Chapter 03: Financial Analysis

SMITH CORPORATION

Current Assets

Liabilities

Cash ……………………………

$ 35,000

Accounts payable ………………

$ 75,000

Marketable securities ……

7,500

Bonds payable (long-term) ….

210,000

Accounts receivable ……..

70,000

Inventory …………………….

75,000

Long-Term Assets

Stockholders’ Equity

Fixed assets …………………

$500,000

Common stock …………………..

$ 75,000

Less: Accum. dep. ………

(250,000)

Paid-in capital ……………………

30,000

Net fixed assets* ………….

250,000

Retained earnings ………………

47,500

Total assets ……………..

$437,500

Total liab. and equity ………..

$437,500

*Use net fixed assets in computing fixed asset turnover.

SMITH CORPORATION

Sales (on credit)……………………………………………………………………………

$1,000,000

Cost of goods sold ………………………………………………………………………..

600,000

Gross profit …………………………………………………………………………………

400,000

Selling and administrative expense† ……………………………………………..

224,000

Less: Depreciation expense ……………………………………………………….

50,000

Operating profit ……………………………………………………………………………

126,000

Interest expense ……………………………………………………………………………

21,000

Earnings before taxes ……………………………………………………….

105,000

Tax expense …………………………………………………………………………………

52,500

Net income ………………………………………………………………………………….

$ 52,500

†Includes $7,000 in lease payments.

3-37. Solution:

Jones and Smith Comparison

One way of analyzing the situation for each company is to

compare the respective ratios for each. Examining those ratios

which would be most important to a supplier or short-term lender

and a stockholder.

Chapter 03: Financial Analysis

Jones Corp.

Smith Corp.

Profit margin

7.4%

5.25%

Return on assets (investments)

18.5%

12.00%

Return on equity

28.9%

34.4%

Receivable turnover

15.63x

Average collection period

Inventory turnover

Fixed asset turnover

4x

Total asset turnover

Current ratio

Quick ratio

Debt to total assets

65.1%

Times interest earned

24.13x

6x

Fixed charge coverage

13.33x

4.75x

Fixed charge coverage

calculation

(200/15)

(133/28)

3-37. (Continued)

a. Since suppliers and short-term lenders are most concerned with

liquidity ratios, Smith Corporation would get the nod as having

b. Stockholders are most concerned with profitability. In this

category, Jones has much better ratios than Smith. Smith does

have a higher return on equity than Jones, but this is due to its

much larger use of debt. Its return on equity is higher than

Chapter 03: Financial Analysis

SMITH CORPORATION

Sales (on credit) ……………………………………

$1,000,000

Cost of goods sold …………………………………

600,000

Gross profit …………………………………………..

400,000

Selling and administrative expense……….

224,000

50,000

Operating profit …………………………………….

126,000

Interest expense …………………………………….

21,000

Earnings before taxes……………………………..

Tax expense ………………………………………….

52,500

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Lamar Swimwear (trend analysis and industry comparisons)(LO3) Bob Adkins has recently

been approached by his first cousin, Ed Lamar, with a proposal to buy a 15 percent interest in

Lamar Swimwear. The firm manufactures stylish bathing suits and sunscreen products.

Mr. Lamar is quick to point out the increase in sales that has taken place over the last three years

as indicated in the income statement, Exhibit 1. The annual growth rate is 25 percent. A balance

sheet for a similar time period is shown in Exhibit 2, and selected industry ratios are presented in

Exhibit 3. Note the industry growth rate in sales is only 10 to 12 percent per year.

There was a steady real growth of 3 to 4 percent in gross domestic product during the period

under study.

Chapter 03: Financial Analysis

Comprehensive Problem 1 (Continued)

Exhibit 1

LAMAR SWIMWEAR

Income Sheet

20X1

20X2

20X3

Sales (all on credit) ………………………………………

$1,200,000

$1,500,000

$1,875,000

Cost of goods sold ………………………………………..

800,000

1,040,000

1,310,000

Gross profit …………………………………………………

$ 400,000

$ 460,000

$ 565,000

Selling and administrative expense* ……………….

239,900

274,000

304,700

Operating profit (EBIT) ………………………………..

