© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 51

Problem 6-23 (continued)

b. The absorption costing income statement would be constructed as

follows:

The absorption costing unit product cost will remain at $26.50, the

same as in part (1).

Sales (32,000 units × $40 per unit)…………………….. $1,280,000

c. The reconciliation of variable costing and absorption costing income

is:

Units in ending inventory = Units in beginning inventory + Units

Manufacturing overhead deferred in (released from) inventory = Fixed

manufacturing overhead in ending inventory – Fixed manufacturing

V

ariable costin

g

net operatin

g

income ……………….. $ 60,000

A

Deduct fixed manufacturin

g

overhead cost released

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

52 Managerial Accounting, 16th Edition

Problem 6-24 (45 minutes)

1. The intern’s decision to use the absorption format for her segmented

income statements is a bad idea because it does not focus on cost

2.a. To answer this question, students must understand that cost of goods

sold for a merchandiser is a variable cost. Thus, all of the company’s

T

ota

l

Commercia

l

Residentia

l

T

otal sellin

g

and administrative

expense (a) ……………………… $240,000 $104,000 $136,000

T

raceable fixed expenses ………… $ 93,000 $55,000 $38,000

Sales commissions

–

2.b. The amount of common fixed expenses allocated to Residential

($48,000) is twice as much as the amount of common fixed expenses

allocated to Commercial ($24,000). Because the Residential sales

3. No. Allocating common fixed expenses is a bad idea because these

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 53

Problem 6-24 (continued)

4. The contribution format segmented income statements would appear as

follows:

T

ota

l

Company Commercial Residential

Sales ……………………………… $750,000 $250,000 $500,000

V

ariable expenses:

Cost of

g

oods sold …………. 500,000 140,000 360,000

Sales commissions (10%) … 75,000 25,000 50,000

T

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

54 Managerial Accounting, 16th Edition

Problem 6-24 (continued)

5. The companywide break-even point is computed as follows:

Dollar sales for company

to break even = Traceable fixed expenses + Common fixed expenses

Overall CM ratio

=

$93,000 + $72,000

6. The break-even point for the Commercial Division is computed as follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 55

Problem 6-24 (continued)

The break-even point for the Residential Division is computed as follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

7. The new break-even point for the Commercial Division is computed as

follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

The new break-even point for the Residential Division is computed as

follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

56 Managerial Accounting, 16th Edition

Problem 6-25 (75 minutes)

1.

Year 1 Year 2 Year 3

Sales …………………………………… $800,000 $ 640,000 $800,000

V

ariable expenses:

Variable cost of

g

oods sold

@ $2 per unit …………………… 100,000 80,000 100,000

Variable sellin

g

and

administrative expenses

T

)

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 57

Problem 6-25 (continued)

2.a.

Year 1 Year 2 Year 3

V

ariable manufacturin

g

cost ……………. $ 2.00 $ 2.00 $ 2.00

Fixed manufacturin

g

cost:

$480,000 ÷ 50,000 units ……………… 9.60

b.Units in be

g

innin

g

inventory ……………. 0 0 20,000

+ Units produced …………………………. 50,000 60,000 40,000

− Units sold ………………………………… 50,000 40,000 50,000

= Units in endin

g

inventory …………….. 0 20,000 10,000

g

Fixed manufacturin

g

overhead in

V

A

A

3. Production went up sharply in Year 2, thereby reducing the unit product

cost, as shown in (2a) above. This reduction in cost per unit, combined

4. The fixed manufacturing overhead deferred in inventory from Year 2

was charged against Year 3 operations. This added charge against Year

3 operations was offset somewhat by the fact that part of Year 3’s fixed

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

58 Managerial Accounting, 16th Edition

Problem 6-25 (continued)

5. a. With lean production, production would have been tied to sales in

b. If lean production had been in use, the net operating income under

absorption costing would have been the same as under variable

costing in all three years. With production tied to sales, there would

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 59

Problem 6-26 (60 minutes)

1. The weaknesses of the company’s version of a segmented income

statement are as follows:

a. The company should include a column showing the combined results

b. The regional expenses should be segregated into variable and fixed

c. The corporate expenses are probably common to the regions and

2. Corporate advertising expenses have been allocated on the basis of

sales dollars; the general administrative expenses have been allocated

evenly among the three regions. Such allocations can be misleading to

management because they seem to imply that these expenses are

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

60 Managerial Accounting, 16th Edition

Problem 6-26 (continued)

