© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 31

Exercise 6-13 (20 minutes)

1. The company is using variable costing. The computations are:

Variable

Costing

Absorption

Costing

Direct materials …………………….. $ 9 $ 9

Direct labor ………………………….. 10 10

2. a. No, $72,000 is not the correct figure to use because variable costing

b. The Finished Goods inventory account should be stated at $90,000,

which represents the absorption cost of the 3,000 unsold units. Thus,

the account should be increased by $18,000 for external reporting

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

32 Managerial Accounting, 16th Edition

Exercise 6-14 (30 minutes)

1. Under variable costing, only the variable manufacturing costs are

included in product costs.

Direct materials ……………………… $ 50

Direct labor …………………………… 80

2. The variable costing income statement appears below:

Sales (19,000 units × $210 per unit) …………. $3,990,000

V

ariable expenses:

Variable cost of

g

oods sold (19,000 units ×

$150 per unit) ………………………………….. $2,850,000

)

3. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

Sellin

g

price per unit ………….. $210

V

ariable cost per unit …………. 160

V

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 33

Exercise 6-15 (20 minutes)

1. Under absorption costing, all manufacturing costs (variable and fixed)

are included in product costs.

Direct materials ……………………………………. $ 50

2. The absorption costing income statement appears below:

Sales (19,000 units × $210 per unit) …………………. $3,990,000

Cost of

g

oods sold (19,000 units × $185 per unit) … 3,515,000

Gross mar

g

in ……………………………………………….. 475,000

Sellin

g

and administrative expenses

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

34 Managerial Accounting, 16th Edition

Exercise 6-16 (20 minutes)

1. The companywide break-even point is computed as follows:

Dollar sales for company

to break even = Traceable fixed expenses + Common fixed expenses

Overall CM ratio

The break-even point for the Chicago office is computed as follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 35

Exercise 6-16 (continued)

The break-even point for the Minneapolis office is computed as follows:

Dollar sales for a

segment to break even = Segment traceable fixed expenses

Segment CM ratio

2. $75,000 × 40% CM ratio = $30,000 increased contribution margin in

Minneapolis. Because the fixed costs in the office and in the company as

It is not correct to multiply the $75,000 increase in sales by Minneapolis’

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

36 Managerial Accounting, 16th Edition

Exercise 6-16 (continued)

3. a. The segmented income statement follows:

Segments

Total Company Chicago

Minneapolis

Amount % Amount % Amount %

Sales ……………………. $500,000 100.0 $200,000 100 $300,000 100

V

ariable expenses ……. 240,000 48.0 60,000 30 180,000 60

Contribution mar

g

in …. 260,000 52.0 140,000 70 120,000 40

T

raceable fixed

b. The segment margin ratio rises and falls as sales rise and fall due to

In contrast to the segment ratio, the contribution margin ratio for a

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 37

Exercise 6-17 (15 minutes)

1. and 2. The profit impacts in both markets are as follows:

Medical Dental

Increased sales ……………………………..……… $40,000 $35,000

Market CM ratio ……………………………………. × 36% × 48%

4. The $48,000 in traceable fixed expenses for Minneapolis in the previous

exercise is now partly traceable and partly common. When we segment

Minneapolis by market, only $33,000 remains a traceable fixed expense.

This amount represents costs such as advertising and salaries of

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

38 Managerial Accounting, 16th Edition

Problem 6-18 (45 minutes)

1. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

Break-even unit sales = Fixed expenses ÷ Unit contribution margin

2. a. Under variable costing, only the variable manufacturing costs are

included in product costs.

Y

ear

1

Y

ear

2

Y

ear

3

Direct materials ……………………………… $20 $20 $20

Direct labor …………………………………… 12 12 12

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 39

Problem 6-18 (continued)

