321

8

roduction

WHAT’S NEW IN THE SEVENTH EDITION:

The tables and values have been updated to the most recently available numbers. The

In The News

feature on “The Economics of Immigration” has been updated.

LEARNING OBJECTIVES:

By the end of this chapter, students should understand:

the labor demand of competitive, profit-maximizing firms.

why equilibrium wages equal the value of the marginal product of labor.

how the other factors of production—land and capital—are compensated.

CONTEXT AND PURPOSE:

Chapter 18 is the first chapter in a three-chapter sequence that addresses the economics of labor

altering the distribution of income.

The purpose of Chapter 18 is to provide the basic theory for the analysis of factor markets—the

markets for labor, land, and capital. As you might expect, we find that the wages earned by the factors of

production depend on the supply and demand for the factor. What is new in the analysis is that the

KEY POINTS:

The economy’s income is distributed in the markets for the factors of production. The three most

THE MARKETS FOR THE

FACTORS OF PRODUCTION

18

322 ❖ Chapter 18/The Markets for the Factors of Production

The demand for factors, such as labor, is a derived demand that comes from firms that use the

factors to produce goods and services. Competitive, profit-maximizing firms hire each factor up to the

point at which the value of the factor’s marginal product equals its price.

The supply of labor arises from individuals’ trade-offs between work and leisure. An upward-sloping

labor supply curve means that people respond to an increase in the wage by working more hours and

enjoying less leisure.

Because factors of production are used together, the marginal product of any one factor depends on

the quantities of all factors that are available. As a result, a change in the supply of one factor alters

the equilibrium earnings of all the factors.

CHAPTER OUTLINE:

A. The markets for these factors of production are similar to the markets for goods and services

discussed earlier, but they are different in one important way.

B. The demand for a factor of production is a

derived demand

, meaning that the firm’s demand for

II. The Demand for Labor

B. The Competitive Profit-Maximizing Firm

2. Assume that the firm operates in both a competitive output market and a competitive labor

market.

Figure 1

Begin this chapter by reviewing how demand and supply determine product prices.

Start by asking, “Why is chicken cheaper than steak?” and “Why are apples cheaper

(per pound) than grapes?” Review the explanations using supply and demand

analysis. Now ask, “Why do airline pilots earn more than school bus drivers?” and

“Why is land on the Boardwalk in Atlantic City more expensive than land 50 miles

southwest of Atlantic City?”

In the market for labor, households are the suppliers while firms are the demanders.

You will need to remind students of this because they are used to seeing markets in

which this is reversed.

Chapter 18/The Markets for the Factors of Production ❖ 323

a. This implies that the firm is a price taker in the apple market, meaning that it has no

control over the price at which it can sell its apples.

3. Assume also that the firm’s goal is to maximize profit (total revenue – total cost).

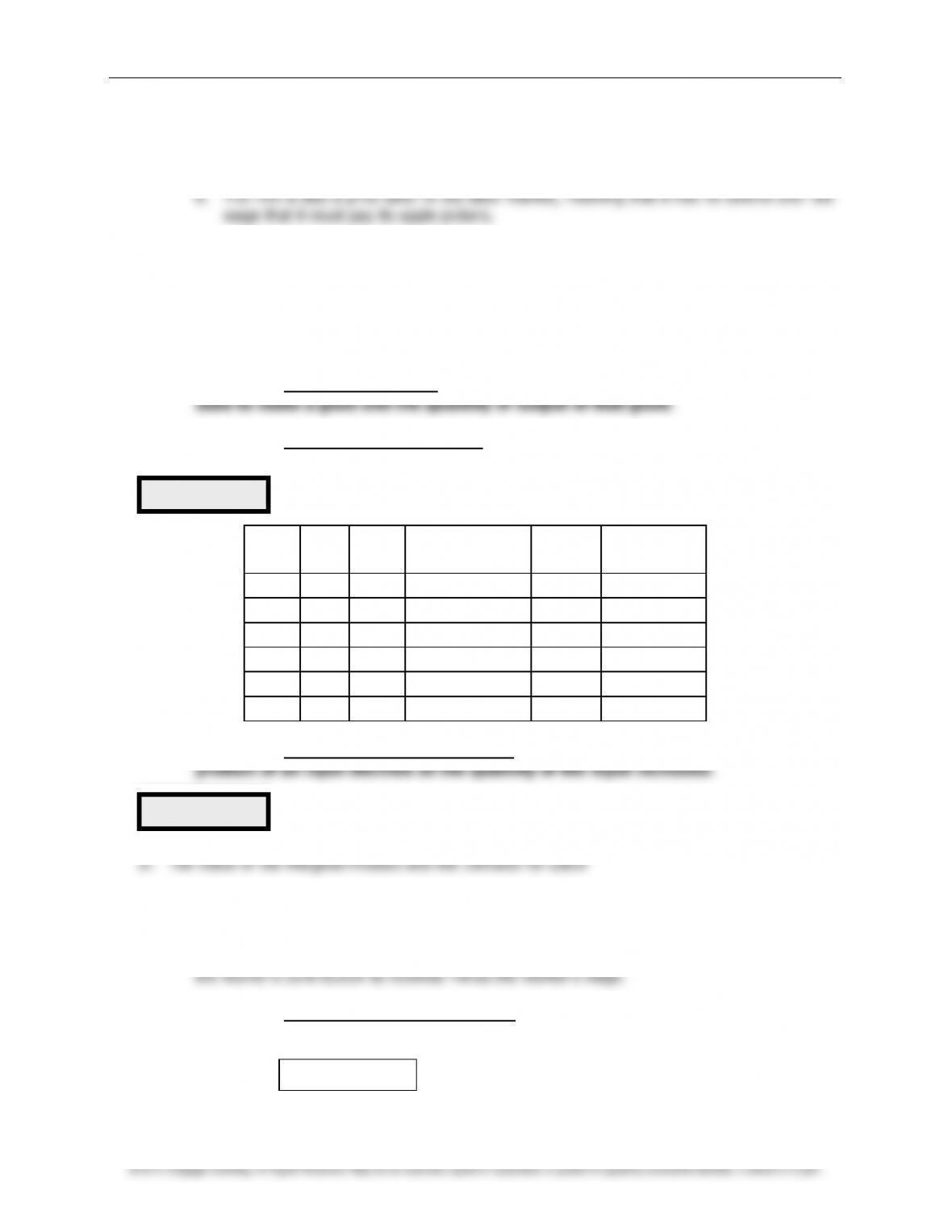

C. The Production Function and the Marginal Product of Labor

1. The firm must consider how the quantity of apples it can harvest and sell is affected by the

number of apple pickers hired.

2. Definition of production function: the relationship between the quantity of inputs

3. Definition of marginal product of labor: the increase in the amount of output from

an additional unit of labor.

L

Q

MPL

VMPL

(=

P

x

MPL

)

W

Marginal

Profit

0

0

—-

—-

—-

—-

1

100

100

$1,000

$500

$500

2

180

80

800

500

300

3

240

60

600

500

100

4

280

40

400

500

–100

5

300

20

200

500

–300

4. Definition of diminishing marginal product: the property whereby the marginal

1. When deciding how many workers to hire, the firm considers how much profit each worker

would bring in.

2. Because profit equals total revenue minus total cost, the profit from an additional worker is

3. Definition of value of the marginal product: the marginal product of an input times

the price of the output.

Table 1

Figure 2

VMPL = P MPL

a. Economists sometimes refer to the value of the marginal product as the firm’s

marginal

revenue product

.

