Chapter 13/The Costs of Production ❖ 231

A. The division of total costs into fixed and variable costs will vary from firm to firm.

2. Once a factory is chosen, the firm must deal with the short-run costs associated with that

plant size.

C. The long-run average-total-cost curve lies along the lowest points of the short-run average-total-

cost curves because the firm has more flexibility in the long run to deal with changes in

production.

D. The long-run average-total-cost curve is typically U-shaped, but is much flatter than a typical

short-run average-total-cost curve.

E. The length of time for a firm to get to the long run will depend on the firm involved.

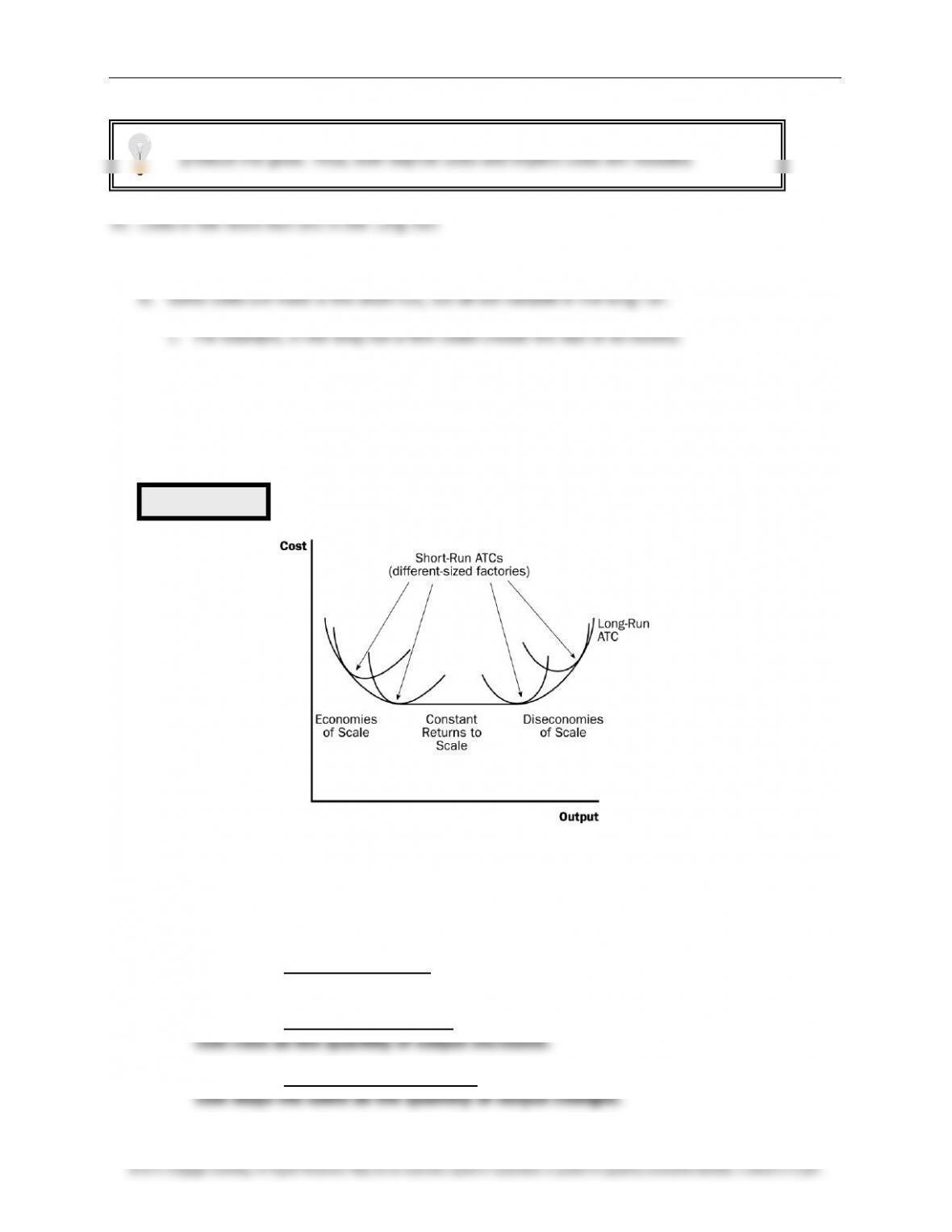

F. Economies and Diseconomies of Scale

1. Definition of economies of scale: the property whereby long-run average total cost

falls as the quantity of output increases.

