© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 41

Problem 7-17 (45 minutes)

1. Under the traditional direct labor-hour based costing system,

manufacturing overhead is applied to products using the predetermined

overhead rate computed as follows:

Estimated total manufacturin

g

overhead cost

Predetermined =

overhead rate Estimated total direct labor –hours

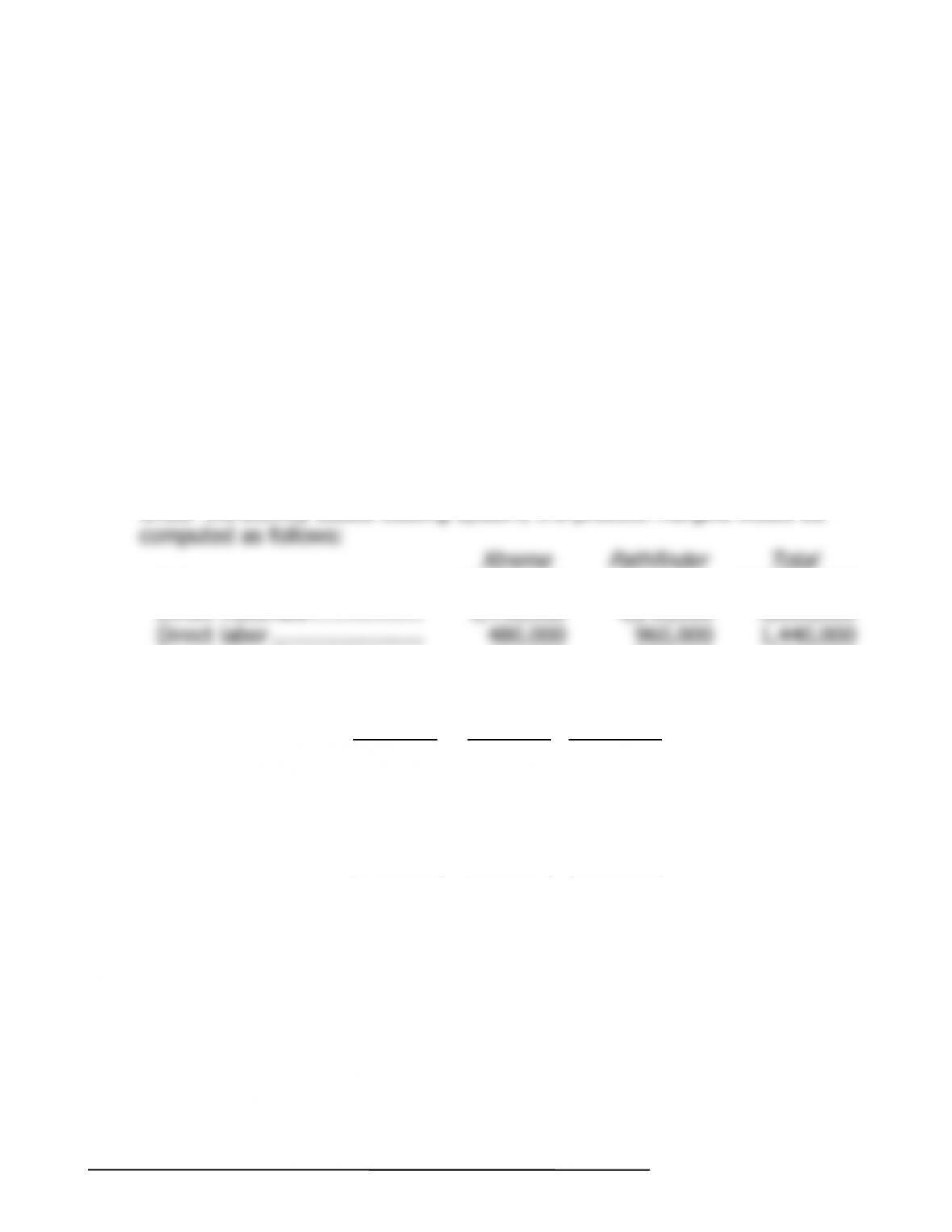

Consequently, the product margins using the traditional approach would

be computed as follows:

Xtrem

e

Pathfinde

r

T

ota

l

Sales ……………………………. $2,800,000 $7,920,000 $10,720,000

Direct materials ………………. 1,440,000 4,240,000 5,680,000

Direct labor ……………………. 480,000 960,000 1,440,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

42 Managerial Accounting, 16th Edition

Problem 7-17 (continued)

2. The first step is to determine the activity rates:

Activity Cost Pools

(a)

