10–19

(6) Default risk is inherent in all bonds except Treasury bonds. The question here is: Will the

issuer have the cash to make the promised payments? Bonds are rated from AAA to D,

b. The value of any asset is the present value of its expected future cash flows:

0 1 2 3 N-1 N

1

CF

2

CF

3

CF

1N

CF −

N

CF

c. The value of a bond is merely the present value of its expected future cash flows:

0 1 2 3 N-1 N

INT INT INT INT INT

A bond has a specific cash flow pattern consisting of a stream of constant interest payments

plus the return of par at maturity. The annual coupon payment is the cash flow: pmt = (coupon

rate) x (par value) = 0.1($1,000) = $100. For a one-year bond, we have this cash flow time line

situation:

Expressed as an equation, we have:

…

r%

…

rd%

Chapter 10 Principles of Finance 6e

Besley/Brigham

$1,000. $909.09 + $90.91

)10.1(

000,1$

)10.1(

100$

V11

d

==

+=

Numerical (regular calculator) solution: Given above.

Financial calculator solution: Input N = 1, I/Y = 10, PMT = 100, and FV = 1,000; compute PV =

–1,000

Spreadsheet solution: Use the PV financial function that is available on the spreadsheet.

For a 10-year, 10 percent annual coupon bond, the bond’s value is found as follows:

0 1 2 3 9 10

Numerical (regular calculator) solution:

)10.1(

1

000,1$

10.0

1

100$

)r1(

1

M

r

1

INTV 10

)10.1(

1

N

d

d

)r1(

1

d

10

N

d

+

−

=

+

+

−

=+

d. (1) Numerical (regular calculator) solution:

)13.1(

1

000,1$

13.0

1

100$

)r1(

1

M

r

1

INTV 10

)13.1(

1

N

d

d

)r1(

1

d

10

N

d

+

−

=

+

+

−

=+

10%

…

Principles of Finance 6e Chapter 10

10–21

(2) In the second situation, where rd falls to 7 percent, the price of the bond rises above par.

Just change rd from 13 percent to 7 percent. We see that the value of the 1-year bond rises

Numerical (regular calculator) solution:

)07.1(

1

000,1$

07.0

1

100$

)r1(

1

M

r

1

INTV 10

)07.1(

1

N

d

d

)r1(

1

d

10

N

d

+

−

=

+

+

−

=+

(3) Assuming that interest rates remain at the new levels (either 7 percent or 13 percent), we

could find the bond’s value as time passes, and as the maturity date approaches. If we

then plotted the data, we would find the situation shown in the following graph:

At maturity, the value of any bond must equal its par value (plus accrued interest). As a

e. (1) The yield to maturity (YTM) is the discount rate that equates the present value of a

bond’s cash flows to its price—that is, it is the promised rate of return on the bond.

Bond Value, Vd

($)

Time Path of Bond Value When rd (10%) = Coupon Rate (10%)

Market Price = Par Value: Par Bond

Time Path of Bond Value When rd (13%) > Coupon Rate (10%)

Market Price > Par Value: Discount Bond

M = $1,000

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–22

(Note that the expected rate of return is less than the YTM if some probability of default

exists.) On a cash flow time line, we have the following situation when the bond sells for

$887:

0 1 2 3 9 10

We want to find rd in this equation:

.

)r+ (1

M

+

)r + (1

INT

+ … +

)r + (1

INT

=PV = V

d

N

d

N

d

1

d

We can estimate the YTM using the following computation:

+ INT

Maturity to Yield

eApproximat

3

M + )V (2

N

V – M

d

d

=

Spreadsheet solution: use the rate financial function that is available on the spreadsheet.

We can tell from the bond’s price, even before we begin the calculations, that the YTM

(2) The current yield is defined as follows:

bond the of price Current

Yield

The capital gains yield is defined as follows:

10%

…

Principles of Finance 6e Chapter 10

Besley/Brigham

10–23

yearthe of beginning the at Price

Yield

The total expected return is the sum of the current yield and the expected capital gains

yield:

yieldcurrent

return total

The term yield to maturity, or YTM, is often used in discussing bonds. It is simply the

Recall also that securities have required returns, r, which depend on a number of factors:

Required return = r = r* + IP + LP + MRP + DRP

The capital gains yield calculation can be checked by asking this question: “What is the

expected value of the bond one year from now, assuming that interest rates remain at

current levels?” This is the same as asking: “What is the value of a 9-year, 9 percent

annual coupon bond if its YTM (its required rate of return) is 10.91 percent?” The answer,

using a financial calculator, is $893.87. With this data, we can now calculate the bond’s

capital gains yield as follows:

When the bond is selling for $1,134.20 and providing a total return of r = YTM = 7.08%, we

have this situation:

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–24

f. Vd = $887.00

Financial calculator solution: Input N = 5, PV = -887, PMT = 90, and FV = 1,090; compute

I/Y = 13.63%

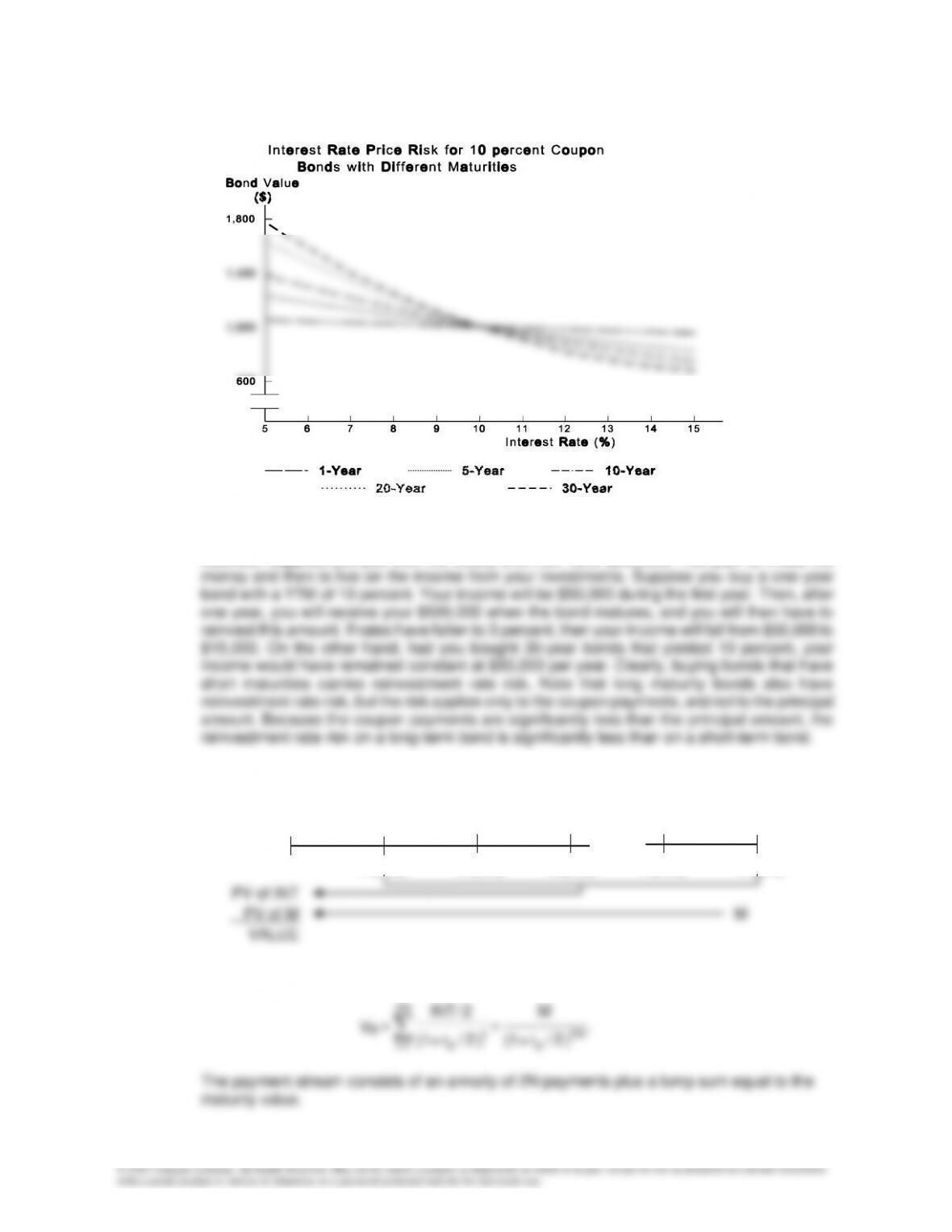

g. Interest rate price risk, which is often just called price risk, is the risk that a bond will lose value

as the result of an increase in interest rates. Earlier, we developed the following values for a 10

percent, annual coupon bond:

Maturity

r 1-year Change 10-year Change

7% $1,028 $1,211

Principles of Finance 6e Chapter 10

Besley/Brigham

10–25

h. Interest rate reinvestment rate risk is defined as the risk that cash flows (interest plus principal

repayments) will have to be reinvested in the future at rates different than today’s rate. To

illustrate, suppose you just won the lottery and now have $500,000. You plan to invest the

i. In reality, virtually all bonds issued in the U.S. have semiannual coupons and are valued using

the setup shown below:

Periods 0 1 2 3 n-1 n

PMT/2 PMT/2 PMT/2 PMT/2 PMT/2

We would use this equation to find the bond’s value:

.

