Year 0 Year 1 Year 2 Year 3 Year 4

Revenues $2,167,500 $2,465,000 $2,720,000 $1,997,500

Fixed costs 345,000 345,000 345,000 345,000

Capital spending –$2,650,000 $308,100

Notice the calculation of the cash flow at Time 0. The capital spending on equipment and investment

in net working capital are both cash outflows. The aftertax selling price of the land is also a cash

outflow. Even though no cash is actually spent on the land because the company already owns it, the

aftertax cash flow from selling the land is an opportunity cost, so we need to include it in the

analysis. The company can sell the land at the end of the project, so we need to include that value as

well. With all the project cash flows, we can calculate the NPV, which is:

The company should accept the new product line.

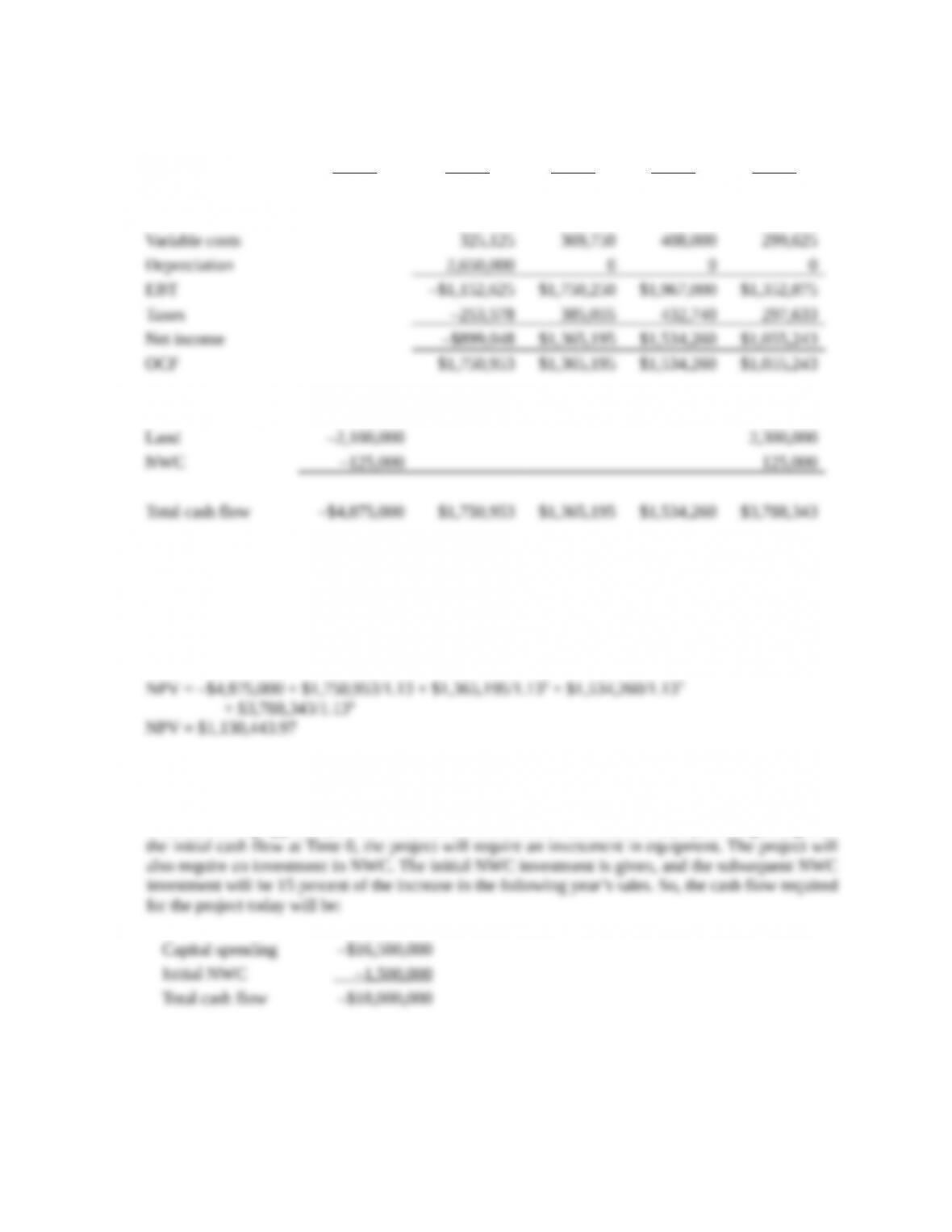

36. This is an in-depth capital budgeting problem. Probably the easiest OCF calculation for this problem

is the bottom-up approach, so we will construct an income statement for each year. Beginning with

Now we can begin the remaining calculations. Sales figures are given for each year, along with the

price per unit. The variable costs per unit are used to calculate total variable costs, and fixed costs

are given at $3.2 million per year. To calculate depreciation each year, we use the initial equipment

cost of $16.5 million, times the appropriate MACRS depreciation each year. The remainder of each

income statement is calculated below. Notice at the bottom of the income statement we added back

depreciation to get the OCF for each year. The section labeled “Net cash flows” will be discussed

below:

Year 1 2 3 4 5

Ending book value $14,142,150 $10,101,300 $7,215,450 $5,154,600 $3,681,150

Sales $27,375,000 $32,250,000 $39,375,000 $36,375,000 $25,125,000

Net cash flows

Operating CF $4,887,549 $6,473,379 $8,032,029 $7,100,379 $4,133,025

After we calculate the OCF for each year, we need to account for any other cash flows. The other

Notice that the NWC cash flow is negative. Since the sales are increasing, we will have to spend

more money to increase NWC. In Year 4, the NWC cash flow is positive since sales are declining.

