity is as follows:

( )

18.75% = 0.05 +

0.20) – $8.59(1

1.05$0.90

=

re

8

9

10

11

%

5

10

15

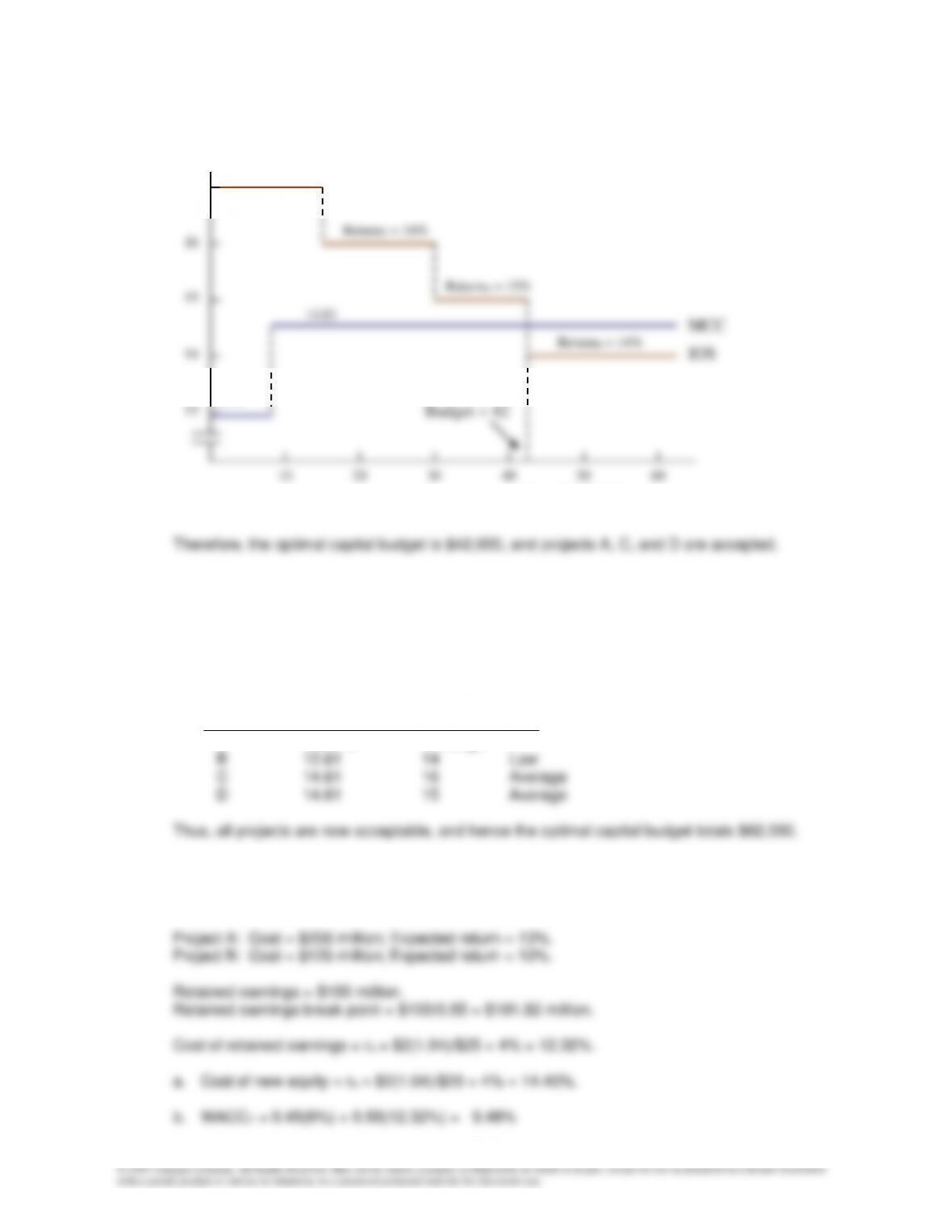

20

New Capital ($ millions)

8.4

9.9

10.5

10.2

MCC

IOS

Optimal Capital Budget

Principles of Finance 5e Chapter 12

Besley/Brigham

12-7

12–20 The firm’s marginal cost of capital is 14.61 percent. Thus, Project A (high–risk) should be evaluated

at a risk-adjusted cost of capital of 16.61 percent, while Project B (low-risk) should be evaluated at

12.61 percent. The average-risk projects (C and D) continue to be evaluated at 14.61 percent.