)

2/r + (1

M

+

)

2/r + (1

2INT/

=

VN2

d

t

d

N2

1=t

B

The payment stream consists of an annuity of 2N payments plus a lump sum equal to the

maturity value.

r%/2

…

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–26

For a 10 percent, semiannual payment, 1-year bond, semiannual interest = annual coupon/2 =

$100/2 = $50 and N = 2(years to maturity) = 2(1) = 2. To find the value of the bond with a

financial calculator, enter N = 2, rd/2 = I/Y = 5, PMT = 50, FV = 1000, and then compute PV = –

$1,000.

i. The semiannual payment bond would be better. Its ear would be:

10.25%.1025.0 = 1

2

0.10

+ 1 = 1

m

r

+ 1 = r

2

SIMPLE

m

EAR =−

−

k. The value of a perpetuity is simply:

r

PMT

=

Vd

Principles of Finance 6e Chapter 10

Besley/Brigham

10–27

Thus:

$1,428.57 =

0.07

$100

=

V

$769.23 =

0.13

$100

=

V

$1,000.00 =

0.10

$100

=

V

7%

13%

10%

Perpetual bonds actually have the most interest rate risk of any coupon bond—their value

changes the most as interest rates change. (However, a zero coupon bond can be more

volatile than even a perpetuity. The controlling factor is duration, which we do not discuss in

this book.)

10-43 Integrative Problem

a. Preferred stock generally pays a constant dividend, whereas common stock often pays variable

dividends. Neither preferred stock nor common stock has a maturity. Whether preferred or

b. (1) The value of any stock is the present value of its expected dividend stream:

.

)r + (1

D

ˆ

+ . . . +

)r + (1

D

ˆ

+

)r + (1

D

ˆ

+

)r + (1

D

ˆ

=

P

ˆ

ss

3

3

s

2

2

s

1

1

0

However, some stocks have dividend growth patterns that allow them to be valued

using short-cut formulas.

(2) A constant growth stock is one whose dividends are expected to grow at a constant rate

forever. “Constant growth” means that the best estimate of the future growth rate is

For a constant growth stock:

With this regular dividend pattern, the general stock valuation model can be

simplified to the following very important equation:

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–28

.

g –r

g) + (1

D

=

g – r

D

ˆ

=

P

ˆ

s

0

s

1

0

This is the well-known “Gordon,” or “constant–growth” model for valuing stocks. Here

1

D

ˆ

, is

the next expected dividend, which is assumed to be paid one year from now, rs is the

required rate of return on the stock, and g is the constant growth rate.

(3) The model is derived mathematically, and the derivation requires that rs > g. If g is greater

d. (1) Because Bon Temps is a constant growth stock, its dividend is expected to grow at a

constant rate of 6 percent per year. Expressed as a cash flow time line, we have the

following setup. Just enter $2 in your calculator; then keep multiplying by 1 + g = 1.06 to

get

1

D

ˆ

,

2

D

ˆ

, and

3

D

ˆ

:

0 1 2 3

2

3

ˆ

ˆ

ˆ

(2) We could extend the cash flow time line on out forever, find the value of Bon Temps’

dividends for every year on out into the future, and then the PV of each dividend,

$21.20. =

0.10

$2.12

=

0.06 – 0.16

$2.12

=

g –

r

D

ˆ

=

P

ˆ

s

1

0

(3) After one year,

1

D

ˆ

will have been paid, so the expected dividend stream will then be

2

D

ˆ

,

3

D

ˆ

,

4

D

ˆ

, and so forth. Thus, the expected value one year from now is $22.47:

47.22$

06.016.0

2472.2$

gr

D

ˆ

P

ˆ

s

2

1=

−

=

−

=

(4) The expected dividend yield in any year n is

1n

P

ˆ

Yield

−

16%

Principles of Finance 6e Chapter 10

Besley/Brigham

10–29

and the expected capital gains yield is

e. The constant growth model can be rearranged to this form:

.g +

P

D

ˆ

=r

ˆ

0

1

s

Here the current price of the stock is known, and we solve for the expected return. For Bon

Temps:

s

r

ˆ

= $2.12/$21.20 + 0.060 = 0.100 + 0.060 = 16%.

f. If Bon Temps’ dividends were not expected to grow at all, then its dividend stream would be a

perpetuity. Perpetuities are valued as shown below:

0 1 2 ∞-1 ∞

2 2 2 2

$12.50

Note that preferred stock is generally a perpetuity, so it can be valued with this formula.

