Chapter 13: Risk and Capital Budgeting

Calculator solution:

b.

Find the PV of cash inflow using a financial calculator at 15 percent:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, enter 27,900 and press +|–, press the Enter key.

17. Deferred cash flows and risk-adjusted discount rate Highland Mining and Minerals Co.

is considering the purchase of two gold mines. Only one investment will be made. The

Australian gold mine will cost $1,649,000 and will produce $353,000 per year in years 5

through 15 and $503,000 per year in years 16 through 25. The U.S. gold mine will cost

$2,054,000 and will produce $282,000 per year for the next 25 years. The cost of capital is

13 percent.

a. Which investment should be made? (Note: In looking up present value factors for this

problem, you need to work with the concept of a deferred annuity for the Australian

mine. The returns in years 5 through 15 actually represent 11 years; the returns in

years 16 through 25 represent 10 years.)

b. If the Australian mine justifies an extra 2 percent premium over the normal cost of

capital because of its riskiness and relative uncertainty of cash flows, does the

investment decision change?

13-17. Solution:

Highland Mining and Minerals Co.

a. Calculate the net present value for each project.

The Australian Mine

Chapter 13: Risk and Capital Budgeting

Years

Cash

Flow

n Factor

PVIFA@13%

Present

Value

5–15

$353,000

(15 – 4)

(6.462 – 2.974)

$1,231,264

16–25

$503,000

(25 – 15)

(7.330 – 6.462)

$ 436,604

The U.S. Mine

Years

Cash Flow

n Factor

PVIFA@13%

Present

Value

1–25

$282,000

(25)

7.330

$2,067,060

b. Recalculate the net present value of the Australian Mine at a

15 percent discount rate.

Years

Cash Flow

n Factor

PVIFA @ 15%

Present

Value

5–15

$353,000

(15 – 4)

(5.847 – 2.855)

$ 1,056,176

16–25

$503,000

(25 – 15)

(6.464 – 5.847)

$ 310,351

Present Value of Inflows $1,366,527

Present Value of Outflows $1,649,000

Chapter 13: Risk and Capital Budgeting

18. Coefficient of variation and investment decision (LO13-1) Mr. Sam Golff desires to

invest a portion of his assets in rental property. He has narrowed his choices down to two

apartment complexes, Palmer Heights and Crenshaw Village. After conferring with the present

owners, Mr. Golff has developed the following estimates of the cash flows for these properties:

Palmer Heights

Crenshaw Village

Yearly Aftertax

Cash Inflow

(in thousands)

Probability

Yearly Aftertax

Cash Inflow

(in thousands)

Probability

$70 ……………..

.2

$75 …………….

.2

75 ……………..

.2

80 …………….

.3

90 ……………..

.2

90 …………….

.4

105 ……………

.2

100 …………..

.1

110 ……………

.2

a. Find the expected cash flow from each apartment complex.

b. What is the coefficient of variation for each apartment complex?

c. Which apartment complex has more risk?

