Chapter 9

Time Value of Money

Discussion Questions

9-1.

How is the future value (Appendix A) related to the present value of a single

sum (Appendix B)?

The future value represents the expected worth of a single amount, whereas the

present value represents the current worth.

FV = PV (1 + i)n future value

( )

luePresent va

1

1

FVPV

+

=n

i

9-2.

How is the present value of a single sum (Appendix B) related to the present

value of an annuity (Appendix D)?

The present value of a single amount is the discounted value for one future

payment, whereas the present value of an annuity represents the discounted

value of a series of consecutive future payments of equal amount.

9-3.

Why does money have a time value?

Money has a time value because funds received today can be invested to reach a

greater value in the future. A person would rather receive $1 today than $1 in

10 years, because a dollar received today, invested at 6 percent, is worth $1.791

after 10 years.

9-4.

Does inflation have anything to do with making a dollar today worth more than

a dollar tomorrow?

Inflation makes a dollar today worth more than a dollar in the future. Because

inflation tends to erode the purchasing power of money, funds received today

will be worth more than the same amount received in the future.

9-5.

Adjust the annual formula for a future value of a single amount at 12 percent

for 10 years to a semiannual compounding formula. What are the interest

factors (FVIF) before and after? Why are they different?

( )

IF

FV PV FV Appendix A

12%, 10 3.106 Annual

6%, 20 3.207 Semiannual

in

in

=

==

==

The more frequent compounding under the semiannual compounding

assumption increases the future value so that semiannual compounding is worth

.101 more per dollar.

9-6.

If, as an investor, you had a choice of daily, monthly, or quarterly

compounding, which would you choose? Why?

The greater the number of compounding periods, the larger the future value.

The investor should choose daily compounding over monthly or quarterly.

9-7.

What is a deferred annuity?

A deferred annuity is an annuity in which the equal payments will begin at

some future point in time.

9-8.

List five different financial applications of the time value of money.

Different financial applications of the time value of money:

Equipment purchase or new product decision

Present value of a contract providing future payments

Future value of an investment

Regular payment necessary to provide a future sum

Regular payment necessary to amortize a loan

Determination of return on an investment

Determination of the value of a bond

Chapter 9

Problems

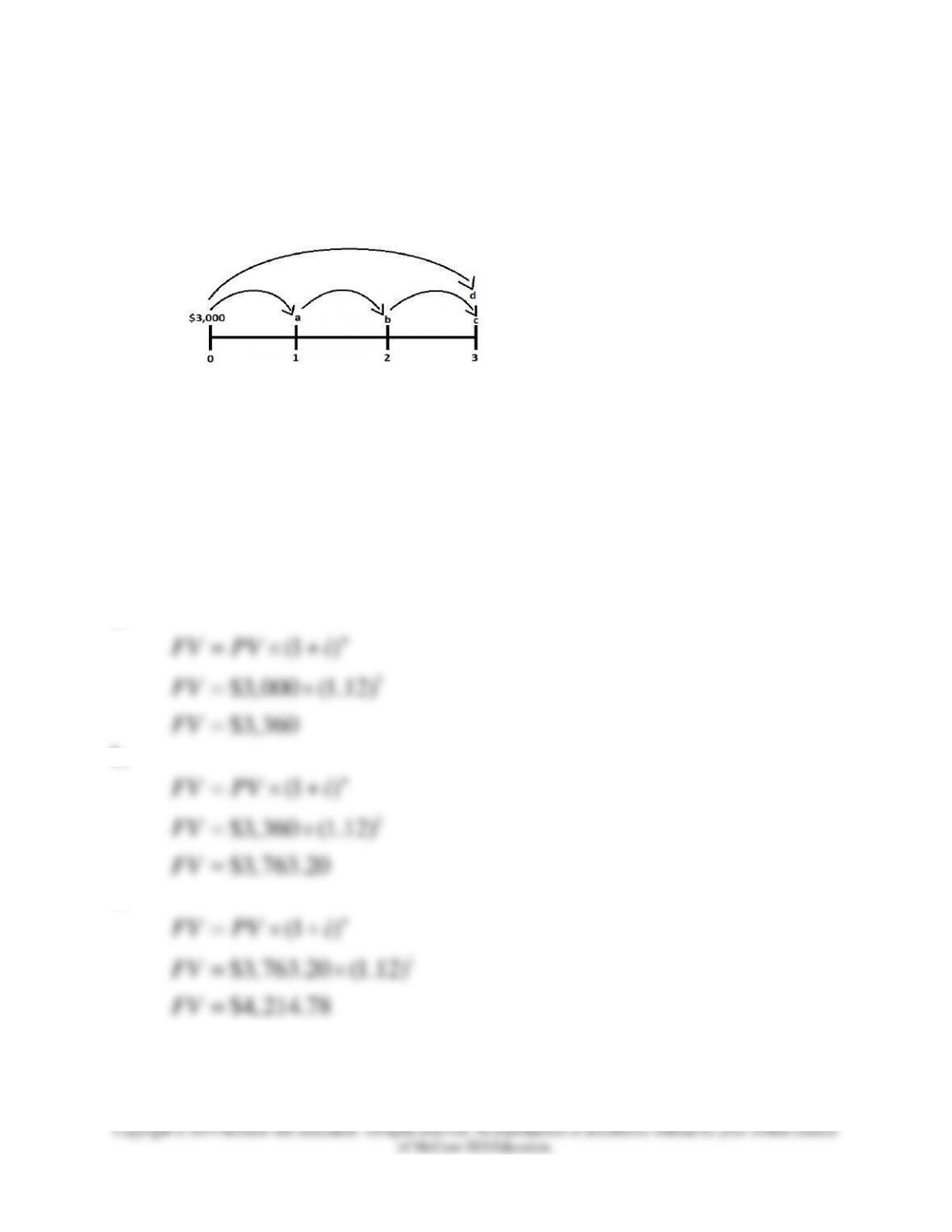

1.You invest $3,000 for three years at 12 percent.

a. What is the value of your investment after one year? Multiply $3,000 × 1.12.

b. What is the value of your investment after two years? Multiply your answer to part a

by 1.12.

c. What is the value of your investment after three years? Multiply your answer to part b

by 1.12. This gives your final answer.

d. Combine these three steps by using the formula

( )

1n

FV PV i= +

to find the future

value of $3,000 in 3 years at 12 percent interest.

9-1. Solution:

a.

1

(1 )

$3,360

n

FV PV i

FV

= +

=

b.

1

(1 )

$3,763.20

n

FV PV i

FV

= +

=

c.

1

(1 )

$4,214.78

n

FV PV i

FV

= +

=

d.

3

(1 )

$3,000 (1.12)

$4, 214.78

n

FV PV i

FV

FV

=+

=

=

Calculator Solution:

(d)

N

I/Y

PV

PMT

FV

3

12

3,000

0

CPT FV −4,214.78

Answer: $4,214.78

Solution using TVM Tables:

a. $3,000 × 1.12 = $3,360.00

2. Present value (LO9-3) What is the present value of

a. $7,900 in 10 years at 11 percent?

b. $16,600 in 5 years at 9 percent?

c. $26,000 in 14 years at 6 percent?

9-2. Solution:

a.

10

1

(1 )

1

$2,788.86

n

PV FV

i

PV

=

+

=

b.

1

(1 )

1

n

PV FV

i

=

+

3. Present Value (LO9-3)

a. What is the present value of $140,000 to be received after 30 years with a

14 percent discount rate?

b. Would the present value of the funds in part a be enough to buy a $2,900 concert

ticket?

9-3. Solution:

(a)

1

(1 )n

PV FV

i

=

+

1

$140,000 1.14

PV =

Calculator Solution:

(a)

N

I/Y

PV

PMT

FV

30

14

CPT PV -2747.78

0

140,000

Answer: $2747.78

(b)

No. You only have $2747.78.

Appendix B

PV = FV × PVIF (14%, 30 periods)

