144

Chapter 8

of Taxation

WHAT’S NEW IN THE SEVENTH EDITION:

A new

In the News

box on “The Tax Debate” has been added.

LEARNING OBJECTIVES:

how taxes reduce consumer and producer surplus.

the meaning and causes of the deadweight loss from a tax.

how tax revenue and deadweight loss vary with the size of a tax.

CONTEXT AND PURPOSE:

Chapter 9 will address the effects of trade restrictions on welfare.

The purpose of Chapter 8 is to apply the lessons learned about welfare economics in Chapter 7 to the

issue of taxation that was addressed in Chapter 6. Students will learn that the cost of a tax to buyers and

sellers in a market exceeds the revenue collected by the government. Students will also learn about the

government.

8

APPLICATION: THE COSTS OF

TAXATION

Chapter 8 /Application: The Costs of Taxation ❖ 145

KEY POINTS:

A tax on a good reduces the welfare of buyers and sellers of the good, and the reduction in

consumer and producer surplus usually exceeds the revenue raised by the government. The fall in

total surplus—the sum of consumer surplus, producer surplus, and tax revenue—is called the

deadweight loss of the tax.

As a tax grows larger, it distorts incentives more, and its deadweight loss grows larger. Because a tax

reduces the size of a market, however, tax revenue does not continually increase. It first rises with

the size of a tax, but if the tax gets large enough, tax revenue starts to fall.

CHAPTER OUTLINE:

I. The Deadweight Loss of Taxation

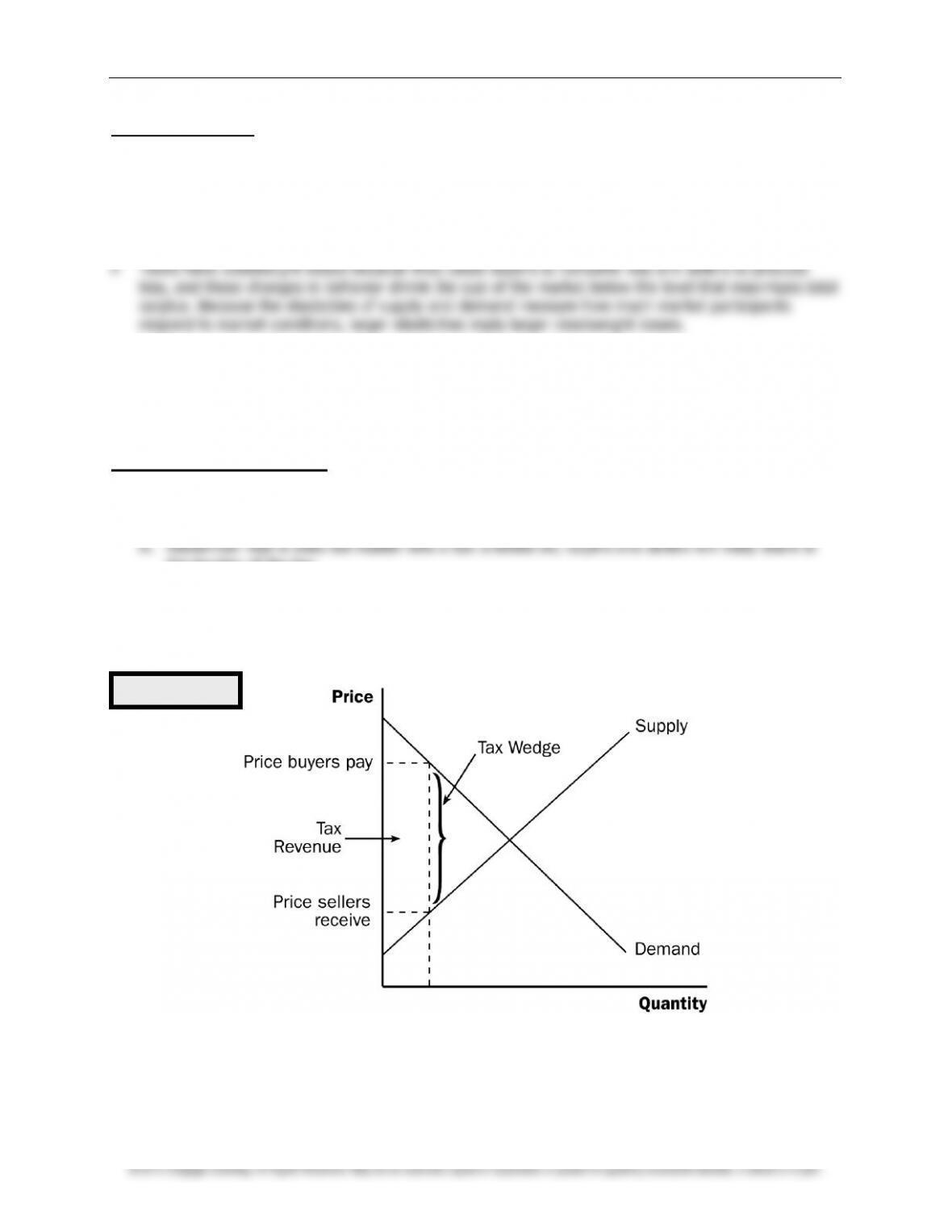

the burden of the tax.

B. If there is a tax on a product, the price that a buyer pays will be greater than the price the seller

receives. Thus, there is a tax wedge between the two prices and the quantity sold will be smaller

if there was no tax.

Figure 1

146 ❖ Chapter 8 /Application: The Costs of Taxation

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

C. How a Tax Affects Market Participants

1. We can measure the effects of a tax on consumers by examining the change in consumer

change in producer surplus.

2. However, there is a third party that is affected by the tax—the government, which gets total

3. Welfare without a Tax

b. Producer surplus is equal to: D + E + F.

4. Welfare with a Tax

a. Consumer surplus is equal to: A.

Figure 2

If you spent enough time covering consumer and producer surplus in Chapter 7,

students should have an easy time with this concept.

Figure 3

Chapter 8 /Application: The Costs of Taxation ❖ 147

b. Producer surplus is equal to: F.

d. Total surplus is equal to: A + B + D + F.

5. Changes in Welfare

a. Consumer surplus changes by: –(B + C).

b. Producer surplus changes by: –(D + E).

c. Tax revenue changes by: +(B + D).

d. Total surplus changes by: –(C + E).

6. Definition of deadweight loss: the fall in total surplus that results from a market

distortion, such as a tax.