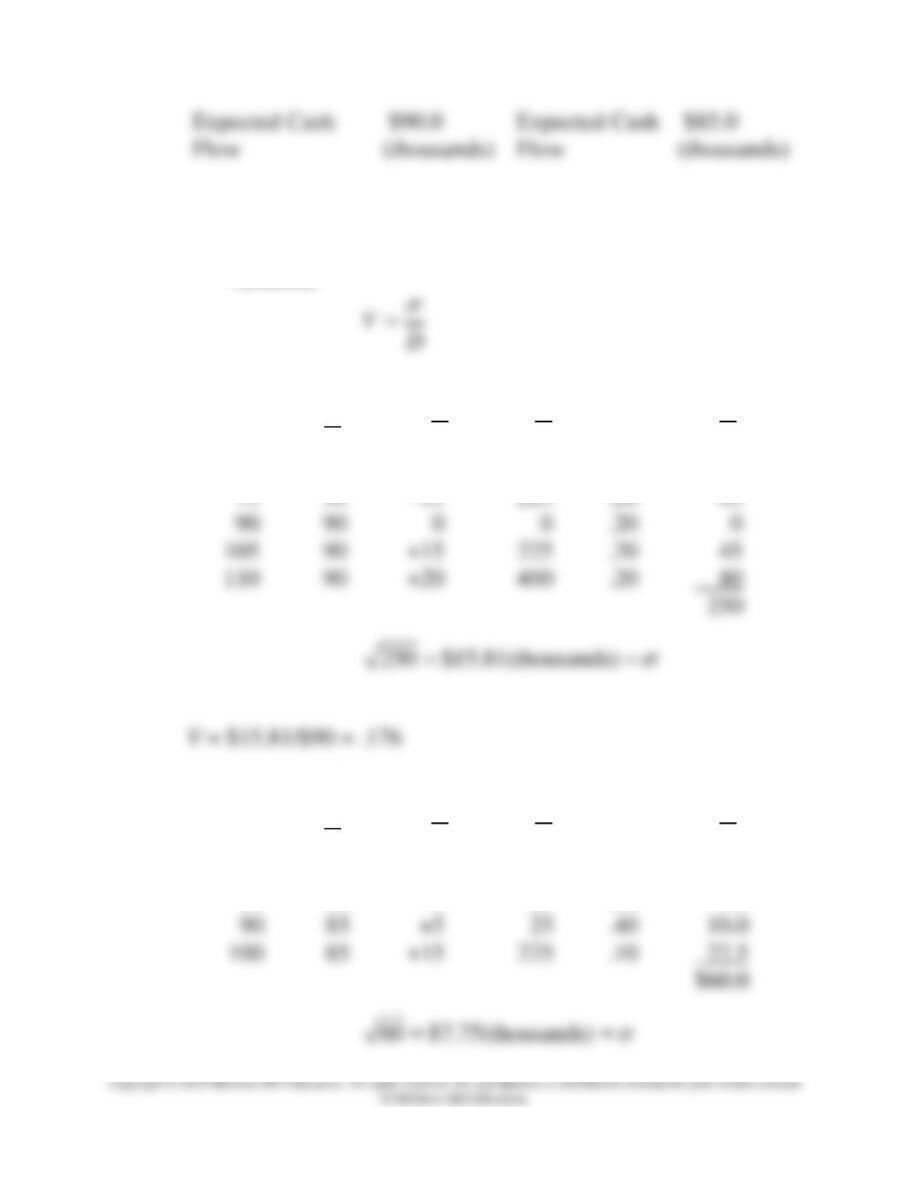

13-18. Solution:

Mr. Sam Golff

D DP=

Palmer Heights

Crenshaw Village

D

P

DP

D

P

DP

70

.2

$14.0

75

.2

$ 15.0

75

.2

15.0

80

.3

24.0

90

.2

18.0

90

.4

36.0

105

.2

21.0

100

.1

10.0

110

.2

22.0

Chapter 13: Risk and Capital Budgeting

Expected Cash

Flow

$90.0

(thousands)

Expected Cash

Flow

$85.0

(thousands)

a. First find the standard deviation and then the coefficient of

variation.

V

D

=

Palmer Heights

D

D

()DD−

2

()DD−

P

2

()DD−

P

$70

$90

$–20

$400

.20

80

75

90

–15

225

.20

45

90

90

0

0

.20

0

105

90

+15

225

.20

45

110

90

+20

400

.20

80

250

250 $15.81 (thousands)

==

V = $15.81/$90 = .176

Crenshaw Village

D

D

()DD−

2

()DD−

P

2

()DD−

P

$75

$85

$–10

$100

.20

20.0

80

85

–5

25

.30

7.5

90

85

+5

25

.40

10.0

100

85

+15

225

.10

22.5

$60.0

60 $7.75 (thousands)

==

Chapter 13: Risk and Capital Budgeting

19. Decision-tree analysis (LO13-4) Allison’s Dresswear Manufacturers is preparing a

strategy for the fall season. One alternative is to expand its traditional ensemble of wool

sweaters. A second option would be to enter the cashmere sweater market with a new line

of high-quality designer label products. The marketing department has determined that the

wool and cashmere sweater lines offer the following probability of outcomes and related

cash flows:

Expand Wool

Sweaters Line

Enter Cashmere

Sweaters Line

Expected

Sales

Probability

Present Value

of Cash Flows

from Sales

Probability

Present

Value of

Cash Flows

from Sales

Fantastic ………………..

.5

$221,000

.3

$341,000

Moderate ……………….

.2

192,000

.4

272,000

Low ………………………

.3

88,600

.3

0

The initial cost to expand the wool sweater line is $142,000. To enter the cashmere sweater

line, the initial cost in designs, inventory, and equipment is $102,000.

a. Diagram a complete decision tree of possible outcomes similar to Figure 13-8. Note

that you are dealing with thousands of dollars rather than millions. Take the analysis

all the way through the process of computing expected NPV (the last column for each

investment).

b. Given the analysis in part a, would you automatically make the investment indicated?

13–26

13–19. Solution:

Allison’s Dresswear Manufacturers

a.

(1)

(2)

(3)

(4)

(5)

(6)

Expected

Sales

Probability

Present Value

of Cash Flows

from Sales

Initial Cost

NPV

(3) – (4)

Expected

NPV

(2) × (5)

Expand

Fantastic

.5

$221,000

$142,000

$79,000

$39,500

Wool

Moderate

.2

192,000

142,000

50,000

10,000

Sweaters

Low

.3

88,600

142,000

(53,400)

(16,020)

Expected

NPV

$33,480

Enter

Fantastic

.3

$341,000

$102,000

$239,000

$71,700

Cashmere

Moderate

.4

272,000

102,000

170,000

68,000

Sweaters

Low

.3

0

102,000

(102,000)

(30,600)

Expected

NPV

$109,100

b. The indicated investment, based on the expected NPV, is in the Cashmere sweater line.

Chapter 13: Risk and Capital Budgeting

20. Probability analysis with a normal curve distribution (LO13-4) When returns from a

project can be assumed to be normally distributed, such as those shown in Figure 13-6

(represented by a symmetrical, bell-shaped curve), the areas under the curve can be

determined from statistical tables based on standard deviations. For example, 68.26 percent

of the distribution will fall within one standard deviation of the expected value (

D

± 1σ).

Similarly, 95.44 percent will fall within two standard deviations (

D

± 2σ), and so on. An

abbreviated table of areas under the normal curve is shown next.

Number of σ’s

from Expected Value

+ or –

+ and –

0.5…………………..

0.1915

0.3830

1.0…………………..

0.3413

0.6826

1.5…………………..

0.4332

0.8664

1.65…………………

0.4505

0.9010

2.0 ………………….

0.4772

0.9544

Assume Project A has an expected value of $24,000 and a standard deviation (σ) of $4,800.

a. What is the probability that the outcome will be between $16,800 and $31,200?

b. What is the probability that the outcome will be between $14,400 and $33,600?

c. What is the probability that the outcome will be at least $14,400?

d. What is the probability that the outcome will be less than $31,900?

e. What is the probability that the outcome will be less than $19,200 or greater than

$26,400?

