© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 71

Case 6-30 (continued)

Division

Association

Total Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Sales:

Membership dues …………………….. $2,000,000 $1,600,000 $400,000

Non-member ma

g

azine

subscriptions ………………………… 75,000 75,000

Expenses traceable to se

g

ments:

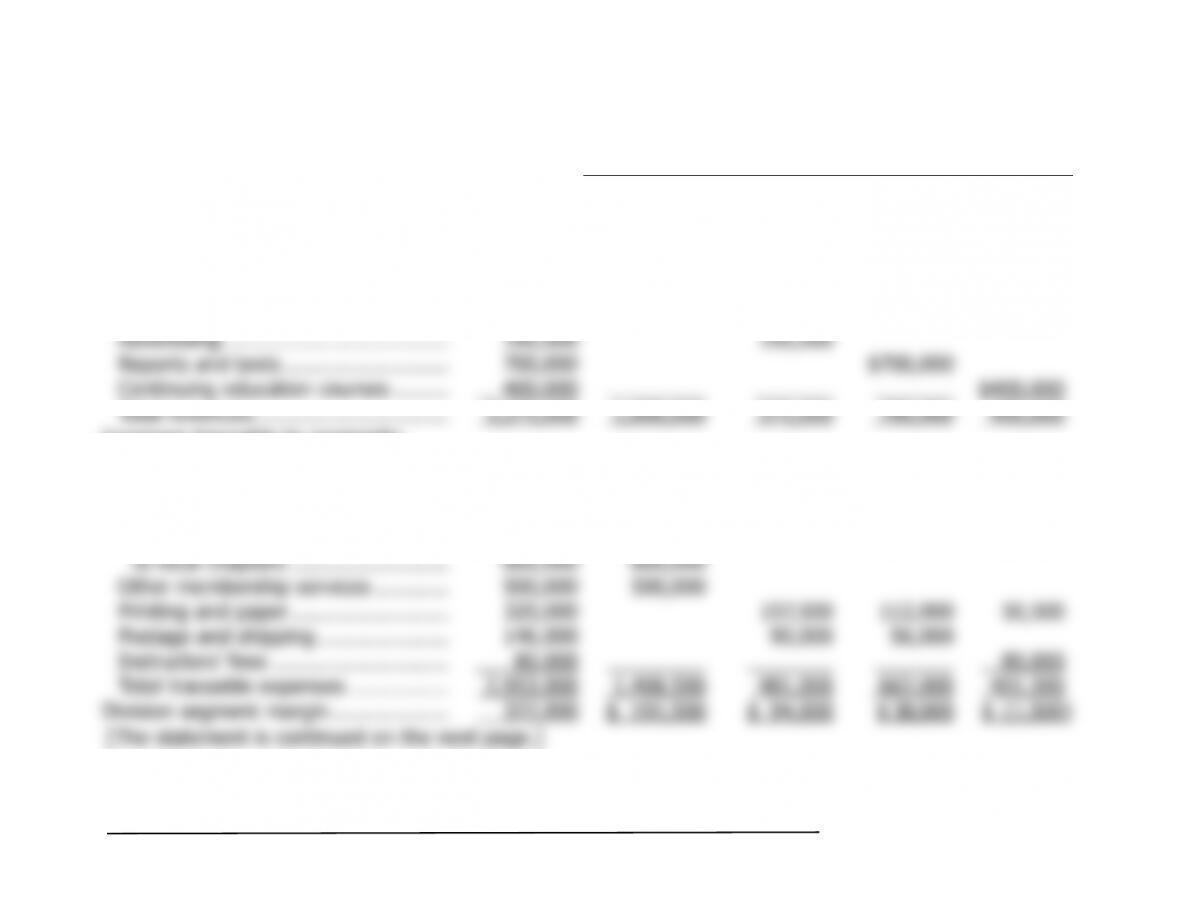

Salaries ………………………………….. 840,000 210,000 150,000 300,000 180,000

Personnel costs ……………………….. 210,000 52,500 37,500 75,000 45,000

Occupancy costs ………………………. 257,000 46,000 46,000 119,000 46,000

Reimbursement of member costs

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

72 Managerial Accounting, 16th Edition

Case 6-30 (continued)

[Continuation of the segmented income statement.]

