© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 11

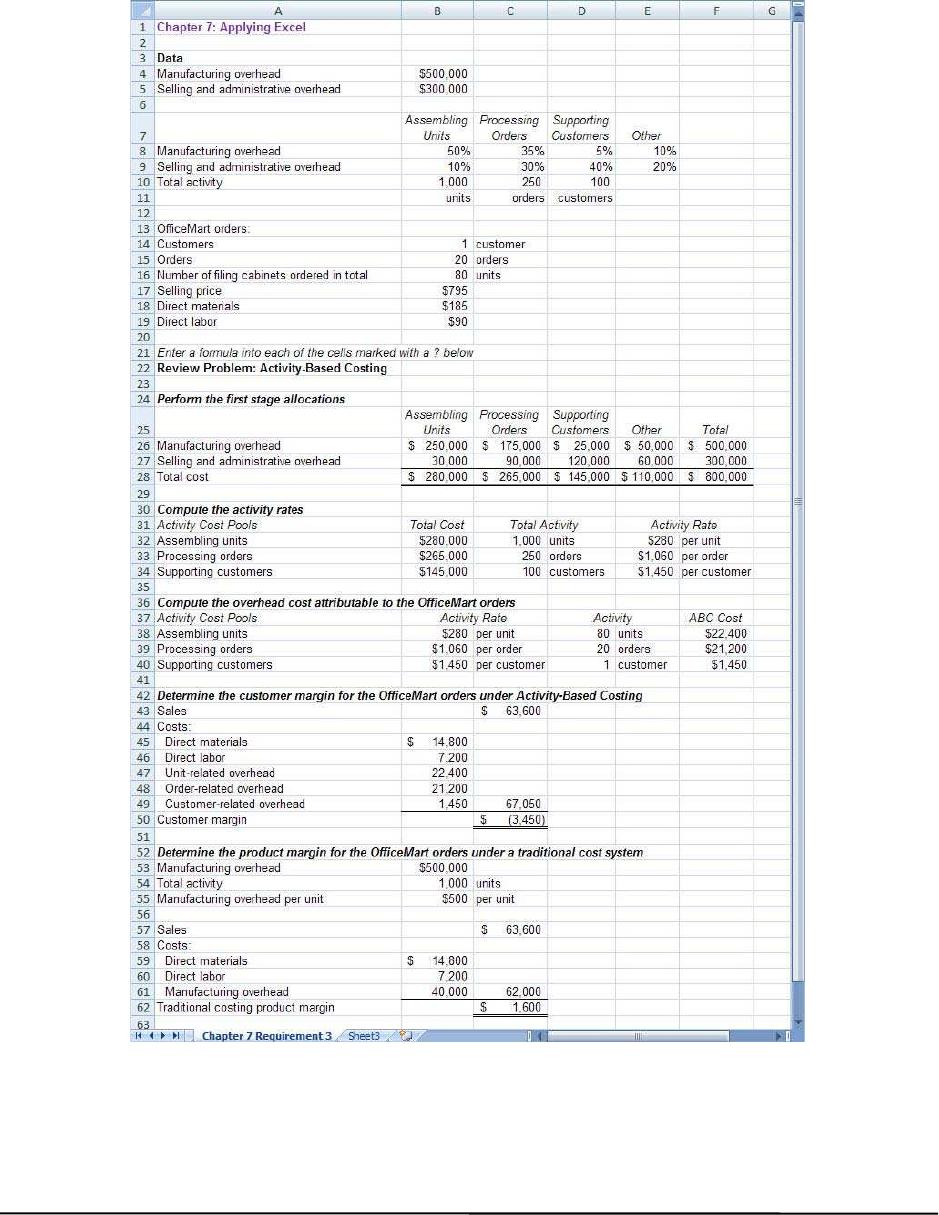

Chapter 7: Applying Excel (continued)

3. With the change in the selling and administrative percentages, the result

is:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

12 Managerial Accounting, 16th Edition

Chapter 7: Applying Excel (continued)

a. The customer margin under activity-based costing has improved from

$(6,600) to $(3,450) because costs have shifted from the order-

related activity cost pool to the customer-related activity cost pool.

The average number of orders per customer is 2.5 (= 250 orders ÷

100 customers). Since in this part we assume that this customer had

b. Shifting selling and administrative costs from the order-related cost

pool to the customer-related cost pool has no effect on product

margins under traditional costing for two reasons. First, selling and

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 13

The Foundational 15

1. The plantwide overhead rate is computed as follows:

T

otal estimated overhead cost (a)………… $684,000

T

2. The overhead cost assignments to Products Y and Z are as follows:

Product Y Product Z

T

otal direct labor hours (a) …………………. 8,000 4,000

3-6.