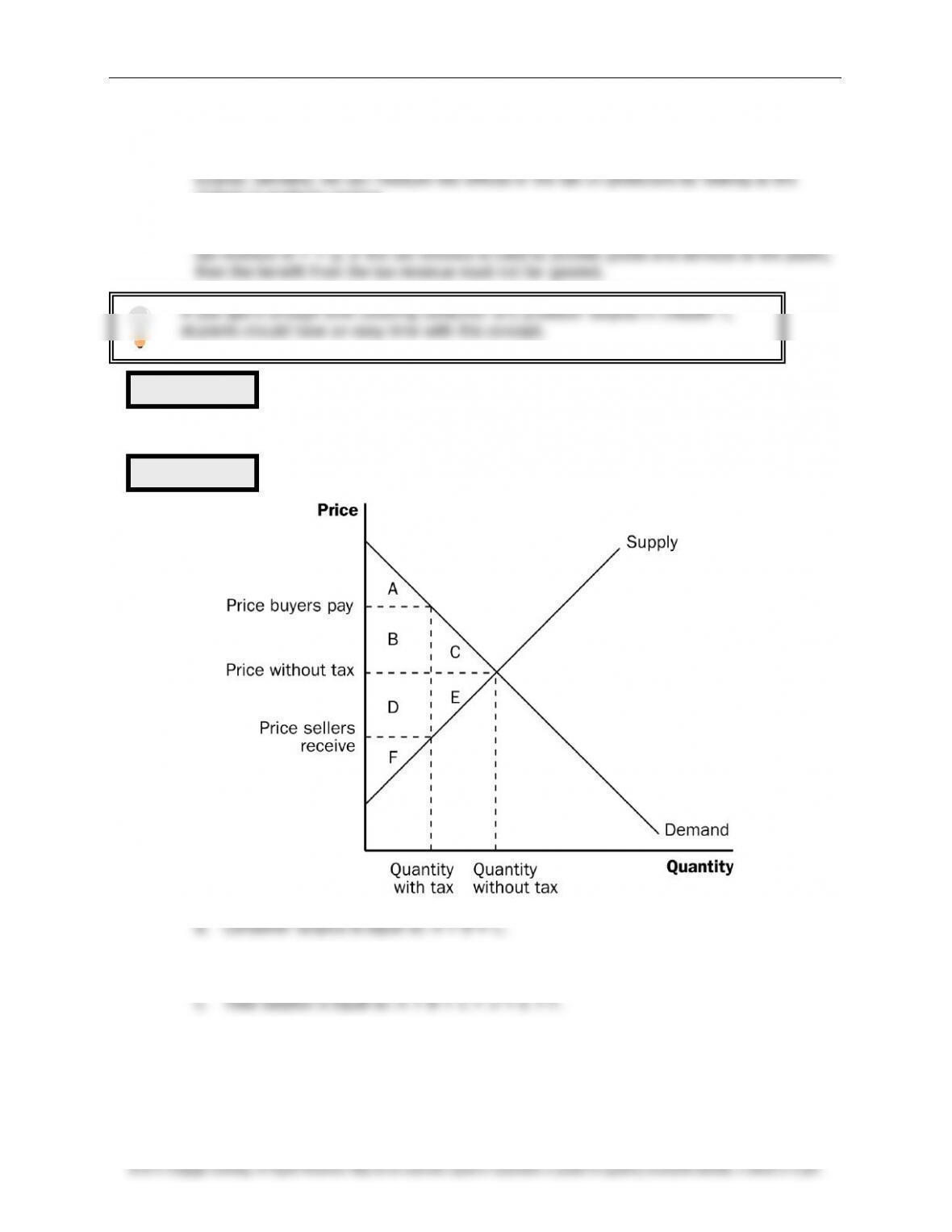

D. Deadweight Losses and the Gains from Trade

1. Taxes cause deadweight losses because they prevent buyers and sellers from benefiting from

trade.

2. This occurs because the quantity of output declines; trades that would be beneficial to both

4. Note that output levels between the equilibrium quantity without the tax and the quantity

with the tax will not be produced, yet the value of these units to consumers (represented by

supply curve).

Figure 4

Show the students that the nature of this deadweight loss stems from the reduction

in the quantity of the output exchanged. Stress the idea that goods that are not

produced, consumed, or taxed do not generate benefits for anyone.