Division

Association

Total Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Division se

g

ment mar

g

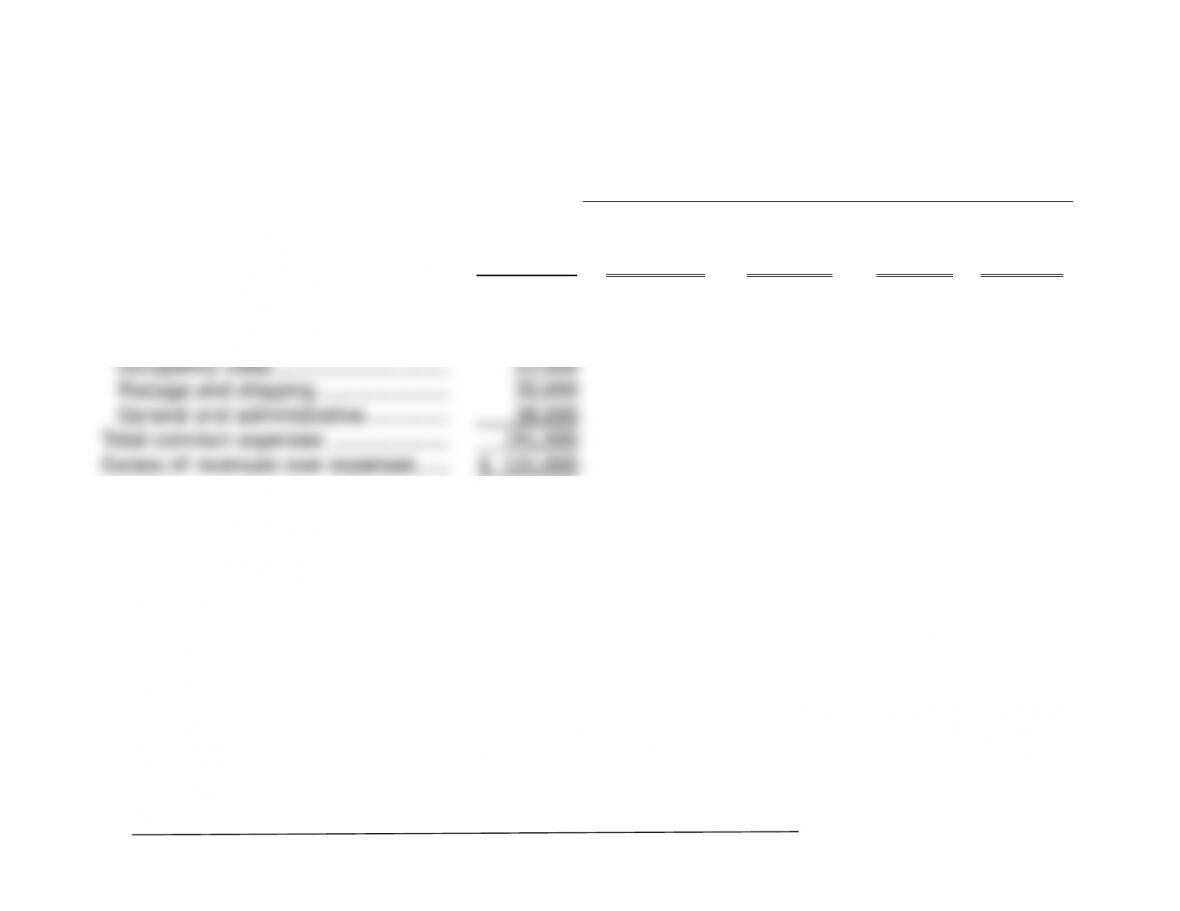

in ………………. 322,000 $ 191,500 $94,000 $3

8

,000 $ (1,500)

Common expenses not traceable to divisions:

Salaries

—

corporate staff ……………. 80,000

Personnel costs ……………………….. 20,000

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 6A 73

Case 6-30 (continued)

2. While we do not favor the allocation of common costs to segments, the

most common reason given for this practice is that segment managers

Arguments against allocation of all costs:

• Allocation bases will need to be chosen arbitrarily because no cause-

• Management may be misled into eliminating a profitable segment

• Segment managers usually have little control over common costs.

• Allocations of common costs undermine the credibility of performance

Appendix 6A

Super-Variable Costing

Exercise 6A-1 (10 minutes)

1. a. The unit product cost under super-variable costing would include

b. The super-variable costing income statement would be:

Sales (20,000 units × $50 per unit)……….. $1,000,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 6A 75

Exercise 6A-2 (20 minutes)

1. a. The unit product cost under super-variable costing would include

b. The super-variable costing income statement would be:

Sales (52,000 units × $40 per unit)……….. $2,080,000

V

ariable cost of

g

oods sold

2. a. The unit product cost under variable costing would be:

Direct materials …………………………………………………… $13.00

b. The variable costing income statement would be:

Sales (52,000 units × $40 per unit)……….. $2,080,000

V

ariable cost of

g

oods sold

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

76 Managerial Accounting, 16th Edition

Exercise 6A-2 (continued)

3. The difference between the super-variable costing and variable costing

net operating incomes is explained as follows:

Units in ending inventory = Units in beginning inventory + Units

Direct labor cost deferred in (released from) inventory = Direct labor

Super-variable costin

g

net operatin

g

income ……….……. $124,000

A

dd direct labor cost deferred in inventory under

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 6A 77

Exercise 6A-3 (20 minutes)

1. a. Under super-variable costing, the unit product cost for both years

1. b.

Year 1 Year 2

Sales (@ $50 per unit) ………………………….. $2,000,000 $3,000,000

V

ariable cost of

g

oods sold (@ $12 per unit) 480,000 720,000

Contribution mar

g

in …………………………….. 1,520,000 2,280,000

Fixed expenses:

T

2. a. The unit product costs under variable costing:

Y

ear

1

Y

ear

2

V