Part Six:

Unincorporated Business Associations

CONTENTS

Chapter 30 Formation and Internal Relations of General Partnerships

Chapter 31 Operation and Dissolution of General Partnerships

Chapter 32 Limited Partnerships and Limited Liability Companies

ETHICS QUESTIONS RAISED IN THIS PART

1. From an ethical perspective what obligations does one partner have toward her fellow partners? Are the

ethical obligations of a partner to her fellow partners the same as her legal obligations? What moral

obligations does a partner have to her fellow partners in dealing with third parties?

2. A partnership is defined as “an association of two or more persons to carry on as co-owners a business for

ACTIVITIES AND RESEARCH PROBLEMS

1. Have students get together with one or more other students and draft the necessary papers to create (a) a

general partnership (b) a limited partnership and (c) a limited liability company to carry on a business of

some type.

2. Have students find the relative number of new business entities that are formed as partnerships, limited

partnerships, limited liability companies, limited liability partnerships, limited liability limited partnerships,

and corporations.

Chapter 30

FORMATION & INTERNAL RELATIONS OF GENERAL

PARTNERSHIPS

NOTE: the following outline reflects the contents of the student’s textbook. This instructor’s manual is

in a slightly different order because it presents a side-by-side comparison of UPA and RUPA where

appropriate.

I. Choosing a Business Association

A. Factors Affecting the Choice

1. Ease of Formation

2. Taxation

3. External Liability

4. Management and Control

5. Transferability

6. Continuity

B. Forms of Business Associations

1. Sole Proprietorship

2. General Partnership

3. Joint Venture

4. Limited Partnership

5. Limited Liability Company

6. Limited Liability Partnership

7. Limited Liability Limited Partnership

8. Corporation

9. Business Trusts

II. Formation of General Partnerships

A. Nature of Partnership

1. Definition

2. Entity Theory

a. Partnership as a Legal Entity

b. Partnership as a Legal Aggregate

B. Formation of a Partnership

1. Partnership Agreement

a. Statute of Frauds

b. Firm Name

2. Tests of Partnership Existence

a. Association

b. Business for Profit

c. Co-ownership

3. Partnership Capital and Property

III. Relationships Among Partners

A. Duties Among Partners

1. Fiduciary Duty

2. Duty of Obedience

3. Duty of Care

B. Rights Among Partners

1. Rights in Specific Partnership Property

2. Partner’s Transferable Interest in the

Partnership

a. Assignability

b. Creditors’ Rights

3. Right to Share in Distributions

a. Right to Share in Profits

b. Right to Return of Capital

c. Right to Indemnification

d. Right to Compensation

4. Right to Participate in Management

5. Right to Choose Associates

6. Enforcement Rights

a. Right to Information &

Inspection of the Books

b. Legal Action

Cases in This Chapter

In Re KeyTronics

Thomas v. Lloyd

Enea v. The Superior Court of Monterey County

Chapter Outcomes

After reading and studying this chapter, the student should be able to:

Identify the various types of business associations and explain the factors

relevant to deciding which form to use.

Distinguish between a legal entity and a legal aggregate and identify

a partner’s interest in the partnership.

Identify and explain the duties owed by a partner to her copartners.

Identify and describe the rights of partners.

TEACHING NOTES

Various factors such as ease of formation, type of control, and taxation are

considered when the owners of a business enterprise decide what type of entity

they wish to become. Choices include sole proprietorship, an unincorporated

I. CHOOSING A BUSINESS ASSOCIATION

*** Chapter Objective***

Identify various types of business associations & explain the factors relevant to deciding

which to use.

A. FACTORS AFFECTING THE CHOICE

Ease of Formation

Some business associations are created with no formalities, some require filing

of documents with the state.

Taxation

Some business associations are considered separate taxable entities; others are

not. Income from a business which is not a taxable entity is “credited” to the

owners and taxed on their personal returns. Separate taxable entitles, such as

corporations, are directly taxed. Funds distributed to the owners are then also

taxed on the owners’ personal returns. All businesses that have publicly traded

ownership interests must be taxed as a corporation.

External Liability

The most common types of external liability are tort and contract liability. In

some business, owners have unlimited liability, meaning their entire estate may

be liable for some or all of the business’ debts. In other businesses, the owner’s

Management and Control

Owners may share fully in the control of the business or their right to control

may be restricted.

Transferability

In some businesses, owners may transfer their financial interest, but not their

managerial interest; in other businesses, ownership is freely transferable.

Continuity

Low continuity in a business means that the death or withdrawal of an owner will

dissolve the business. High continuity ensures that the business will continue

through an ownership change.

Note: See Figure 30-1: General Partnership, Limited Partnership, Limited Liability Company and

Corporation

B. FORMS OF BUSINESS ASSOCIATIONS

Sole Proprietorship

An unincorporated business owned by just one person; formed with no formality

and no documents to be filed. If one person conducts a business and does not

file with the state to form an LLC or corporation, a sole proprietorship will result

by default. It is not a separate taxable entity. Owners have unlimited liability for

all debts. Ownership is freely transferable, but the business dissolves upon the

owner’s death.

General Partnership

An unincorporated business formed for profit, owned by two or more persons;

formed with no formality and no documents to be filed. If two or more people

conduct a business and do not file with the state to form another type of

Joint Venture

An unincorporated business established by two or more persons, usually for a

short time period and for a specific purpose. In most cases, joint ventures are

governed by the law of partnerships.

Limited Partnership

An unincorporated business formed for profit, owned by at least one general

partner and at least one limited partner; requires filing of certificate of limited

partnership with the state. A limited partnership may elect not to be a separate

taxable entity, in which case only the partners are taxed. Publicly traded limited

partnerships, however, are subject to corporate income taxation. General

partners have unlimited liability for all debts; limited partners have limited

Limited Liability Company

A limited liability company (LLC) is an unincorporated business association that

provides limited liability to all of its owners and permits all of its members to

participate in management. It may elect not to be a separate taxable entity. As

noted previously, publicly traded LLCs are subject to corporate income taxation.

If an LLC has only one member, then it will be taxed as a sole proprietorship,

unless separate entity tax treatment is elected. The LLC provides many of the

Limited Liability Partnership

A general partnership that, by making the statutorily required filing, limits the

liability of its partners for some or all of the partnership’s obligations. To become

an LLP, a general partnership must file with the state an application containing

specified information. All of the States have enacted LLP statutes.

Limited Liability Limited Partnership

An unincorporated business similar to a limited partnership, except that the

general partners have limited liability as in an LLP. An existing limited

partnership may be able to register as an LLLP without having to form a new

organization, as would be required to form an LLC.

Corporation

A legal entity distinct and separate from its owners. Formed by filing its articles

of incorporation with the state. A corporation is taxed on its earnings and the

shareholders are taxed on distributions they receive from the corporation. (Some

Business Trusts

Created by voluntary agreement between parties, with no state consent

required. Has three distinguishing characteristics: 1) is devoted to the conduct

II. FORMATION OF A GENERAL PARTNERSHIP

Partnerships as a form of business can be traced as far back in time as ancient

Babylonia, classical Greece and the Roman Empire. Partnerships are important

because they allow people with di>erent expertise, backgrounds, resources, and

interests to combine their skills to form a more competitive enterprise. It should

be recalled that except for the filing requirements and the partners’ liability

shield, the law governing LLPs is identical to the law governing general

partnerships.

A. NATURE OF PARTNERSHIP

The National Conference of Commissioners on Uniform State Laws promulgated

the Uniform Partnership Act (UPA) in 1914. In August 1986, the UPA Revision

Subcommittee of the Committee on Partnerships and Unincorporated Business

Organizations of the American Bar Association’s Section of Corporation, Banking

and Business Law and the National Conference of Commissioners on Uniform

State Laws decided to undertake a complete revision of the UPA. The revision

was approved in August 1992 and was amended in 1993, 1994, 1996, and 1997.

More than 60% of the States have adopted the Revised Act (RUPA).

This Instructor’s Manual will discuss both UPA and RUPA, with a

side-by-side comparison when appropriate. Note that the chapter in the

text discusses the RUPA but, where the RUPA has made signi.cant

changes, the UPA is also discussed. The chapter summary in the text

re/ects only the RUPA.

Definition

RUPA and UPA both define a partnership as “an association of two or more

persons to carry on as co-owners a business for profit.” Section 101(6). The

RUPA broadly defines “person” to include individuals, partnerships, corporations,

joint ventures, business trusts, estates, trusts, and any other legal or commercial

entity.” Section 101(10). The comments indicate that this definition would

include a limited liability company. Also defined by Section 101, a business

includes every trade, occupation, and profession. [UPA Sections 2, 6]

*** Chapter Objective***

Distinguish between a legal entity and a legal aggregate. Identify those purposes for which

a partnership is treated as a legal entity and those purposes for which it is treated as a legal

aggregate.

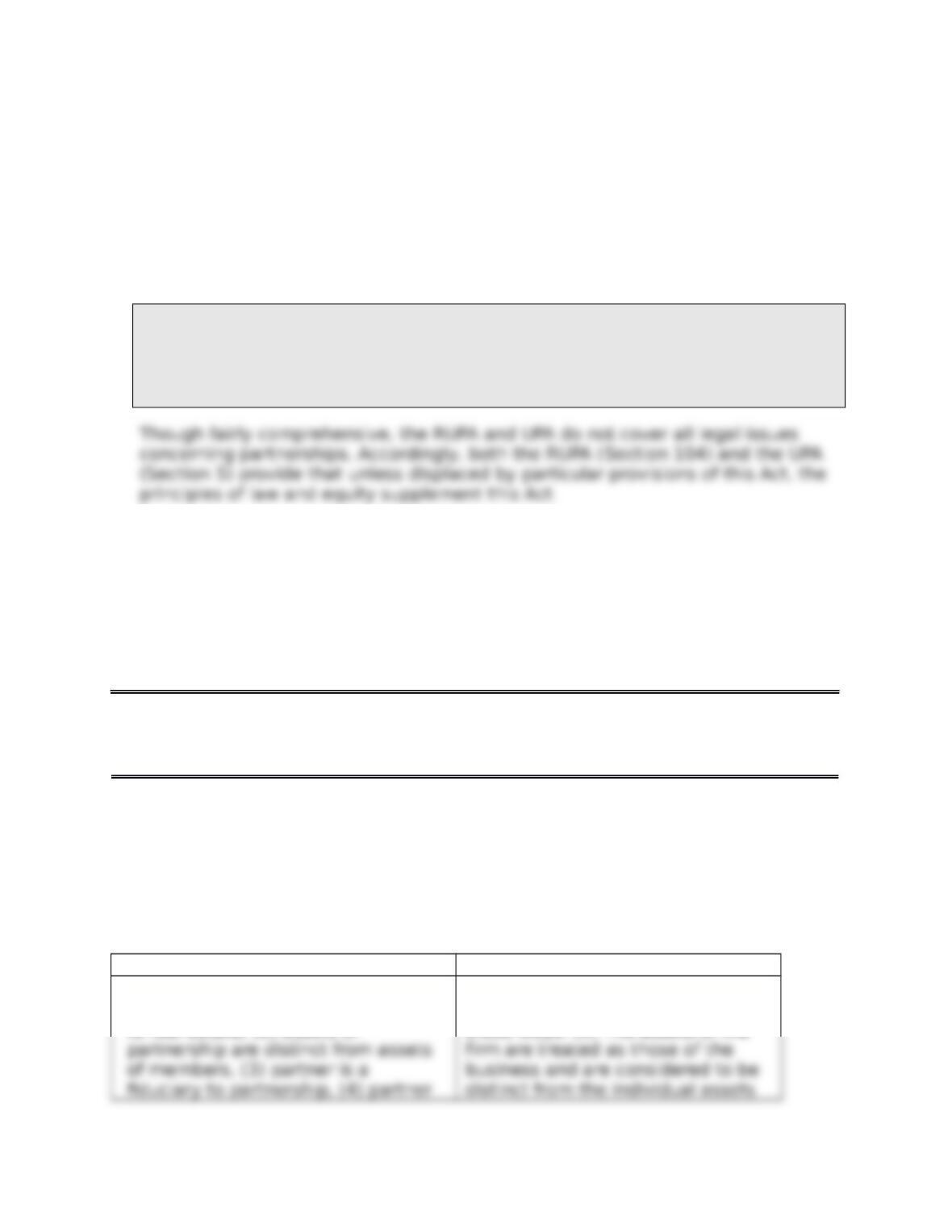

Entity Theory

Partnership as a Legal Entity — A legal entity is a unit capable of

possessing legal rights and of being subject to legal duties. A legal entity may

acquire, own, and dispose of property. It may enter into contracts, commit

wrongs, sue, and be sued. A partnership is an entity distinct from its partners,

but what this means exactly depends on whether UPA or RUPA is ruling.

UPA RUPA

Under UPA, a partnership is a legal

entity with regard to (1) holding title

to real estate, (2) assets of

Under the Revised Act a

partnership is a legal entity in

these ways: (1) The assets of the

is an agent of partnership, and (5)

marshaling of assets.

of the members. (2) A partner is

accountable as a fiduciary to the

partnership. (3) Every partner is

considered an agent of the

partnership. (4) A partnership may

sue and be sued in the name of the

partnership.

Partnership as a Legal Aggregate — The common law regarded a

partnership as a legal aggregate, a group having no legal existence apart from

that of its individual members. The Internal Revenue Code treats a partnership

as an aggregate. The partnership does not pay federal income tax; but the

partners are taxed on the income each derives from the partnership.

UPA RUPA

The UPA partially rejected the

common law view and treats

partnerships as legal aggregates for

some purposes but as legal entities

for others. The UPA continues

The Revised Act has greatly

increased the extent to which

partnerships are treated as entities.

It applies aggregate treatment to

very few aspects of partnerships,

B. FORMATION OF A PARTNERSHIP

Forming a partnership is simple. A partnership may result from an oral or written

agreement between the parties or simply from the conduct of the parties.

Persons become partners by agreeing to associate themselves in a business as

co-owners. If two or more individuals share the control and profits of a business,

the law may deem them partners regardless of how they themselves

characterize their relationship.

Partnership Agreement

A “partnership agreement” is “the agreement, whether written, oral, or implied,

among the partners concerning the partnership, including amendments to the

partnership agreement.” This definition does not include other agreements

between some or all of the partners, such as a lease or a loan agreement.

Partners should put their agreement to associate as partners in writing, although

they are not usually required to do so by law.

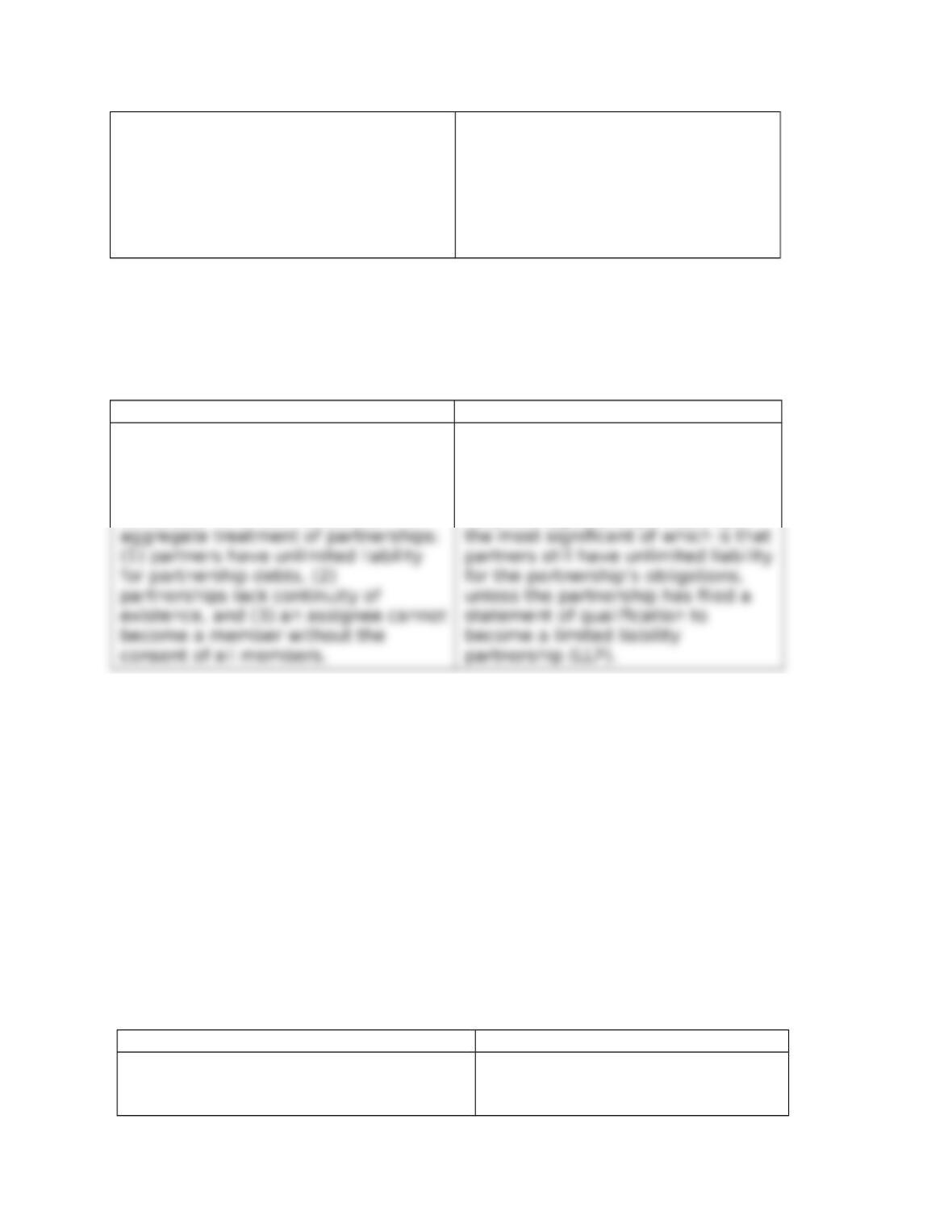

UPA RUPA

Any partnership agreement

(sometimes called articles of

partnership) should include:

Any partnership agreement

should include

1. the firm name and identity of

the partners,

2. the nature and scope of the

partnership business,

3. the duration of the partnership,

4. the capital contributions of each

desired,

8. the restrictions, if any, on the

authority of particular partners to

bind the firm,

9. the right, if desired, of a partner

to withdraw from the firm, and the

terms, conditions, and notice such

withdrawal would require, and

10. a provision for continuation of

1. The firm name and the

identity of the partners;

2. The nature and scope of

the partnership business;

3. The duration of the

partnership;

7. A provision for salaries, if

desired;

8. Restrictions, if any, upon

the authority of particular

partners to bind the firm;

9. Any desired variations from

the partnership statute’s

default provisions governing

dissolution; and

Statute of Frauds – Partnership agreements required to be in writing are: a

contract to form a partnership to exist longer than one year; a contract for the

transfer of an interest in real estate to or by a partnership.

Firm Name – A partnership should have a firm name, which may not be

identical with or deceptively similar to the name of any other existing business

concern; it may be the name of the partners or of any one of them, or a fictitious

or assumed name. In most states, statutes require anyone conducting business

under an assumed or fictitious name to file in a designated public oLce a

certificate with the business name and the real names and addresses of all

persons conducting the business. The name must not be likely to indicate to the

public that it is a corporation.

Tests of Partnership Existence

not the parties intend to form a partnership

Business for Pro.t — The partners must co-own a business for profit. Not a

partnership because not for profit are: social clubs, charitable organizations,

fraternal orders and civic societies.

Also not a partnership: an association of people for financial gain on a temporary

basis or for relatively few isolated transactions, although they may have formed

a joint venture.

Co-ownership — The co-ownership of a business is essential for the existence

of a partnership; the co-ownership of property used in a business is not

necessary. The two most important factors in business ownership are (a) sharing

of profits and (b) right to manage and control the business.