© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 1

Chapter 6

Variable Costing and Segment Reporting:

Tools for Management

Solutions to Questions

6-1 Absorption and variable costing differ in

how they handle fixed manufacturing overhead.

Under absorption costing, fixed manufacturing

manufacturing overhead costs are included in

product costs, along with direct materials, direct

labor, and variable manufacturing overhead. If

some of the units are not sold by the end of the

costs with revenues than variable costing. They

argue that all manufacturing costs must be

6-5 Advocates of variable costing argue that

one say that these costs are part of the costs of

the products? These costs are incurred to have

the capacity to make products during a

particular period and should be charged against

absorption and variable costing. When

6-7 If production exceeds sales, absorption

costing will usually show higher net operating

income than variable costing. When production

6-8 If fixed manufacturing overhead cost is

the level of production without any increase in

sales. If production exceeds sales, units of

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

2 Managerial Accounting, 16th Edition

6-10 Differences in reported net operating

income between absorption and variable costing

arise because of changing levels of inventory. In

Lean Production, goods are produced strictly to

6-11 A segment is any part or activity of an

organization about which a manager seeks cost,

6-13 A traceable fixed cost of a segment is a

cost that arises specifically because of the

existence of that segment. If the segment were

eliminated, the cost would disappear. A common

costs of a department would include the salary

of the department’s supervisor and depreciation

of machines used exclusively by the department.

Examples of common fixed costs would include

building, corporate image advertising, and

6-14 The contribution margin is the difference

between sales revenue and variable expenses.

The segment margin is the amount remaining

after deducting traceable fixed expenses from

6-15 If common fixed costs were allocated to

segments, then the costs of segments would be

overstated and their margins would be

6-16 There are often limits to how far down

an organization a cost can be traced. Therefore,

fixed costs that are traceable to a segment may

become common as that segment is divided into

6-17 No, a company should not allocate its

common fixed costs to business segments.

