© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 9 1

Chapter 9

Flexible Budgets and Performance Analysis

Solutions to Questions

9-3 Actual results can differ from the budget

for many reasons. Very broadly speaking, the

activity can have a very big impact on costs.

From a manager’s perspective, a variance that is

due to a change in activity is very different from

a variance that is due to changes in prices and

9-5 An activity variance is the difference

between a revenue or cost item in the flexible

budget and the same item in the static planning

9-6 A revenue variance is the difference

between the actual revenue for the period and

how much the revenue should have been, given

9-7 A spending variance is the difference

between the actual amount of the cost and how

much a cost should have been, given the actual

9-8 In a flexible budget performance report,

the actual results are not directly compared to

the static planning budget. The flexible budget is

interposed between the actual results and the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

2 Managerial Accounting, 16th Edition

budget are the revenue and spending variances.

The flexible budget performance report cleanly

separates the differences between the actual

9-9 The only difference between a flexible

budget based on a single cost driver and one

9-10 When actual results are directly

compared to the static planning budget, it is

implicitly assumed that costs (and revenues)

adjusted proportionately for a change in activity

and then directly compared to actual results, it

is implicitly assumed that costs should change in

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 9 3

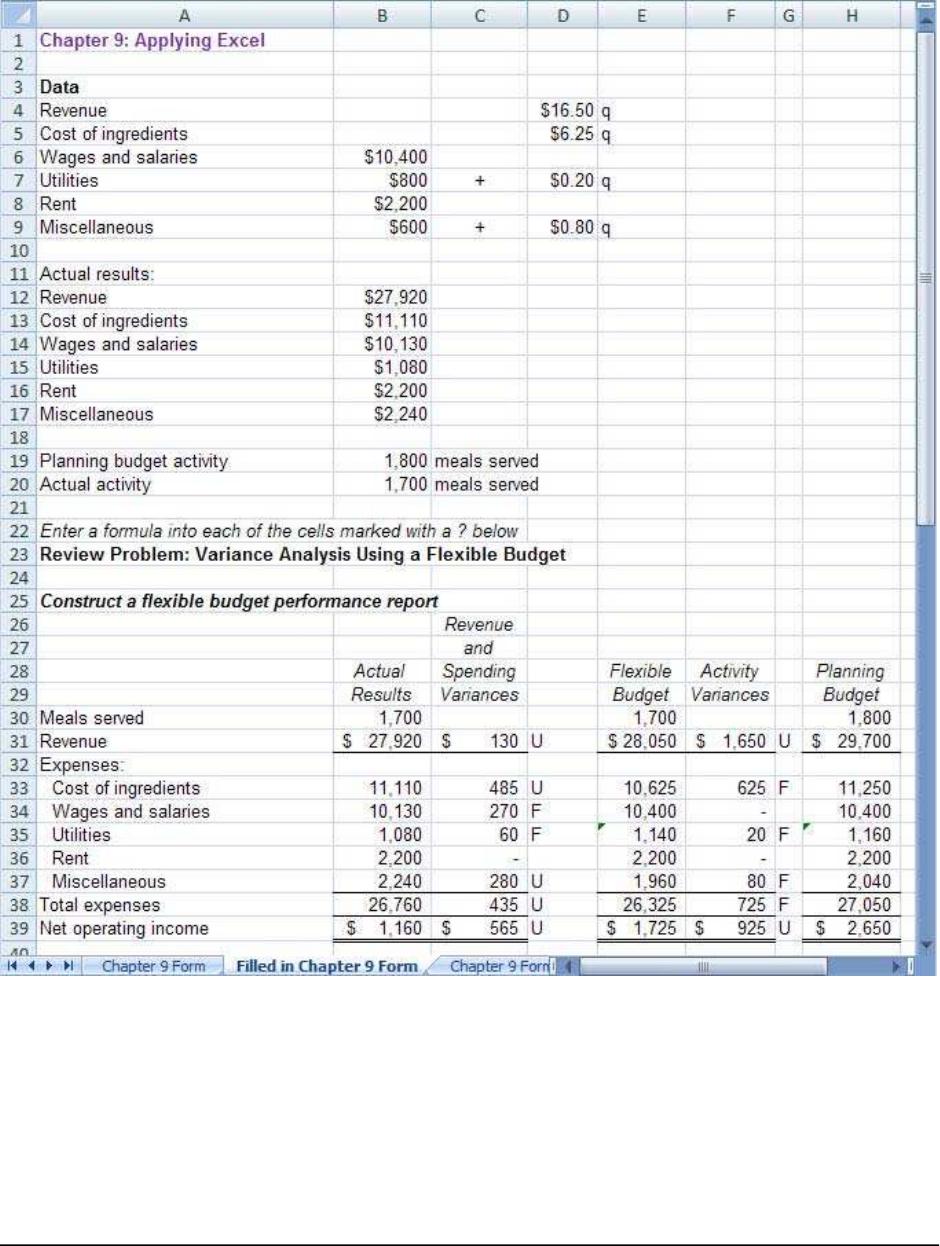

Chapter 9: Applying Excel

The completed worksheet is shown below.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