The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Machinin

g

………….. $200,000 10,000 MH $20 per MH

7. Machine setups is a batch-level activity. A setup is performed to run a

batch of units. The cost of the setup is determined by the resources

8. The product design activity is a product-level activity. The product

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

14 Managerial Accounting, 16th Edition

The Foundational 15 (continued)

9-10. Using the ABC system, the total overhead assigned to Products Y and Z is computed as follows:

Product Y Product Z

Expected

Activity Amount

Expected

Activity Amount

Machinin

g

, at $20.00 per machine-hour …………… 7,000 $140,000 3,000 $ 60,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 15

The Foundational 15 (continued)

11-15. The percentages of overhead assigned using the plantwide and ABC approaches are computed

as follows:

Product

Y

Product

Z

T

ota

l

Plantwide Approach

(a)

Amount

(a) ÷ (c)

%

(b)

Amount

(b) ÷ (c)

%

(c)

Amount

Manufacturin

g

overhead …….. $456,000 66.7% $228,000 33.3% $684,000

A

ctivit

y

–

Based Costin

g

Syste

m

Machinin

g

……………………….. $140,000 70.0% $ 60,000 30.0% $200,000

The Machining allocation percentages used in the ABC system are similar to the plantwide allocation

percentages because the Machining cost pool uses a unit-level activity measure (machine-hours).

Under the ABC system, 25% and 75% of the Machine Setups cost is allocated to Products Y and Z,

respectively, whereas the plantwide approach allocates 67% and 33% of all overhead costs to the

two products. These allocation percentages are different because Machine Setups is a batch-level

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

16 Managerial Accounting, 16th Edition

The Foundational 15 (continued)

Under the ABC system, 50% of the Product Design cost is allocated to each

product, whereas the plantwide approach allocates 67% and 33% of all

overhead costs to Products Y and Z, respectively. These percentages are

different because Product Design is a product-level cost pool. Although

Under the ABC system, the General Factory allocation percentages are the

same as the plantwide allocation percentages because the General Factory

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 17

Exercise 7-1 (10 minutes)

a. Receive raw materials from suppliers. Batch-level

b. Mana

g

e parts inventories. Product-level

c. Do rou

g

h millin

g

work on products. Unit-level

d. Interview and process new employees in the

personnel department.

Or

g

anization-

sustaining

e. Desi

g

n new products. Product-level

g

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

18 Managerial Accounting, 16th Edition

Exercise 7-2 (15 minutes)

Travel

Pickup

and

Delivery

Customer

Service Other Totals

Driver and

g

uard wa

g

es ………………….. $360,000 $252,000 $ 72,000 $ 36,000 $ 720,000

Vehicle operatin

g

expense ……………….. 196,000 14,000 0 70,000 280,000

Vehicle depreciation ……………………….. 72,000 18,000 0 30,000 120,000

Customer representative salaries and

Each entry in the table is derived by multiplying the total cost for the cost category by the percentage

taken from the table below that shows the distribution of resource consumption:

Travel

Pickup

and

Delivery

Customer

Service Other Totals

Driver and

g

uard wa

g

es ………………….. 50% 35% 10% 5% 100%

Vehicle operatin

g

expense ……………….. 70% 5% 0% 25% 100%

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 7 19

Exercise 7-3 (10 minutes)

Activity Cost Pool

Estimated

Overhead

Cost Expected Activity Activity Rate

Carin

g

for lawn …………….…. $72,000 150,000 square ft. of lawn $0.48 per square ft. of lawn

Carin

g

for

g

arden beds

–

low maintenance ……………

$26,400 20,000 square ft. of low

maintenance beds

$1.32 per square ft. of low

maintenance beds

T

g

g

–

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

20 Managerial Accounting, 16th Edition

Exercise 7-4 (10 minutes)

K42

5

A

ctivity Cost Poo

l

A

ctivity Rat

e

A

ctivit

y

A

BC Cos

t

Supportin

g

direct labor ……… $6 per direct labor-hour 80 direct labor-hours $ 480

Machine processin

g

…….……. $4 per machine-hour 100 machine-hours 400

Machine setups ……………….. $50 per setup 1 setups 50

M6

7

A

ctivity Cost Poo

l

A

ctivity Rat

e

A

ctivit

y

A

BC Cos

t

Supportin

g

direct labor ……… $6 per direct labor-hour 500 direct labor-hours $ 3,000

Machine processin

g

…….……. $4 per machine-hour 1,500 machine-hours 6,000

Machine setups ……………….. $50 per setup 4 setups 200