Chapter 16: Long-Term Debt and Lease Financing

a) Operating lease

i. $48,055

ii. $48,055

iii. ($10,000 + $15,000 + $20,000 +$25,000) /4 =

$17,500

iv. $0 Interest not applicable to operating leases.

v. $0 amortization not applicable to operating leases.

b) Finance lease

i. $48,055

ii. $48,055

iii. $0 lease expense not applicable to finance leases.

iv. ($48,055 x .07) = $3364

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Broadband Inc. Bond prices refunding (LO16-2 and 3) Barton Simpson, the chief financial

officer of Broadband Inc. could hardly believe the change in interest rates that had taken place

over the last few months. The interest rate on A2 rated bonds was now 6 percent. The $30

Chapter 16: Long-Term Debt and Lease Financing

percent and a 4 percent discount rate will be applied for the refunding decision. The new bond

would have a 10-year life.

Before Barton used the 8 percent call provision to reacquire the old bonds, he wanted to make

sure he could not buy them back cheaper in the open market.

a. First compute the price of the old bonds in the open market. Use the valuation procedures for

a bond that were discussed in Chapter 10 (use the annual analysis). Determine the price of a

single $1,000 par value bond.

b. Compare the price in part a to the 8 percent call premium over par value. Which appears to

be more attractive in terms of reacquiring the old bonds?

c. Now do the standard bond refunding analysis as discussed in this chapter. Is the refunding

financially feasible?

d In terms of the refunding decision, how should Barton be influenced if he thinks interest rates

might go down even more?

Chapter 16: Long-Term Debt and Lease Financing

Chapter 16: Long-Term Debt and Lease Financing

Appendix

16A–1. Settlement of claims in bankruptcy liquidation (LO16-5) The trustee in the

bankruptcy settlement for Titanic Boat Co. lists the following book values and

liquidation values for the assets of the corporation. Liabilities and stockholders’ claims

are shown.

Liquidation

Assets Book Value Value

Accounts receivable …………………… $1,400,000 $1,200,000

Inventory …………………………………………..

1,800,000

900,000

Machinery and equipment …………………..

1,100,000

600,000

Building and plant …………………………..

4,200,000

2,500,000

Total assets

$8,500,000

$ 5,200,000

Liabilities and Stockholders’ Claims

Liabilities:

Accounts payable …………………………..

$2,800,000

First lien, secured by

machinery and equipment ……………..

900,000

Senior unsecured debt ………………………

2,200,000

Subordinated debenture ……………………

1,700,000

Total liabilities …………………………..

7,600,000

Stockholders’ claims:

Preferred stock …………………………..

250,000

Common stock …………………………..

650,000

Total stockholders’ claims …………….

900,000

Total liabilities and

stockholders’ claims ……………… $8,500,000

a. Compute the difference between the liquidation value of the assets and the liabilities.

b. Based on the answer to part a, will preferred stock or common stock participate in

the distribution?

c. Assuming the administrative costs of bankruptcy, workers’ allowable wages, and

unpaid taxes add up to $400,000, what is the total remaining asset value available to

cover secured and unsecured claims?

d. After the machinery and equipment are sold to partially cover the first lien secured

claim, how much will be available from the remaining asset liquidation values to

cover unsatisfied secured claims and unsecured debt?

Chapter 16: Long-Term Debt and Lease Financing

e. List the remaining asset claims of unsatisfied secured debt holders and unsecured

debt holders in a manner similar to that shown in the bottom portion of Table 16A-3.

f. Compute a ratio of your answers in part d and e. This will indicate the initial

allocation ratio.

g. List the remaining claims (unsatisfied secured and unsecured) and make an initial

allocation and final allocation similar to that shown in Table 16A-4. Subordinated

debenture holders may keep the balance after full payment is made to senior debt

holders.

h. Show the relationship of amount received to total amount of claim in a similar

fashion to that in Table 16A-5. Remember to use the sales (liquidation) value for

machinery and equipment plus the allocation amount in part g to arrive at the total

received on secured debt.