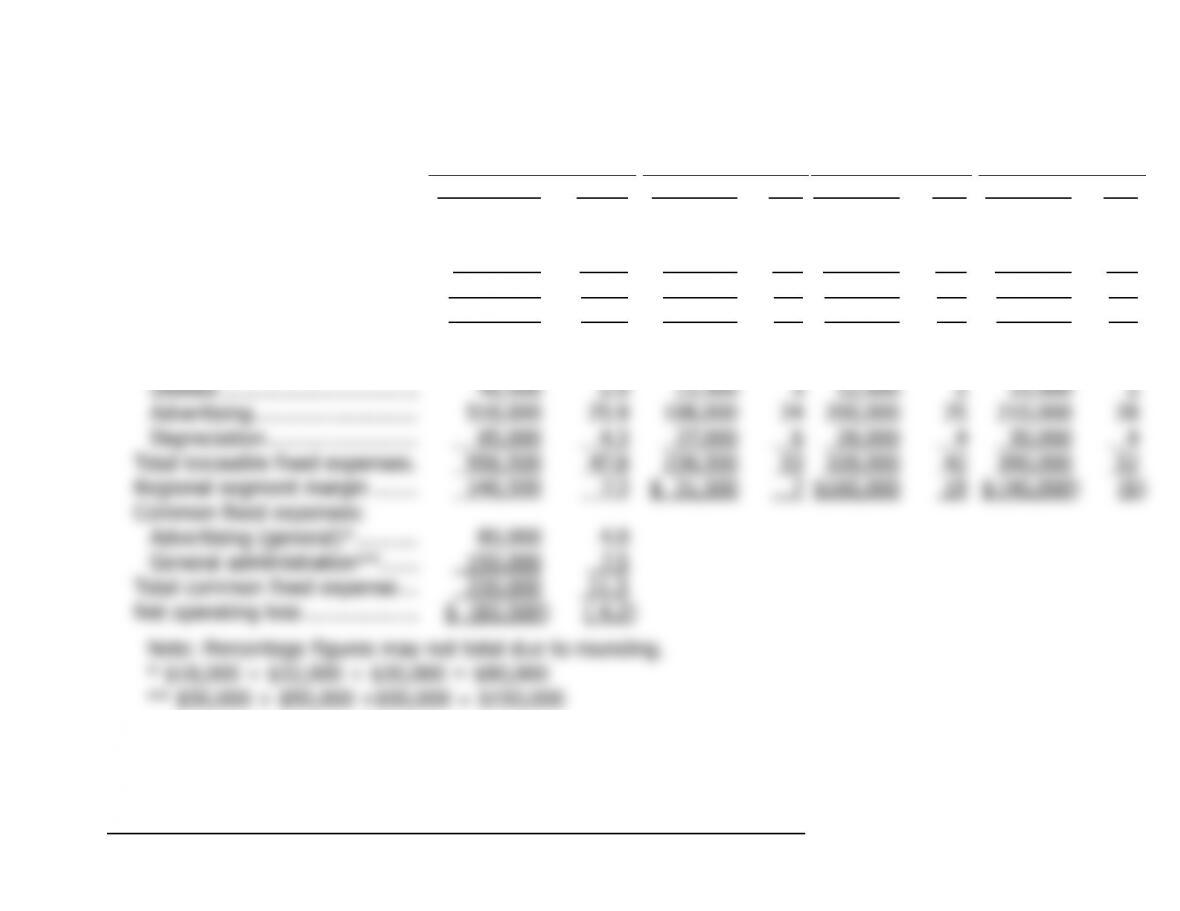

3.

Total Company West Central East

Sales ………………………………. $2,000,000 100.0 $450,000 100 $800,000 100 $750,000 100

V

ariable expenses:

Cost of

g

oods sold …………… 819,400 41.0 162,900 36 280,000 35 376,500 50

Shippin

g

expense ……………. 77,600 3.9 17,100 4 32,000 4 28,500 4

T

otal variable expenses ……….. 897,000 44.9 180,000 40 312,000 39 405,000 54

Contribution mar

g

in …………… 1,103,000 55.1 270,000 60 488,000 61 345,000 46

T

raceable fixed expenses:

Salaries …………………………. 313,000 15.6 90,000 20 88,000 11 135,000 18

T

A

T

A