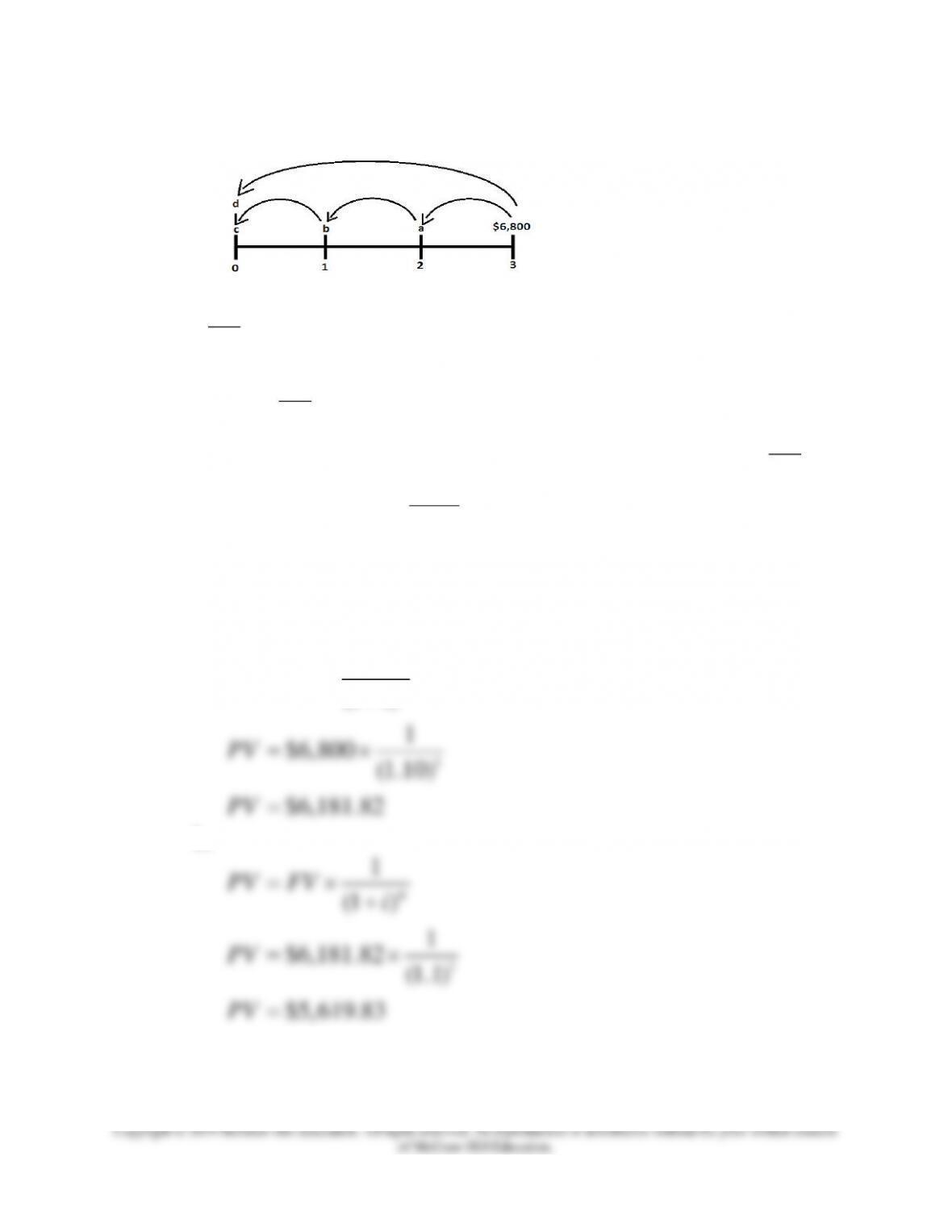

4. Present Value (LO9-4) you will receive $6,800 three years from now. The discount rate is

10 percent.

a. What is the value of your investment two years from now? Multiply $6,800 by

1

1.10

or divide by 1.10 (one year’s discount rate at 10 percent).

b. What is the value of your investment one year from now? Multiply your answer to

part a by

1

1.10

.

c. What is the value of your investment today? Multiply the part b answer by

1

1.10

.

d. Use the formula

1

(1 )n

PV FV

i

=

+

to find the present value of $6,800 received three

years from now at 10 percent interest.

9-4. Solution:

a.

1

(1 )

1

n

PV FV

i

=

+

1

1

(1 )

1

$5,108.94

n

PV FV

i

PV

=

+

=

d.

3

1

(1 )

1

$6,800 (1.1)

$5,108.94

n

PV FV

i

PV

PV

=

+

=

=

Calculator Solution:

(d)

N

I/Y

PV

PMT

FV

3

10

CPT −5,108.94

0

FV 6,800

Answer: $5,108.94

Solution using TVM Tables:

a. $6,800 × .909 = $6,181.20

b. $6,181.20× .909 = $5,618.71

c. $5,618.71× .909 = $5,107.41

d. Appendix B (10%, 3 periods)

PV= FV × PVIF

$6,800 ×.751 = $5,106.80

5. If you invest $9,000 today, how much will you have

a. In 2 years at 9 percent?

b. In 7 years at 12 percent?

c. In 25 years at 14 percent?

d. In 25 years at 14 percent (compounded semiannually)?