$ 160,100

$ 186,000

$ 260,300

Interest expense ……………………………………………

35,000

45,000

85,000

Net income before taxes ……………………………….

$ 125,100

$ 141,000

$ 175,300

Taxes ………………………………………………………….

36,900

49,200

55,600

Net income ………………………………………………….

$ 88,200

$ 91,800

$ 119,700

Shares …………………………………………………………

30,000

30,000

38,000

Earnings per share ………………………………………..

$ 2.94

$ 3.06

$ 3.15

*Includes $15,000 in lease payments for each year.

Exhibit 2

LAMAR SWIMWEAR

Balance Sheet

Assets

20X1

20X2

20X3

Cash…………………………………………………………..

$ 30,000

$ 40,000

$ 30,000

Marketable securities …………………………………..

20,000

25,000

30,000

Accounts receivable …………………………………….

170,000

259,000

360,000

Inventory ……………………………………………………

230,000

261,000

290,000

Total current assets ………………………………….

$ 450,000

$ 585,000

$ 710,000

Net plant and equipment ………………………………

650,000

765,000

1,390,000

Total assets …………………………………………………

$1,100,000

$1,350,000

$ 2,100,000

Liabilities and Stockholders’ Equity

Accounts payable ………………………………………..

$ 200,000

$ 310,000

$ 505,000

Accrued expenses………………………………………..

20,400

30,000

35,000

Total current liabilities ……………………………..

$ 220,400

$ 340,000

$ 540,000

Long-term liabilities…………………………………….

325,000

363,600

703,900

Total liabilities ………………………………………..

$ 545,400

$ 703,600

$ 1,243,900

Common stock ($2 par) ……………………………….

60,000

60,000

76,000

Capital paid in excess of par …………………………

190,000

190,000

264,000

Retained earnings ………………………………………..

304,600

396,400

516,100

Total stockholders’ equity…………………………

$ 554,600

$ 646,400

$ 856,100

Total liabilities and stockholders’ equity ………..

$1,100,000

$1,350,000

$2, 100,000

Chapter 03: Financial Analysis

Exhibit 3

Selected Industry Ratios

20X1

20X2

20X3

Growth in sales …………………………….

—

10.00%

12.00%

Profit margin ………………………………..

7.71%

7.82%

7.96%

Return on assets (investment) …………

7.94%

8.86%

8.95%

Return on equity ……………………………

14.31%

15.26%

16.01%

Receivable turnover ………………………

9.02x

8.86x

9.31x

Average collection period ………………

39.9 days

40.6 days

38.7 days

Inventory turnover ………………………..

4.24x

5.10x

5.11x

Fixed asset turnover ………………………

1.60x

1.64x

1.75x

Total asset turnover ……………………….

1.05x

1.10x

1.12x

Current ratio …………………………………

1.96x

2.25x

2.40x

Quick ratio …………………………………..

1.37x

1.41x

1.38x

Debt to total assets ………………………..

43.47%

43.11%

44.10%

Times interest earned …………………….

6.50x

5.99x

6.61x

Fixed charge coverage …………………..

4.70x

4.69x

4.73x

Growth in EPS ……………………………..

—

10.10%

13.30%

The stock in the corporation has become available due to the ill health of a current stockholder,

who is in need of cash. The issue here is not to determine the exact price for the stock, but rather

whether Lamar Swimwear represents an attractive investment situation. Although Mr. Adkins

has a primary interest in the profitability ratios, he will take a close look at all the ratios. He has

no fast and firm rules about required return on investment, but rather wishes to analyze the

overall condition of the firm. The firm does not currently pay a cash dividend, and return to the

investor must come from selling the stock in the future. After doing a thorough analysis

(including ratios for each year and comparisons to the industry), what comments and

recommendations do you offer to Mr. Adkins?