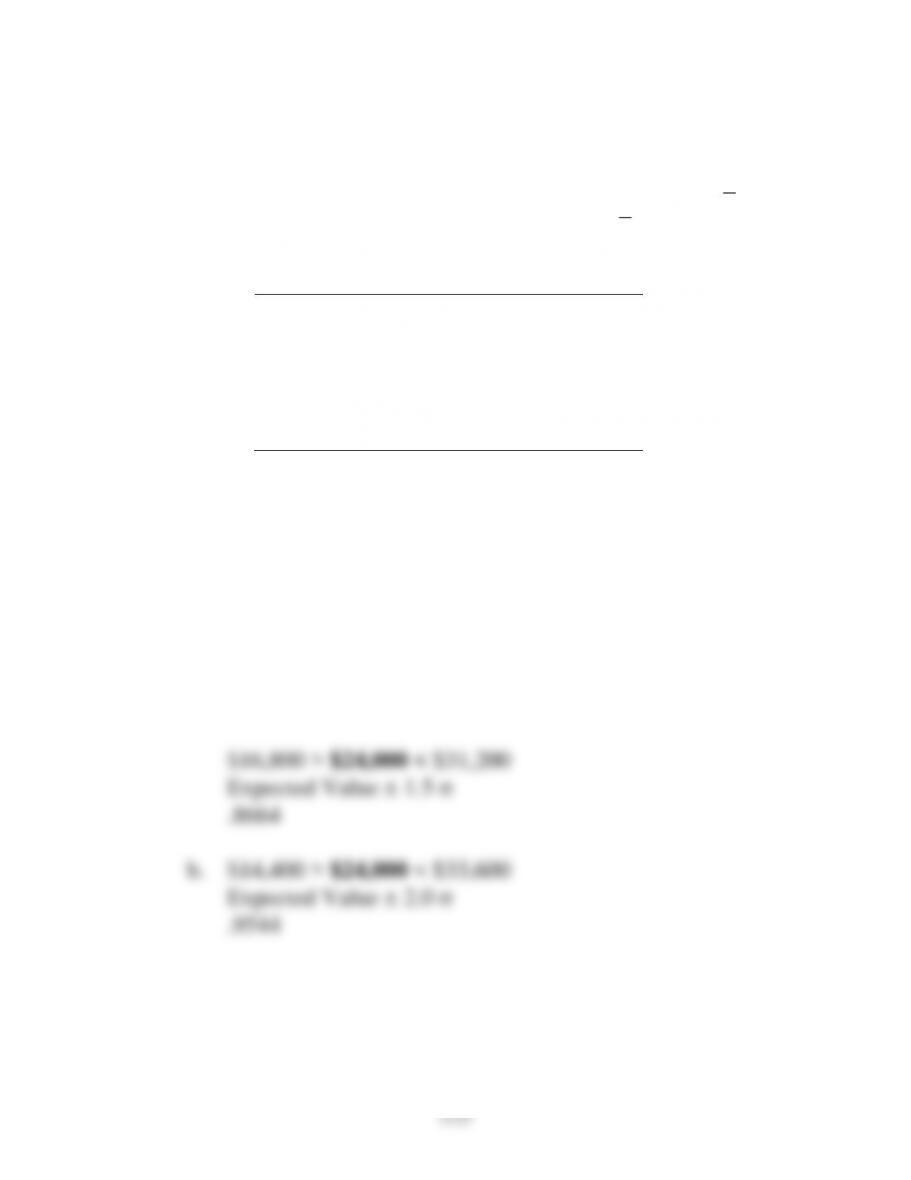

13-20. Solution:

a. Expected Value = $24,000, σ = $4,800

13-20. (Continued)

