© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 41

Problem 6-19 (30 minutes)

1. The unit product cost under variable costing is computed as follows:

Direct materials ……………………. $ 4

V

2. With this figure, the variable costing income statements can be

prepared:

Year 1 Year 2

Sales (@ $25 per unit) ………………………….. $1,000,000 $1,250,000

V

ariable expenses:

Variable cost of

g

oods sold

(@ $12 per unit) …………………………….. 480,000 600,000

Variable sellin

g

and administrative

T

T

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

42 Managerial Accounting, 16th Edition

Problem 6-19 (continued)

3. The reconciliation of absorption and variable costing follows:

Y

ear

1

Y

ear

2

Units in be

g

innin

g

inventory…………………… 0 5,000

Y

ear

1

Y

ear

2

Fixed manufacturin

g

overhead in endin

g

inventory (5,000 units × $6 per unit) …….. $30,000 $ 0

Deduct: Fixed manufacturin

g

overhead in

Y

ear

1

Y

ear

2

V

ariable costin

g

net operatin

g

income (loss). $40,000 $150,000

A

dd: Fixed manufacturin

g

overhead cost

deferred in inventory under absorption

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 43

Problem 6-20 (45 minutes)

1. a. The unit product cost under absorption costing is:

Direct materials …………………………….. $20

Direct labor ………………………………….. 8

b. The absorption costing income statement is:

Sales (8,000 units × $75 per unit)…………….………. $600,000

Cost of

g

oods sold (8,000 units × $40 per unit) …… 320,000

2. a. The unit product cost under variable costing is:

Direct materials ………………………. $20

V

V

b. The variable costing income statement is:

Sales (8,000 units × $75 per unit) ……………… $600,000

V

ariable expenses:

Variable cost of

g

oods sold

(8,000 units × $30 per unit) …………………. $240,000

Variable sellin

g

expenses

V

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

44 Managerial Accounting, 16th Edition

Problem 6-20 (continued)