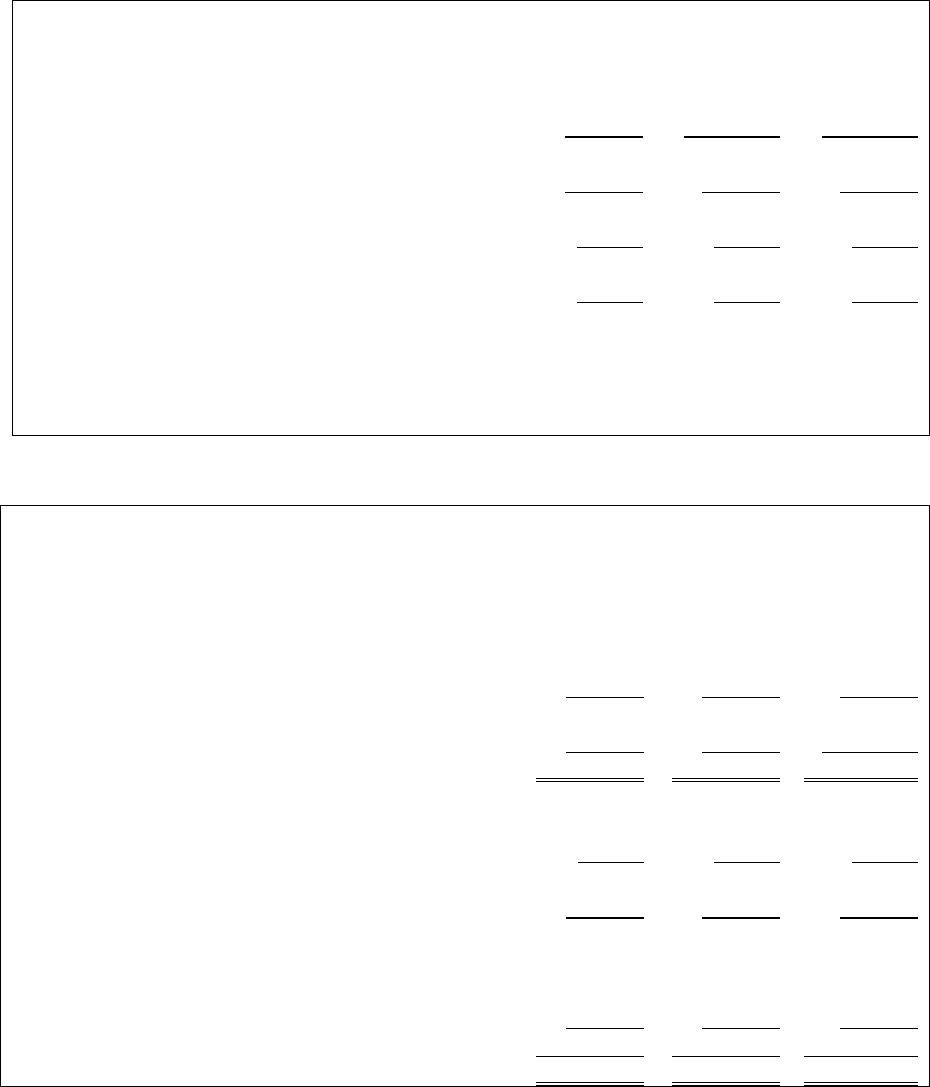

CP 3-1. Solution:

Lamar Swimwear

20X1

20X2

20X3

Growth in sales

(Company)

25%

25%

(Industry)

10%

12%

Profit margin

(Company)

7.35%

6.12%

6.38%

(Industry)

7.71%

7.96%

Return on assets

(Company)

8.02%

6.80%

5.70%

(Industry)

7.94%

8.68%

8.95%

Return on equity

(Company)

15.90%

14.20%

13.98%

(Industry)

14.31%

15.26%

16.01%

Receivable turnover

(Company)

7.06x

5.79x

5.21x

(Industry)

9.02x

8.86x

9.31x

Average collection

(Company)

62.2 days

69.1 days

(Industry)

39.9 days

40.6 days

38.7 days

Inventory turnover

(Company)

5.22x

5.75x

6.47x

(Industry)

4.24x

5.10x

5.11x

Fixed asset turnover

(Company)

1.85x

1.96x

1.35x

(Industry)

1.60x

1.64

1.75x

Total asset turnover

(Company)

1.09x

1.11x

0.89x

(Industry)

1.05x

1.10x

1.12x

Current ratio

(Company)

2.04x

1.72x

1.31x

(Industry)

1.96x

2.25x

2.40x

Quick ratio

(Company)

1.00x

0.78x

(Industry)

1.37x

1.41x

1.38x

(Company)

49.58%

52.12%

59.23%

Times interest

(Company)

4.57x

4.13x

3.06x

(Industry)

Fixed charge

(Company)

3.50x

3.35x

2.75x

(Industry)

(Company)

—-

4.1%

2.9%

CP 3-1. (Continued)

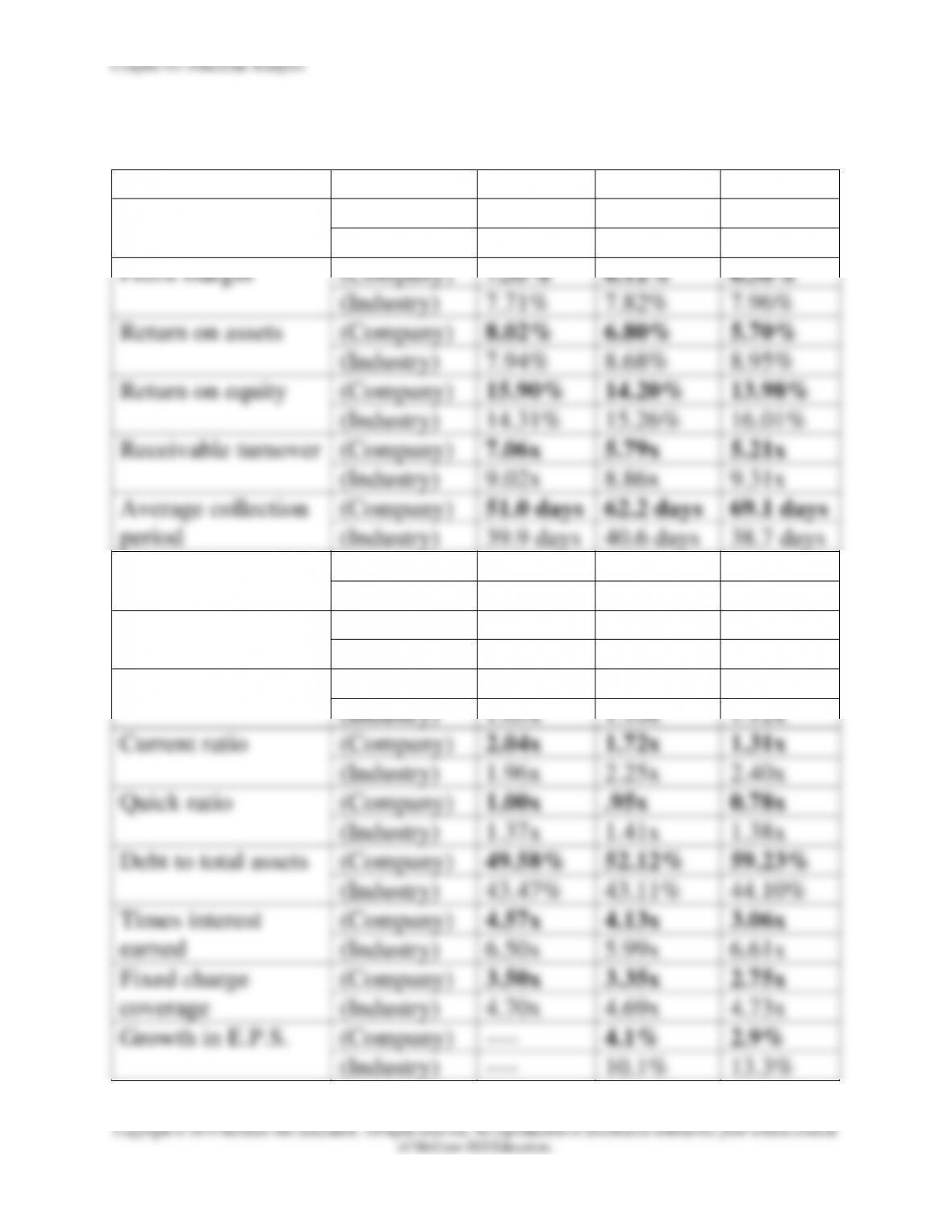

Discussion of Ratios

While Lamar Swimwear is expanding its sales much more rapidly than

others in the industry, there are some clear deficiencies in their

performance. These can be seen in terms of a trend analysis over time as

well as a comparative analysis with industry data.

