CHAPTER 13

RISK, RETURN, AND THE SECURITY

MARKET LINE

Answers to Concepts Review and Critical Thinking Questions

1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

assets, this unique portion of the total risk can be eliminated at little cost. On the other hand, there

2. If the market expected the growth rate in the coming year to be 2 percent, then there would be no

change in security prices if this expectation had been fully anticipated and priced. However, if the

3. a. systematic

b. unsystematic

4. a. a change in systematic risk has occurred; market prices in general will most likely decline.

b. no change in unsystematic risk; company price will most likely stay constant.

5. No to both questions. The portfolio expected return is a weighted average of the asset returns, so it

6. False. The variance of the individual assets is a measure of the total risk. The variance on a well-

7. Yes, the standard deviation can be less than that of every asset in the portfolio. However, p cannot

8. Yes. It is possible, in theory, to construct a zero beta portfolio of risky assets whose return would be

CHAPTER 13 – 2

9. Alpha measures the vertical distance of an asset’s return from the SML. As such, it measures the

return in excess of the return the asset should have earned based on the level of risk as measured by

11. Such layoffs generally occur in the context of corporate restructurings. To the extent that the market

12. Earnings contain information about recent sales and costs. This information is useful for projecting

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. The portfolio weight of an asset is the total investment in that asset divided by the total portfolio

value. First, we will find the portfolio value, which is:

The portfolio weight for each stock is:

2. The expected return of a portfolio is the sum of the weight of each asset times the expected return of

each asset. The total value of the portfolio is:

CHAPTER 13 – 3

So, the expected return of this portfolio is:

3. The expected return of a portfolio is the sum of the weight of each asset times the expected return of

each asset. So, the expected return of the portfolio is:

4. Here we are given the expected return of the portfolio and the expected return of each asset in the

portfolio and are asked to find the weight of each asset. We can use the equation for the expected

We can now solve this equation for the weight of Stock X as:

So, the dollar amount invested in Stock X is the weight of Stock X times the total portfolio value, or:

And the dollar amount invested in Stock Y is:

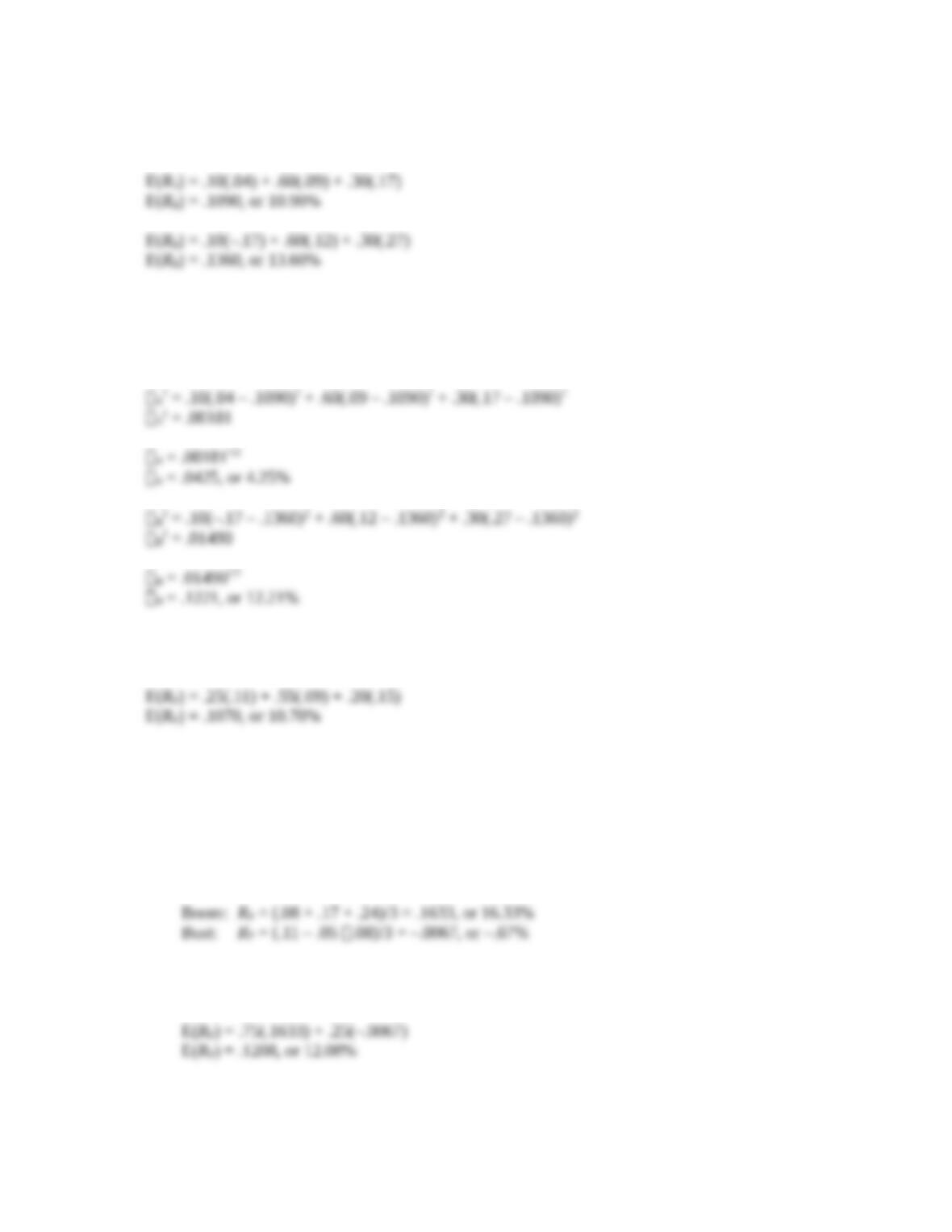

5. The expected return of an asset is the sum of each return times the probability of that return

occurring. So, the expected return of the asset is:

6. The expected return of an asset is the sum of each return times the probability of that return

occurring. So, the expected return of the asset is:

CHAPTER 13 – 4

7. The expected return of an asset is the sum of each return times the probability of that return

occurring. So, the expected return of each stock asset is:

To calculate the standard deviation, we first need to calculate the variance. To find the variance, we

find the squared deviations from the expected return. We then multiply each possible squared

deviation by its probability, then add all of these up. The result is the variance. So, the variance and

standard deviation of each stock are:

8. The expected return of a portfolio is the sum of the weight of each asset times the expected return of

each asset. So, the expected return of the portfolio is:

If we own this portfolio, we would expect to get a return of 10.70 percent.

9. a. To find the expected return of the portfolio, we need to find the return of the portfolio in each

state of the economy. This portfolio is a special case since all three assets have the same weight.

To find the expected return of an equally weighted portfolio, we can sum the returns of each

asset and divide by the number of assets, so the return of the portfolio in each state of the

economy is:

To find the expected return of the portfolio, we multiply the return in each state of the economy

by the probability of that state occurring, and then sum the products. Doing so, we find:

CHAPTER 13 – 5

b. This portfolio does not have an equal weight in each asset. We still need to find the return of the

portfolio in each state of the economy. To do this, we will multiply the return of each asset by

its portfolio weight and then sum the products to get the portfolio return in each state of the

economy. Doing so, we get:

And the expected return of the portfolio is:

To find the variance, we find the squared deviations from the expected return. We then multiply

each possible squared deviation by its probability, than add all of these up. The result is the

variance. So, the variance of the portfolio is:

10. a. This portfolio does not have an equal weight in each asset. We first need to find the return of

the portfolio in each state of the economy. To do this, we will multiply the return of each asset

by its portfolio weight and then sum the products to get the portfolio return in each state of the

economy. Doing so, we get:

Boom: RP = .30(.35) + .40(.40) + .30(.27) = .3460, or 34.60%

And the expected return of the portfolio is:

b. To calculate the standard deviation, we first need to calculate the variance. To find the variance,

we find the squared deviations from the expected return. We then multiply each possible

squared deviation by its probability, then add all of these up. The result is the variance. So, the

variance and standard deviation of the portfolio are:

CHAPTER 13 – 6

11. The beta of a portfolio is the sum of the weight of each asset times the beta of each asset. So, the

beta of the portfolio is:

12. The beta of a portfolio is the sum of the weight of each asset times the beta of each asset. If the

portfolio is as risky as the market, it must have the same beta as the market. Since the beta of the

market is one, we know the beta of our portfolio is one. We also need to remember that the beta of

the risk-free asset is zero. It has to be zero since the asset has no risk. Setting up the equation for the

beta of our portfolio, we get:

Solving for the beta of Stock X, we get:

13. CAPM states the relationship between the risk of an asset and its expected return. CAPM is:

Substituting the values we are given, we find:

14. We are given the values for the CAPM except for the beta of the stock. We need to substitute these

values into the CAPM, and solve for the beta of the stock. One important thing we need to realize is

that we are given the market risk premium. The market risk premium is the expected return of the

market minus the risk-free rate. We must be careful not to use this value as the expected return of the

market. Using the CAPM, we find:

15. Here we need to find the expected return of the market using the CAPM. Substituting the values

given, and solving for the expected return of the market, we find:

CHAPTER 13 – 7

16. Here we need to find the risk-free rate using the CAPM. Substituting the values given, and solving

for the risk-free rate, we find:

17. First, we need to find the beta of the portfolio. The beta of the risk-free asset is zero, and the weight

of the risk-free asset is one minus the weight of the stock, so the beta of the portfolio is:

So, to find the beta of the portfolio for any weight of the stock, we multiply the weight of the stock

times its beta.

Even though we are solving for the beta and expected return of a portfolio of one stock and the risk-

free asset for different portfolio weights, we are really solving for the SML. Any combination of this

stock, and the risk-free asset will fall on the SML. For that matter, a portfolio of any stock and the

risk-free asset, or any portfolio of stocks, will fall on the SML. We know the slope of the SML line is

the market risk premium, so using the CAPM and the information concerning this stock, the market

risk premium is:

So, now we know the CAPM equation for any stock is:

The slope of the SML is equal to the market risk premium, which is .0773. Using these equations to fill in

the table, we get the following results:

wWE(RP) ßP

0% 3.30% .000

25 5.43 .275

CHAPTER 26 – 8