16A–1. Solution:

Titanic Boat Co.

a. Liquidation value of assets $5,200,000

Liabilities 7,600,000

Difference ($2,400,000)

b. Preferred and common stock will not participate in the

Chapter 16: Long-Term Debt and Lease Financing

unsecured debt holder

Secured debt (unsatisfied first lien) $ 300,000

Accounts payable 2,800,000

Senior unsecured debt 2,200,000

Subordinated debentures 1,700,000

$7,000,000

f. Amount available to unsatisfied

$4,200,000

security claims and unsecured debt (part d) 60%

Remaining claims of unsatisfied secured $7,000,000

debt and unsecured debt holders (part e)

==

Chapter 16: Long-Term Debt and Lease Financing

CP16A-1. (Continued)

g.

Allocation procedures for unsatisfied secured claims and

unsecured debt.

(1)

Category

(2)

Amount of

Claim

(3)

Initial

Allocation

(60%)

(4)

Amount

Received

Secured ebt

(unsatisfied first lien)

$ 300,000

$ 180,000

$ 180,000

Accounts Payable

2,800,000

1,680,000

1,680,000

Senior unsecured debt

2,200,000

1,320,000

2,200,000

Subordinated

debentures*

1,700,000

1,020,000

140,000*

$ 7,000,000

$4,200,000

$4,200,000

* The subordinated debenture holders must transfer $880,000

of their initial allocation to the senior unsecured debt holders

to fully provide for their payment ($1,320,000 + $880,000 =

$2,200,000). This will leave $140,000 for subordinated

debentures ($1,020,000 – $880,000).

Chapter 16: Long-Term Debt and Lease Financing

CP16A-1. (Continued)

h.

