Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CASE 29-3

Seigel v. Merrill Lynch, Pierce, Fenner & Smith, Inc.

Steadman J.

* * *

The events giving rise to this lawsuit

arose in January and February of 1997 *

* * . During that time period,

plainti /appellant Seigel, a Maryland

resident, traveled to Atlantic City, New

Jersey to gamble. While there, he wrote

a number of checks to various casinos,

and, in exchange, received gambling

all the checks.

Seigel eventually gambled away all of

the chips he had received for the

checks. Upon returning to Maryland,

Seigel discussed the status of the

outstanding checks with Merrill Lynch,

informing his broker of the gambling

nature of the transactions, and his

desire to avoid realizing the apparent

losses. Merrill Lynch informed Seigel that

it was possible to escape paying the

checks by placing a stop payment order

and liquidating his cash management

account. Seigel took this advice and

instructed Merrill Lynch to close his

account, liquidate the assets, and not to

honor any checks drawn on the account.

Merrill Lynch agreed, and con1rmed

Seigel’s instructions.

plus interest * * * . Seigel 1led a motion

for summary judgment * * * . He argued

that D.C. Code §16–1701 precluded

enforcement of the checks as a void

gambling debt, or in the alternative that

New Jersey law prohibited the

enforcement of the checks, and that

therefore Merrill Lynch had no rights by

way of subrogation as a defense to its

payment over the stop payment order.

had not su ered any actual loss as a

result of the payment of the checks. On

June 24, 1998, the trial court issued an

order granting defendant’s motion, and

dismissing the complaint. This appeal

followed.

* * *

We begin with an examination of the

statutory scheme relating to stop

payment orders, because we believe

these provisions are determinative of

this appeal. The relevant sections are

found in the Uniform Commercial Code *

* * §§4403 and 4407.

The basic right of the depositor to stop

payment on any item drawn on the

depositor’s account is set forth in

Section 4403(a). However, liability on

the bank for payment over a stop

payment order is far from automatic. On

the drawer or maker (that is, the

depositor), the bank is subrogated both

to the rights of “any holder in due

course on the item” and to the rights of

“the payee or any other holder of the

item against the drawer or maker either

on the item or under the transaction out

of which the item arose.” As a leading

rights of the casino payees against

Seigel. As the payee of a dishonored

check, the casino would have a prima

facie right to recover its amount from

Seigel as drawer, 3414(b), and the

burden would be on Seigel to establish

any defense he might assert on the

instrument. 3308(b); [citation]. Seigel

asserts two such defenses: duress and

illegality. We turn to an examination of

those defenses.

* * *

The entirety of appellant’s duress

argument emanates from a single

sentence in his a-davit: “For years I

have had [a] gambling problem.” If not

ambiguous, the statement is conclusory.

Unlike the gambler in [citation],

appellant fails to produce any evidence

in the record, specific or otherwise,

regarding his problem and its relation to

any unconscionable duress in the

We therefore conclude that Seigel’s

assertion that the checks would be

unenforceable in New Jersey fails. Seigel

also invokes the fact that these checks

were given in order to obtain chips with

which to gamble, and cites us in

particular to D.C. Code * * * [which]

provides that:

In substance, Seigel claims that this

statute would serve as a defense if the

casinos were to seek to enforce the

checks in the first instance in a District

of Columbia court, and therefore this

same statute requires that he be

entitled to a-rmatively recover from

Merrill Lynch the amount of the checks

in a District of Columbia court,

regardless of the checks’ enforceability

elsewhere.

We may assume for present purposes

that this statute would prevent direct

enforcement of the checks in the District

of Columbia, a somewhat dubious

proposition in itself given the validity of

the checks where made. But that is not

this case. Rather, the question is

whether under the relevant provisions of

the Uniform Commercial Code, Seigel

has met his burden of proof to establish

actual loss. We think he has not.

have provided an appropriate forum for

enforcing the checks. The highest

Maryland court has squarely held that

because there is no longer a strong

enforce the checks directly against

Seigel in the state of his residence—

Maryland.

* * *

Case Questions

1. What does it mean for the bank to have rights of subrogation?

2. How could another check and balance be placed into this system?

Ethical Question: Who should bear the risk of loss in this case? Explain.

Critical Thinking Question: What rule should be established for liability of

a bank making a payment over a stop payment order?

Disclosure Requirements

The Truth in Savings Act, passed in 1992, requires all depositary institutions

to disclose details of customers’ accounts, including fees, interest rates, and

regulations.

Customer's Death or Incompetence

Death or incompetence revokes all agency agreements. Adjudication of

incompentency by a court is regarded as notice to the world of that fact.

Actual notice is not required.

Customer's Duties

A bank customer must exercise reasonable promptness in examining

account statements and canceled checks to detect unauthorized signatures

or alterations. Failure to notify the bank of any false signatures within the

*** Chapter Outcome ***

De1ne a consumer electronic funds transfer, identify the various types of electronic

funds transfers

and outline the major provisions of the Electronic Funds Transfer Act.

CASE 29-4

Mansi v. Gaines

Waller, J.

This appeal involves an issue of first

impression in Mississippi—the

interpretation of [UCC] 4–406 (Rev.

2002), which imposes duties on banks

and their customers insofar as forgeries

are concerned. The case arises from a

series of forgeries made by one person

Washington County, Mississippi. * * * The

Rogers were both in their eighties when

the events which gave rise to this lawsuit

took place. After Neal became bedridden,

Helen hired Jackie Reese to help her take

care of Neal and to do chores and

errands.

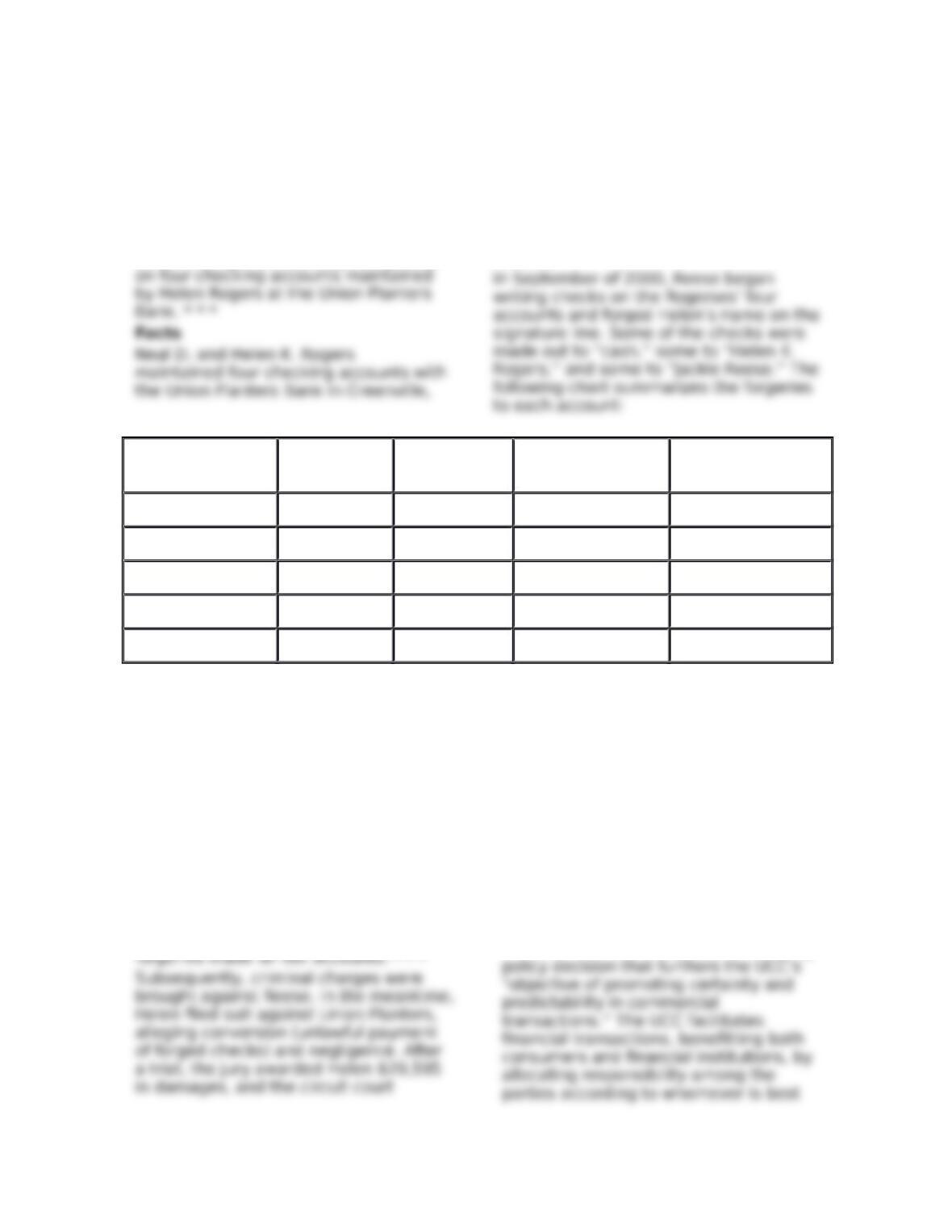

ACCOUNT

NUMBER

BEGINNING ENDING NUMBER OF

CHECKS

AMOUNT OF

CHECKS

54282309 11/27/2000 6/18/2001 46 $16,635.00

0039289441 9/27/2000 1/25/2001 10 $2,701.00

6100110922 11/29/2000 8/13/2001 29 $9,297.00

6404000343 11/20/2000 8/16/2001 83 $29,765.00

TOTAL 168 $58,398.00

Neal died in late May of 2001. Shortly

thereafter, the Rogerses’ son, Neal, Jr.,

began helping Helen with financial

matters. Together they discovered that

many bank statements were missing

and that there was not as much money

in the accounts as they had thought. In

June of 2001, they contacted Union

Planters and asked for copies of the

missing bank statements. In September

of 2001, Helen was advised by Union

Planters to contact the police due to

entered judgment accordingly. From this

judgment, Union Planters appeals.

Discussion

* * *

The relationship between Rogers and

Union Planters is governed by Article 4

of the Uniform Commercial Code,

[citation]. [UCC] Section 4–406(a) & (c)

provide that a bank customer has a duty

to discover and report “unauthorized

signatures”; i.e., forgeries. Section

4–406 of the UCC reSects an underlying

able to prevent a loss. Because the

customer is more familiar with his own

signature, and should know whether or

not he authorized a particular

withdrawal or check, he can prevent

further unauthorized activity better than

a financial institution which may process

thousands of transactions in a single

day. Section 4–406 acknowledges that

the customer is best situated to detect

A. Union Planters’ Duty to Provide

Information under §4–406(a).

The court admitted into evidence copies

of all Union Planters statements sent to

Rogers during the relevant time period.

Enclosed with the bank statements were

either the cancelled checks themselves

or copies of the checks relating to the

period of time of each statement. The

evidence shows that all bank statements

and cancelled checks were sent, via

United States Mail, postage prepaid, to

all customers at their “designated

to a customer when it “sends . . . to a

customer a statement of account

showing payment of items.” §4–406(a)

(emphasis added). [Citation.] The word

“receive” is absent. The customer’s duty

to inspect and report does not arise

when the statement is received, as

Rogers claims; the customer’s duty to

inspect and report arises when the bank

sends the statement to the customer’s

noti1ed a bank of an irregularity may be

precluded from bringing certain claims

against the bank:

(d) If the bank proves that the customer

failed, with respect to an item, to comply

with the duties imposed on the customer

by subsection (c), the customer is

precluded from asserting against the

bank:

(1) The customer’s unauthorized

signature . . . on the item, if the bank

also proves that it su ered a loss by

reason of the failure; . . .

[UCC] §4–406(d)(1).

A bank may shorten the customer’s

thirty-day period for notifying the bank

of a series of forgeries, and here, Union

Planters shortened the thirty-day period

to 1fteen days. The statute states that a

customer must report a series of

forgeries within “a reasonable period of

time, not exceeding thirty (30) days. . . .

” “The 30-day period is an outside limit

only. However 30 days is presumed to

be reasonable and the bank bears the

burden of proving otherwise.” [Citation.]

Although there is no mention of a

specific date, Rogers testi1ed that she

Reese had been forging checks until

September of 2001. Courts in Louisiana

and Texas have held that, under similar

circumstances, a customer’s claims

against a bank for paying forged checks

are without merit. [Citations.]

Rogers is therefore precluded from

making claims against Union Planters

because (1) under §4–406(a), Union

Planters provided the statements to

Rogers, and (2) under §4– 406(d)(2),

Rogers failed to notify Union Planters of

the forgeries within 15 and/or 30 days of

the date she should have reasonably

Case Questions

1. Should a bank be held responsible for checking every signature on every

check? How signiticant should a variation in signature be before it is

questioned?

2. Should a customer be held responsible for examining her bank statements

to determine if there has been any fraud? How much time should she be

allowed?

Ethical Question: Did either part act unethically? Explain.

Critical Thinking Question: Do you agree with the court's decision?

Explain.

II. ELECTRONIC FUNDS TRANSFERS

The use of commercial paper for payment has already made the United

States a virtually cashless society; technological advances of computers may

bring about a virtually checkless society through electronic funds transfer

systems (EFTs).

An electronic funds transfer has been defined as “any transfer of funds,

other than a transaction originated by check, draft, or similar paper

instrument, which is initiated through an electronic terminal, telephonic

A. NATURE & TYPES OF ELECTRONIC FUNDS TRANSFERS

Automated Teller Machines (ATM)

Permit customers to conduct various banking transactions through the use of

electronic terminals. After activating an ATM with a plastic identification card

and a personal identification number (PIN) a customer can deposit and

withdraw funds from her account, transfer funds between accounts, obtain

cash advances from bank credit card accounts, and make payments on

loans.

Point-of-Sale Systems (POS)

Direct Deposits and Withdrawals

Customer-preauthorized direct deposits (such as direct payroll deposits,

deposits of Social Security payments, and deposits of pension payments)

may be made to the customer’s account through an electronic terminal.

Automatic withdrawals are preauthorized electronic funds transfers from the

customer’s account for regular payments to some other party (such as

insurance companies, utility companies or automobile finance companies).

Pay-By-Phone Systems

Online Banking

Online banking enables the customer to execute many banking transactions

via an Internet-connected computer. For instance, customers may view

account balances, request transfers between accounts, and pay bills

electronically.

*** Chapter Outcome ***

Explain wholesale funds transfers and discuss how they operate.

Wholesale Electronic Funds Transfers

Over one trillion dollars of wholesale electronic funds transfer occur each

business day between financial institutions, between financial institutions

and businesses, and between businesses, under the auspices of the Federal

Reserve wire transfer network system (Fedwire) and the New York Clearing

House Interbank Payment System (CHIPS), and a number of private

wholesale wire systems which exist among large banks.

B. CONSUMER FUNDS TRANSFERS

The Electronic Funds Transfer Act was passed in 1978 and administered by

the Board of Governors of the Federal Reserve System, the act requires

Disclosure

The act is primarily a disclosure statute, which requires the terms and

conditions of electronic funds transfers involving a consumer's account be

disclosed in readily understandable language at the time a consumer

contracts for services. Required disclosures include liabilities, charges,

rights, and procedures.

Documentation and Periodic Statements

Consumers must be provided with written documentation of each transfer

made from an electronic terminal at the time of the transfer. The

transfer; the fee for the transaction; and an address and phone number for

questions and information.

Preauthorized Transfers

A preauthorized transfer from a consumer's account must be authorized in

advance by the consumer in writing. A copy must be provided to the

consumer when made.

Error Resolution

Consumer Liability

Consumer liability is limited to $50 if noti1cation of unauthorized transfers is

provided within two days after the consumer learns of the theft, and $500 if

notice is made subsequently. Customer liability is unlimited if notice is not

given within sixty days after receipt of a periodic statement, and the bank

can demonstrate that the loss would not have occurred absent the

customer's failure to report. If the financial institution fails to investigate in

good faith, it is liable to the consumer for treble damages.

Liability of Financial Institution

The financial institution is liable for damages proximately caused by a failure

to make an EFT within the terms of the customer's account contract. There

C. WHOLESALE FUNDS TRANSFERS

Article 4A, Funds Transfers is designed to provide a statutory framework for

an electric payment system that is not covered by existing U.C.C. provisions

or the Electronic Fund Transfer Act; provides that the rights and obligations

of the parties to a funds transfer covered by the article are subject to the

contrary agreement of the parties or the funds transfer system rules

governing banks.

Scope of Article

Article 4A covers the transfers of credit that move from an originator to a

bene1ciary through the banking system. However, if any step is governed by

the Electronic Fund Transfer Act, the entire transaction is excluded from

Article 4A coverage.

Payment order — A sender’s instruction to a receiving bank to pay, or to

cause another bank to pay, a 1xed or determinable amount of money to a

bene1ciary; may be oral, electronic, or in writing.

NOTE: See Fig. 29-2: Parties to a Funds Transfer for an example.

Excluded Transactions — Article 4A provides that if any part of a funds

transfer is governed by the Electronic Fund Transfer Act, the transfer is

excluded from Article 4A coverage.

NOTE: See Figure 29-2.

Acceptance

If the bene1ciary's bank accepts a payment order, the bank is obligated to

pay the bene1ciary the amount of the order.

Erroneous Execution of Payment Orders

If a receiving bank mistakenly executes a payment order for an amount

greater than that authorized by the sender, the bank is only entitled to the

correct ordered amount.

Unauthorized Payment Orders