4 Managerial Accounting, 16th Edition

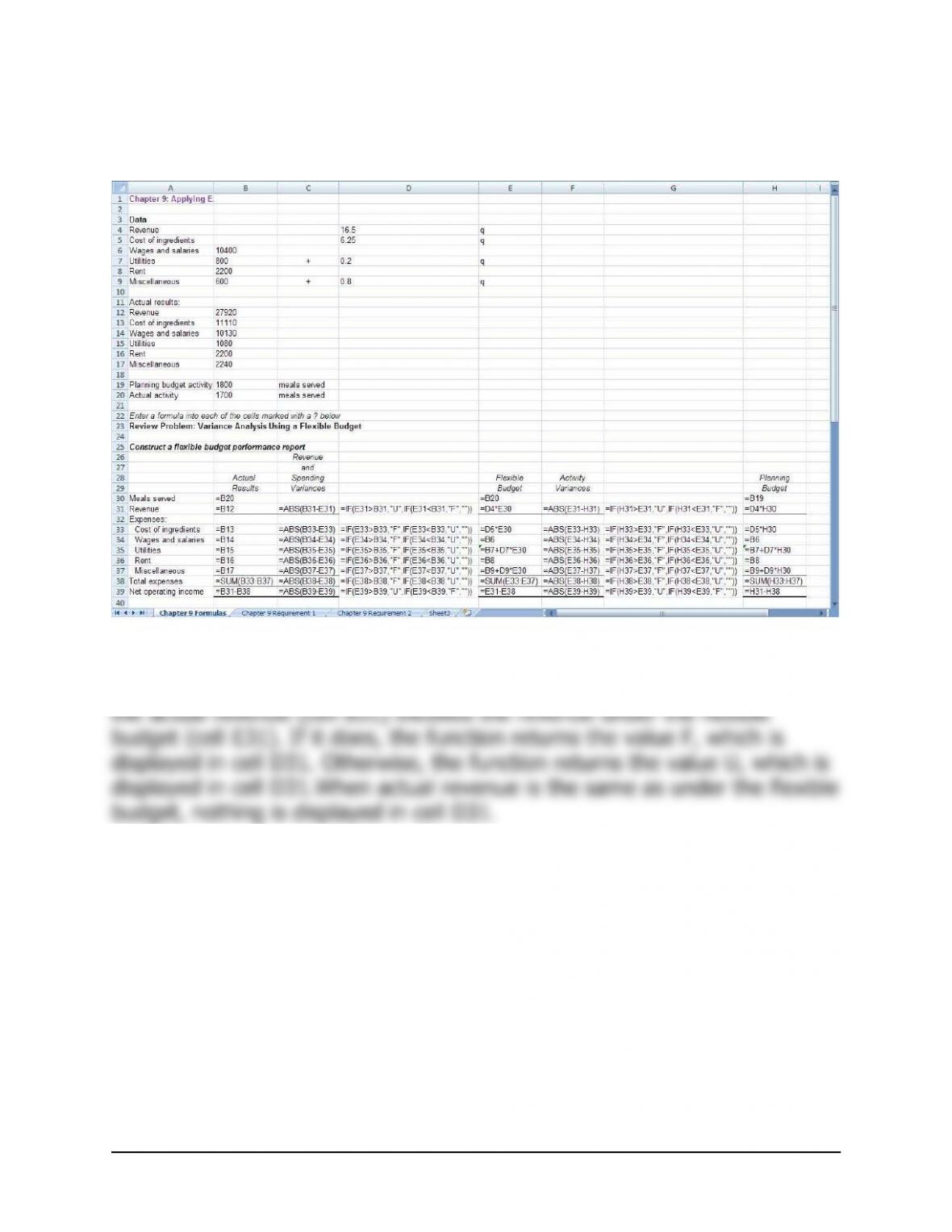

Chapter 9: Applying Excel (continued)

The completed worksheet, with formulas displayed, is shown below.

Note: The formulas to compute whether a variance is Favorable or

Unfavorable use the IF() function. For example, in cell D31, the formula is

=IF(E31>B31,”U”,IF(E31<B31,”F”,””)). This formula first checks whether

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 9 5

Chapter 9: Applying Excel (continued)