The previously mentioned slower turnover of assets can be analyzed

through the turnover ratios. A problem can be found in accounts

Chapter 03: Financial Analysis

CP 3-1. (Continued)

The liquidity ratios also are not encouraging. Both the current and quick

ratios are falling against a stable industry norm of approximately two to

one and one to one, respectively.

Investment Comments:

He would probably have difficulty justifying such an investment based

on the performance of the firm. There are no dividend payouts, so return

Comprehensive Problem 2

Sun Microsystems (trends, ratios stock performance) (LO3) Sun Microsystems is a leading

supplier of computer-related products, including servers, workstations, storage devices, and

network switches.

In the letter to stockholders as part of the 2001 annual report, President and CEO Scott G.

McNealy offered the following remarks:

Fiscal 2001 was clearly a mixed bag for Sun, the industry, and the economy as a whole. Still,

we finished with revenue growth of 16 percent—and that’s significant. We believe it’s a good

indication that Sun continued to pull away from the pack and gain market share. For that, we

owe a debt of gratitude to our employees worldwide, who aggressively brought costs down—

even as they continued to bring exciting new products to market.

The statement would not appear to be telling you enough. For example, McNealy says the

year was a mixed bag with revenue growth of 16 percent. But what about earnings? You can

delve further by examining the income statement in Exhibit 1. Also, for additional analysis of

other factors, consolidated balance sheet(s) are presented in Exhibit 2 on page 92.

1. Referring to Exhibit 1, compute the annual percentage change in net income per common

share-diluted (second numerical line from the bottom) for 1998–1999, 1999–2000, and

2000–2001.

2. Also in Exhibit 1, compute net income/net revenue (sales) for each of the four years.

Begin with 1998.

3. What is the major reason for the change in the answer for Question 2 between 2000 and

2001? To answer this question for each of the two years, take the ratio of the major

income statement accounts to net revenues (sales).

Cost of sales

Research and development

Selling, general and administrative expense

Provision for income tax

4. Compute return on stockholders’ equity for 2000 and 2001 using data from Exhibits 1

and 2.

In 2009, Sun Microsystems was acquired by Oracle Corporation.

Chapter 03: Financial Analysis

Comprehensive Problem 2 (Continued)

Exhibit 1

SUN MICROSYSTEMS INC.

Summary Consolidated Statement of Income (in millions)

2001

2000

1999

1998

Dollars

Dollars

Dollars

Dollars

Net revenues ………………………………………..

$18,250

$15,721

$11,806

$9,862

Costs and expenses:

Cost of sales …………………………………..

10,041

7,549

5,670

4,713

Research and development ………………

2,016

1,630

1,280

1,029

Selling, general and administrative ……

4,544

4,072

3,196

2,826

Goodwill amortization …………………….

261

65

19

.4

In-process research and development ..

77

12

121

176

Total costs and expenses ………………………..

16,939

13,328

10,286

8,748

Operating Income …………………………………

1,311

2,393

1,520

1,114

Gain (loss) on strategic investments ………..

(90)

208

–

–

Interest income, net ……………………………….

363

170

85

48

Litigation settlement ……………………………..

–

–

–

–

Income before taxes ………………………………

1,584

2,771

1,605

1,162

Provision for income taxes …………………….

603

917

575

407

Cumulative effect of change

in accounting principle, net …………………

(54)

–

–

–

Net income …………………………………………..

$ 927

$ 1,854

$ 1,030

$ 755

Net income per common share—diluted ….

$ 0.27

$ 0.55

$ 0.31

$ 0.24

Shares used in the calculation of net

income per common share—diluted ………..

3,417

3,379

3,282

3,180

5. Analyze your results to Question 4 more completely by computing ratios 1, 2a, 2b, and 3b

(all from this chapter) for 2000 and 2001. Actually, the answer to ratio 1 can be found as part

of the answer to question 2, but it is helpful to look at it again.

What do you think was the main contributing factor to the change in return on stockholders’

equity between 2000 and 2001? Think in terms of the Du Pont system of analysis.