148 ❖ Chapter 8 /Application: The Costs of Taxation

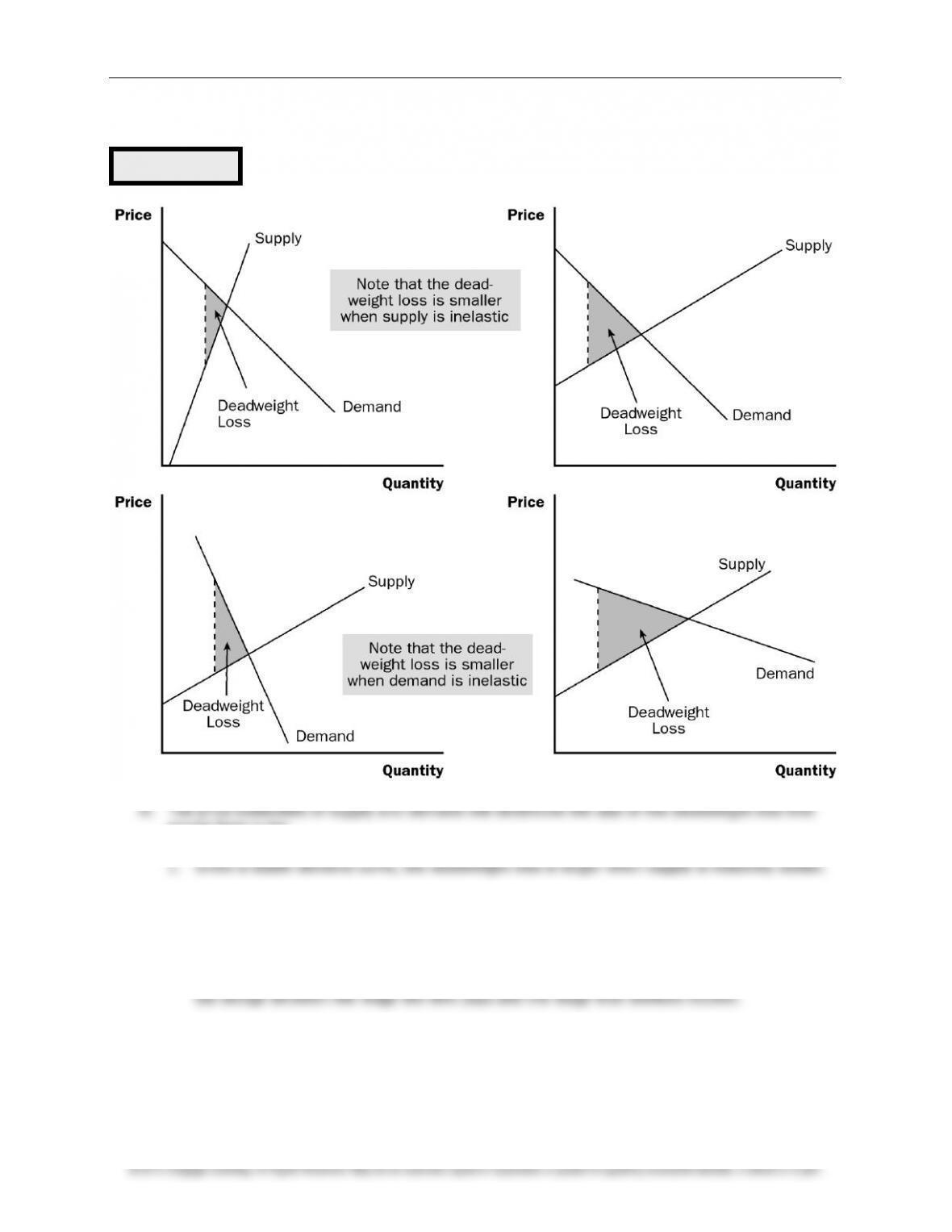

II. The Determinants of the Deadweight Loss

occurs from a tax.

2. Given a stable supply curve, the deadweight loss is larger when demand is relatively elastic.

B.

Case Study: The Deadweight Loss Debate

1. Social Security tax and federal income tax are taxes on labor earnings. A labor tax places a

2. There is considerable debate among economists concerning the size of the deadweight loss

from this wage tax.

3. The size of the deadweight loss depends on the elasticity of labor supply and demand, and

there is disagreement about the magnitude of the elasticity of supply.

Figure 5

Chapter 8 /Application: The Costs of Taxation ❖ 149

a. Economists who argue that labor taxes do not greatly distort market outcomes believe

that labor supply is fairly inelastic.

b. Economists who argue that labor taxes lead to large deadweight losses believe that labor

supply is more elastic.

III. Deadweight Loss and Tax Revenue as Taxes Vary

A. As taxes increase, the deadweight loss from the tax increases.

B. In fact, as taxes increase, the deadweight loss rises more quickly than the size of the tax.

1. The deadweight loss is the area of a triangle and the area of a triangle depends on the

square of its size.

Activity 1—Labor Taxes

Type: In-class discussion

Topics: Deadweight loss, taxation

Materials needed: None

Time: 10 minutes

Class limitations: Works in any size class

Purpose

Most students have not spent a great deal of time considering the effects of taxation on labor

supply. This in-class exercise gives them the opportunity to consider the effects of proposed

tax rates on their own willingness to supply labor.