50

(1 )

n

FV PV i

= +

9-5. Solution:

a.

2

(1 )

$10,692.90

n

FV PV i

FV

= +

=

b.

2

(1 )

$19,896.13

n

FV PV i

FV

= +

=

c.

25

(1 )

n

FV PV i

= +

N

I/Y

PV

PMT

FV

25

14

9,000

0

CPT FV −238,157.24

Answer: $238,157.24

(d)

N

I/Y

PV

PMT

FV

50

7

9,000

0

CPT FV −265,113.23

Answer: $265,113.23

Appendix A

FV = PV × FVIF

a. $9,000 × 1.188 = $ 10,692

6. Present value (LO9-3) Your aunt offers you a choice of $20,100 in 20 years or $870

today. If money is discounted at 17 percent, which should you choose?

9-6. Solution:

1

(1 )

1

n

PV FV

i

=

+

Calculator Solution:

N

I/Y

PV

PMT

FV

20

17

−869.92

0

20,100

PV = FV × PVIF (9%, 10 periods)

Answer: $869.92

Appendix B

PV = FV × PVIF (17%, 20 periods)

PV = $20,100 × .043 = $864

Choose $870 today.

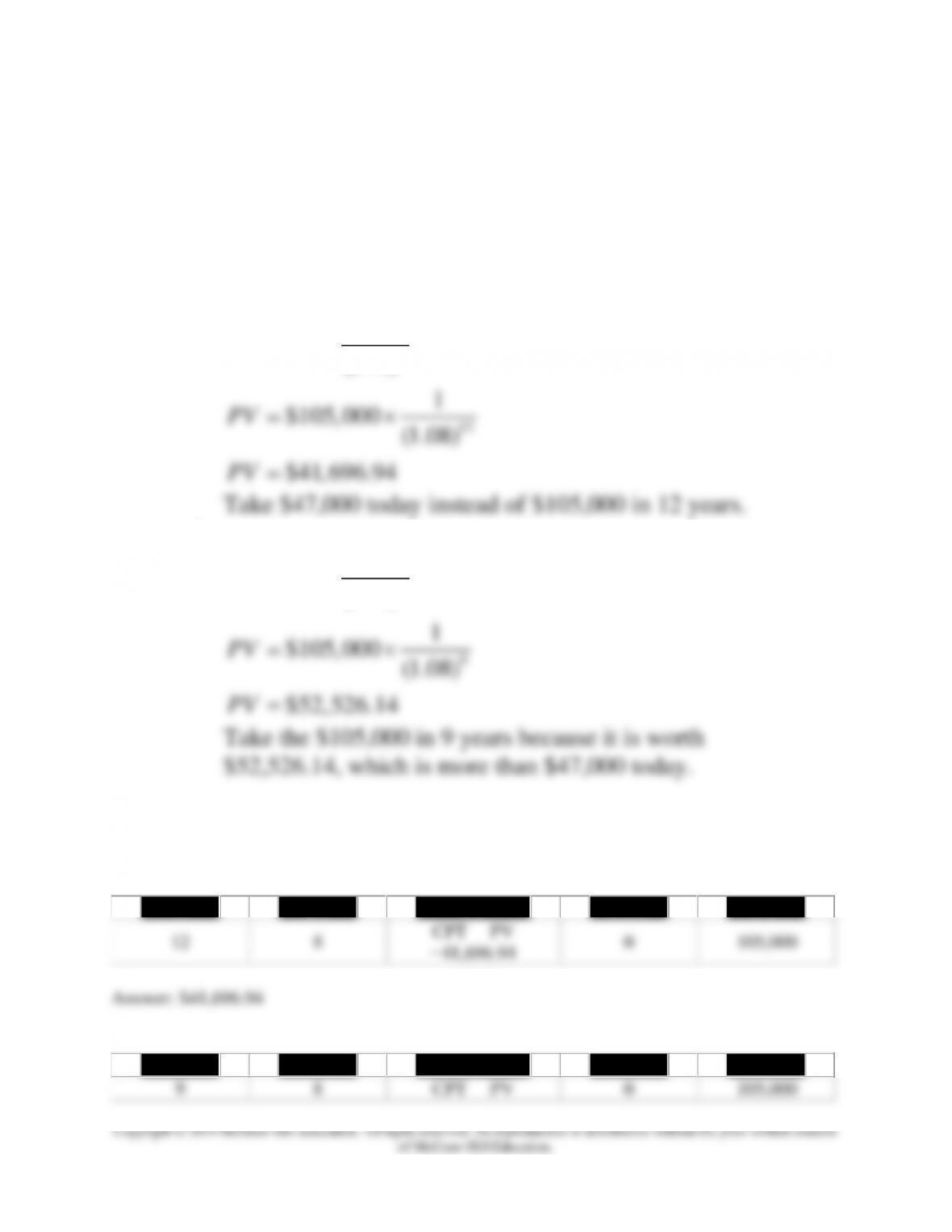

7. Present Value (LO9-3) Your uncle offers you a choice of $105,000 in 10 years or $47,000

today. If money is discounted at 9 percent, which should you choose?

9-7. Solution:

1

(1 )

1

n

PV FV

i

=

+

8. Present Value (LO9-3) Your father offers you a choice of $105,000 in 12 years or $47,000

today.

a. If money is discounted at 8 percent, which should you choose?

b. If money is still discounted at 8 percent, but your choice is between $105,000 in 9

years or $47,000 today, which should you choose?

9-8. Solution:

a.

1

(1 )

1

n

PV FV

i

=

+

−52,526.14

Answer: $52,526.14

a. Appendix B

b. Appendix B

PV = FV × PVIF (8%, 9 periods)

9. Present Value (LO9-3) You are going to receive $205,000 in 18 years. What is the

difference in present value between using a discount rate of 12 percent versus 9 percent?

9-9. Solution:

9% Rate

1

(1 )

1

n

PV FV

i

=

+

The Difference

–26,658.12

Calculator Solution:

At 12%

N

I/Y

PV

PMT

FV

18

12

CPT PV

−26,658.12

0

205,000

Answer: $26,658.12

At 9%

N

I/Y

PV

PMT

FV

18

9

CPT PV −43,458.72

0

205,000

Answer: $43,458.72

The difference is 43,458.72 – 26,658.12 = $16,800.60

Appendix B

$205,000 $205, 000

.130 (12%,18) .212 (9%,18)