6. The average stock prices for each of the four years shown in Exhibit 1 were as follows:

1998 11¼

1999 16¾

2000 28½

2001 9½

a. Compute the price/earnings (P/E) ratio for each year. That is, take the stock price shown

above and divide by net income per common stock-dilution from Exhibit 1.

b. Why do you think the P/E has changed from its 2000 level to its 2001 level?

A brief review of P/E ratios can be found under the topic of Price-Earnings Ratio

Applied to Earnings per Share in Chapter 2.

Chapter 03: Financial Analysis

Comprehensive Problem 2 (Continued)

Exhibit 2

SUN MICROSYSTEMS, INC

Consolidated Balance Sheets (in millions)

Assets

2001

2000

Current assets:

Cash and cash equivalents ……………………………………………………………

$ 1,472

$ 1,849

Short-term investments ………………………………………………………………..

387

626

Accounts receivable, net allowances of $410 in 2001 and

$534 in 2000 ……………………………………………………………………………

2,955

2,690

Inventories………………………………………………………………………………….

1,049

557

Deferred tax assets ………………………………………………………………………

1,102

673

Prepaids and other current assets …………………………………………………..

969

482

Total current assets …………………………………………………………………..

$7,934

$6,877

Property, plant and equipment, net ……………………………………………………

2,697

2,095

Long-term investments ……………………………………………………………………

4,677

4,496

Goodwill, net of accumulated amortization of $349 in 2001 and

$88 in 2000 ………………………………………………………………………………..

2,041

163

Other assets, net ……………………………………………………………………………..

832

521

$18,181

$14,152

Liabilities and Stockholders’ Equity

Current liabilities:

Short-term borrowings …………………………………………………………………

$ 3

$ 7

Accounts payable ………………………………………………………………………..

1,050

924

Accrued payroll-related liabilities ………………………………………………….

488

751

Accrued liabilities and other …………………………………………………………

1,374

1,155

Deferred revenues and customer deposits ……………………………………….

1,827

1,289

Warranty reserve …………………………………………………………………………

314

211

Income taxes payable …………………………………………………………………..

90

209

Total current liabilities ………………………………………………………………

$5,146

$4,546

Deferred income taxes …………………………………………………………………….

744

577

Long-term debt and other obligations………………………………………………..

1,705

1,720

Total debt ………………………………………………………………………………..

$ 7,595

$ 6,843

Commitments and contingencies

Stockholders’ equity:

Preferred stock, $0.001 par value, 10 shares authorized (1 share which

has been designated as Series A Preferred participating stock): no

shares issued and outstanding …………………………………………………….

–

–

Common stock and additional paid-in–capital, $0.00067 par value, 7,200

shares authorized; issued: 3,536 shares in 2001 and 3,495 shares in 2000 …

6,238

2,728

Treasury stock, at cost: 288 shares in 2001 and 301 shares in 2000 ………

(2,435)

(1,438)

Deferred equity compensation ………………………………………………………….

(73)

(15)

Retained earnings……………………………………………………………………………

6,885

5,959

Accumulated other comprehensive income (loss) ……………………………….

(29)

75

Total stockholders’ equity ……………………………………………………………..

$10,586

$7,309

Chapter 03: Financial Analysis

$18,181

$14,152

7. The book values per share for the same four years discussed in the preceding question were:

1998 $1.18

1999 $1.55

2000 $2.29

2001 $3.26

a. Compute the ratio of price to book value for each year.

b. Is there any dramatic shift in the ratios worthy of note?