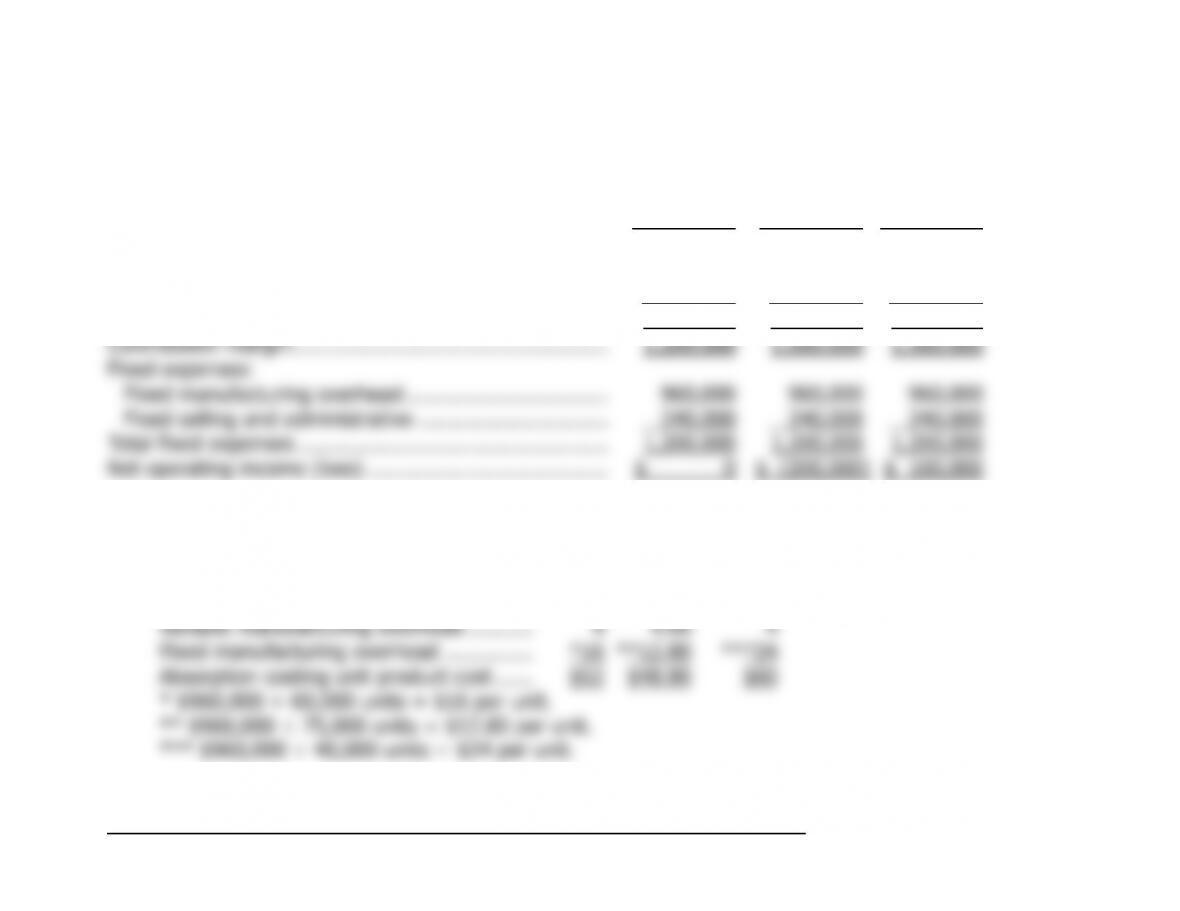

2. b. The variable costing income statements appear below:

Y

ear

1

Y

ear

2

Y

ear

3

Sales (@ $58 per unit) ………………………………………. $3,480,000 $2,900,000 $3,770,000

V

ariable expenses:

Variable cost of

g

oods sold @ $36 per unit ………….. 2,160,000 1,800,000 2,340,000

Variable sellin

g

and administrative @ $2 per unit…… 120,000 100,000 130,000

T

otal variable expenses ………………………………….….. 2,280,000 1,900,000 2,470,000

T

3. a. The unit product costs under absorption costing:

Y

ear

1

Y

ear

2

Y

ear

3

Direct materials ……………………………… $20 $20.00 $20

Direct labor …………………………………… 12 12.00 12

V

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

40 Managerial Accounting, 16th Edition

Problem 6-18 (continued)

3. b. The absorption costing income statements appears below:

Y

ear

1

Y

ear

2

Y

ear

3

Sales ……………………………………………. $3,480,000 $2,900,000 $3,770,000

Cost of

g

oods sold …………………………… 3,120,000 2,440,000 3,620,000

Gross mar

g

in ………………………………….. 360,000 460,000 150,000

Sellin

g

and administrative expenses

4.

Y

ear

1

Y

ear

2

Y

ear

3

Units sold …………………………………………….……. 60,000 50,000 65,000

Break-even point in units ………………………………. 60,000 60,000 60,000

The absorption costing net operating incomes in years 2 and 3 are counterintuitive. In year 2, the

number of units sold is below the break-even point; however, absorption costing reports a net