Instructions

Ask students to assume that they are full-time workers earning $10 per hour, $80 per day,

$400 per week, $20,000 per year.

Ask them if they would quit their jobs or keep working if the tax rate was 10%, 20%, 30%,

… (up to 100%).

Keep a tally as they show hands indicating that they are leaving the labor force.

Ask students what they think the “best” tax rate is.

Points for Discussion

Many students have no idea that current marginal tax rates are greater than 30% for many

taxpayers.

Students will likely say that a tax rate of zero would be best, but remind them that there

would be no roads, libraries, parks, or national defense without at least some revenue raised

Figure 6

150 ❖ Chapter 8 /Application: The Costs of Taxation

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

2. If we double the size of a tax, the base and height of the triangle both double so the area of

the triangle (the deadweight loss) rises by a factor of four.

C. As the tax increases, the level of tax revenue will eventually fall.

D.

Case Study: The Laffer Curve and Supply-Side Economics

curve.

2. Supply-side economists in the 1980s used the Laffer curve to support their belief that a drop

in tax rates could lead to an increase in tax revenue for the government.

3. Economists continue to debate Laffer’s argument.

b. Others believe that the events of the 1980s tell a more favorable supply-side story.

c. Some economists believe that, while an overall cut in taxes normally decreases revenue,

some taxpayers may find themselves on the wrong side of the Laffer curve.

E.

In the News:

The Tax Debate

higher-income taxpayers.

2. These two opinion pieces from

The Wall Street Journal

present both sides of the issue.

ALTERNATIVE CLASSROOM EXAMPLE:

Draw a graph showing the demand and supply of paper clips. (Draw each curve as a 45–

degree line so that buyers and sellers will share any tax equally.) Mark the equilibrium price

as $0.50 (per box) and the equilibrium quantity as 1,000 boxes. Show students the areas of

producer and consumer surplus.

Impose a $0.20 tax on each box. Assume that sellers are required to “pay” the tax to the

government. Show students that:

the price buyers pay will rise to $0.60.

the price sellers receive will fall to $0.40.

the quantity of paper clips purchased will fall (assume to 800 units).

tax revenue would be equal to $160 ($0.20 800).

Have students calculate the area of deadweight loss. (You may have to remind students how

to calculate the area of a triangle.)

Show students that as the tax increases (to $0.40, $0.60, and $0.80), tax revenue rises and

then falls, and the deadweight loss increases.

Chapter 8 /Application: The Costs of Taxation ❖ 151

Activity 2—Tax Alternatives

Type: In-class assignment

Topics: Taxes and deadweight loss

Materials needed: None

Time: 20 minutes

Class limitations: Works in any size class

Purpose

The market impact of taxes can be a new concept to many students. This exercise helps them

think about the effects of taxes on different goods. Taxes that may be appealing for equity

reasons can be distortionary from a market perspective.

Instructions

Tell the class, “The state has decided to increase funding for public education. They are

considering four alternative taxes to finance these expenditures. All four taxes would raise the

same amount of revenue.” List these options on the board:

1. A sales tax on food.

2. A tax on families with school-age children.

3. A property tax on vacation homes.

then discuss their answers before moving to the next question:

A. Taxes change incentives. How might individuals change their behavior because of

each of these taxes?

B. Rank these taxes from smallest deadweight loss to largest deadweight loss. Explain.

C. Is deadweight loss the only thing to consider when designing a tax system?

Common Answers and Points for Discussion

A. Taxes change incentives. How might individuals change their behavior because of

each of these taxes?

1. A sales tax on food: At the margin, some consumers will purchase less food.

for adoption to avoid taxes. A large tax could have implications for family

planning; couples may choose not to have children, or to have fewer children,

over time. A more realistic concern would be relocation to other states by mobile

families to avoid the tax.

3. A property tax on vacation homes: This tax would be concentrated on fewer

Developers would build fewer vacation homes in the long run. In many areas,

people could choose an out-of-state vacation home to avoid the tax.

4. A sales tax on jewelry: This tax would also be relatively concentrated. People