Principles of Finance 6e Chapter 10

Besley/Brigham

10-1

CHAPTER 10

ANSWERS

10-1 The value of any asset is determined by computing the present value of the future cash flows htat

10-2 The price of the bond will fall and its YTM for other investors will rise if interest rates rise. If the bond

10-4 The yield to maturity (YTM) represents the average rate of return that an investor will earn if he or

10-5 True. The value of a share of stock is the PV of its expected future dividends. If the two investors

10-6 Yes. All else equal, if a company decides to increase its dividend payout ratio, then the dividend

10-7 If investors demand a higher required rate of return for investing in AT&T stock, then, all else equal,

the price of the stock must to drop to provide the higher return. In our valuation model, the value for

10-8 Investors who have sufficient income to support their chosen life styles often purchase stocks that

Chapter 10 Principles of Finance 6e

10-9 The par value of a common stock has no direct relationship to its market value. The market value is

10–10 Effect on Value

a. Investors require a higher rate of return to buy the stock. –

(The price of the stock must decrease so that the return that is

expected by new investors equals the higher rate of return.)

10–11 The general principle behind valuing a real asset is the same as for a financial asset. The principal

________________________________________________________

SOLUTIONS

10-1 Calculator solution: Input N = 12, I/Y= 6, PMT = 40, and FV = 1,000, compute PV = -832.32.

1

000,1

1

40V12

)06.1(

1

d

12

+

−

=

10-3 a. The bonds now have n = 8 x 2 = 16 interest payments remaining until maturity, and their value

is calculated as follows:

22.251,117.62305.628)62317.0(000,1)61102.12(50

)03.1(

1

000,1

03.0

1

50V16

)03.1(

1

d

16

=+=+=

+

−

=

Calculator solution: Input N = 16, I/Y= 3, PMT = 50, and FV = 1,000, compute PV = -1,251.22.

b. The price of the bond will decline from $1,251.22 toward $1,000, hitting $1,000 (plus accrued

interest) at the maturity date eight years (16 six-month periods) from now (assuming the firm

does not default).

10-4 a. Calculator solution: Input N = 20, I/Y= 5, PMT = 35, and FV = 1,000, compute PV = -813.07.

07.813889.3761774.436)376889.0(000,1)46221.12(35

)05.1(

1

000,1

05.0

1

35V10

)05.1(

1

d

20

=+=+=

+

−

=

b. The price of the bond will increase from $813.77 toward $1,000, hitting $1,000 (plus accrued

interest) at the maturity date (assuming the firm does not default).

10-5

85$

08.0

80.6$

r

D

=

P

ˆ

ps

0==

08.0

r

ps

0==

10-8

20.5$)04.1(5$D

ˆ1==

20.5$

g) + (1

D

D

ˆ

0

1

Chapter 10 Principles of Finance 6e

Besley/Brigham

53.1$

g) + (1

D

D

ˆ

0

1

Principles of Finance 6e Chapter 10

Besley/Brigham

10-5

10–13 a.

N

)r1(

1

d)r1(

M

r

1

PMTV

N

+

+

−

=+

Calculator solutions:

(1) 5%: Bond L: Input N = 15, I/Y= 5, PMT = 100, and FV = 1000; compute PV = -1,518.98

Bond S: Change N = 1; compute PV = -1,047.62

b. Think about a bond that matures in one month. Its present value is influenced primarily by the

maturity value, which will be received in only one month. Even if interest rates double, the price

10-14 a. Year Dividend

1 $2.100 = $2.000(1.05)

You will also receive the market price of the stick when you sell it in Year 3. The market price of

the stock in Year 3 will be:

431.2$

(1.05)2$

g) + (1

D

D

ˆ

4

4

0

4

070.

0.05– 20.1

g –

r

g –

r

s

s

0

10-6

10-15 D0 = $1

r = 7% + 6% = 13% = dividend yield + g

1

D

ˆ

=$1.000(1.50) = $1.5000

2

3

D

ˆ

=$1.875(1.06) = $1.9875

Nonconstant growth ends at the end of Year 2, thus

2

P

ˆ

can be computed using the constant growth

dividend discount model:

393.28$

06.013.0

9875.1$

gr

D

ˆ

P

ˆ

ns

3

2=

−

=

−

=

The current price is the present value of

1

D

ˆ

,

2

D

ˆ

, and

2

P

ˆ

:

03.25$

704.23$327.1$

=

+=

10-16 Calculate the dividend stream, and place them on a cash flow time line. Also, calculate the price of

the stock at the end of the supernormal growth period, and include it, along with Year 5 dividend.