2. Definition of diseconomies of scale: the property whereby long-run average total

3. Definition of constant returns to scale: the property whereby long-run average total

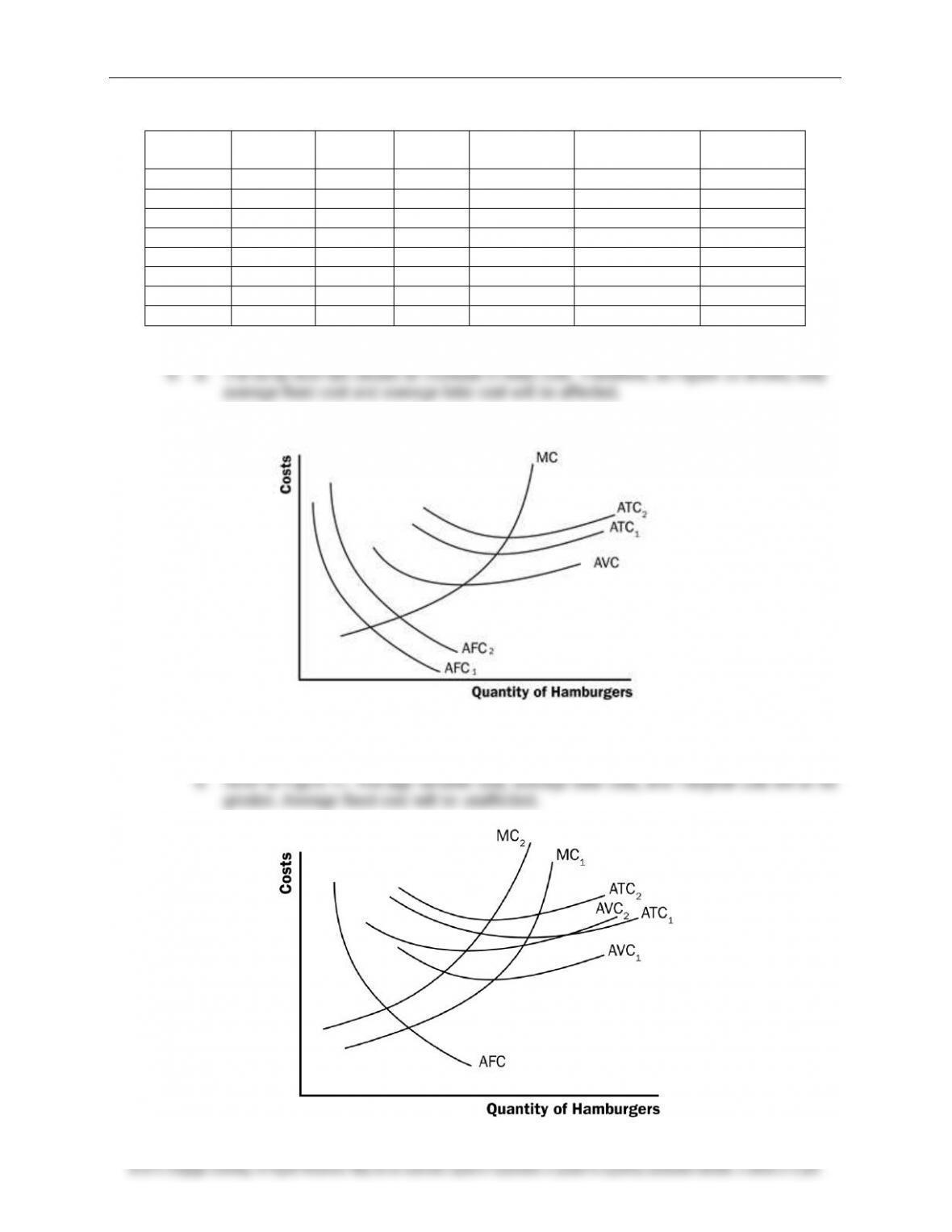

Figure 6

Emphasize that these cost curves include ALL costs for the resources needed to

produce the good. Thus, both explicit costs and implicit costs are included.

232 ❖ Chapter 13/The Costs of Production

4.

FYI: Lessons from a Pin Factory

perform many different tasks.

b. The use of specialization allows firms to achieve economies of scale.

SOLUTIONS TO TEXT PROBLEMS:

Quick Quizzes

1. Farmer McDonald’s opportunity cost is $300, consisting of 10 hours of lessons at $20 an hour

an economic loss of $100 ($200 sales minus $300 opportunity cost).

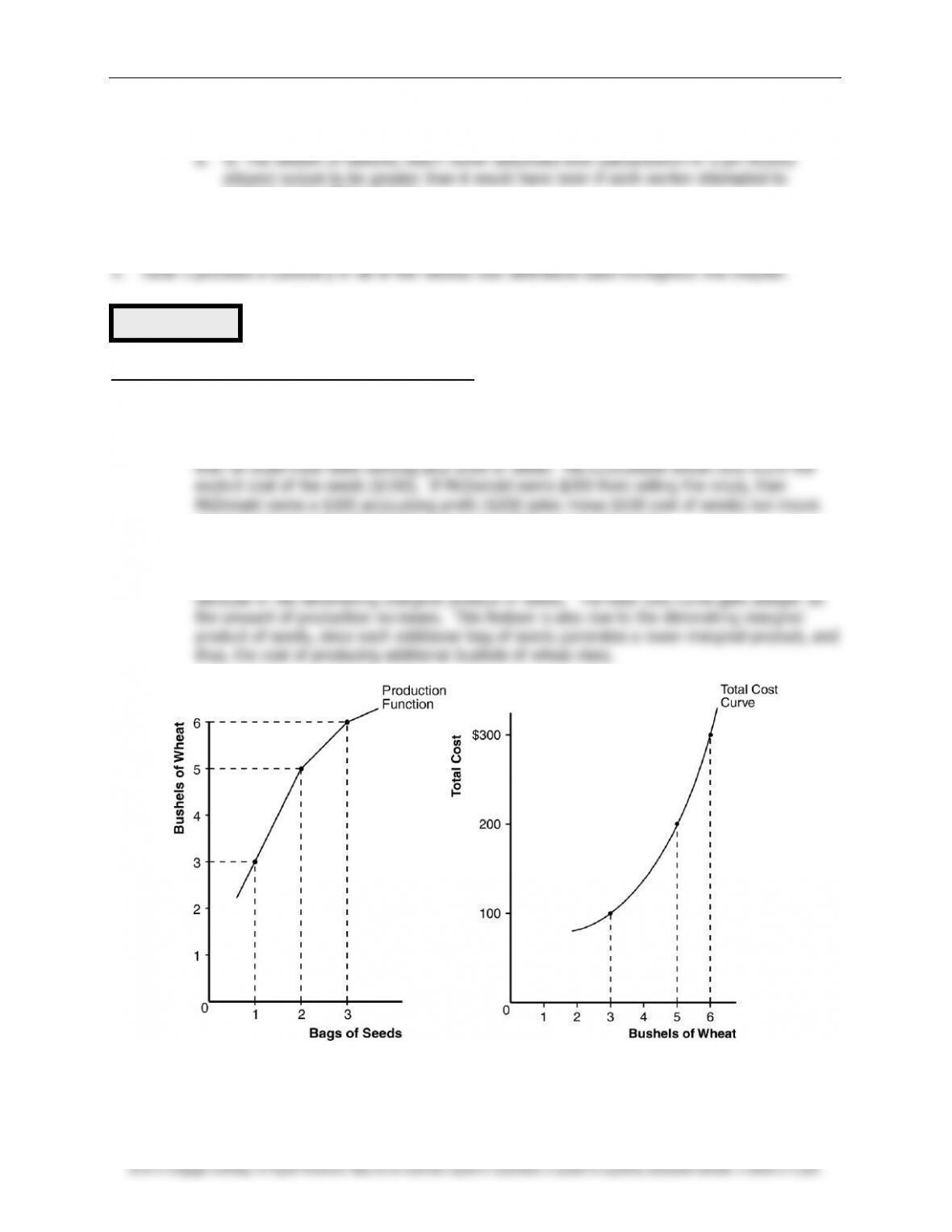

2. Farmer Jones’s production function is shown in Figure 1 and his total-cost curve is shown in

Figure 2. The production function becomes flatter as the number of bags of seeds increases

Figure 1 Figure 2

Table 3

Chapter 13/The Costs of Production ❖ 233

3. The average total cost of producing 5 cars is $250,000/5 = $50,000. Since total cost rose

from $225,000 to $250,000 when output increased from 4 to 5, the marginal cost of the fifth

car is $25,000.

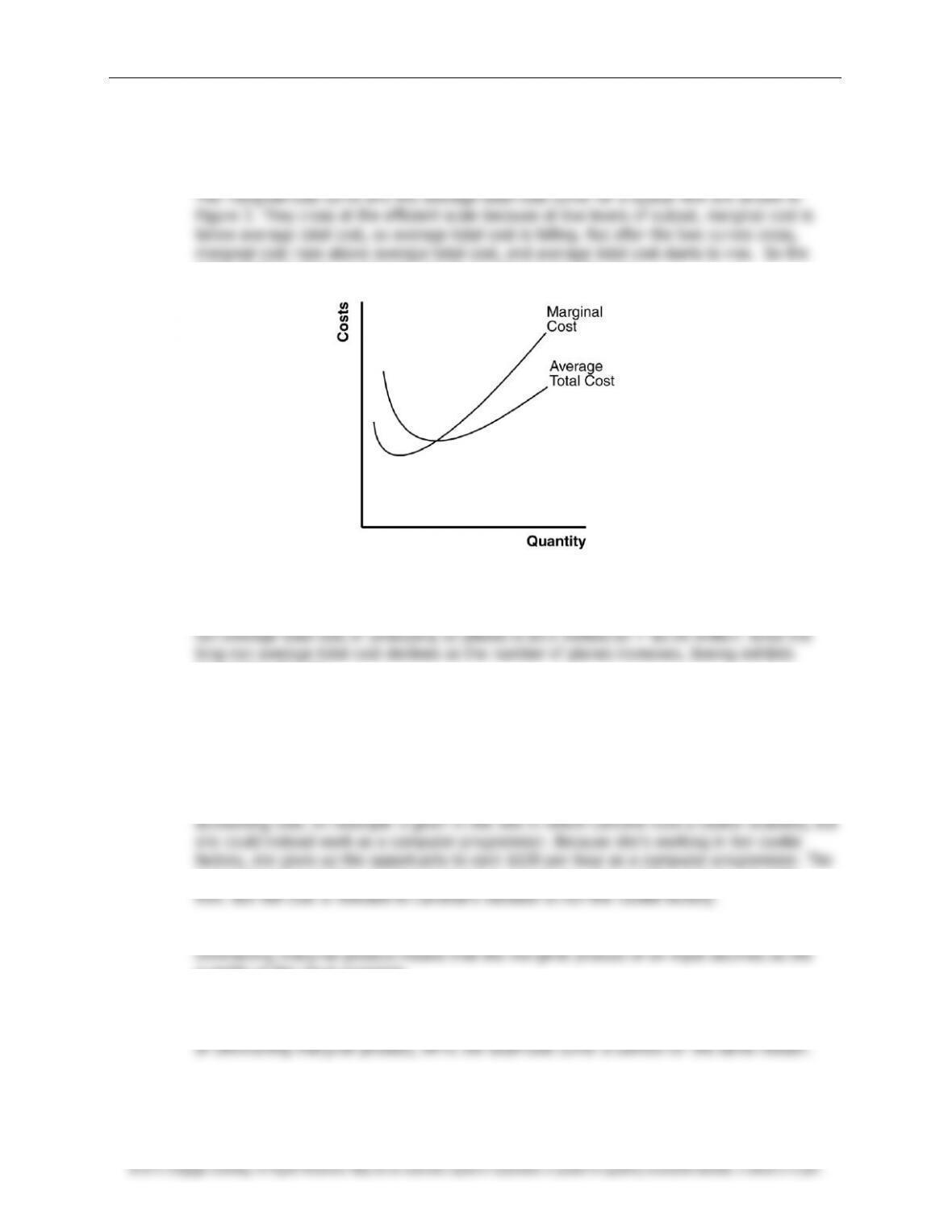

point of intersection must be the minimum of average total cost.

Figure 3

4. The long-run average total cost of producing 9 planes is $9 million/9 = $1 million. The long–

economies of scale.

Questions for Review

1. The relationship between a firm’s total revenue, profit, and total cost is profit equals total

revenue minus total costs.