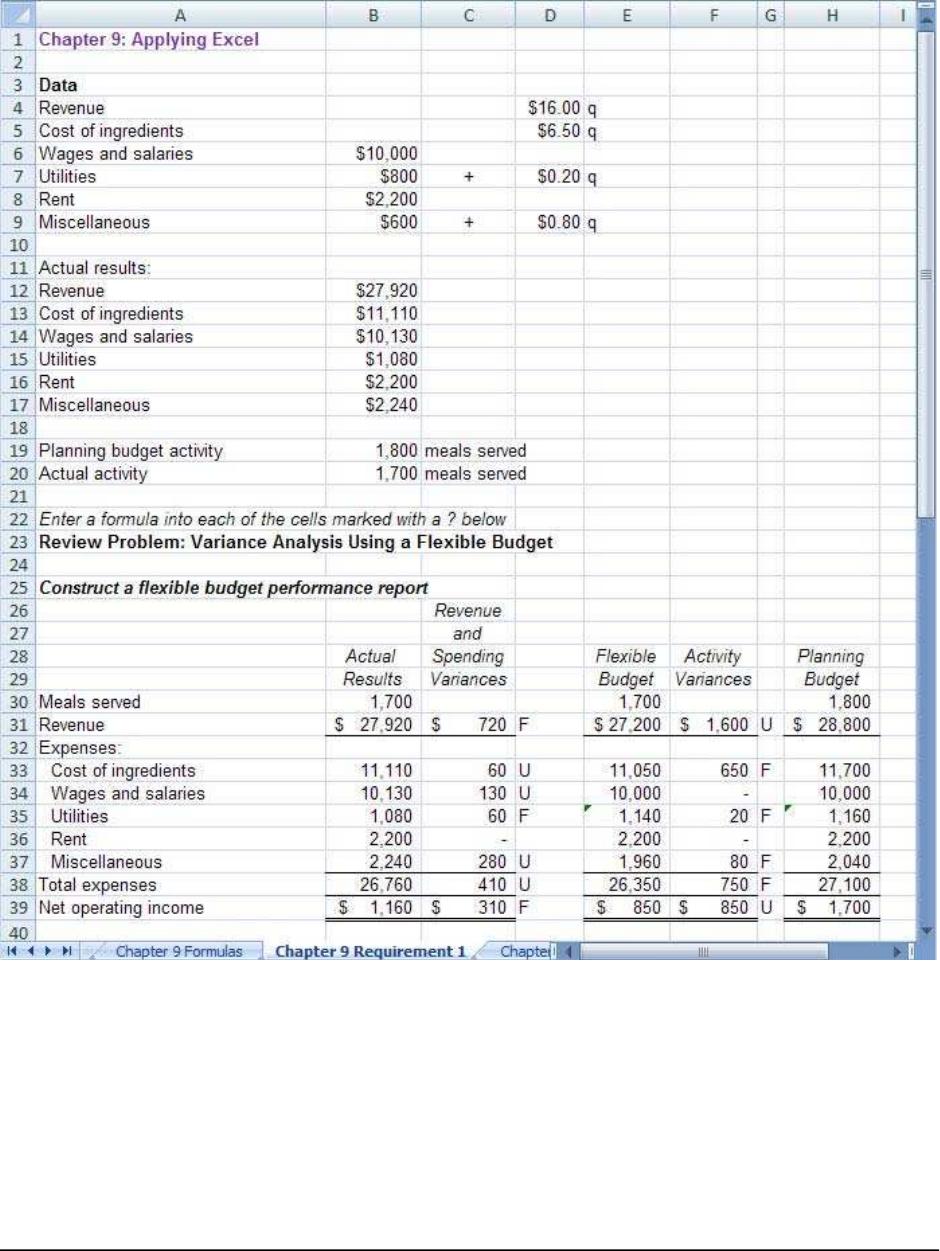

1. With the changes in data, the result is:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

6 Managerial Accounting, 16th Edition

Chapter 9: Applying Excel (continued)

a. The activity variance for revenue is $1,600 U. This variance is the

difference between the revenue under the planning budget and under

b. The spending variance for the cost of ingredients is $60 U. This

variance is the difference between what the cost should have been

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 9 7

Chapter 9: Applying Excel (continued)