D0 =

0D

ˆ

D

ˆ21 ==

3

D

ˆ

= 1.00

6

D

ˆ

0 1 2 3

…

g1 = 50% g2 = 25% gnorm = 6%

1.327 1.50 1.875

+ 28.393 = 1.9875/(0.13 – 0.06)

23.704 = 30.268

25.031

rs = 13%

Principles of Finance 6e Chapter 10

Besley/Brigham

)15.1(

7143.34$25.2$

)15.1(

50.1$

)15.1(

00.1$

)15.1(

0$

)15.1(

0$

P

ˆ54321

0

+

++++=

…

g1 = 50% g2 = 50% gnorm = 8%

0.6575 1.00 1.50 2.25

0.8576 + 34.7143 = 2.43/(0.15 – 0.08)

18.3778 = 39.9643

19.8929

rs = 15%

0 1 2 3 4 5 6

Chapter 10 Principles of Finance 6e

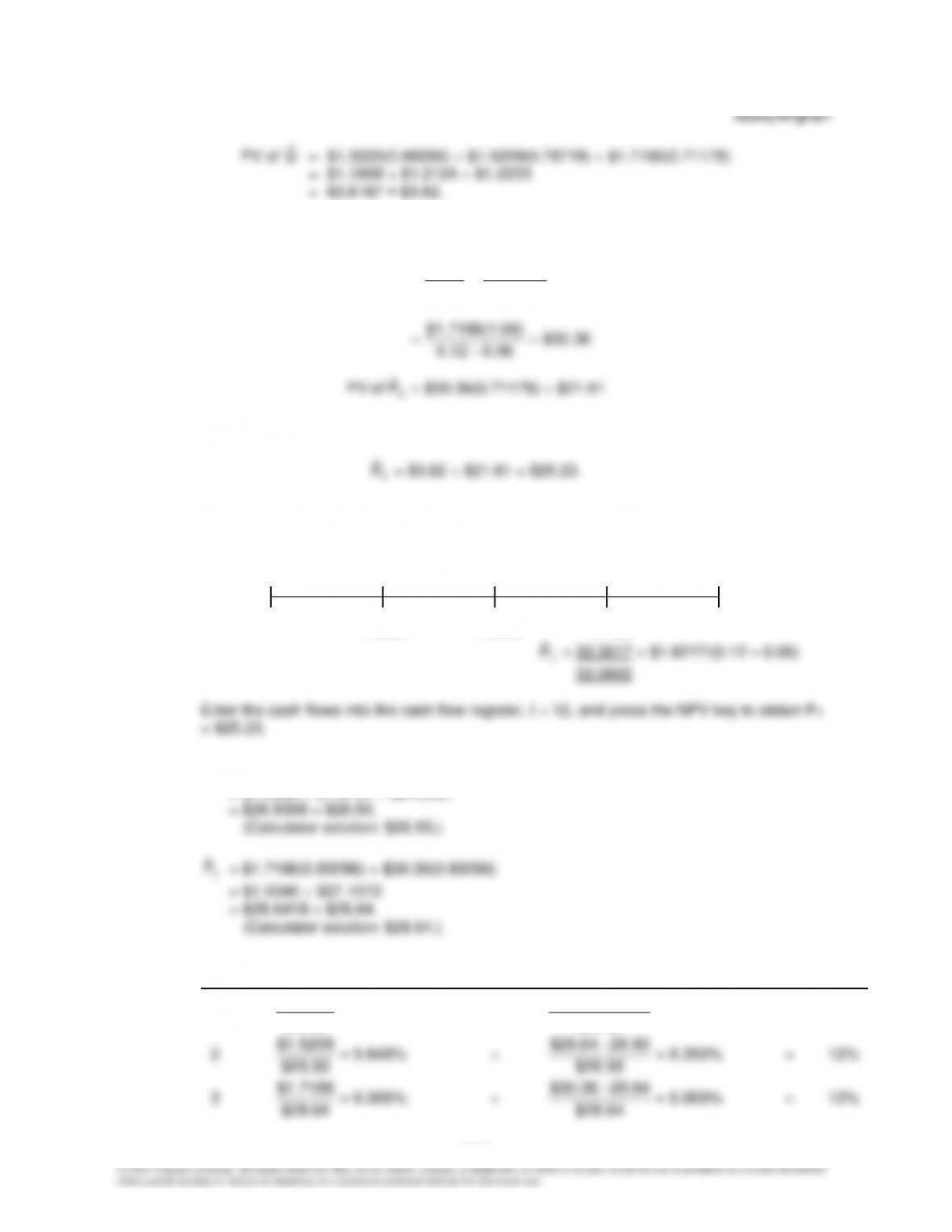

10-8

ˆ

(2) Find the PV of Snyder’s stock price at the end of Year 3:

$21.611178)$30.36(0.7P

ˆ

ofPV

0.060.12

06)$1.7186(1.

gr

g)(1D

ˆ

gr

D

ˆ

P

ˆ

3

s

3

s

4

3

==

−

−

+

=

−

=

(3) Sum the two components to find the value of the stock today:

Alternatively, the cash flows can be placed on a time line as follows:

0 1 2 3 4

g = 15% g = 13% g = 6%

1.3225 1.5209 1.7186

ˆ

b.

1

P

ˆ

= $1.5209(0.89286) + $1.7186(0.79719) + $30.36(0.79719)

= $1.3580 + $1.3701 + $24.2027

c. Dividend Capital Gains Total

Year Yield + Yield = Return

1

5.242%

$25.23

$1.3225

+

6.738%

$25.23

25.23–$26.93

= 12%

$1.5209

26.93–$28.64

$28.64

$28.64

12%

10-9

10-19 Calculator solution: Input N = 20, PV = -598.55, PMT = 25, and FV = 1,000, compute I/Y = 6.0 per

six months.

10–21 Calculator solution: Input N = 16, PV = -902.81, PMT = 30, and FV = 1,000, compute I/Y = 3.83 per