2. An accountant would not count the owner’s opportunity cost of alternative employment as an

accountant ignores this opportunity cost because money does not flow into or out of the

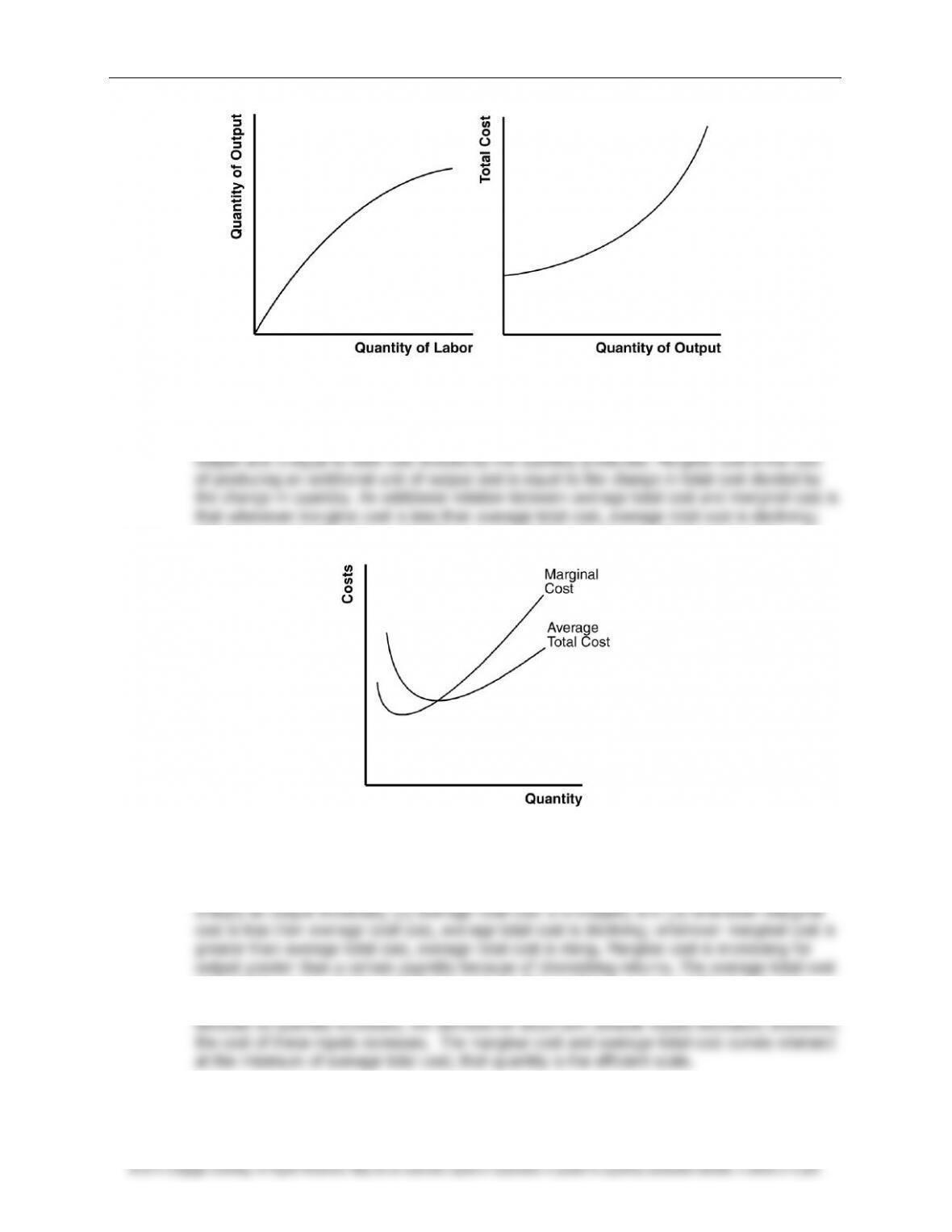

3. Marginal product is the increase in output that arises from an additional unit of input.

quantity of the input increases.

4. Figure 4 shows a production function that exhibits diminishing marginal product of labor.

Figure 5 shows the associated total-cost curve. The production function is concave because

234 ❖ Chapter 13/The Costs of Production

Figure 4 Figure 5

5. Total cost consists of the costs of all inputs needed to produce a given quantity of output. It

includes fixed costs and variable costs. Average total cost is the cost of a typical unit of

whenever marginal cost is greater than average total cost, average total cost is rising.