Total

Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Supportin

g

direct

*The Other activity cost pool is not shown above because it includes

Under the activity-based costing system, the product margins would be

computed as follows:

Xtrem

e

Pathfinde

r

T

ota

l

Sales ………………………….. $2,800,000 $7,920,000 $10,720,000

Direct materials …………….. 1,440,000 4,240,000 5,680,000

Direct labor ………………….. 480,000 960,000 1,440,000

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 43

Problem 7-17 (continued)

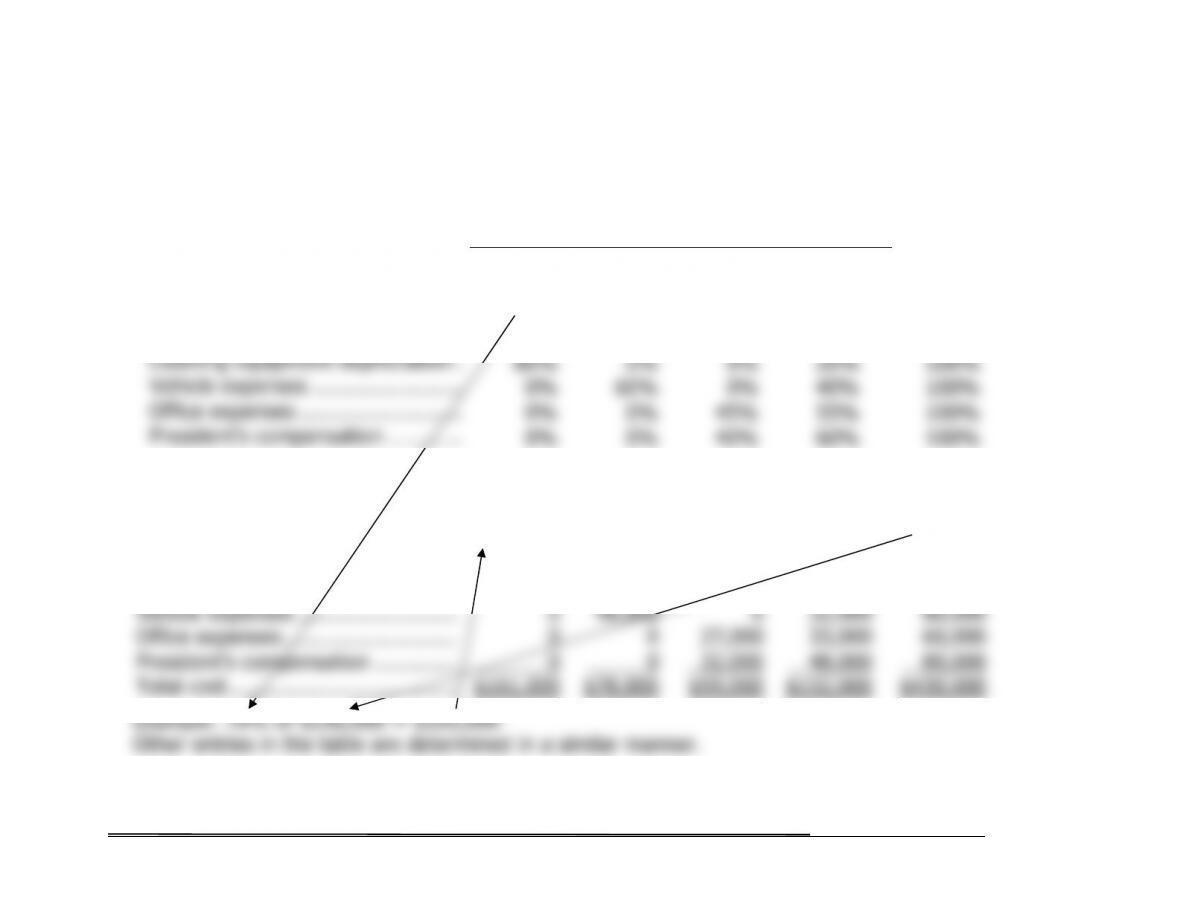

3. The quantitative comparison is as follows:

XtremePathfinder

T

otal

T

raditional Cost Syste

m

(a)

Amount

(a) ÷ (c)

%

(b)

Amount

(b) ÷ (c)

%

(c)

Amount

Direct materials ………………….. $1,440,000 25.4% $4,240,000 74.6% $5,680,000

Direct labor …………….…………. 480,000 33.3% 960,000 66.7% 1,440,000

T

A

ctivit

y

–

Based Costin

g

Syste

m

Direct costs:

Direct materials ………………….. $1,440,000 25.4% $4,240,000 74.6% $5,680,000

Direct labor …………….…………. 480,000 33.3% 960,000 66.7% 1,440,000

Indirect costs:

T

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

44 Managerial Accounting, 16th Edition

Problem 7-17 (continued)

The traditional and activity-based cost assignments differ for two

reasons. First, the traditional system assigns all $1,980,000 of

manufacturing overhead to products. The ABC system assigns only

$1,881,000 (= $783,600 + $495,000 + $602,400) of manufacturing

overhead to products. The ABC system does not assign the $99,000 of

Other activity costs to products because they represent organization-

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 45

Problem 7-18 (45 minutes)

1. The results of the first-stage allocation appear below:

Job Size

Estimating

and Job

Setup

Working on

Nonroutine

Jobs Other Totals

Wa

g

es and salaries ……… $150,000 $ 30,000 $ 90,000 $ 30,000 $ 300,000

Disposal fees ……………… 420,000 0 280,000 0 700,000

Equipment depreciation … 36,000 4,500 18,000 31,500 90,000

On-site supplies ………….. 30,000 15,000 5,000 0 50,000

2.

Activity Cost Pool

(a)

Total Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Job size …………….. $776,000 800 thousand square feet $970 per thousand square feet

Estimatin

g

and

j

ob

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

46 Managerial Accounting, 16th Edition

Problem 7-18 (continued)

3. The costs of each of the jobs can be computed as follows using the activity rates computed above:

a.

Routine one thousand square foot

j

ob

:

Job size (1 thousand square feet @ $970 per thousand square feet) …. $ 970.00

b.

Routine two thousand square foot

j

ob

:

Job size (2 thousand square feet @ $970 per thousand square feet) …. $1,940.00

Estimatin

g

and

j

ob setup (1

j

ob @ $239 per

j

ob) ………………………….. 239.00

c.

Nonroutine two thousand square foot

j

ob

:

Job size (2 thousand square feet @ $970 per thousand square feet) …. $1,940.00

Estimatin

g

and

j

ob setup (1

j

ob @ $239 per

j

ob) ………………………….. 239.00

g

j

j

j

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 47

Problem 7-18 (continued)

4. The objectivity of the interview data can be questioned because the on-

site work supervisors were undoubtedly trying to prove their case about

the cost of nonroutine jobs. Nevertheless, the activity-based costing

data certainly suggest that dramatic differences exist in the costs of

jobs. While some of the costs may be difficult to adjust in response to

Savvy competitors are likely to bid less than $2,500 per thousand

square feet on routine work and substantially more than $2,500 per

thousand square feet on nonroutine work. Consequently, Mercer

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

48 Managerial Accounting, 16th Edition

Problem 7-19 (20 minutes)

1. The cost of serving the local commercial market according to the ABC model can be determined as

follows:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

$257,625

2. The margin earned serving the local commercial market is negative, as shown below:

Profitability Analysi

s

Sales …………………………………………… $180,000

Costs:

A

nimation concept ……………………….. $151,000

A

3. It appears that the local commercial market is losing money and the company would be better off

dropping this market segment. However, as discussed in the previous problem, not all of the costs

A

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 49

Problem 7-20 (45 minutes)

1. The first-stage allocation of costs to activity cost pools appears below:

Distribution of Resource Consumption

Across Activity Cost Pools

Cleaning

Carpets

Travel

to Jobs

Job

Support Other Total

Wa

g

es ………………………………… 70% 20% 0% 10% 100%

Cleanin

g

supplies …………………… 100% 0% 0% 0% 100%

Cleaning

Carpets

Travel

to Jobs

Job

Support Other Total

Wa

g

es …………………………………. $105,000 $30,000 $ 0 $ 15,000 $150,000

Cleanin

g

supplies ……………………. 40,000 0 0 0 40,000

Cleanin

g

equipment depreciation .. 16,000 0 0 4,000 20,000

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

50 Managerial Accounting, 16th Edition

Problem 7-20 (continued)

2. The activity rates are computed as follows:

Activity Cost Pool

(a)

Total Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Cleanin

g

carpets .. $161,000 20,000 hundred

$8.05 per hundred

3. The cost for the Flying N Ranch job is computed as follows:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Cleanin

g

carpets .. $8.05 per hundred

5 hundred

$ 40.25

4. The margin earned on the job can be easily computed by using the

costs calculated in part (3) above.

Sales …………………… $140.00

Costs:

g