3. The difference in the ending inventory relates to a difference in the

handling of fixed manufacturing overhead costs. Under variable costing,

these costs have been expensed in full as period costs. Under

absorption costing, these costs have been added to units of product at

A

dded to the endin

g

inventory

(2,000 units × $10 per unit) …………………………….…. $ 20,000

Expensed as part of cost of

g

oods sold

T

Because $20,000 of fixed manufacturing overhead cost has been

deferred in inventory under absorption costing, the net operating

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 45

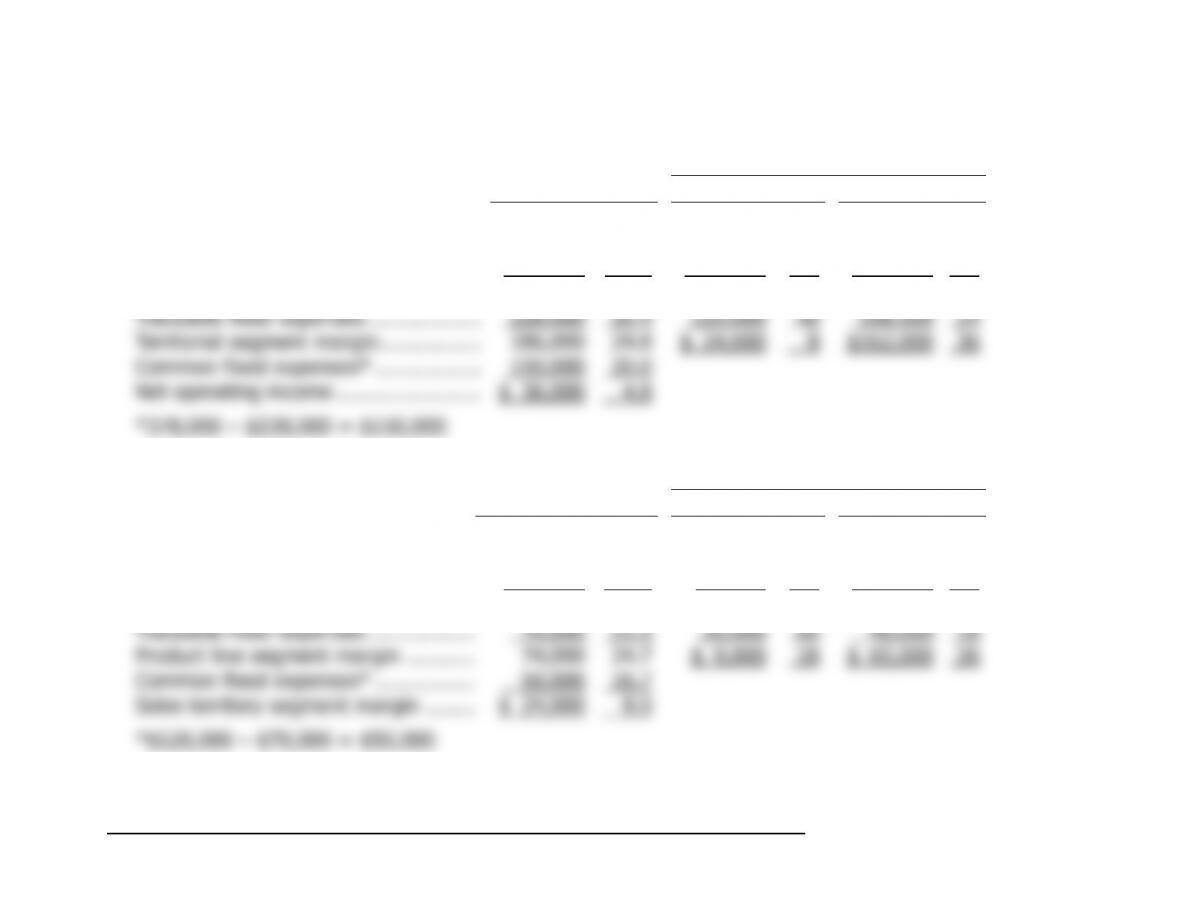

Problem 6-21 (30 minutes)

1.

Sales Territory

Total Company Northern Southern

Amount % Amount % Amount %

Sales ……………………………………….. $750,000 100.0 $300,000 100 $450,000 100

V

ariable expenses ………………………. 336,000 44.8 156,000 52 180,000 40

Contribution mar

g

in ……………………. 414,000 55.2 144,000 48 270,000 60

–

Product Line

Northern Territory Paks Tibs

Amount % Amount % Amount %

Sales ………………………………………. $300,000 100.0 $50,000 100 $250,000 100

V

ariable expenses ……………………… 156,000 52.0 11,000 22 145,000 58

Contribution mar

g

in …………………… 144,000 48.0 39,000 78 105,000 42

T

g

–

T

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

46 Managerial Accounting, 16th Edition

Problem 6-21 (continued)

2. Two insights should be brought to the attention of management. First,

compared to the Southern territory, the Northern territory has a low

3. Again, two insights should be brought to the attention of management.

First, the Northern territory has a poor sales mix. Note that the territory

sells very little of the Paks product, which has a high contribution margin

ratio. This poor sales mix accounts for the low overall contribution

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 47

Problem 6-22 (45 minutes)

1. a. and b.