c. At least $14,400

$14,400 $24,000 $9,600 2

$4,800 $4,800

−−

d. Less than $31,900

$31,900 $24,000 $7,900 1.65

−==

$14,400

$31,900

.4772

.5000

.9772

Distribution

under the curve

.4505

.5000

Chapter 13: Risk and Capital Budgeting

13–29

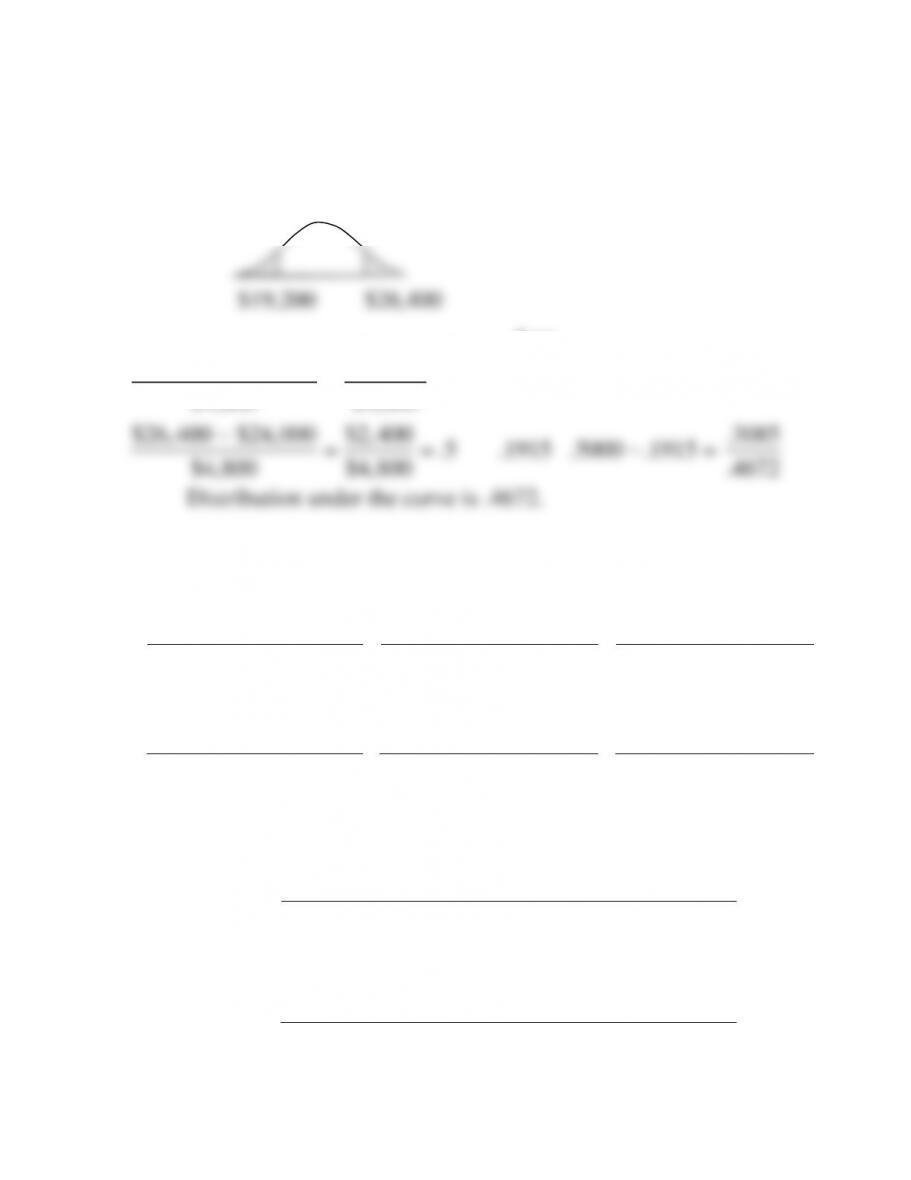

13-20. (Continued)

e. Less than $19,200 or greater than $26,400

Area

$19,200 $24,000 $4,800 1 .3413 .5000 .3413 = .1587

$4,800 $4,800

$26,400 $24,000 $2,400 .3085

.5 .1915 .5000 .1915 =

$4,800 $4,800 .4672

−−

= = − −

−= = −

Distribution under the curve is .4672.

21. Increasing risk over time (LO13-1) The Oklahoma Pipeline Company projects the

following pattern of inflows from an investment. The inflows are spread over time to

reflect delayed benefits. Each year is independent of the others.

Year 1

Year 5

Year 10

Cash

Inflow

Probability

Cash Inflow

Probability

Cash

Inflow

Probability

55 …………..

.40

40 …….

.30

20 ………

.40

70 …………..

.20

70 …….

.40

70 ………

.20

85 …………..

.40

100 …….

