CHAPTER 11

COMPENSATION

A. OVERVIEW

This chapter provides insight into key compensation topics. Equity issues are examined

from the individual, internal and external points of view. Basic coverage is provided of

legal requirements of compensation, including Title VII of the Civil Rights Act of 1964;

the Equal Pay Act of 1963; and the Fair Labor Standards Act of 1938. Executive

compensation closes the chapter with topics related to over compensation; controlling

compensation; tying individual compensation to organizational performance, etc.

B. LECTURE OUTLINE

I. OPENING CASE – JAMBA JUICE

Jamba Juice is a leading retail purveyor of blended-to-order fruit

smoothies, fresh-squeezed juices, and healthy soups and breads. They are a high

growth company in an intensively competitive industry, and have developed a

compensation plan that keeps them competitive with others in their industry, and

also with tech-based employers as well. Jamba’s J.U.I.C.E. Plan allows general

managers to receive a percentage of store cash flow; share profits where money

accrues in a retention account payable in three year cycles; and stock options.

II. INTRODUCTION

Compensation is a key strategic area for organizations, impacting ability

to attract applicants, as well as insure optimal performance levels from

employees. Compensation programs continue to assume an increasingly larger

share of organizational operating expenses, especially in service industries. Three

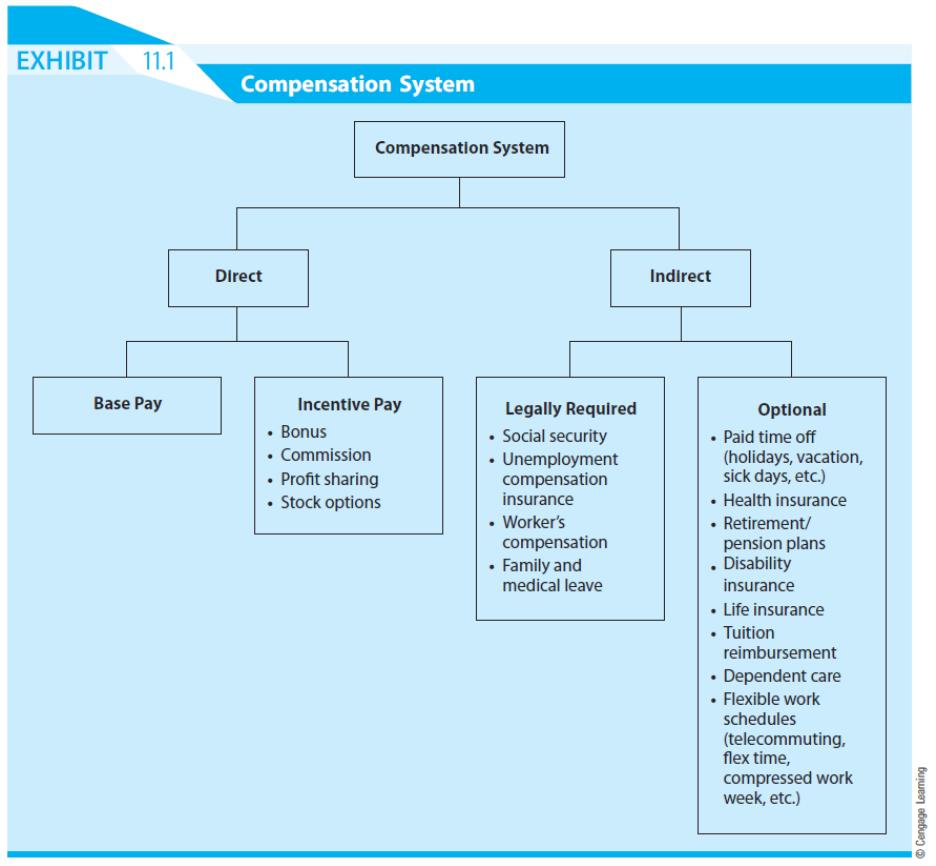

separate components to an organizational compensation system are illustrated in

EXHIBIT 11.1: COMPENSATION SYSTEM,, including direct cost of base and

incentive pays, as well as indirect costs.