Now we have the following situation:

Risk-Adjusted Rate of

Project Cost of Capital Return Risk

A 16.61% 17%High

12–21 rd = 10%, rdT = rd(1 – T) = 10(0.6) = 6%.

Debt/Assets = 45%; D0 = $2; g = 4%; P0 = $25; NP = $20; T = 40%.

13

14

15

16

%

10

20

30

40

New Capital ($

th d )

14.61

ReturnA = 17%

12.96

IOS

Optimal Capital

Budget = 42

50

60

17

ReturnC = 16%

ReturnD = 15%

ReturnB = 14%

MCC

Chapter 12 Principles of Finance 6e

Besley/Brigham

12-8

12–22 a.

%3.16163.007.0093.007.0

23$

14.2$

g

P

D

ˆ

r

0

1

s==+=+=+=

12–23 a. Solving directly, $6.50 = $4.42(1+g)5

12–24 a. Retained earnings = ($30 million)(1 – Payout) = ($30 million)(0.60) = $18 million.

12–25 a.

g

P

D

ˆ

r

0

1

s+=

Principles of Finance 5e Chapter 12

Besley/Brigham

60.3$

b. Current EPS $5.40

Less: Dividends per share 3.60

12–26 a. Common equity needed: 0.50($70,000,000) = $35,000,000.

b. Expected internally generated equity (retained earnings) is $13.5 million. External equity

needed is as follows:

c. Cost of equity:

rs = Cost of retained earnings

000,500,13$

earnings retained Estimated

Chapter 12 Principles of Finance 6e

Besley/Brigham

12–10

f.

12–27 a. After-tax cost of new debt: rd(1 – T) = 9%(1 – 0.4) = 5.4%.

Cost of common equity from retained earnings:

Calculate g as follows:

65$

P

0

b. WACC1 calculation:

After-tax Weighted

Component Weight x Cost = Cost

Principles of Finance 5e Chapter 12

Besley/Brigham

12–11

c. For the capital structure to remain optimal, retained earnings must comprise 60 percent of total

new financing before external equity is sold.

Retained earnings for 2015:

d. Cost of new equity:

From Part a,

1

D

ˆ

= $4.63 and g = 8%. The cost of new equity is as follows:

12–28 a. A break point will occur each time a low-cost type of capital is used up. We establish the break

points as follows, after first noting that LEI has $24,000 of retained earnings:

Retained earnings = (Total earnings)(1.0 – Payout)

structure capital the in capital of type this of Proportion

Break Break

Type of Capital Break Point Calculation Point Number

Retained earnings

0.60

$24,000

BPRE =

= $40,000 2

$12,000$24,000

+

0.25

Summary of break points:

12–12

(1) There are three common equity costs and hence two changes and, therefore, two

(2) The numbers in the fourth column of the table designate the sequential order of the

(3) The first break point occurs at $20,000, when the 12 percent debt is used up. The

b. Component costs within indicated total capital intervals are as follows:

Retained earnings (used in interval $0 to $40,000):

g

P

g)(1D

ˆ

g

P

D

ˆ

r

0

0

0

1

s

+

+

=+=

Preferred with F = 5% ($0 to $50,000):

)F0.1(P

D

ˆ

r

0

p

ps

−

=

Principles of Finance 5e Chapter 12

Besley/Brigham

12–13

c. WACC calculations within indicated total capital intervals:

(1) $1 to $20,000 (debt = 7.2%, preferred = 11.58%, and retained earnings [RE] = 15.54%):

(3) $40,001 to $50,000 (debt = 9.6%, preferred = 11.58%, and equity = 16.27%):

WACC3 = 0.25(9.6%) + 0.15(11.58%) + 0.60(16.27%) = 13.90%

d. Expected return calculation for Project E using a financial calculator:

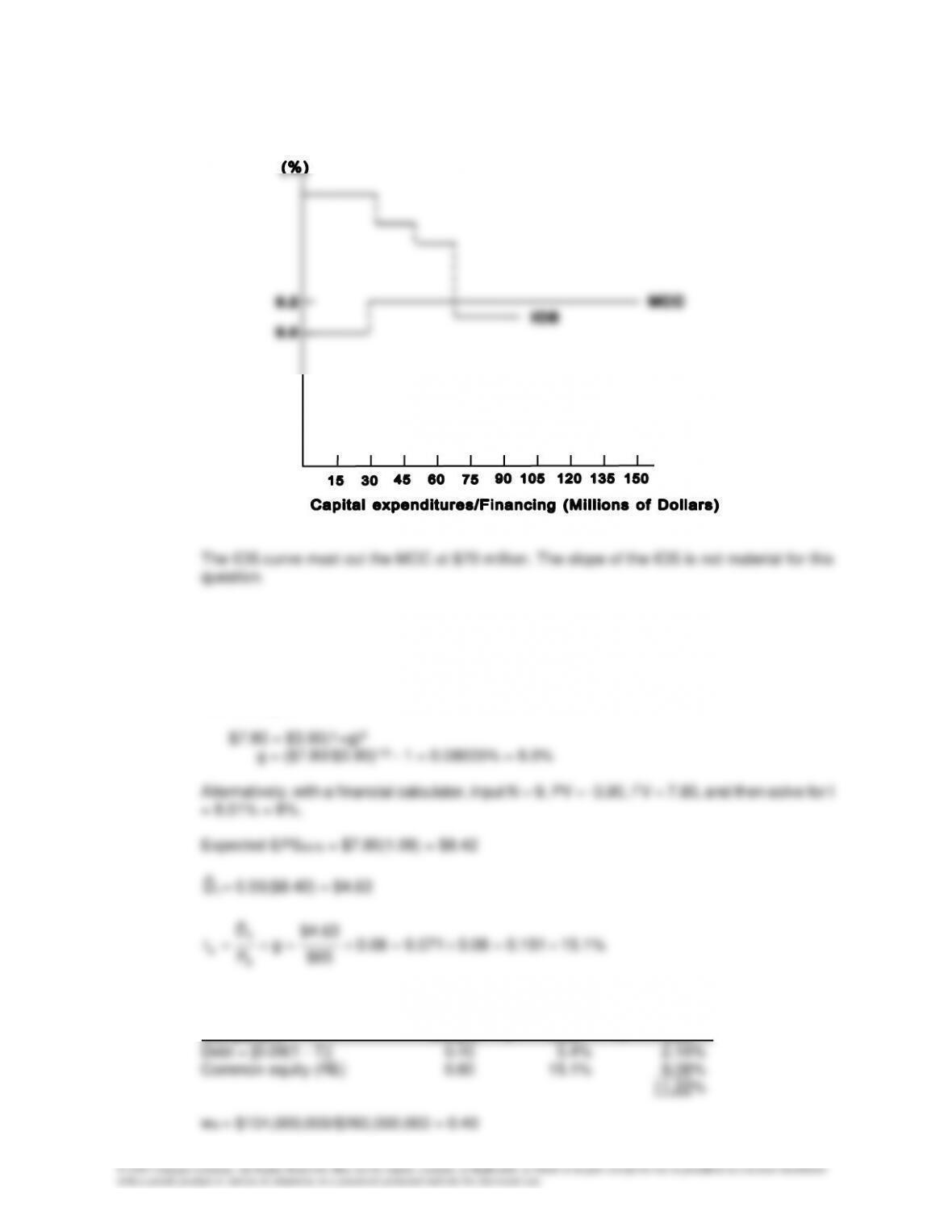

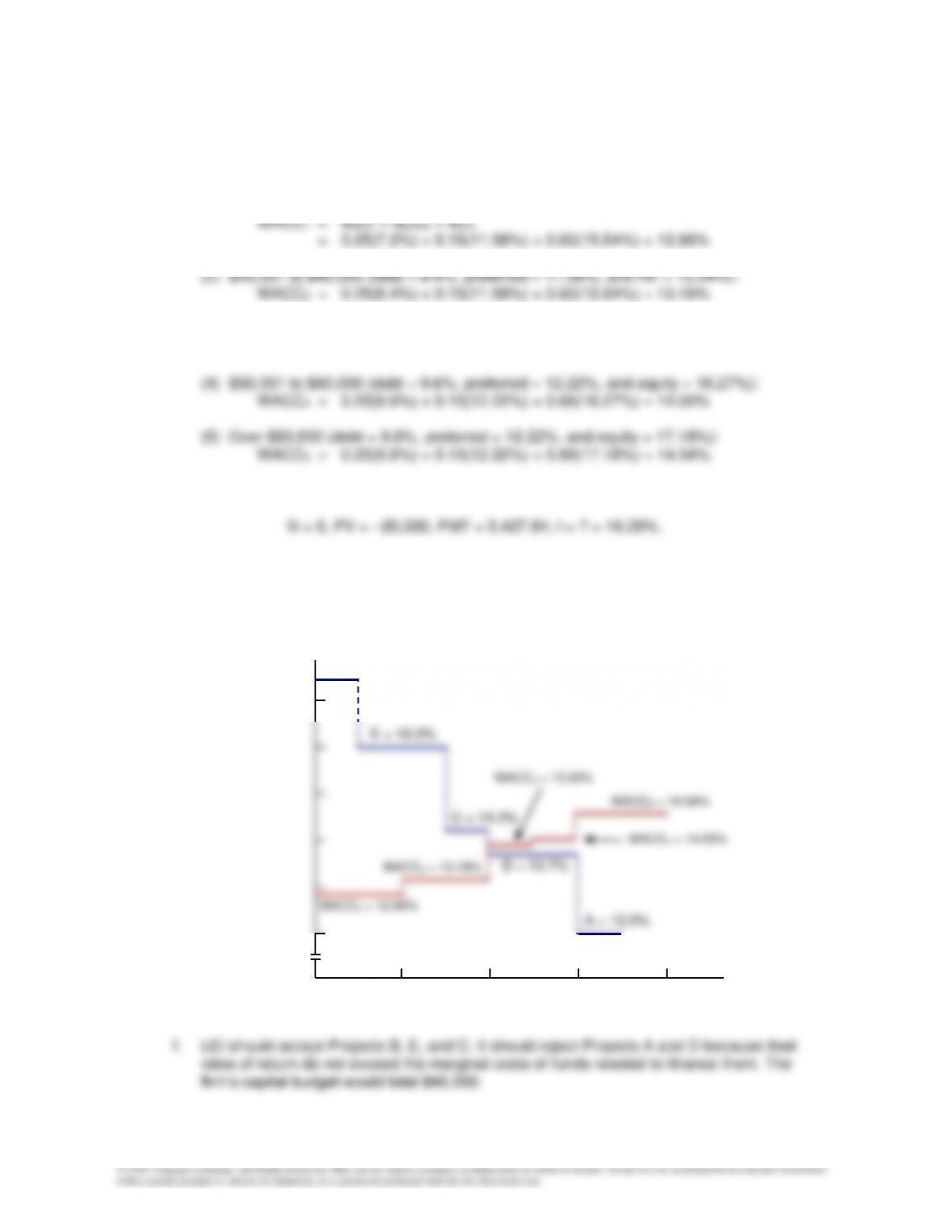

e. See the graph of the MCC and IOS schedules for LEI.

20 40 60 80

New funds (capital)

($ thousands)

Percent

B = 17.4%

E = 16.0%

C = 14.2%

D = 13.7%

A = 12.0%

WACC1 = 12.86%

WACC2 = 13.16%

WACC3 = 13.90%

WACC5 = 14.54%

WACC4 = 14.00%

LEI: MCC and IOS Schedules

12–14

12-29 a. There are three breaks in the MCC schedule. These breaks occur as follows:

Break #1 (New debt—9%): $500,000/0.45 = $1,111,111

b. (1) Cost below first break: Total funds of $1 to $1,111,111

After-tax Weighted

Component Weight x Cost = Cost

(2) Cost between first and second breaks: Total funds of $1,111,112 to $1,818,182

After-tax Weighted

(3) Cost between second and third breaks: Total funds of $1,818,183 to $2,000,000

After-tax Weighted

Component Weight x Cost = Cost

(4) Cost above third break: Total funds greater than $2,000,000

After-tax Weighted

Component Weight x Cost = Cost

*Cost of retained earnings:

$22

P

0

**Cost of external equity: