Chapter 11 Principles of Finance 6e

Besley/Brigham

11–12

The T-bills are risk-free in the default risk sense because the 8 percent return will be

realized in all possible economic states. However, remember that this return is composed

(2) High Tech’s returns move with, and thus are positively correlated with, the economy,

b. The expected rate of return,

r

ˆ

, is expressed as follows:

=

=

n

1i

ii rr

ˆPr

c. (1) The standard deviation is calculated as follows:

i

n

1i

2

i

2)r

ˆ

r( Pr

=

−==

440.401276.106952.61704.2272.75236.155

%)4.17%0.50(1.0%)4.17%0.35(2.0

%)4.17%0.20(4.0%)4.17%0.2(2.0%)4.17%0.22(1.0

22

2222

Tech High

=++++=

−+−+

−+−−+−−=

11–13

(2) The standard deviation is a measure of a security’s (or a portfolio’s) total, or stand-alone,

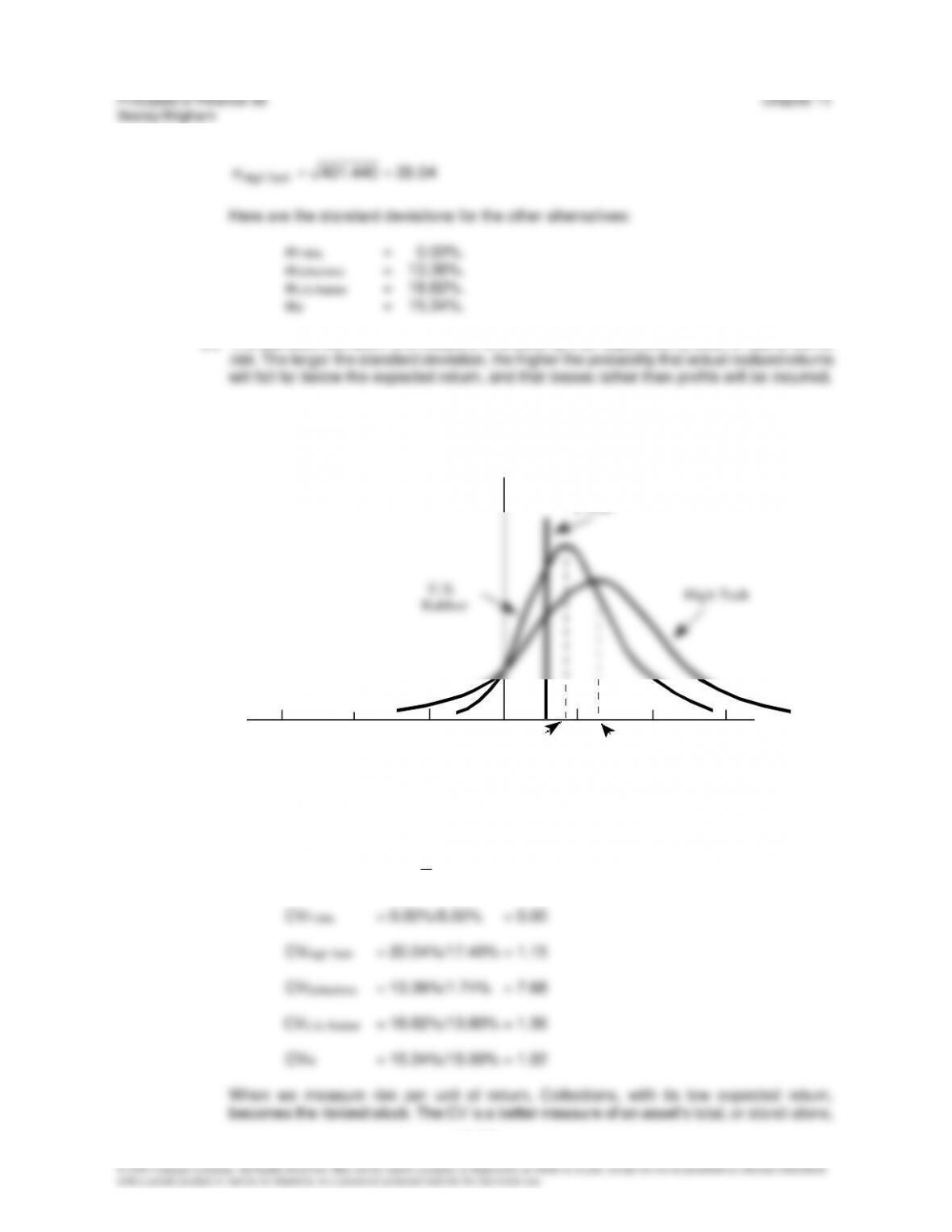

(3) Probability distribution curves for High Tech, U.S. Rubber, and T-bills are shown here:

–45 –30 –15 15 30 45

13.8 17.4

T-bills

High Tech

U.S.

Rubber

Probability

Rate of

Return

(%)

d. The coefficient of variation (CV) is a standardized measure of dispersion about the expected

value; it shows the amount of risk per unit of return.

r

ˆ

CV

Variation

of tCoefficien

==

Chapter 11 Principles of Finance 6e

11–14

e. (1) To find the expected rate of return on the two-stock portfolio, we first calculate the rate of

return on the portfolio in each state of the economy. Because we have half of our money in

the other states of the economy, and get these results:

State Portfolio

Recession 3.00%

Alternatively, we could apply this formula:

The standard deviation of the portfolio is:

129.11948.2717.1074.0074.2316.4

%)57.9%0.15(1.0%)57.9%50.12(2.0

%)57.9%00.10(4.0%)57.9%35.6(2.0%)57.9%00.3(1.0

22

2222

P

=++++=

−+−+

−+−+−=

%336.3129.11

P==

CVP = 3.336%/9.57% = 0.349

(2) Using either σ or CV as our total risk measure, the total risk of the portfolio is significantly

Principles of Finance 6e Chapter 11

Besley/Brigham

11–15

f.

–45 –30 –15 15 30 45

Probability

Rate of

Return

(%)

Portfolio of

Similar Stocks

Single-Stock

Portfolio

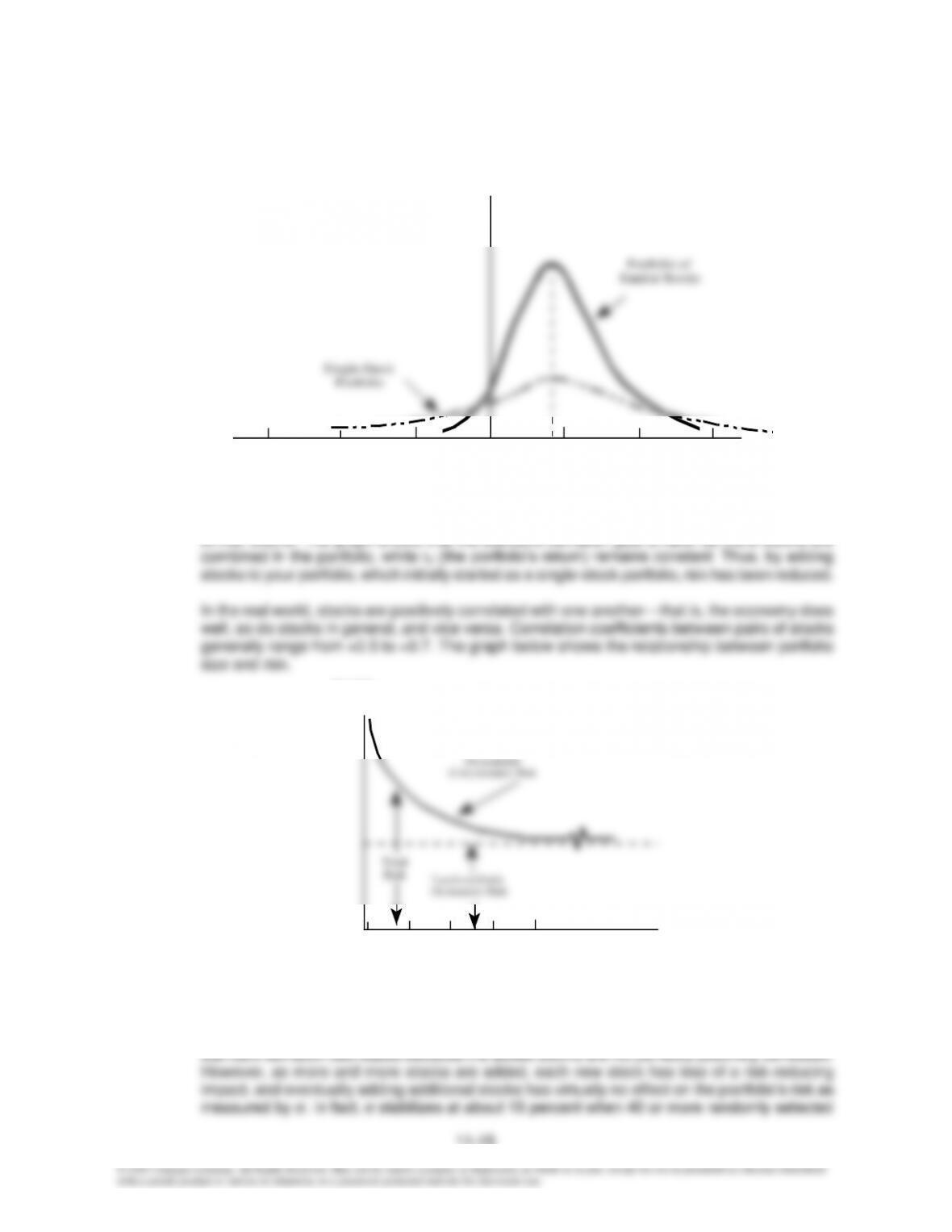

This graph shows the probability distributions for a one-stock portfolio and a portfolio of many

similar stocks. The graph shows that the standard deviation gets smaller as more stocks are

Portfolio

Risk, FP (%)

Number of

Stocks

Total

Risk Nondiversifiable

(Systematic) Risk

Diversifiable

(Unsystematic) Risk

10 20130 40

Chapter 11 Principles of Finance 6e

Besley/Brigham

11–16

g. (1) Portfolio diversification does affect investors’ views of risk. A stock’s total, or stand-alone,

risk as measured by its σ or CV, might be important to an undiversified investor, but it is not

(2) If you hold a one-stock portfolio, you will be exposed to a high degree of risk, but you won’t

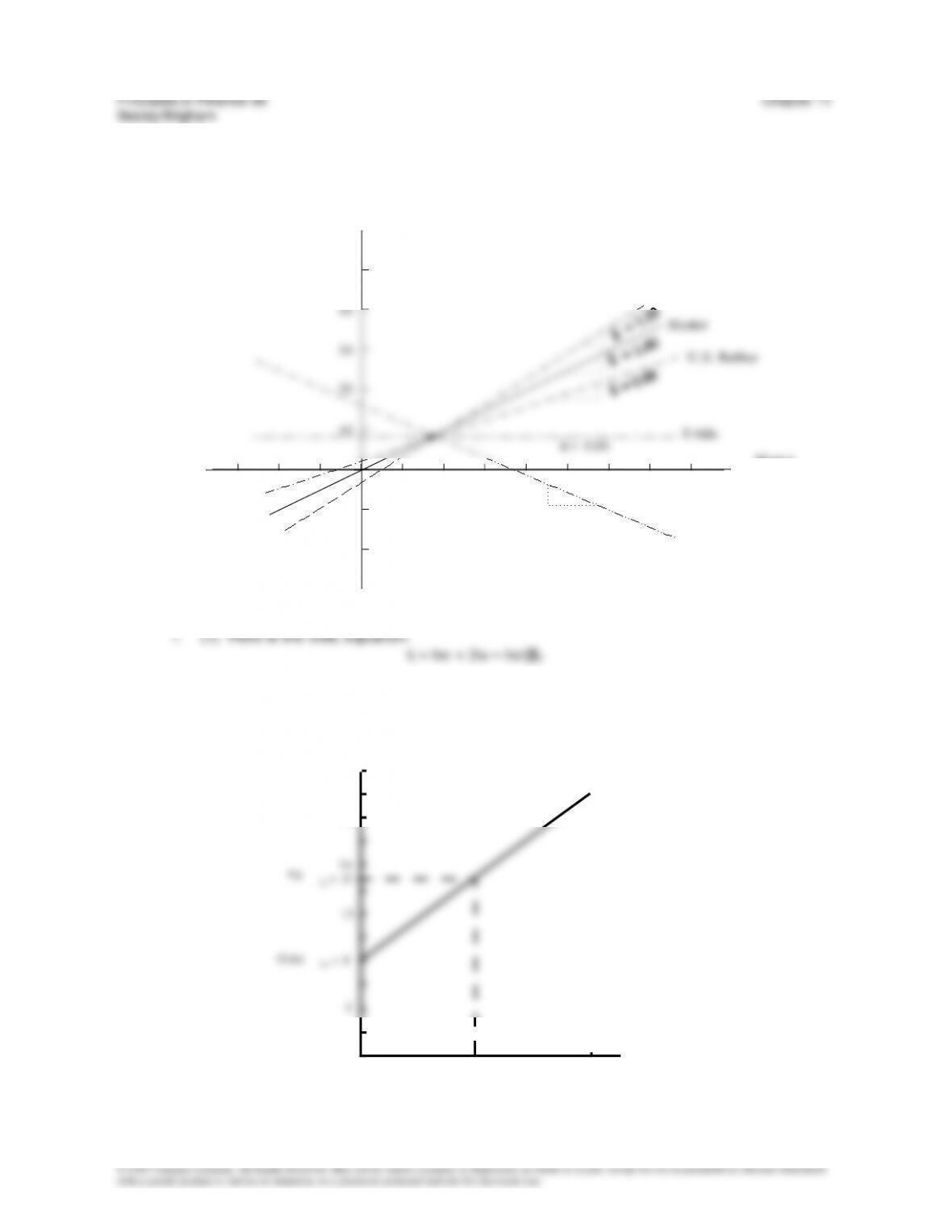

h. (1) Draw the framework of the graph, put up the data, plot the points for the market (45° line)

and connect them, and then get the slope as δY/δX = 1.0.) State that an average stock, by

(3) We do not yet have enough information to choose among the various alternatives. We

(4)

-10 10 20 30 40

50

40

30

20

10

-10

-20

Stock

Return

(%)

Market

Return

(%)

High Tech

Market

U.S . Rubber

T-bills

Collections

ß = -0.86

ß = 0.00

•

Characteristic Lines

If we use the T-bill yield as a proxy the risk-free rate, then rRF = 8%. Further, our estimate

of rM =

r

ˆ

is 15%. Thus, the SML is drawn as follows:

24

20

16

12

k

(%)

kM = 15

SML

r

(%)

rM

Chapter 11 Principles of Finance 6e

Besley/Brigham

(2) Using the SML equation, we have the following relationships:

Expected Required

Return Return

Security (

r

ˆ

) (r) Condition

High Tech 17.4% 17.0% undervalued:

r

ˆ

> r

r

ˆ

These returns are plotted on the SML graph next.

012

24

20

16

12

kT-BILLS = 8

4

B eta ( ß )

k

(%)

kM = 15

SML

•

•

Hig h Tec h

U.S.

R ub ber

-1

•C ol lec ti on s

•

•

The T-bills and market portfolio plot on the SML, High Tech and U.S. Rubber plot above

(3) Collections is an interesting stock. Its negative beta indicates negative market risk—

including it in a portfolio of “normal” stocks will lower the portfolio’s risk. Therefore, its

r

(%)

rM

rT-bill

Principles of Finance 6e Chapter 11

Besley/Brigham

j. (1) This effect is graphed next.

012

24

20

16

12

8

4

B ETA ( ß )

k

(%)

C HA N GES I N TH E S ML

-1

ORIGINAL

SITUATION

IN CR EASED

INFLATION

IN CR EASED

R ISK AVER SION

Here we have plotted the SML for betas ranging from 0 to 2.0. The base case SML is

r (%)

Chapter 11 Principles of Finance 6e

Besley/Brigham

Stock A Stock B Stock C Portfolio

2011 –18.00% –14.50% 32.00% –0.17%

Principles of Finance 6e Chapter 11

Besley/Brigham

11–21

• Should RIP be more concerned with return than risk when making its decision about the PAIDs?

This question follows the above discussion. The short, simple answer is “absolutely not.” There are

• If the PAIDs are recommended, what should RIP tell its customers?

RIP could find itself in a great deal of trouble, both financially and legally, if it doesn’t fully disclose any

• Would you recommend the PAIDs?

References:

The scenario presented here parallels the well-publicized cases of (1) Orange County, California that came

to light in 1994 and (2) Long-Term Capital Management L.P. Orange County lost billions of dollars with its

investment fund, apparently because the managers of the fund did not fully understand the risk ramifications

of some of the investments in the portfolio, especially derivatives. Long-Term Capiôal Management L.P.,

which employed complex arbitrage strategies to construct investment qosi|ions that were suppose to

generate positive returns in any type of market, was “bailed out” of bankruptcy only after large financial

institutions provided nearly $4 billion.

The following articles offer interesting insights into what caused Orange County’s problems:

“Untangling the Derivative Mess,” Fortune, March 20, 1995, p. 50+.

“Orange County is Looking Green Around the Gills,” Business Week, December 26, 1994, p. 66+.

“Derivatives Lead to a Huge Loss in Public Fund,” The Wall Street Journal, December 2, 1994, p. A3+.

“Bitter Fruit in Orange County,” Business Week, May 30, 1994, p. 44+.

The following articles describe some of the complexities and the reasons for the trouble at Long-Term

Capital Management L.P.:

“Failed Wizards of Wall Street: Can You Devise Surefire Ways to Beat the Markets? The Rocket Scientists

Thought They Could. Boy Were They Wrong,” Business Week, September 21, 1998, p. 114.

“Bailout Blues: How a Big Hedge Funds Marketed Its Expertise and Shrouded Its Risk; Regulators and

Chapter 11 Principles of Finance 6e

Besley/Brigham

Lenders Knew Little About the Gambles At Long-Term Capital; ‘Stardust in Investors’ Eyes,” The Wall Street

Journal, September 25, 1998, p. A1+.

“A House Built on Sand. John Meriwether’s Once-Mighty Long-Term Capital Has All But Crumbled. So Why

Did Warren Buffett Offer to Buy It?,” Fortune, October 26, 1998, p. 110+.