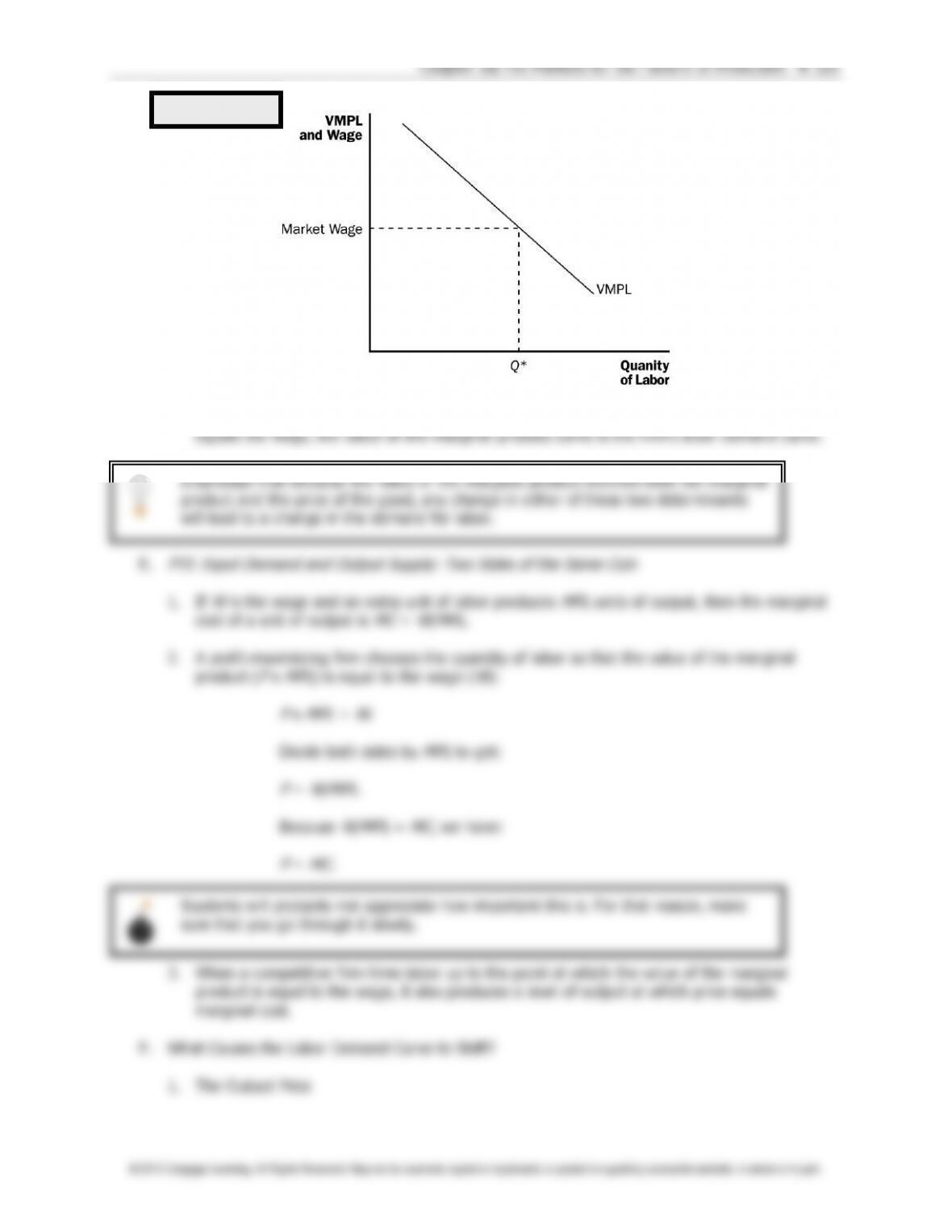

4. If the wage for workers is $500 per week, the firm will only hire three workers.

b. For the fourth worker, the value of the marginal product is lower than the wage, so the

5. We can show the firm’s decision graphically.

market.

6. A competitive, profit-maximizing firm hires workers up to the point at which the value of the

marginal product of labor equals the wage.

ALTERNATIVE CLASSROOM EXAMPLE:

Binkle, Inc. produces and sells plastic bottles in a perfectly competitive market at a price of

$0.25. Binkle hires its labor in a perfectly competitive labor market at an hourly wage of $10.

The relationship between the quantity of labor hired and the amount of output produced per

hour is presented in the following table:

L

Q

MPL

VMPL

(=

P

x

MPL

)

W

Marginal Profit

0

0

—-

—-

—-

—-

1

90

90

$22.5

$10

$12.5

2

170

80

20

10

10

3

240

70

17.5

10

7.5

4

300

60

15

10

5

5

350

50

12.5

10

2.5

6

390

40

10

10

0

7

420

30

7.5

10

–2.5

8

440

20

5

10

–5

7. Because the firm chooses the quantity of labor at which the value of the marginal product

E.

FYI: Input Demand and Output Supply: Two Sides of the Same Coin

cost of a unit of output is

MC

=

W

/

MPL

.

2. A profit-maximizing firm chooses the quantity of labor so that the value of the marginal

product (

P

x

MPL

) is equal to the wage (

W

):

P

x

MPL

=

W

.

Divide both sides by

MPL

to get:

P

=

W/MPL

.

Because

W/MPL

=

MC

, we have:

P

=

MC

.

3. When a competitive firm hires labor up to the point at which the value of the marginal

product is equal to the wage, it also produces a level of output at which price equals

marginal cost.

1. The Output Price

Figure 3

Students will probably not appreciate how important this is. For that reason, make

sure that you go through it slowly.

Emphasize that because the value of the marginal product involves both the marginal

product and the price of the good, any change in either of these two determinants

will lead to a change in the demand for labor.

a. An increase in the price of the product raises the value of the marginal product of labor

and therefore increases the demand for labor.

2. Technological Change

a. Technological advance raises the marginal product of labor, which in turn raises the

value of the marginal product of labor.

technological change (such as an industrial robot) could reduce the marginal product of

labor and thus the value of the marginal product of labor.

3. The Supply of Other Factors

b. Therefore, any change in the availability of another factor will likely affect the demand

for labor.

III. The Supply of Labor

A. The Trade-off between Work and Leisure

2. The opportunity cost of an hour of leisure is the amount of money that would have been

earned if that hour were spent at work.

3. Therefore, as the wage increases, so does the opportunity cost of leisure.

4. The labor supply curve shows how individuals respond to changes in the wage in terms of

the labor–leisure trade-off.

a. An upward-sloping labor supply curve means that an increase in the wage induces

workers to increase the quantity of labor they supply.

b. Note that, for some individuals, the labor supply curve may in fact be backward bending.