.30

120 ………

.40

The expected value for all three years is $70.

a. Compute the standard deviation for each of the three years.

b. Diagram the expected values and standard deviations for each of the three years in a

manner similar to Figure 13-6.

c. Assuming 6 percent and 12 percent discount rates, complete the following table for

present value factors:

Year

PVIF

6%

PVIF

12%

Difference

1 ………

.943

.893

.050

5 ………

________

________

________

10 ………

________

________

________

$19,200

$26,400

Chapter 13: Risk and Capital Budgeting

13–30

d. Is the increasing risk over time, as diagrammed in part b, consistent with the larger

differences in PVIFs over time, as computed in part c?

e. Assume the initial investment is $135. What is the net present value of the investment

at a 12 percent discount rate? Should the investment be accepted?

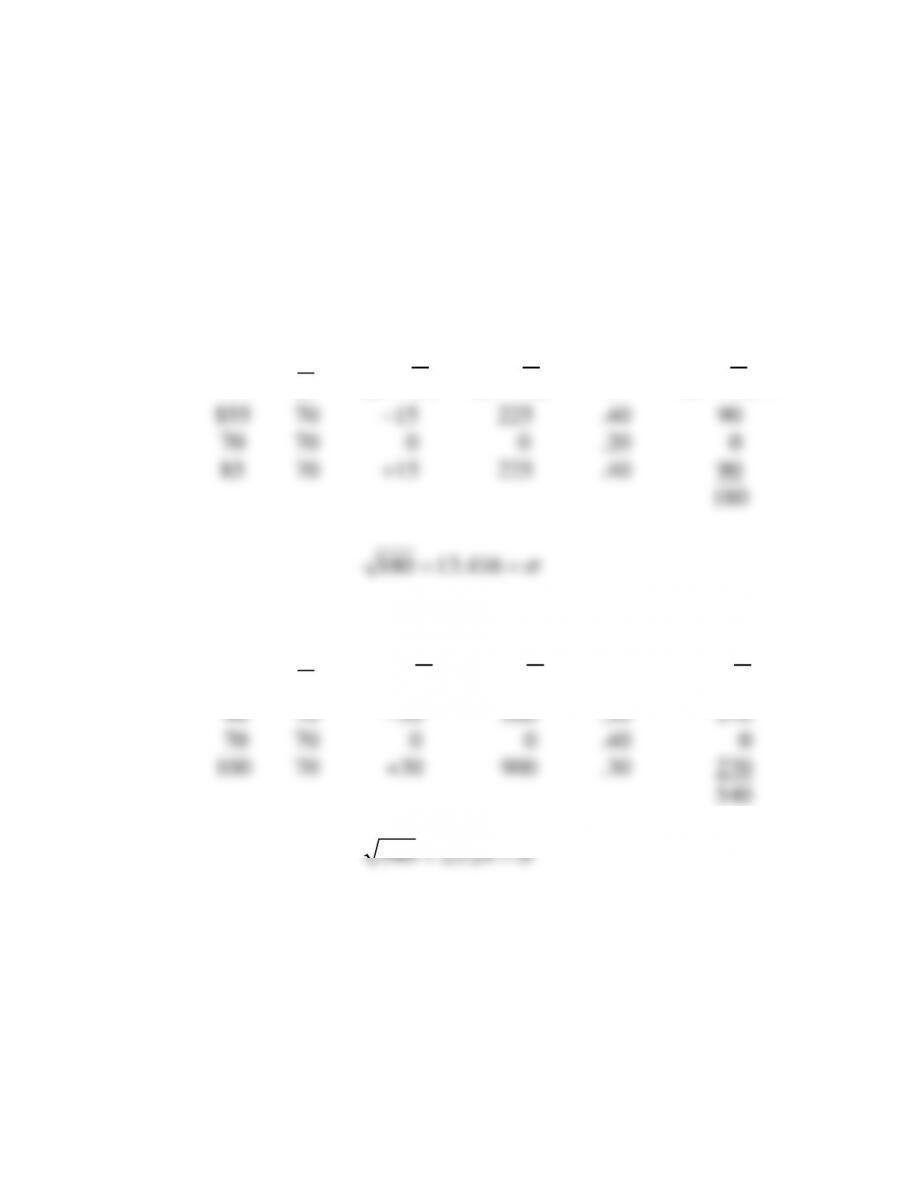

13-21. Solution:

Oklahoma Pipeline Company

a. Standard deviation—year 1

D

D

()DD−

2

()DD−

P

2

()DD−

P

$55

70

–15

225

.40

90

70

70

0

0

.20

0

85

70

+15

225

.40

90

180

180 13.416

==

Standard deviation—year 5

D

D

()DD−

2

()DD−

P

2

()DD−

P

40

70

–30

900

.30

270

70

70

0

0

.40

0

100

70

+30

900

.30

270

540

540 23.24

==

Chapter 13: Risk and Capital Budgeting

13–31

13-21. (Continued)

Standard deviation—year 10

D

D

()DD−

2

()DD−

P

2

()DD−

P

20

70

–50

2,500

.40

1,000

70

70

0

0

.20

0

120

70

+50

2,500

.40

1,000

2,000

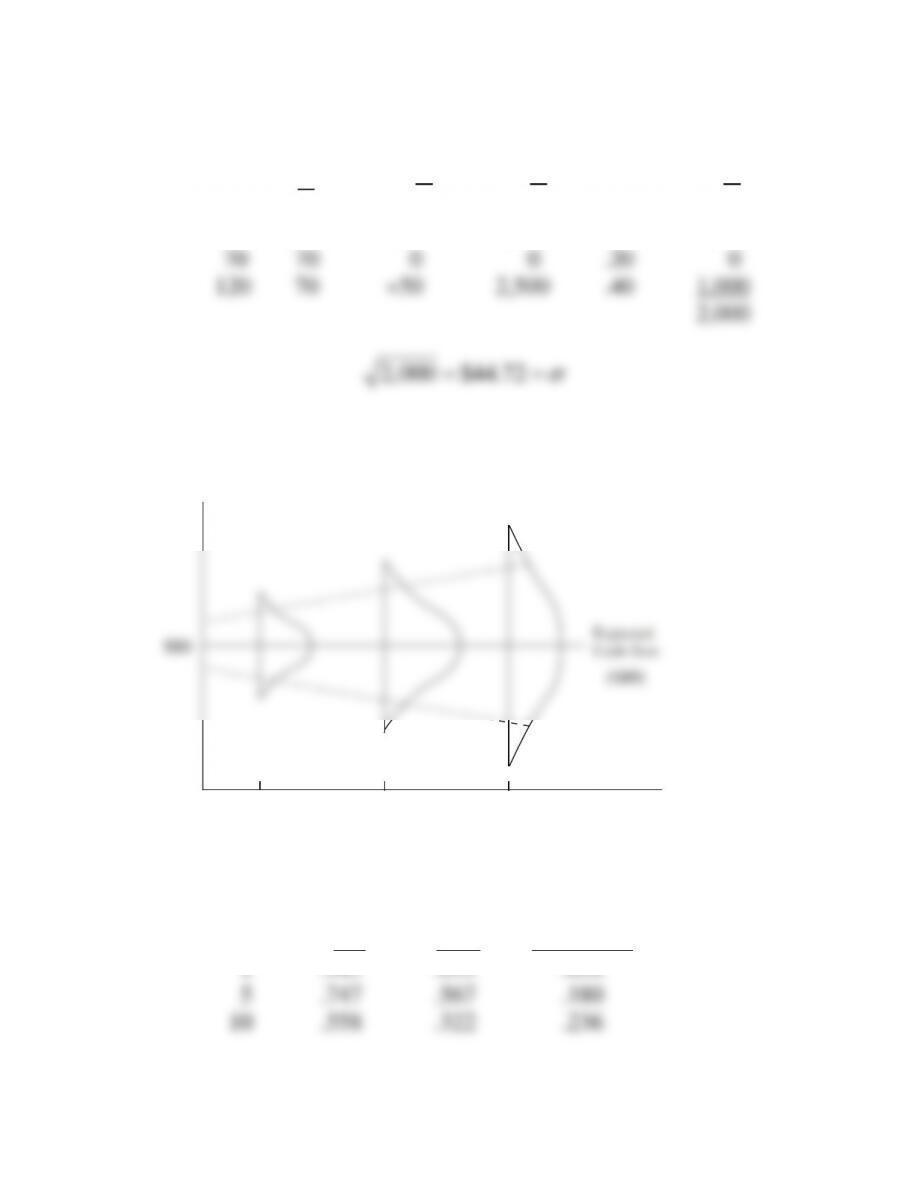

b. Risk over time

Dollars

Expected

Cash flow

($80)

$80

1 yr. 5 yr. 10 yr.

Time

c.

Year

(1)

PVIF

(2)

PVIF

(3)

PVIF

6%

12%

Difference

5

.747

.567

.180

10

.558

.322

.236

$80

($80)

Chapter 13: Risk and Capital Budgeting

13–32

13-21. (Continued)

d. Yes. The larger risk over time is consistent with the larger

differences in the present value interest factors (PVIF) over

time. In effect, future uncertainty is being penalized by a

lower present value interest factor (PVIF). This is one of the

consequences of using progressively higher discount rates

to penalize for risk.

Year

Inflow

PVIF (12%)

PV

1

$70

.893

$ 62.51

5

70

.567

$ 39.69

10

70

.322

$ 22.54

PV of Inflows

$124.74

Investment

$135.00

NPV

$ 10.26

e. Accept the investment.

22. Portfolio effect of a merger (LO13-5) Treynor Pie Company is a food company

specializing in high-calorie snack foods. It is seeking to diversify its food business and

lower its risks. It is examining three companies—a gourmet restaurant chain, a baby food

company, and a nutritional products firm. Each of these companies can be bought at the

same multiple of earnings. The following table represents information about all the

companies:

Company

Correlation

with Treynor

Pie Company

Sales

($ millions)

Expected

Earnings

($ millions)

Standard

Deviation

in Earnings

($ millions)

Treynor Pie Company ………….