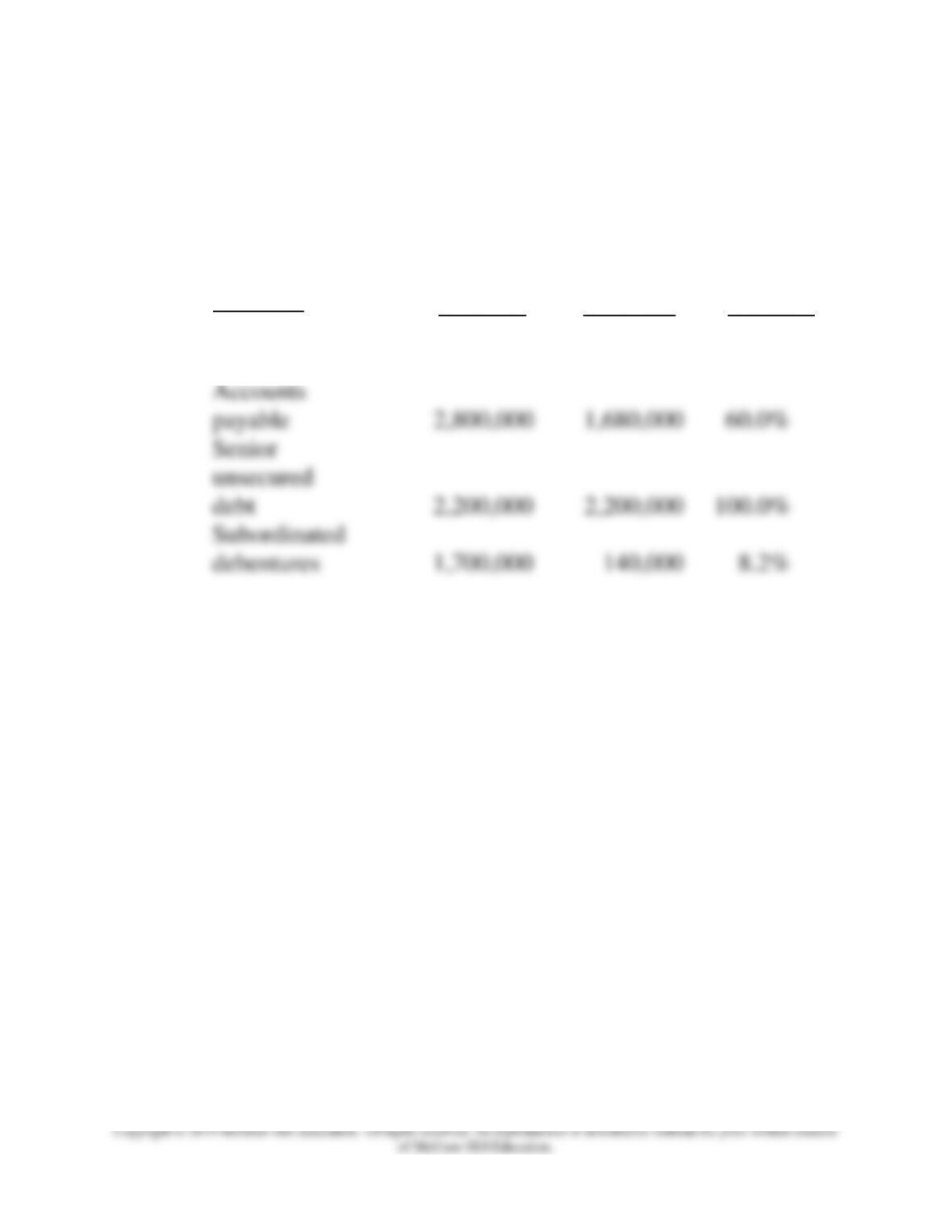

Payments and percent of claims

Category

Total Amount

of Claim

Amount

Received

Percent of

Claim

Satisfied

Secured debt

(first lien)

$ 900,000

$ 780,000

86.7%

Accounts

payable

2,800,000

1,680,000

60.0%

Senior

unsecured

debt

2,200,000

2,200,000

100.0%

Subordinated

debentures

1,700,000

140,000

8.2%

16B-1. Lease versus purchase decision (LO16-4) Howell Auto Parts is considering whether

to borrow funds and purchase an asset or to lease the asset under an operating lease

arrangement. If the company purchases the asset, the cost will be $10,000. It can borrow

funds for four years at 12 percent interest. The firm will use the three-year MACRS

depreciation category (with the associated four-year write-off). Assume a tax rate of

35 percent.

The other alternative is to sign two operating leases, one with payments of $2,600 for

the first two years, and the other with payments of $4,600 for the last two years. In your

analysis, round all values to the nearest dollar.

a. Compute the aftertax cost of the leases for the four years.

b. Compute the annual payment for the loan (round to the nearest dollar).

c. Compute the amortization schedule for the loan. (Disregard a small difference

from a zero balance at the end of the loan due to rounding.)

d. Determine the depreciation schedule (see Table 12-9).

e. Compute the aftertax cost of the borrow-purchase alternative.

f. Compute the present value of the aftertax cost of the two alternatives. Use a

discount rate of 8 percent.

g. Which alternative should be selected, based on minimizing the present value of

aftertax costs?

Chapter 16: Long-Term Debt and Lease Financing

d. Depreciation Depreciation

Year

Base

Percentage

Depreciation

1

$10,000

.333

$ 3,330

2

10,000

.445

4,450

3

10,000

.148

1,480

4

10,000

.074

740

$10,000

e.

(1)

(2)

(3)

(4)

(5)

(6)

Year

Payment

Interest

Depreciation

Total Tax

Deductions

Tax

Shield

35% × (4)

Net

Aftertax

Cost (1)

– (5)

1

$3,293

$1,200

$3,330

$4,530

$1,586

$1,707

2

3,293

949

4,450

5,399

1,890

1,403

3

3,293

668

1,480

2,148

752

2,541

4

3,293

353

740

1,093

383

2,910

CP16B-1. (Continued)

f.

Year

Aftertax

Cost of

Leasing

PV

Factor

at 8%

Present

Value

Aftertax

Cost of

Borrow-

Purchase

PV

Factor

at 8%

Present

Value

1

$1,690

.926

$1,565

$1,707

.926

$1,581

2

1,690

.857

1,448

1,403

.857

1,202

3

2,990

.794

2,374

2,541

.794

2,018

4

2,990

.735

2,198

2,910

.735

2,139

$7,585

$6,940

Chapter 16: Long-Term Debt and Lease Financing