$26, 650 $43, 460

The difference is $16,810

$43, 460

26,650

$16,810

−

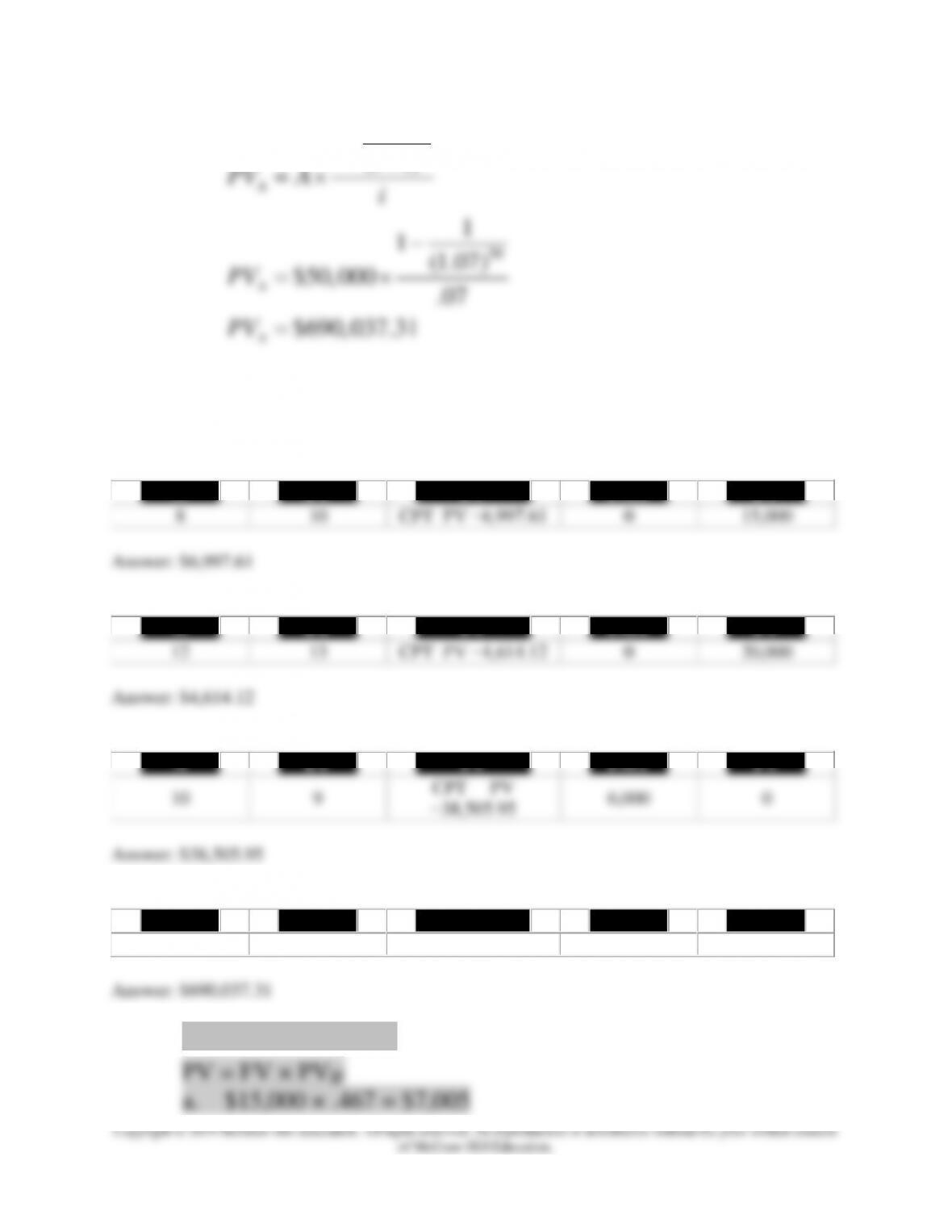

10. How much would you have to invest today to receive

a. $15,000 in 8 years at 10 percent?

b. $20,000 in 12 years at 13 percent?

c. $6,000 each year for 10 years at 9 percent?

d. $50,000 each year for 50 years at 7 percent?

9-10. Solution:

a.

8

1

(1 )

1

$6,997.61

n

PV FV

i

PV

=

+

=

b.

12

1

(1 )

1

$4,614.12

n

PV FV

i

PV

=

+

=

c.

10

1

1(1 )

1

1(1.09)

n

A

i

PV A

i

−+

=

−

50

1

1(1 )

1

1(1.07)