+ 1.0

$126

$10

$4.0

Gourmet restaurant ………………

+ .4

63

9

1.4

Baby food company …………….

+ .3

52

5

1.6

Nutritional products

company …………………………..

− .7

77

7

3.2

a. Using the last two columns, compute the coefficient of variation for each of the four

companies. Which company is the least risky? Which company is the most risky?

b. Discuss which of the acquisition candidates is most likely to reduce Treynor Pie

Company’s risk. Explain why.

Chapter 13: Risk and Capital Budgeting

13–33

13-22. Solution:

Treynor Pie Company

a.

Standard deviation

Coefficient of variation ( ) Expected value

V=

(millions)

b. Because the nutritional products firm is highly negatively

correlated (–.7) with Treynor Pie Company, it is most likely

Chapter 13: Risk and Capital Budgeting

examining a plastics firm to add to its operations. Before the acquisition, the normal

expected outcomes for the firm were as follows:

Outcomes

($ millions)

Probability

Recession ……………………….

$20

.30

Normal economy ……………..

40

.40

Strong economy ………………

60

.30

After the acquisition, the expected outcomes for the firm would be:

Outcomes

($ millions)

Probability

Recession ……………………….

$10

.3

Normal economy ……………..

40

.4

Strong economy ………………

80

.3

a. Compute the expected value, standard deviation, and coefficient of variation before

the acquisition.

b. After the acquisition, these values are as follows:

Expected value ………………………………….

43.0 ($ millions)

Standard deviation ……………………………..

27.2 ($ millions)

Coefficient of variation ………………………

.633

Comment on whether this acquisition appears desirable to you.

c. Do you think the firm’s stock price is likely to go up as a result of this acquisition?

d. If the firm was interested in reducing its risk exposure, which of the following three

industries would you advise it to consider for an acquisition? Briefly comment on

your answer.

(1) Chemical company

(2) Oil company

(3) Computer company

13-23. Solution:

Hooper Chemical Co.

D DP=

D P PD