Absorption

Costing

Variable

Costing

Direct materials …………………………….. $ 7 $ 7

Direct labor ………………………………….. 10 10

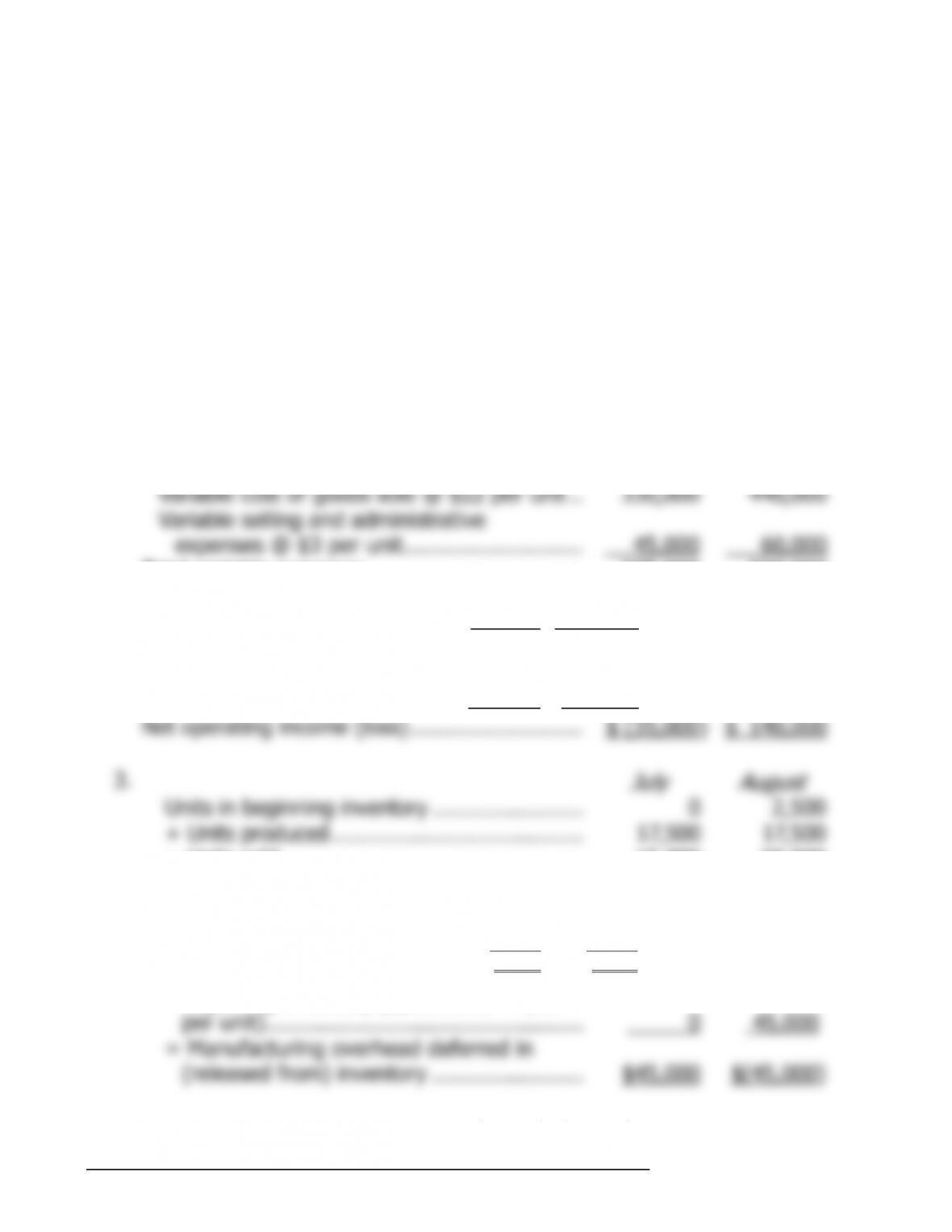

2.

July August

Sales ………………………………………………….. $900,000 $1,200,000

V

ariable expenses:

Variable cost of

g

oods sold @ $22 per unit .. 330,000 440,000

Variable sellin

g

and administrative

expenses @ $3 per unit ……………………… 45,000 60,000

T

g

T

3.

July August

Units in be

g

innin

g

inventor

y

…………………… 0 2,500

+ Units produced …………………………………. 17,500 17,500

− Units sold ………………..………………………. 15,000 20,000

= Units in endin

g

inventor

y

……………………. 2,500 0

Fixed manufacturin

g

overhead in endin

g

g

V

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

48 Managerial Accounting, 16th Edition

Problem 6-22 (continued)

July August

Variable costin

g

net operatin

g

income

(loss) ………………………………………………. $ (35,000) $ 140,000

A

dd fixed manufacturin

g

overhead cost

4. As shown in the reconciliation in part (3) above, $45,000 of fixed

manufacturing overhead cost was deferred in inventory under

absorption costing at the end of July because $18 of fixed

manufacturing overhead cost “attached” to each of the 2,500 unsold

units that went into inventory at the end of that month. This $45,000

was part of the $560,000 total fixed cost that has to be covered each

month in order for the company to break even. Because the $45,000

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 49

Problem 6-23 (60 minutes)

1. a. Absorption costing unit product cost is:

Direct materials …………………………… $ 3.50

Direct labor ………………………………… 12.00

b. The absorption costing income statement is:

Sales (28,000 units × $40 per unit) …………………… $1,120,000

Cost of

g

oods sold (28,000 units × $26.50 per unit) 742,000

c. The reconciliation is as follows:

Units in ending inventory = Units in beginning inventory + Units

Manufacturing overhead deferred in (released from) inventory = Fixed

manufacturing overhead in ending inventory – Fixed manufacturing

V

ariable costin

g

net loss …………………………………. $(10,000)

A

A

dd fixed manufacturin

g

overhead cost deferred in

V

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

50 Managerial Accounting, 16th Edition

Problem 6-23 (continued)

2. Under absorption costing, the company did earn a profit for the quarter.

However, before the question can really be answered, one must first

define what is meant by a “profit.” The central issue here relates to

timing

of release of fixed manufacturing overhead costs to expense.

Advocates of absorption costing would argue, however, that fixed

manufacturing overhead costs attach to units of product as they are

produced, and that such costs do not become an expense until the units

are sold. Therefore, if the selling price of a unit is greater than the unit

product cost (including a proportionate amount of fixed manufacturing

overhead), then a profit is earned even if some units produced are

3. a. The variable costing income statement is:

Sales (32,000 units × $40 per unit) ……….. $1,280,000

V

ariable expenses:

Variable cost of

g

oods sold

[32,000 units × ($3.50 + $12.00 +

$1.00) per unit] ……………………………. $528,000

Variable sellin

g

and administrative