And, in Year 5, the NWC cash flow is the recovery of all NWC the company still has in the project.

To calculate the aftertax salvage value, we first need the book value of the equipment. The book

The market value of the used equipment is 20 percent of the purchase price, or $3.3 million, so the

aftertax salvage value will be:

The aftertax salvage value is included in the total cash flows as capital spending. Now we have all of

the cash flows for the project. The NPV of the project is:

And the IRR is:

We should accept the project.

37. To find the initial pretax cost savings necessary to buy the new machine, we should use the tax shield

approach to find the OCF. We begin by calculating the depreciation each year using the MACRS

depreciation schedule. The depreciation each year is:

D1 = $735,000(.3333) = $244,975.50

Using the tax shield approach, the OCF each year is:

OCF1 = (S – C)(1 – .22) + .22($244,975.50)

Now we need the aftertax salvage value of the equipment. The aftertax salvage value is:

To find the necessary cost reduction, we must realize that we can split the cash flows each year. The

OCF in any given year is the cost reduction (S – C) multiplied by one minus the tax rate, which is an

annuity for the project life, and the depreciation tax shield. To calculate the necessary cost reduction,

we would require a zero NPV. The equation for the NPV of the project is:

Solving this equation for the sales minus costs, we get:

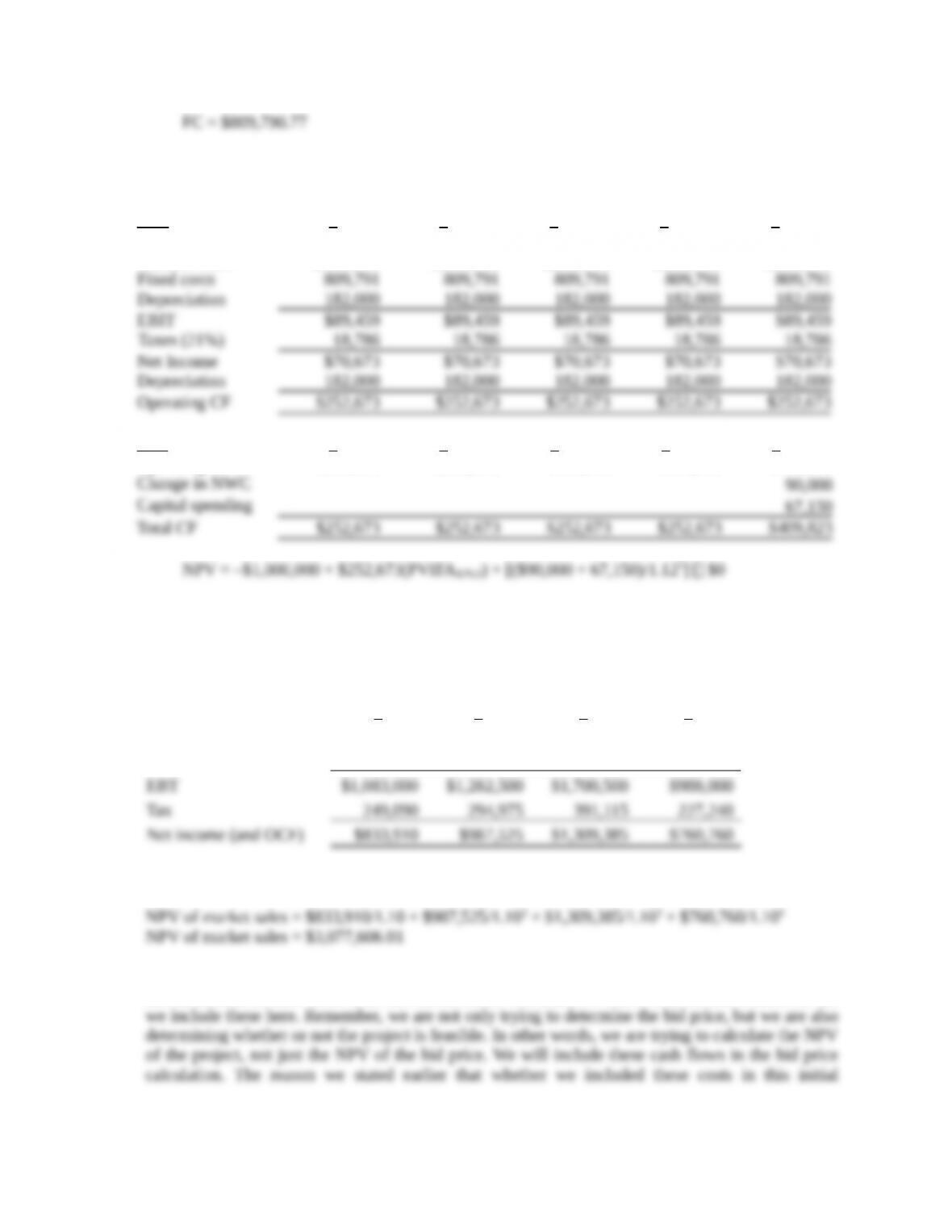

38. a. The cash flow at Time 0 for all three parts of this question will be:

Capital spending –$910,000

We will use the initial cash flow and the salvage value we already found in that problem. Using

the bottom-up approach to calculating the OCF, we get:

Assume price per unit = $26 and units/year = 125,000

Year 1 2 3 4 5

Sales $3,250,000 $3,250,000 $3,250,000 $3,250,000 $3,250,000

Variable costs 2,168,750 2,168,750 2,168,750 2,168,750 2,168,750

Fixed costs 485,000 485,000 485,000 485,000 485,000

Year 1 2 3 4 5

Operating CF $509,258 $509,258 $509,258 $509,258 $509,258

With these cash flows, the NPV of the project is:

If the actual price is above the bid price that results in a zero NPV, the project will have a

b. To find the minimum number of cartons sold to still break even, we need to use the tax shield

So, the necessary OCF for a zero NPV is:

Now we can use the tax shield approach to solve for the minimum quantity as follows:

As a check, we can calculate the NPV of the project with this quantity. The calculations are:

Year 1 2 3 4 5

Sales $2,273,750 $2,273,750 $2,273,750 $2,273,750 $2,273,750

Variable costs 1,517,291 1,517,291 1,517,291 1,517,291 1,517,291

Fixed costs 485,000 485,000 485,000 485,000 485,000

Year 1 2 3 4 5

Operating CF $252,673 $252,673 $252,673 $252,673 $252,673

Note, the NPV is not exactly equal to zero because we had to round the number of cartons sold;

you cannot sell one-half of a carton.

c. To find the highest level of fixed costs and still break even, we need to use the tax shield

Notice this is the same OCF we calculated in part b. Now we can use the tax shield approach to

solve for the maximum level of fixed costs as follows:

As a check, we can calculate the NPV of the project with this level of fixed costs. The

calculations are:

Year 1 2 3 4 5

Sales $3,250,000 $3,250,000 $3,250,000 $3,250,000 $3,250,000

Variable costs 2,168,750 2,168,750 2,168,750 2,168,750 2,168,750

Year 1 2 3 4 5

Operating CF $252,673 $252,673 $252,673 $252,673 $252,673

39. We need to find the bid price for a project, but the project has extra cash flows. Since we don’t

already produce the keyboard, the sales of the keyboard outside the contract are relevant cash flows.

Since we know the extra sales number and price, we can calculate the cash flows generated by these

sales. The cash flow generated from the sale of the keyboard outside the contract is:

1 2 3 4

Sales $1,938,000 $2,295,000 $3,043,000 $1,768,000

Variable costs 855,000 1,012,500 1,342,500 780,000

So, the addition to NPV of these market sales is:

You may have noticed that we did not include the initial cash outlay, depreciation, or fixed costs in

the calculation of cash flows from the market sales. The reason is that it is irrelevant whether or not

Next, we need to calculate the aftertax salvage value, which is:

Instead of solving for a zero NPV as is usual in setting a bid price, the company president requires an

Solving for the OCF, we get:

Now we can solve for the bid price as follows:

40. a. Since the two computers have unequal lives, the correct method to analyze the decision is the

EAC. We will begin with the EAC of the new computer. Using the depreciation tax shield

approach, the OCF for the new computer system is:

Notice that the costs are positive, which represents a cash inflow. The costs are positive in this

case since the new computer will generate a cost savings. The only initial cash flow for the new

computer is its cost of $1,872,000. We next need to calculate the aftertax salvage value, which

is:

Now we can calculate the PV of costs of the new computer as:

And the EAC of the new computer is:

Analyzing the old computer, the only OCF is the depreciation tax shield, so:

The initial cost of the old computer is a little trickier. You might assume that since we already

own the old computer there is no initial cost, but we can sell the old computer, so there is an

This is the initial cost of the old computer system today because we are forgoing the

Now we can calculate the PV of costs of the old computer as:

And the EAC of the old computer is:

Even if we are going to replace the system in two years no matter what our decision today, we

should replace it today since the EAC is more positive.

b. If we are only concerned with whether or not to replace the machine now, and are not worrying

about what will happen in two years, the correct analysis is NPV. To calculate the NPV of the

decision on the computer system now, we need the difference in the total cash flows of the old

computer system and the new computer system. From our previous calculations, we can say the

cash flows for each computer system are:

tNew computer Old computer Difference

0 –$1,872,000 –$599,040 –$1,272,960

Since we are only concerned with marginal cash flows, the cash flows of the decision to replace

the old computer system with the new computer system are the differential cash flows. The

NPV of the decision to replace, ignoring what will happen in two years is:

If we are not concerned with what will happen in two years, we should not replace the old

computer system.