Figure 6

6. Figure 6 shows the marginal-cost curve and the average-total-cost curve for a typical firm.

There are three main features of these curves: (1) marginal cost is U-shaped but rises

curve is downward-sloping initially because the firm is able to spread out fixed costs over

additional units. The average-total-cost curve is increasing beyond some output level

Chapter 13/The Costs of Production ❖ 235

7. In the long run, a firm can adjust the factors of production that are fixed in the short run; for

8. Economies of scale exist when long-run average total cost decreases as the quantity of

output increases, which occurs because of specialization among workers. Diseconomies of

scale exist when long-run average total cost rises as the quantity of output increases, which

occurs because of the coordination problems inherent in a large organization.

Quick Check Multiple Choice

1. a

2. d

3. d

4. c

5. b

6. a

Problems and Applications

1. a. opportunity cost; b. average total cost; c. fixed cost; d. variable cost; e. total cost; f.

marginal cost.

2. a. The opportunity cost of something is what must be given up to acquire it.

b. The opportunity cost of running the hardware store is $550,000, consisting of $500,000

to rent the store and buy the stock and a $50,000 implicit cost, because your aunt would

quit her job as an accountant to run the store. Because the total opportunity cost of

$550,000 exceeds the projected revenue of $510,000, your aunt should not open the

store, as her economic profit would be negative.

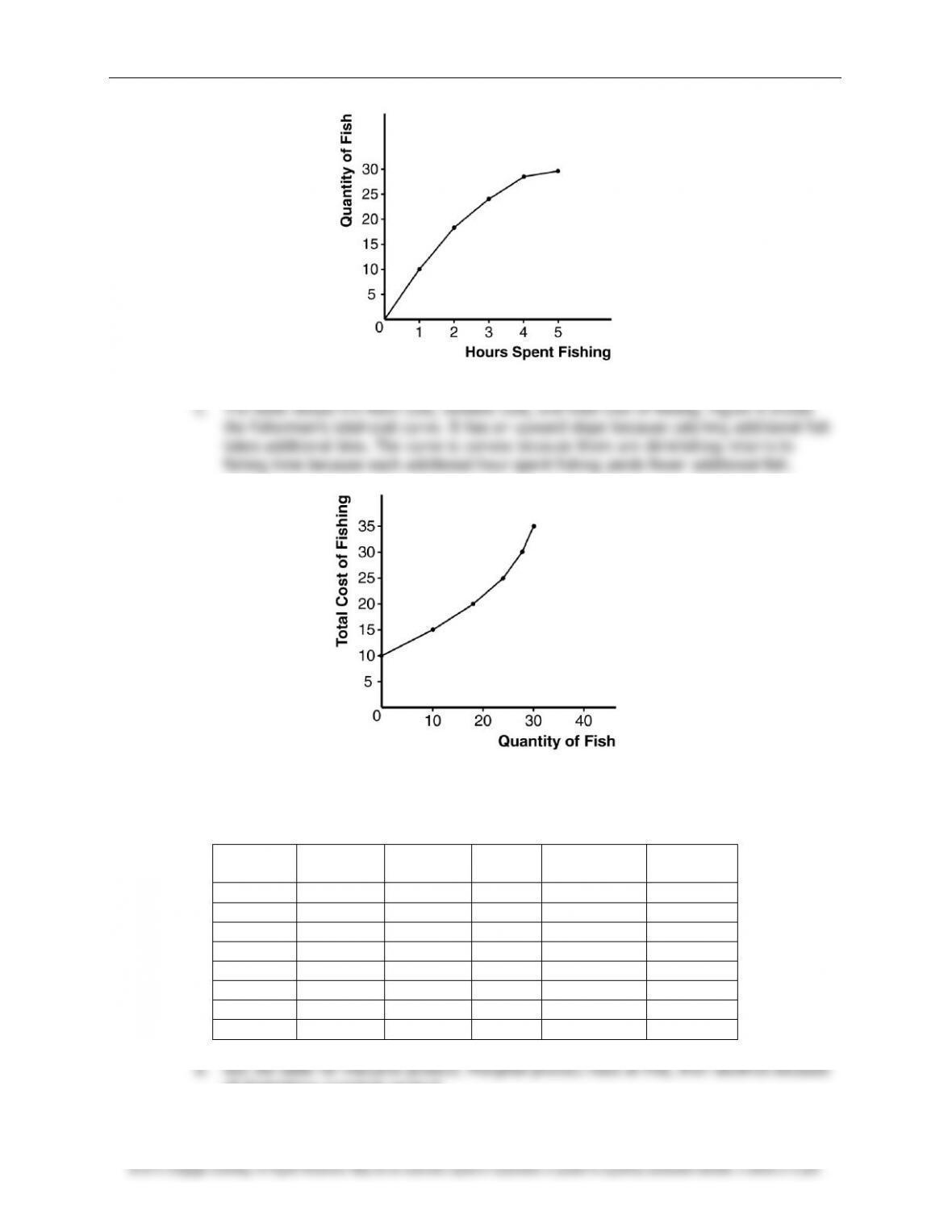

3. a. The following table shows the marginal product of each hour spent fishing:

Hours

Fish

Fixed Cost

Variable Cost

Total Cost

Marginal Product

0

0

$10

$0

$10

—

1

10

10

5

15

10

2

18

10

10

20

8

3

24

10

15

25

6

4

28

10

20

30

4

5

30

10

25

35

2

product.

236 ❖ Chapter 13/The Costs of Production

Figure 7

Figure 8

4. Here is the completed table:

Workers

Output

Marginal

Product

Total

Cost

Average

Total Cost

Marginal

Cost

0

0

—

$200

—

—

1

20

20

300

$15.00

$5.00

2

50

30

400

8.00

3.33

3

90

40

500

5.56

2.50

4

120

30

600

5.00

3.33

5

140

20

700

5.00

5.00

6

150

10

800

5.33

10.00

7

155

5

900

5.81

20.00

of diminishing marginal product.

Chapter 13/The Costs of Production ❖ 237

b. See the table for total cost.

cost rises as quantity rises.

d. See the table for marginal cost. Marginal cost is also U-shaped, but rises steeply as

output increases. This is due to diminishing marginal product.

f. When marginal cost is less than average total cost, average total cost is falling; the cost

of the last unit produced pulls the average down. When marginal cost is greater than

average total cost, average total cost is rising; the cost of the last unit produced pushes

the average up.

6. a. The fixed cost is $300, because fixed cost equals total cost minus variable cost. At an

output of zero, the only costs are fixed cost.

b.

Quantity

Total

Cost

Variable

Cost

Marginal Cost

(using total cost)

Marginal Cost

(using variable cost)

0

$300

$0

—

—

1

350

50

$50

$50

2

390

90

40

40

3

420

120

30

30

4

450

150

30

30

5

490

190

40

40

6

540

240

50

50

7. The following table illustrates average fixed cost (

AFC

), average variable cost (

AVC

), and

because that minimizes average total cost.