This possibility is discussed in more detail in Chapter 21.

B. What Causes the Labor Supply Curve to Shift?

1. Changes in Tastes (for leisure vs. working)

2. Changes in Alternative Opportunities (other occupations)

3. Immigration

Chapter 18/The Markets for the Factors of Production ❖ 327

IV. Equilibrium in the Labor Market

A. Marginal Product in Equilibrium

1. The wage adjusts to balance the quantity of labor supplied and the quantity of labor

demanded.

2. The wage equals the value of the marginal product of labor.

3. At the labor market equilibrium, each firm has bought as much labor as it finds profitable at

the equilibrium wage.

4. Thus, any event that changes the supply or demand for labor must change the equilibrium

wage and the value of the marginal product by the same amount, because these must

always be equal.

B. Shifts in Labor Supply

a. As the number of workers employed rises, the marginal product of labor falls due to the

diminishing marginal product of labor.

b. Thus, both the wage and the value of the marginal product of labor are now lower.

a. As the number of workers employed falls, the marginal product of labor rises due to the

diminishing marginal product of labor.

b. Thus, both the wage and the value of the marginal product of labor are now higher.

3.

In the News: The Economics of Immigration

b. This is an interview with economist Pia Orrenius, an economist at the Federal Reserve

Bank of Dallas, who studies the economic impact of increased immigration.

C. Shifts in Labor Demand

Figure 4

Figure 5

Go through each of these shifts carefully with the class. Make sure that they see the

relationship between the change in the equilibrium wage and the change in the value

of the marginal product of labor.

328 ❖ Chapter 18/The Markets for the Factors of Production

a. The value of the marginal product rises because

VMPL

=

P

×

MPL

(and either

P

or

MPL

b. This implies that both the wage and the value of the marginal product are now higher.

2. A decrease in the demand for labor will shift the labor demand curve to the left, creating a

surplus at the original wage. This will put downward pressure on the equilibrium wage

a. The value of the marginal product falls because

VMPL

=

P

×

MPL

(and either

P

or

MPL

b. This implies that both the wage and the value of the marginal product are now lower.

D.

Case Study: Productivity and Wages

2. This means that highly productive workers are highly paid, and less productive workers are

less highly paid.

3. Table 2 shows data on the growth rates of both productivity and wages in the United States

from 1959 to 2012.

1973 or the period since 1995.

E.

FYI: Monopsony

2. This type of labor market is called a

monopsony

.

wage.

V. The Other Factors of Production: Land and Capital

Figure 6

Table 2

Compare the difference in outcomes between perfect competition and monopoly in

output markets with the differences between perfect competition and monopsony in

labor markets.

Chapter 18/The Markets for the Factors of Production ❖ 329

B. Equilibrium in the Markets for Land and Capital

indefinitely.

2. The rental price of land or capital is the price paid to use that factor for a limited amount of

time.

a. The rental price of land is determined by the supply and demand for land; the rental

price of capital is determined by the supply and demand for capital.

b. For both land and capital, the firm increases the quantity hired until the value of the

4. As long as the firms using the factors of production are competitive and profit maximizing,

land, labor, and capital each earn the value of their marginal contribution to the production

process.

5. The purchase price of land and capital depend on the current value of the marginal product

and the expected future value of the marginal product.

C.

FYI: What Is Capital Income?

1. The measurement of capital income is less obvious than the measurement of labor income.

2. Capital income is the rent that households receive for the use of their capital.

3. Some of the earnings from capital are paid to households in the form of interest or dividends.

4. Also, some of the earnings from capital may be retained by the firm for future purchases of

capital.

D. Linkages among the Factors of Production

used in the production process.

2. This means that a change in the supply of any one factor can change the earnings of all of

the factors.

4.

Case Study: The Economics of the Black Death

Figure 7

a. In 14th-century Europe, the bubonic plague killed about one-third of the population

within a few years.

product of labor rises.

c. With fewer workers available to work the land, each additional unit of land was able to

produce less additional output. Thus, the marginal product of land fell. Because this

would lead to a decrease in the value of the marginal product of land as well, we would

d. History shows that our predictions are correct: Wages doubled during the period and

rents declined by 50%.

SOLUTIONS TO TEXT PROBLEMS:

Quick Quizzes

price of the output.

A competitive, profit-maximizing firm decides how many workers to hire by hiring workers up

to the point where the value of the marginal product of labor equals the wage.

expensive for them.

3. An immigration of workers increases labor supply but has no effect on labor demand. The

result is an increase in the equilibrium quantity of labor and a decline in the equilibrium

wage, as shown in Figure 1. The decline in the equilibrium wage causes the quantity of labor

product of labor to decrease.