16.0

r

s

g. Bon Temps no longer is a constant growth stock, so the constant growth model is not

16%

…

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–30

0 1 2 3 4 ∞

Simply enter $2 and multiply by (1.30) to get

1

D

ˆ

= $2.60; multiply that result by 1.3 to get

2

D

ˆ

=

$3.38, and so forth. Then, recognize that after Year 3, Bon Temps becomes a constant growth

The dividend yield in Year 1 is 6.95 percent, and the capital gains yield is 9.05 percent:

9.05% = 6.95% – 16.00% ield YainsG Capital

6.95% = 0.0695 =

$37.410

$2.600

ield YividendD

=

=

During the nonconstant growth period, the dividend yields and capital gains yields are not

h. Now we have this situation:

0 1 2 3 4 ∞

During Year 1:

11.07% = 0.1107

$18.07

$2.00

ield YividendD

==

16%

…

g1=30%

g3=30%

gn=6%

g1=30%

gn=6%

Principles of Finance 6e Chapter 10

Besley/Brigham

10–31

i. The company is earning something and paying some dividends, so it clearly has a value

greater than zero. That value can be found with the constant growth formula, but where g is

negative:

Because it is a constant growth stock:

10-44 Computer-Related Problem

a. INPUT DATA: KEY OUTPUTS:

Supernormal growth 12.00% Current price (P0) $31.50

Normal growth rate 4.00% Price at the end of Year 5 $40.09

MODEL-GENERATED DATA:

Expected dividends: PV of dividends:

Year 1 1.9600 Year 1 1.7500

Stock price—end of Year 1 40.09 Stock price—beginning of Year 1 31.50

Yields in Year 1 Yields in Year 1

b. (1) r = 13%

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–32

INPUT DATA: KEY OUTPUTS:

Supernormal growth 12.00% Current price (P0) $27.86

Normal growth rate 4.00% Price at the end of Year 5 $35.64

Req. rate of return 13.00% Dividend yield in Year 1 7.03%

b. (2) r = 15%

INPUT DATA: KEY OUTPUTS:

Supernormal growth 12.00% Current price (P0) $22.59

MODEL-GENERATED DATA:

Expected dividends: PV of dividends:

Year 1 1.9600 Year 1 1.7043

Principles of Finance 6e Chapter 10

Besley/Brigham

10–33

Yields in Year 5 Yields in Year 1

b. (3) r = 20%

INPUT DATA: KEY OUTPUTS:

Supernormal growth 12.00% Current price (P0) $15.20

Normal growth rate 4.00% Price at the end of Year 5 $20.05

MODEL-GENERATED DATA:

Expected dividends: PV of dividends:

Year 1 1.9600 Year 1 1.6333

Yields in Year 5 Yields in Year 1

ETHICAL DILEMMA

Which Arm Should You Choose—The Left or The Right?

Ethical dilemma:

As a loan officer for FIFO, Alan’s job is to sell loans that generate revenues for the company. Alan has

been charged with increasing the amount of mortgages that are sold by FIFO. One of the loans that

FIFO wants to emphasize is a new mortgage called an option ARM. The primary benefit to the borrower

is that the monthly amount that is paid in the early years of the mortgage can be set so that he or she

can afford to purchase a house. However, this benefit leads to the primary disadvantage associated

with an option ARM. The difference between the principal and interest that would be paid on an

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–34

equivalent conventional mortgage and the amount paid on the option ARM is added to the amount owed

by the borrower. As a result, the borrower generally owes more than the original principal amount when

the option ARM converts to a conventional mortgage. When the option ARM becomes a conventional

mortgage in three to five years, the monthly payments can increase more than five fold, which becomes

a significant burden to the borrower. If the borrower cannot afford the new, substantially higher

payments, then he or she will default on the mortgage and lose the house.

Discussion questions:

• Is there an ethical problem? If so, what is it?

In this case, the ethical situation would be the manner in which FIFO conducts its lending business.

Apparently FIFO has an unwritten policy that the loan officers should provide only information that is

required by law. Thus, loan officers are encouraged to withhold “bad” information that doesn’t have to

• Is FIFO’s policy about disclosing information to borrowers appropriate?

The dilemma is what information FIFO’s loan officers should provide to prospective borrowers. What

obligation, does FIFO have to provide information and advice to its customers beyond what is required

• What would you do if you were Alan?

In any business, especially a service-oriented business, reputation is very important. If FIFO does not

treat its customers appropriately, the word will spread around the industry and the company will lose

Chapter 10

10–35

References:

The following articles might be assigned for background material:

James R. Hagerty, “Mortgage Brokers: Friends or Foes?” The Wall Street Journal Online, May 24, 2007.