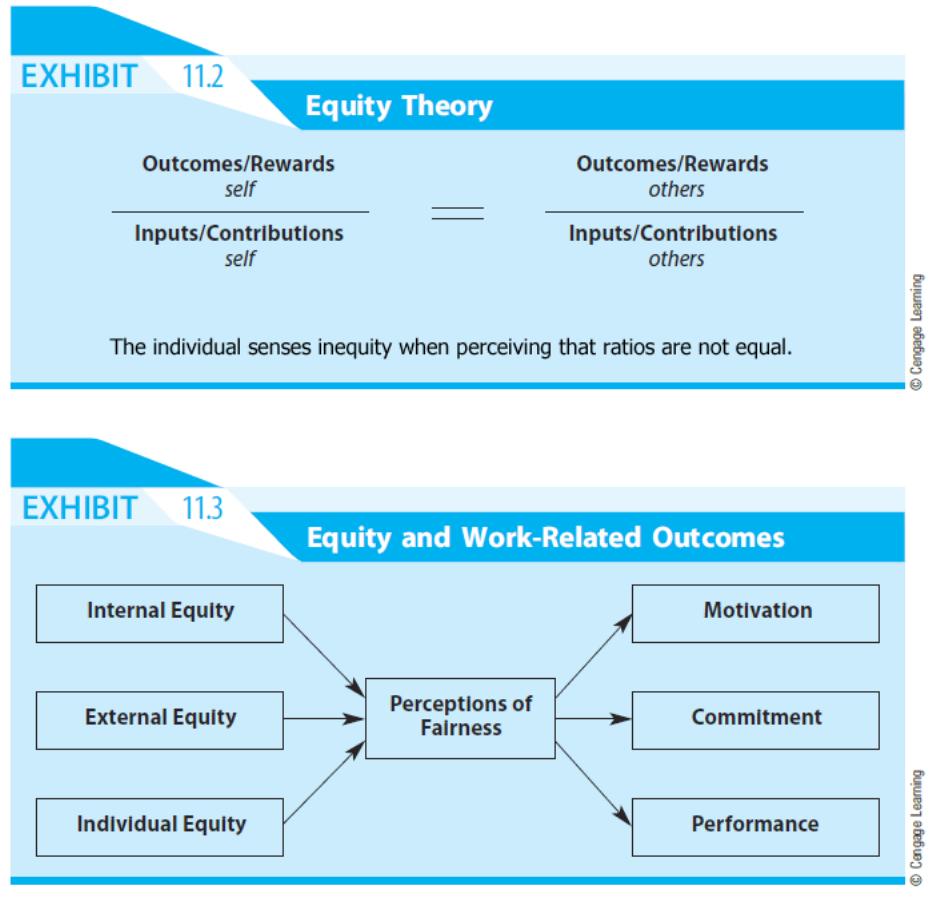

III. EQUITY

Perceived equity or fairness of the compensation system is critical. Equity

theory of motivation holds that workers assess their perceived inputs and

outcomes relative to those of others. When individuals perceive inequities, they

generally act to establish equity by increasing their outcomes or decreasing inputs.

Internal, external and individual equity impact motivation, commitment and on

the job performance.

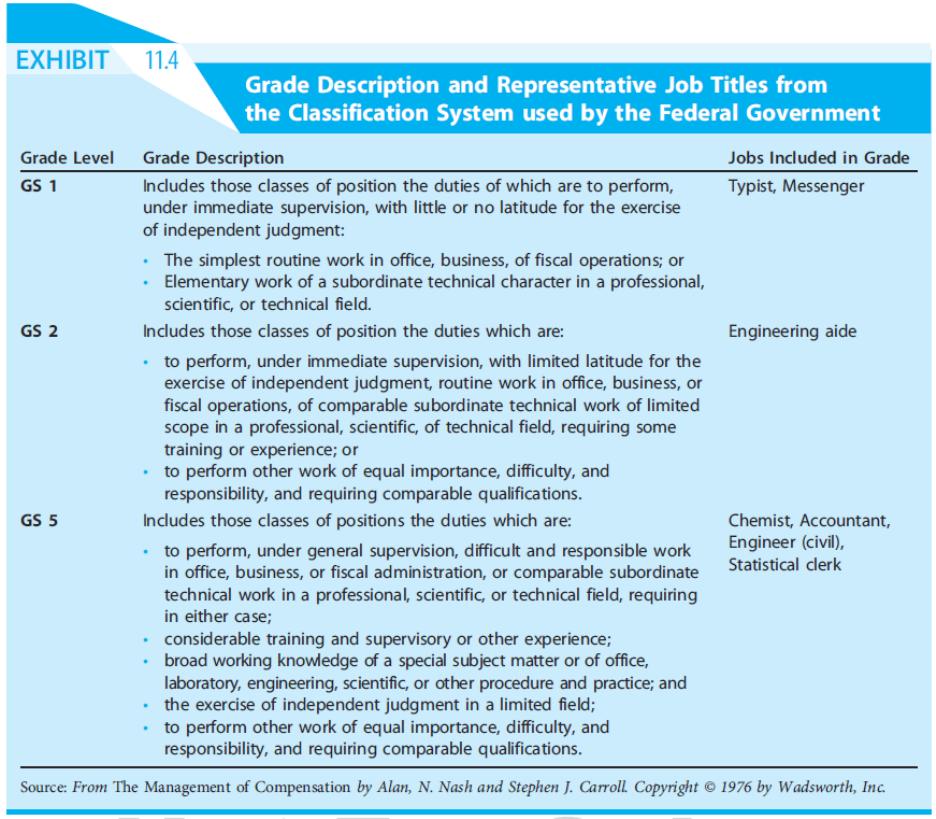

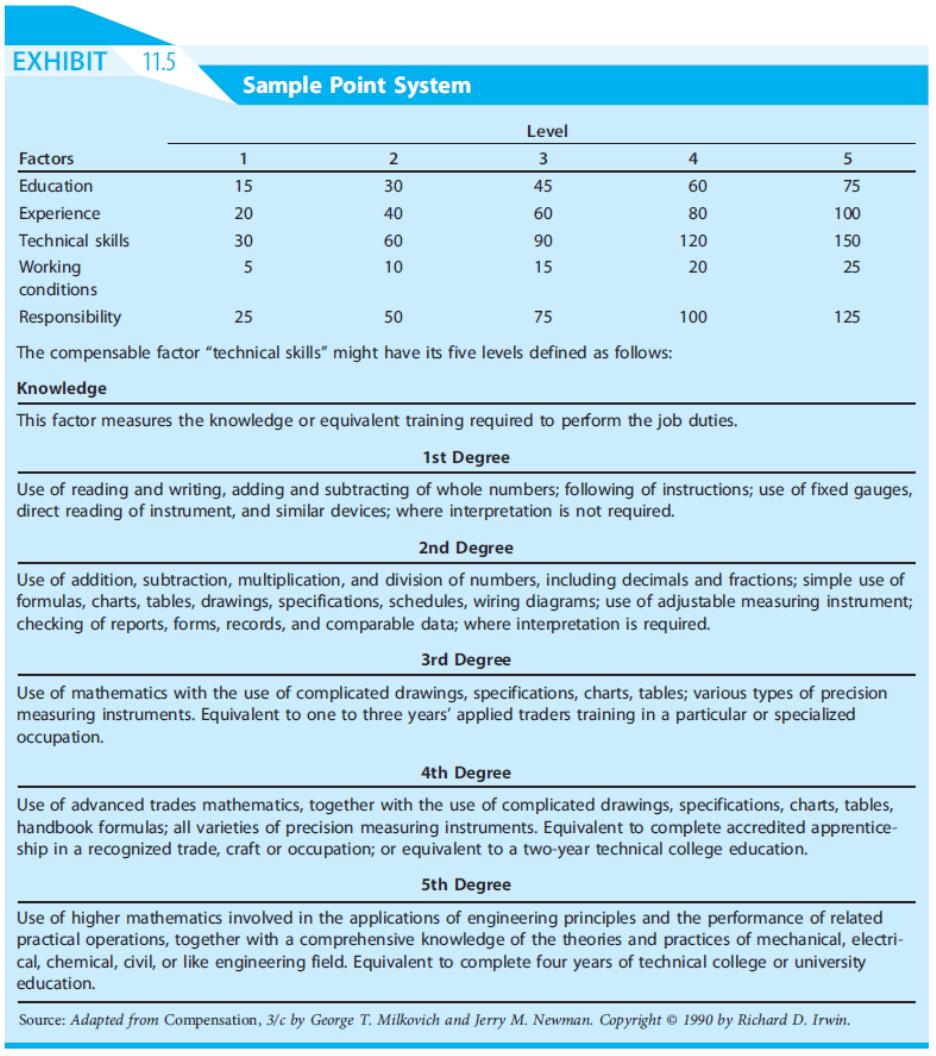

A. Internal equity – involves perceived fairness of pay differentials within an

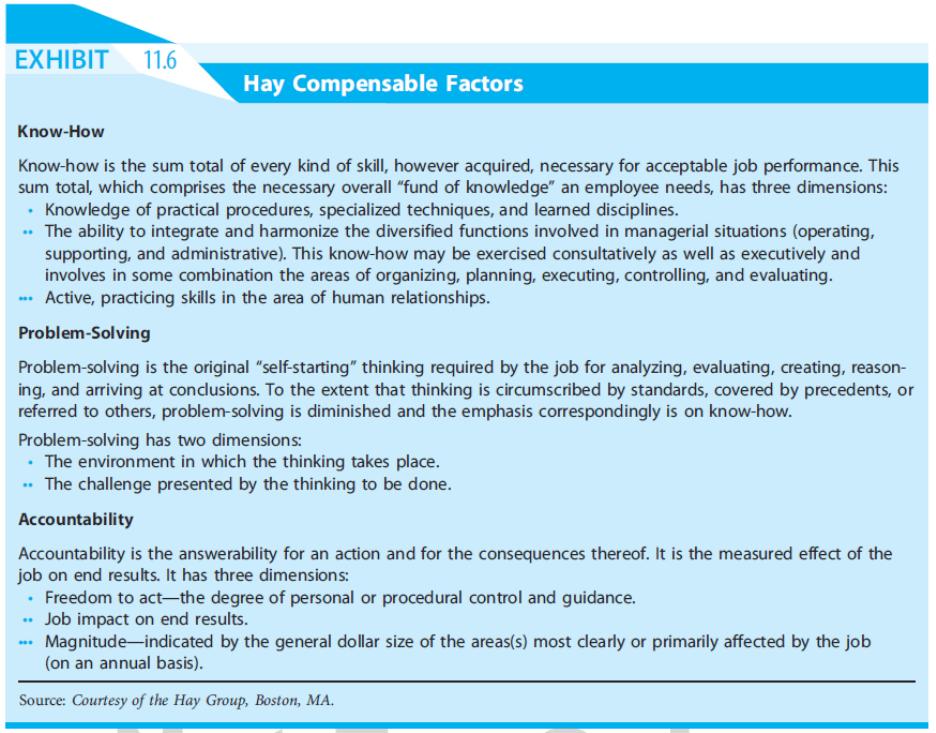

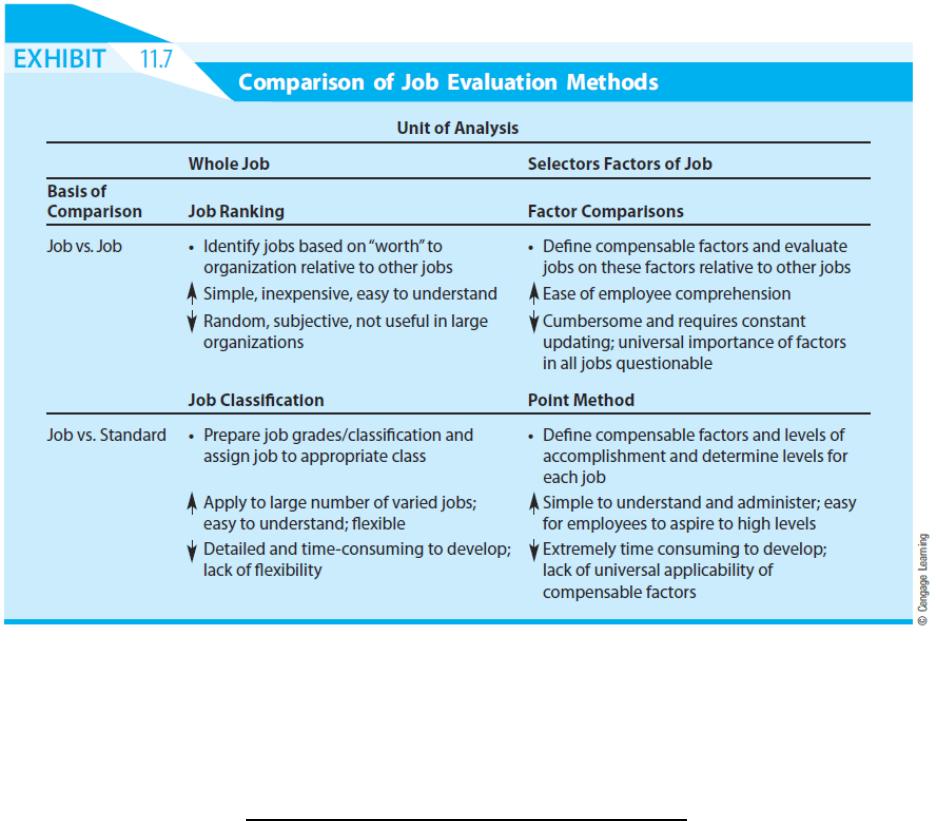

organization. Four techniques can be utilized to establish internal equity:

job ranking; job classification; point systems; and factor comparison.

Salary compression issues are becoming more prevalent in certain

industries based on supply and demand for entry-level skilled employees.

B. External equity – involves employee perceptions of compensation fairness

relative to those outside the organization. Organizations must be sure they

have a means of remaining competitive relative to cost structure and

market prices. Choices of lead, lag or market policy are available.

C. Individual equity – considers employee perceptions of pay differentials

among individuals who hold identical jobs in the same organization.

The effectiveness and appropriateness of merit pay, incentive pay,

skill-based pay, and team-based pay systems are also discussed as a means

of ensuring individual equity. See Joe Torre and the New York Yankees

example,; Team-based Incentive Pay at Children’s Hospital Boston

example,; Team-based Pay at Phelps Dodge example.

IV. LEGAL ISSUES IN COMPENSATION

A. Compensation is a condition of employment covered under both Title VII

of the Civil Rights Act of 1964 and the Equal Pay Act of 1963. Some note

that the Equal Pay Act is not very effective, as men and women often are

not employed in the same jobs, and the Act only requires equal pay for

equal work. To combat these limitations, the concept of comparable worth

has been advanced, although it is generally seen as falling outside of

existing federal law.

B. Fair Labor Standards Act (FLSA) of 1938 regulates federal minimum

wage, as well as policies on overtime and child labor. Certain workers are

exempt from minimum wage laws (generally managers, administrators,

outside sales people and professionals who exercise “independent

judgement” in carrying out job duties). Note: Federal minimum wage

laws and groups covered changed substantially in 2004.

V. EXECUTIVE COMPENSATION

Executive compensation is a controversial area. There is no real standard

or average due to the wide variety of factors faced by organizations and their

executives. Criticisms include the excessiveness of executive pay, and a lack of

relationship between pay and performance. Accounting practices relative to stock

options for executives is also an area of concern.

VI. CONCLUSION

Key compensation issues include: compensation relative to the market;

balance between fixed and variable compensation; utilization of individual versus

team-based pay; the appropriate mix of financial and nonfinancial compensation;

and developing an overall cost-effective program that results in high performance.

Compensation systems must be tied to behavior necessary for achievement of

strategic organizational goals.

READINGS

Reading 11.1 – Exposing Pay Secrecy

This article focuses on the issue of pay secrecy, describing its cost and benefits. Pay secrecy

essentially is a policy which restricts the amount of information employees are provided about

regarding what their co-workers are paid. Whether pay secrecy benefits or is detrimental to an

organization depends on a variety of factors. It is best understood as a continuum rather than an

all-or-nothing construct. Employers could have varying levels of pay secrecy. It also is related

to employee privacy issues, which have become much more prevalent in recent years.

Costs of pay secrecy include; 1) employee judgments about fairness and their perceptions of trust

may be sacrificed; 2) employee performance motivation can be expected to decrease; and 3)

from an economics perspective, the labor market may be less efficient because employees will

not move to their highest valued use.

Benefits of pay secrecy include organizational control, protection of privacy, and decreased labor

mobility.

Factors which influence the cost-benefit tradeoff of pay secrecy for an individual employer: 1)

nature of human capital (firm-specific versus general); 2) criteria for pay allocation (objective

versus subjective); 3) gauging of relative pay status (individual employee “guesses” where they

stand or rank in the organization’s relative pay distribution).

Reading 11.2 –The Development of a Pay-for-Performance Appraisal System for

Municipal Agencies : A Case Study

This reading presents a case study of a pay-for-performance system and outlines the process by

which it was developed. Despite its importance, both employees and management often view

the performance appraisal process as frustrating and unfair. These frustrations are largely

attributed to a reliance on performance appraisal instruments that 1) are not job related; 2) have

confusing or unclear rating levels, and; 3) are viewed as subjective and biased by staff

To address these issues, this case study: (1) identified a systematic procedure for creating

performance appraisal instruments; (2) described the appropriate training for those conducting an

appraisal interview; (3) implemented performance reviews using the developed instruments and

appraisal interview/review training, and; (4) evaluated employee attitudes toward the newly

developed system.

Steps Taken in Defining Job Performance and the Creation of an Appraisal Instrument

Step #1: Job analysis

Step #2: Rating of tasks

Step #3: Creation of appraisal instrument

Step #4: Identifying raters

Step #5: Rater training

Step #6: Performance appraisal interview

The process employed was collaborative throughout (between employee and supervisor). Once

the employee and supervisor had independently completed the appraisal instrument they met and

discussed the ratings. During this time the employee and supervisor reached an agreed upon

rating for each task statement. At this point, the appraisal was completed and signed by both the

employee and supervisor.

Once the employees completed the workshops and the trial run of the newly developed system,

they completed the performance appraisal reaction instrument again to assess their attitudes

toward the new system. Employee perceptions of procedural justice were also assessed.