CP 3-2. Solution

Sun Microsystems

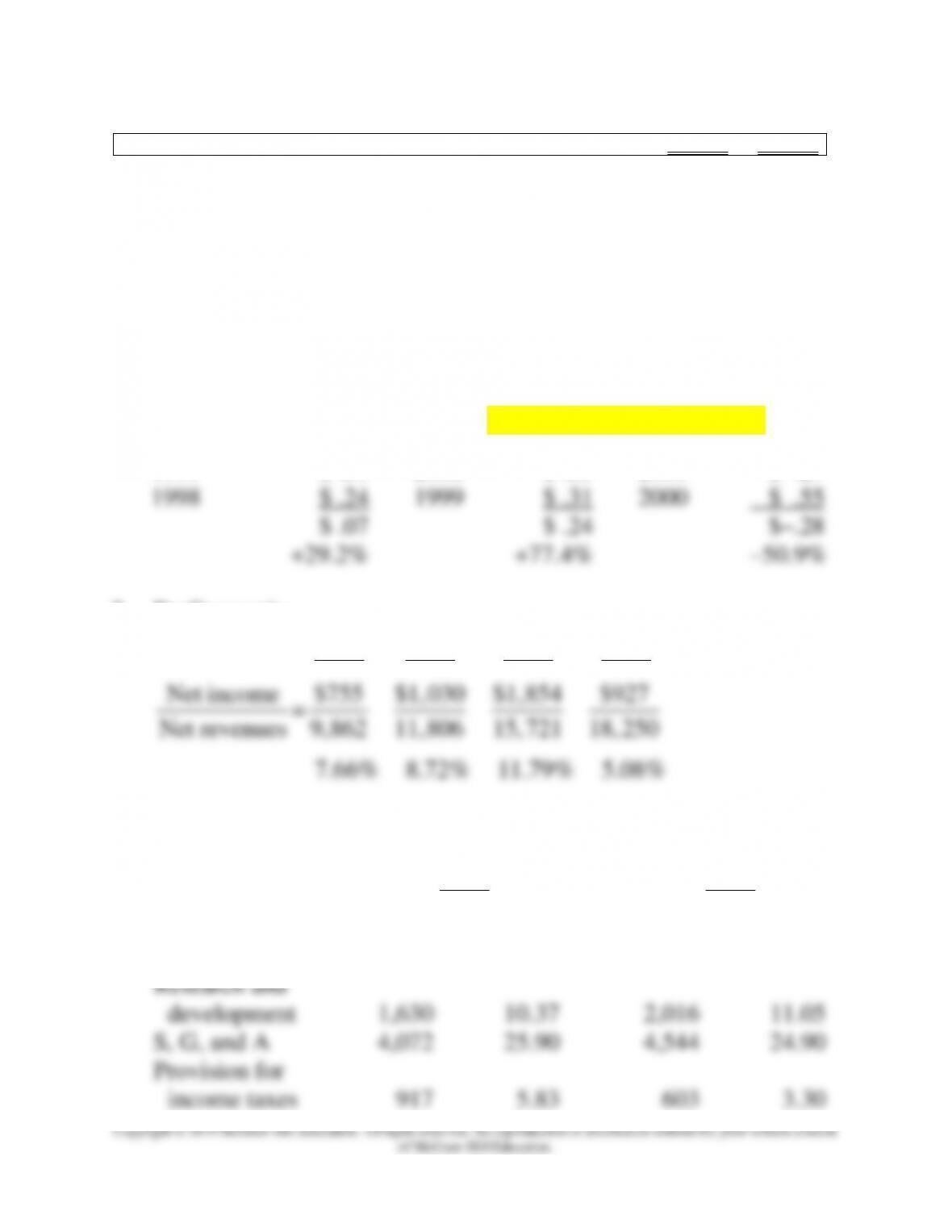

1. Percentage change in net income per common share—diluted

1999

$ .31

2000

$ .55

2001

$ .27

$ .07

$ .24

$–.28

2. Profit margin

1998 1999 2000 2001

3. Percent of net revenue

2000 2001

Net revenues $15,721 $18,250

Cost of sales 7,549 48.02% 10,041 55.02%

Chapter 03: Financial Analysis

CP 3-2. (Continued)

4. Return on stockholders’ equity

2000 2001

5.

2000 2001

1.

Net income

Net revenues (sales)

11.79% 5.08%

13.09% 5.08%

3.b.

( ) ( ) ( )

Return on assets 13.09% 5.08%

1 Debt/Assets 1 .484 1 .418

− − −

Chapter 03: Financial Analysis

CP 3-2. (Continued)

6.a. P/E = Stock price/Net income per common share—diluted (EPS)

P/E 46.9 54.0 51.8 35.2

7.a. Price to book value = Stock price/book value

1998 1999 2000 2001

b. Once again, the sharp falloff in price to book value between 2000