Chapter 19: Convertibles, Warrants, and Derivatives

Chapter 19

Convertibles, Warrants, and Derivatives

Discussion Questions

19-1.

What are the basic advantages to the corporation of issuing convertible

securities?

The advantages to the corporation of a convertible security are:

a. The interest rate is lower than on a straight issue.

b. This type of security may be the only device for allowing a small firm access

to the capital markets.

c. The convertible allows the firm to effectively sell stock at a higher price than

that possible when the bond was initially issued (but perhaps at a lower price

than future price potential might provide).

d. If the bond can be called at a price above its conversion price, the bond will

be converted to stock and the debt-to-asset ratio will decline.

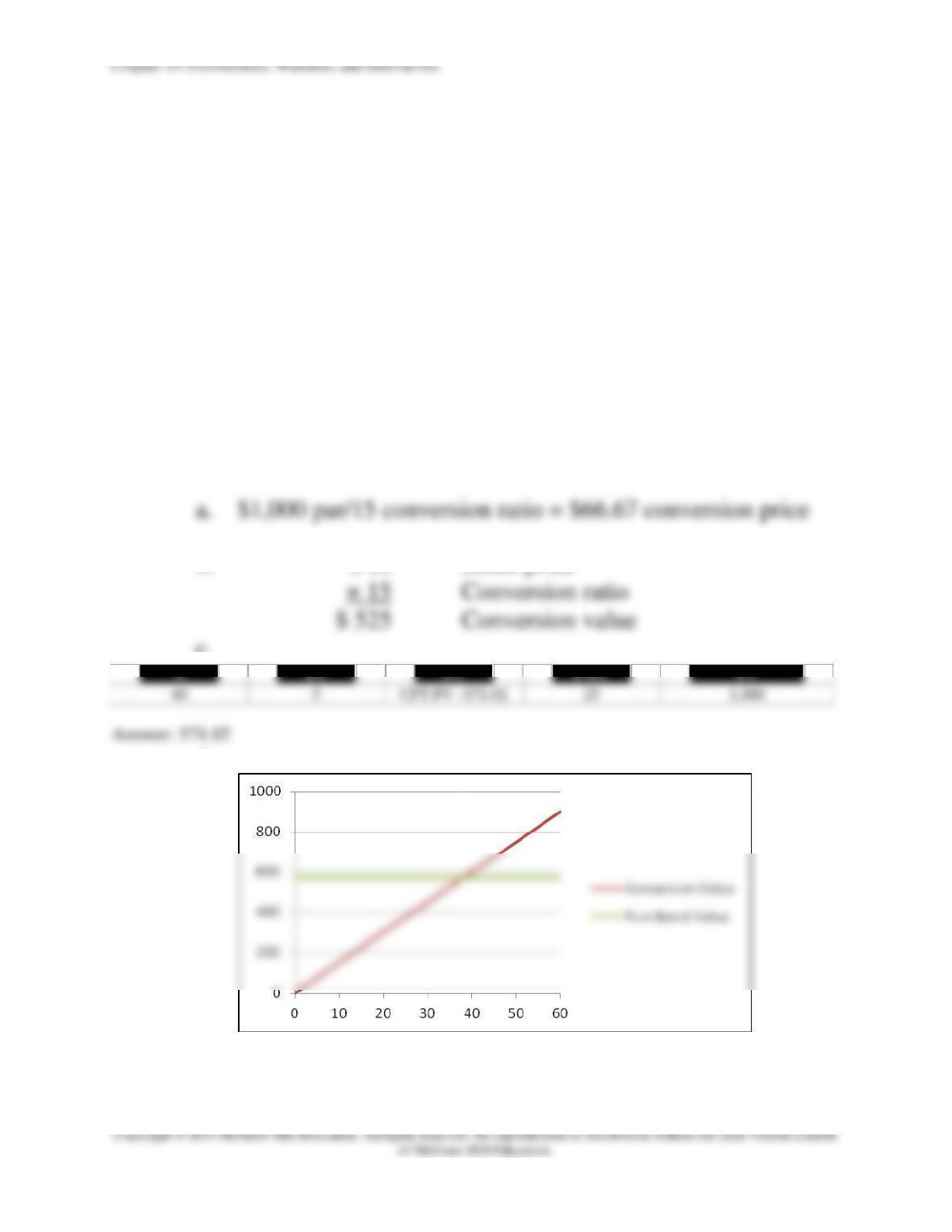

19-2.

Why are investors willing to pay a premium over the theoretical value (pure bond

value or conversion value)?

Investors are willing to pay a premium over the theoretical value for a convertible

bond issue because of the future prospects for the associated common stock.

Thus, if there are many years remaining for the conversion privilege, the investor

will be able to receive a reasonably high interest rate and still have the option of

converting the convertible bond to common stock if circumstances justify.

19-3.

Why is it said that convertible securities have a floor price?

The floor price of a convertible is based on the pure bond value associated with

the interest payments on the bond as shown in Figure 19-1. Regardless of how

low the associated common stock might go, the semiannual interest payments

will set a floor price for the bond.

Chapter 19: Convertibles, Warrants, and Derivatives

15. Convertible bond and rates of return (LO19-2) Vernon Glass Company has $15 million

in 10 percent convertible bonds outstanding. The conversion ratio is 40, the stock price is

$17, and the bond matures in 10 years. The bonds are currently selling at a conversion

premium of $45 over their conversion value.

If the price of the common stock rises to $23 on this date next year, what would your

rate of return be if you bought a convertible bond today and sold it in one year? Assume on

this date next year, the conversion premium has shrunk from $45 to $20.

19–15. Solution:

Vernon Glass Company

First, find the price of the convertible bond. The conversion

value is $680 ($17 × 40). The conversion value of $680,