n

A

i

PV A

i

−+

=

−

b. $20,000 × .231 = $4,620

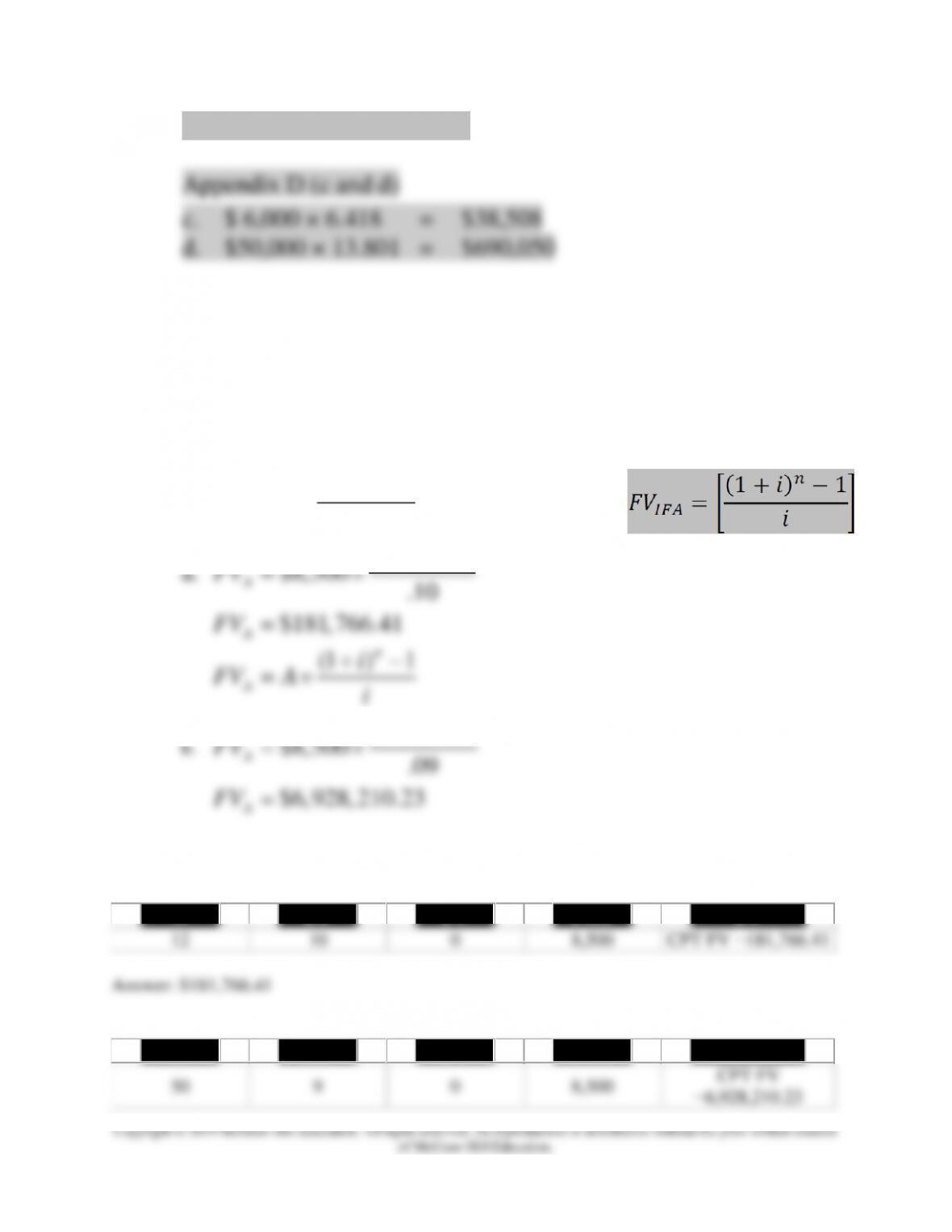

11. Future value (LO9-2) If you invest $8,500 per period for the following number of periods,

how much would you have?

a. 12 years at 10 percent.

b. 50 years at 9 percent.

9-11. Solution:

12

(1 ) 1

(1.10) 1

$181,766.41

n

A

A

A

i

FV A

i

FV

+−

=

−

=

b.

50

(1 ) 1

(1.09) 1

$8,500 .09

$6,928,210.23

n

A

A

A

i

FV A

i

FV

FV

+−

=

−

=

=

Calculator Solution:

(a)

N

I/Y

PV

PMT

FV

12

10

0

8,500

CPT FV −181,766.41

Answer: $181,766.41

(b)

N

I/Y

PV

PMT

FV

50

9

0

8,500

−6,928,210.23

Answer: $6,928,210.23

Appendix C

12. You invest a single amount of $10,000 for 5 years at 10 percent. At the end of 5 years you

take the proceeds and invest them for 12 years at 15 percent. How much will you have

after 17 years?

9-12. Solution:

After 5 Years

5

(1 )

$10,000 (1.10)

$16,105.10

n

FV PV i

FV

FV

= +

=

=

After 17 Years

12

(1 )

$16,10.10 (1.15)

$86,166.31

n

FV PV i

FV

FV

= +

=

=

Calculator Solution:

First step:

N

I/Y

PV

PMT

FV

5

10

10,000

0

CPT FV −16,105.10

Answer: $16,105.10

Second step:

N

I/Y

PV

PMT

FV

12

15

16,105.10

0

CPT FV −86,166.31

Answer: $86,166.31

Appendix A

FV = PV × FVIF

13. Present value (LO9-3) Mrs. Crawford will receive $7,600 a year for the next 19 years

from her trust. If a 14 percent interest rate is applied, what is the current value of the future

payments?

9-13. Solution:

19

1

1(1 )

1

1(1.14)

$7,600 .14

$49,782.80

n

A

A

A

i

PV A

i

PV

PV

−+

=

−

=

=

Calculator Solution:

N

I/Y

PV

PMT

FV

19

14

CPT PV

−49,782.80

7,600

0

Appendix D

14. Phil Goode will receive $175,000 in 50 years. His friends are very jealous of him. If the

funds are discounted back at a rate of 14 percent, what is the present value of his future

“pot of gold”?

9-14. Solution:

50

1

(1 )

1

$175,000 (1.14)

n

PV FV

i

PV

=

+

=