238 ❖ Chapter 13/The Costs of Production

Quantity

Variable

Cost

Fixed

Cost

Total

Cost

Average

Fixed Cost

Average

Variable Cost

Average

Total Cost

0

$0.00

$200.00

$200.00

—

—

—

1

10.00

200.00

210.00

$200.00

$10.00

$210.00

2

20.00

200.00

220.00

100.00

10.00

110.00

3

40.00

200.00

240.00

66.67

13.33

80.00

4

80.00

200.00

280.00

50.00

20.00

70.00

5

160.00

200.00

360.00

40.00

32.00

72.00

6

320.00

200.00

520.00

33.33

53.33

86.67

7

640.00

200.00

840.00

28.57

91.43

120.00

Figure 10

Chapter 13/The Costs of Production ❖ 239

Figure 11

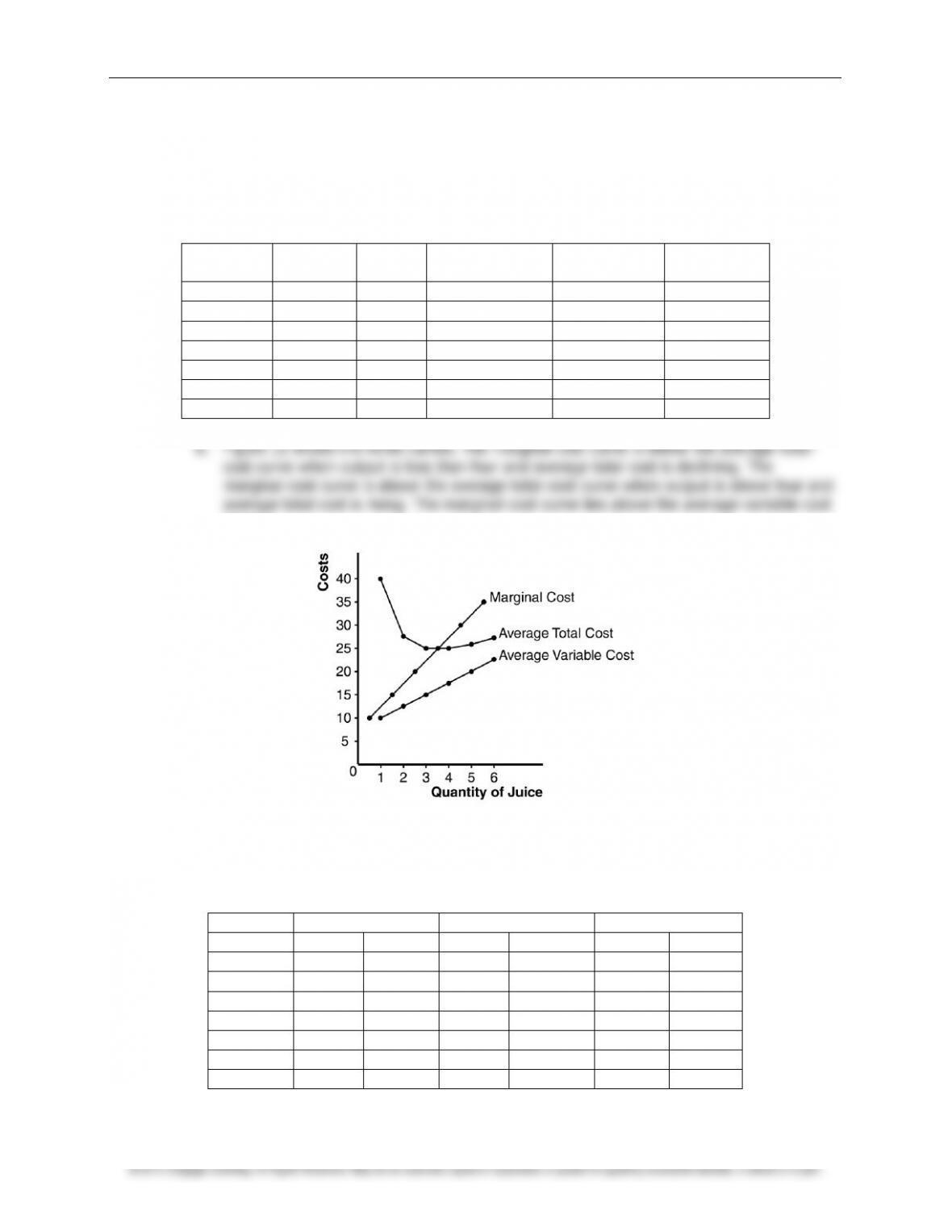

9. a. The following table shows average variable cost (

AVC

), average total cost (

ATC

), and

marginal cost (

MC

) for each quantity.

Quantity

Variable

Cost

Total

Cost

Average

Variable Cost

Average

Total Cost

Marginal

Cost

0

$0.00

$30.00

—

—

—

1

10.00

40.00

$10.00

$40.00

$10.00

2

25.00

55.00

12.50

27.50

15.00

3

45.00

75.00

15.00

25.00

20.00

4

70.00

100.00

17.50

25.00

25.00

5

100.00

130.00

20.00

26.00

30.00

6

135.00

165.00

22.50

27.50

35.00

curve.

Figure 12

10. The following table shows quantity (

Q

), total cost (

TC

), and average total cost (

ATC

) for the

three firms:

Firm A

Firm B

Firm C

Quantity

TC

ATC

TC

ATC

TC

ATC

1

$60.00

$60.00

$11.00

$11.00

$21.00

$21.00

2

70.00

35.00

24.00

12.00

34.00

17.00

3

80.00

26.67

39.00

13.00

49.00

16.33

4

90.00

22.50

56.00

14.00

66.00

16.50

5

100.00

20.00

75.00

15.00

85.00

17.00

6

110.00

18.33

96.00

16.00

106.00

17.67

7

120.00

17.14

119.00

17.00

129.00

18.43

240 ❖ Chapter 13/The Costs of Production

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Firm A has economies of scale because average total cost declines as output increases. Firm

B has diseconomies of scale because average total cost rises as output rises. Firm C has

economies of scale from one to three units of output and diseconomies of scale for levels of

output beyond three units.