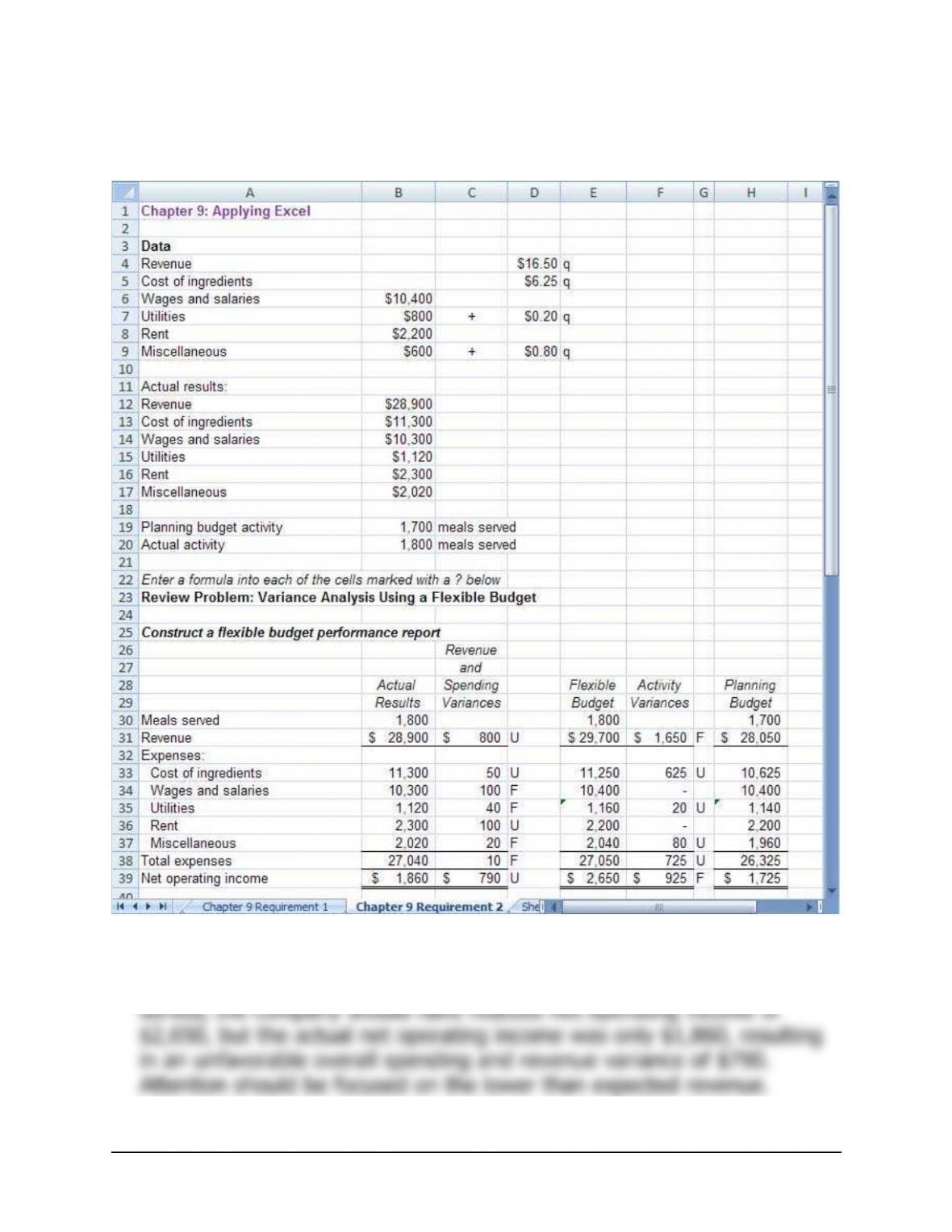

2. With the revised data, the worksheet should look like this:

Actual activity exceeded planned activity by 100 meals served, which

should have boosted net operating income by $925. However, actual

results were not this favorable. Given the actual number of meals

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

8 Managerial Accounting, 16th Edition

The Foundational 15

1. The amount of revenue in the flexible budget for May is:

Revenue:

2. The amount of employee salaries and wages in the flexible budget for

May is:

Employee salaries and wages:

3. The amount of travel expenses in the flexible budget for May is:

Travel expenses:

4. The amount of Other Expenses included in the flexible budget for May

5. The net income reported in the flexible budget can be derived by

combining the answers to questions 1-4 as follows:

Revenue ………………………………………. $175,000

Employee salaries and wa

g

es……………. $88,500

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 9 9

The Foundational 15

6. The revenue variance for May is:

A

ctual results Revenue Variance Flexible Bud

g

et

7. The employee salaries and wages spending variance for May is:

A

ctual results Spendin

g

Variance Flexible Bud

g

et

8. The travel expenses spending variance for May is:

A

ctual results Spendin

g

Variance Flexible Bud

g

et

9. The other expenses spending variance for May is:

A

ctual results Spendin

g

Variance Flexible Bud

g

et

10. The amount of revenue in the planning budget for May is:

Revenue:

Variable element per customer served (a) …… $5,000

11. The amount of employee salaries and wages in the planning budget for

May is:

Employee salaries and wages:

Variable element per customer served (a) …… $1,100

Actual activity (b) ………………………………….. 30

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

10 Managerial Accounting, 16th Edition

The Foundational 15

12. The amount of travel expenses in the planning budget for May is:

Travel expenses:

13. The amount of Other Expenses included in the planning budget for

14. The activity variance for revenue for May is:

Flexible Bud

g

et

A

ctivity Variance Plannin

g

Bud

g

et

15. The activity variances for the expenses for May are as follows:

Flexible

Budget

A

ctivity

Variance

Plannin

g

Budget

T