six months.

10-22

N

)r1(

1

d)r1(

M

r

1

PMTV

N

+

+

−

=+

; r = YTM

10–23 a. M = $1,000 = FV on the calculator

INT = 0.09($1,000) = $90 = PMT on the calculator

N = 4

b.

4

)12.1(

1

N

)r1(

1

d)12.1(

000,1

12.0

1

90

)r1(

M

r

1

PMTV

4N +

−

=

+

+

−

=+

10-24 Because it was a new issue, Robert paid $1,000 for the bond he purchased.

10–10

(2) Current yield = $80/$1,000 = 0.08 = 8.0%

10–25 Vd = INT/rd; therefore, rd = INT/Vd.

INT = 0.08($1,000) = $80

10-26 Bonds: Price $897.40, 20 years, PMT = $40 per 6 mos., N = 40 periods, M = $1,000

Preferred: $2/quarter forever, $95/share

10–27 The bond is selling at a large premium, which means that its coupon rate (C) is much higher than

the going market rate of interest (rd).

10–28 Total dollar return per share = ($21 – $15) + $0.90 = $6.90

Besley/Brigham

10-29 Total dollar return per share = ($27.50 – $25.00) + ($1.25) = $3.75

yield

gains

$25

$25.00

$25.00

return

60.12$

D

D

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–12

c. Return = ($1,042 – $889)/$889 + [2($40)]/$889

10–34

37.034,141.75996.274

)035.1(

000,1

035.0

1

40

)r1(

M

r

1

PMTV 8

)035.1(

1

N

)r1(

1

d

NN =+=+

−

=

+

+

−

=+

10–35 a. This is not necessarily true. Because G plows back two-thirds of its earnings, its growth rate

should exceed that of D, but D pays higher dividends ($6 versus $2). We cannot say which

stock should have the higher price.

10-36 a.

$1,250 =

0.08

$100

=

r

INT

=

V

d

d

Principles of Finance 6e Chapter 10

Besley/Brigham

10–13

(2) At 12%: Vd = $100(7.46944) + $1,000(0.10367) = $746.94 + $103.67 = $850.61

Calculator solution: Change I/Y = 12; compute PV = $850.61

10-37 a. The coupon interest is $50 = 0.05($1,000) per year, and the original yield to maturity was 5.0

percent; so both bonds would have sold for par, or for $1,000, at the time of issue. To see this,

compute the value of the IBM bond:

1

1

)

(1.05

$1,000

+

)

(1.05

$50

V

)05.1(

1

10t

10

1=t

IBM

10

−

=

b. On January 1, 2012, the IBM bond had a remaining life of nine9 years. Thus, its value is

calculated as follows:

$1,000

$50

9

On January 1, 2007, the Microsoft bond had a remaining life of 19 years. Thus, its value is

calculated as follows:

42.888$ = )330513$1,000(0. + )158116.11$50(

)

6(1.0

$1,000

+

)

6(1.0

$50

=

V19t

19

1=t

icrosoftM =

With a calculator, simply change N to 19; compute PV = –888.42

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–14

c. The capital gains yields for the bonds are:

%2.11112.0 =

$1,000

$1,000 – 42.888$

=

gains Capital

icrosoftM

−=−

d. The current yield for both bonds was $50/$1,000 = 0.05 = 5.0%

g. On January 1, 2020, the IBM bond will have a remaining life of four years. Thus, its value will

be:

35.965$ = )792094$1,000(0. + )46511.3$50(

)

6(1.0

$1,000

+

)

6(1.0

$50

=

V4t

4

1=t

IBM =

10-38 a. (1)

$9.50 =

0.20

$1.90

=

0.05 + 0.15

0.05) – $2(1

=

P

ˆ0

(4)

$44.00 =

0.05

$2.20

=

0.10 – 0.15

0.10) $2(1

=

P

ˆ0

+

Chapter 10 Principles of Finance 6e

Besley/Brigham

10–16

Step 2

65

5

ss

nn

ˆˆ(1 + g)

DD

ˆ

P =

r – r –

gg

$3.5199(1.05) $3.6959

= = $52.7981

0.12 – 0.05 0.07

=

=

This is the price of the stock five years from now. The PV of this price, discounted back five

years, is as follows:

55

$52.7981

ˆ

PV of P $52.80(0.56743) $29.9591

(1.12)

= = =

Step 3

The price of the stock today is as follows:

This problem could also be solved by substituting the proper values into the following equation:

c. Year 1

1

D

ˆ

/P0 = $2.01/$39.43 = 5.10%

Year 5

6

D

ˆ

/P5 = $3.70/$52.80 = 7.00%

The main points to note here are as follows:

(1) The total yield is always 12 percent (except for rounding differences).

Principles of Finance 6e Chapter 10

Besley/Brigham

10–17

d. Because Swink’s supernormal and normal growth rates are lower, the dividends and, hence,

e. As the required return increases, the price of the stock goes down, but both the capital gains

10–41 a. Part 1.

1

D

ˆ

= D0(1 + gs) = $1.60(1.20) = $1.92

2

D

ˆ

= D0(1 + gs)2 = $1.60(1.20)2 = $2.304

Part 2.

Expected dividend yield:

1

D

ˆ

/P0 = $1.92/$54.11 = 3.55%

ˆ

Second, find the capital gains yield:

10–18

6.45% = 0.0645 =

$54.11

$54.11 – $57.60

=

P

P

–

P

ˆ

0

0

1

Dividend yield = 3.55%

Capital gains yield = 6.45

10.00% = rs.

b. Due to the longer period of supernormal growth, the value of the stock will be higher for each

year. Although the total return will remain the same, rs = 10%, the distribution between dividend

c. Throughout the supernormal growth period, the total yield will be 10 percent, but the dividend

d. Some investors need cash dividends (retired people) whereas others would prefer growth.

10–42 Integrative Problem

a. Some of the key features of a bond include the following:

(2) Coupon rate. The dollar coupon is the “rent” on the money borrowed, which is generally the

par value of the bond. The coupon rate is the annual interest payment divided by the par

(4) Call provision. Most bonds (except U.S. Treasury bonds) can be called and paid off ahead

of schedule after some specified “call protection period.” Generally, the call price is above