These costs are not traceable to individual

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 3

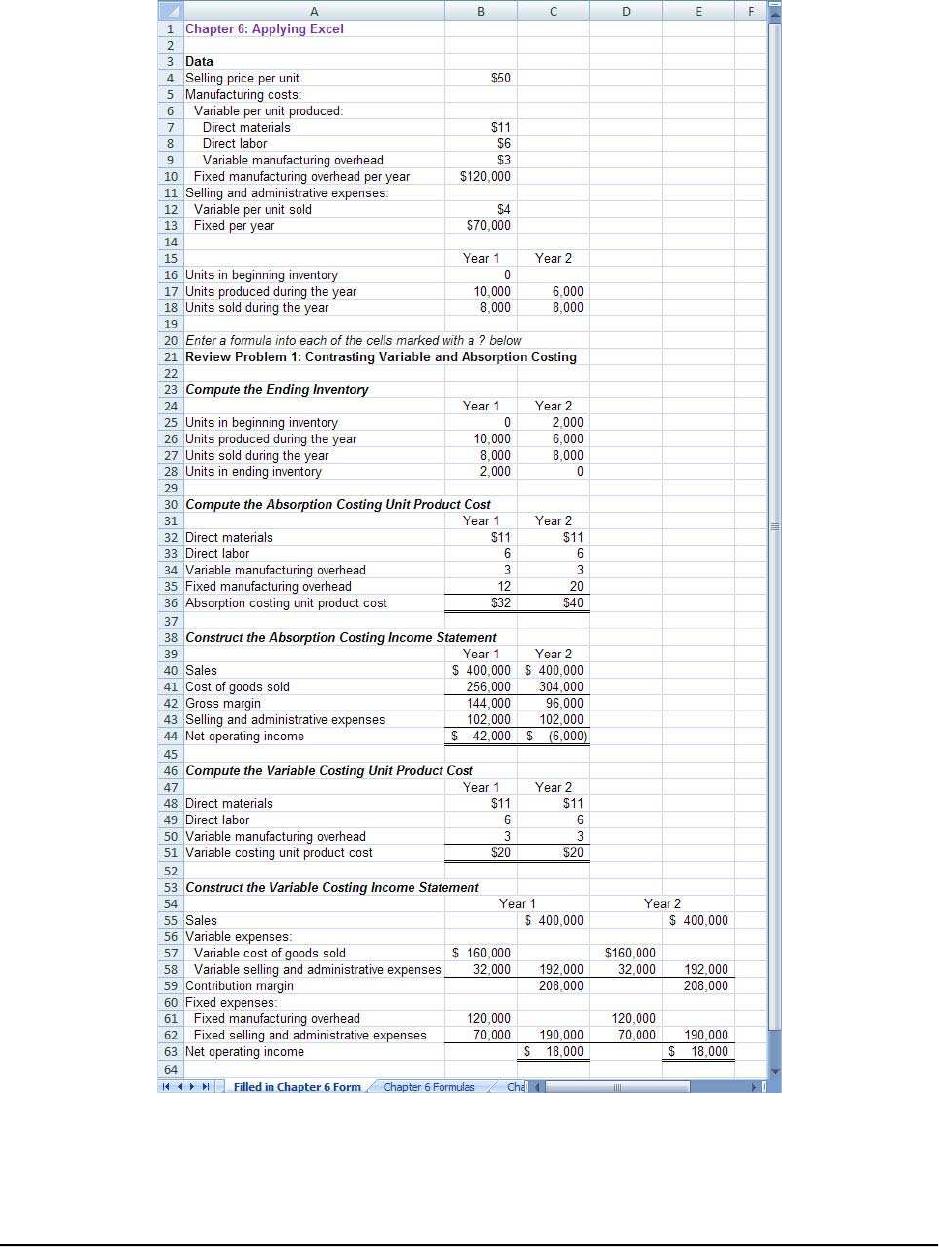

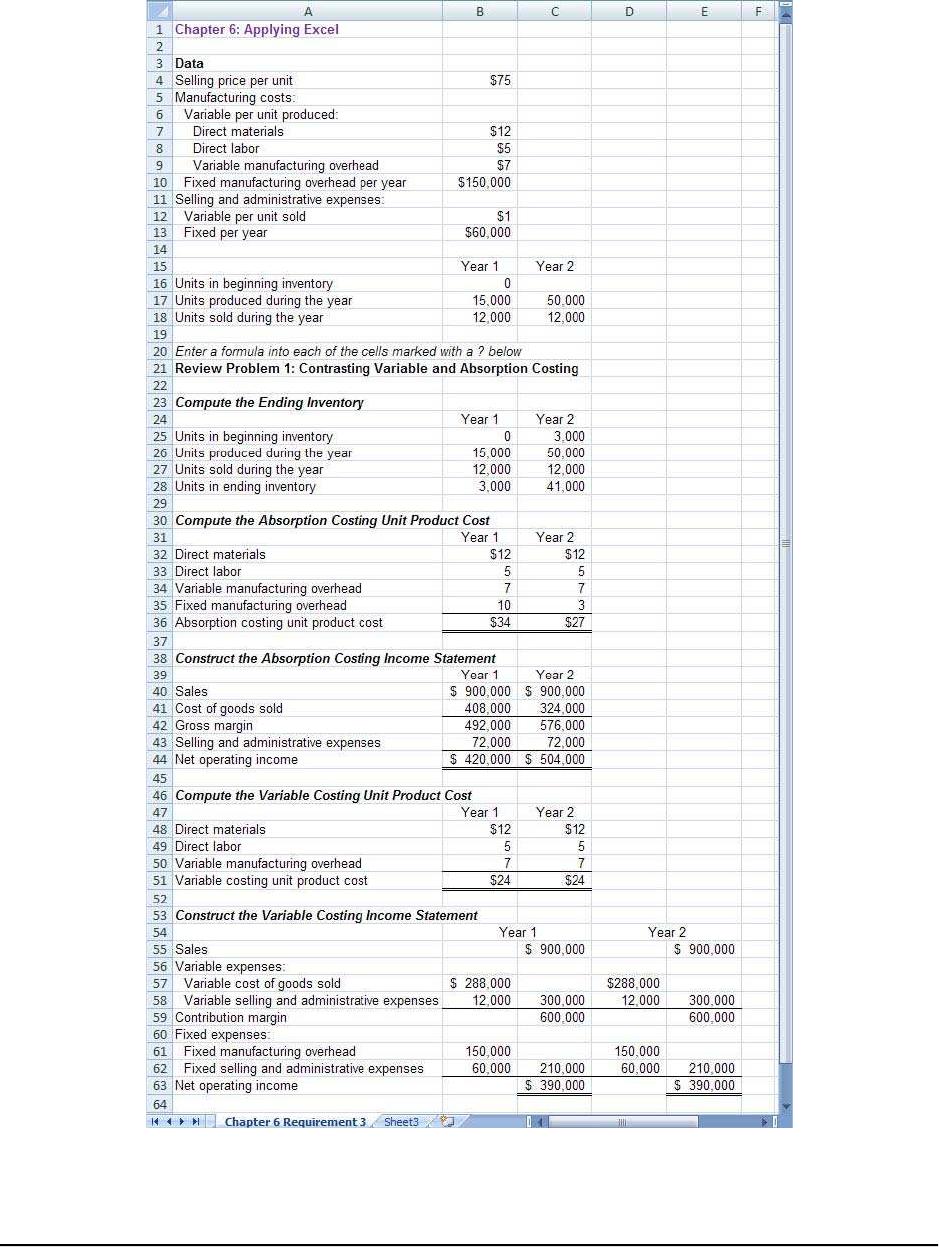

Chapter 6: Applying Excel

The completed worksheet is shown below.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

4 Managerial Accounting, 16th Edition

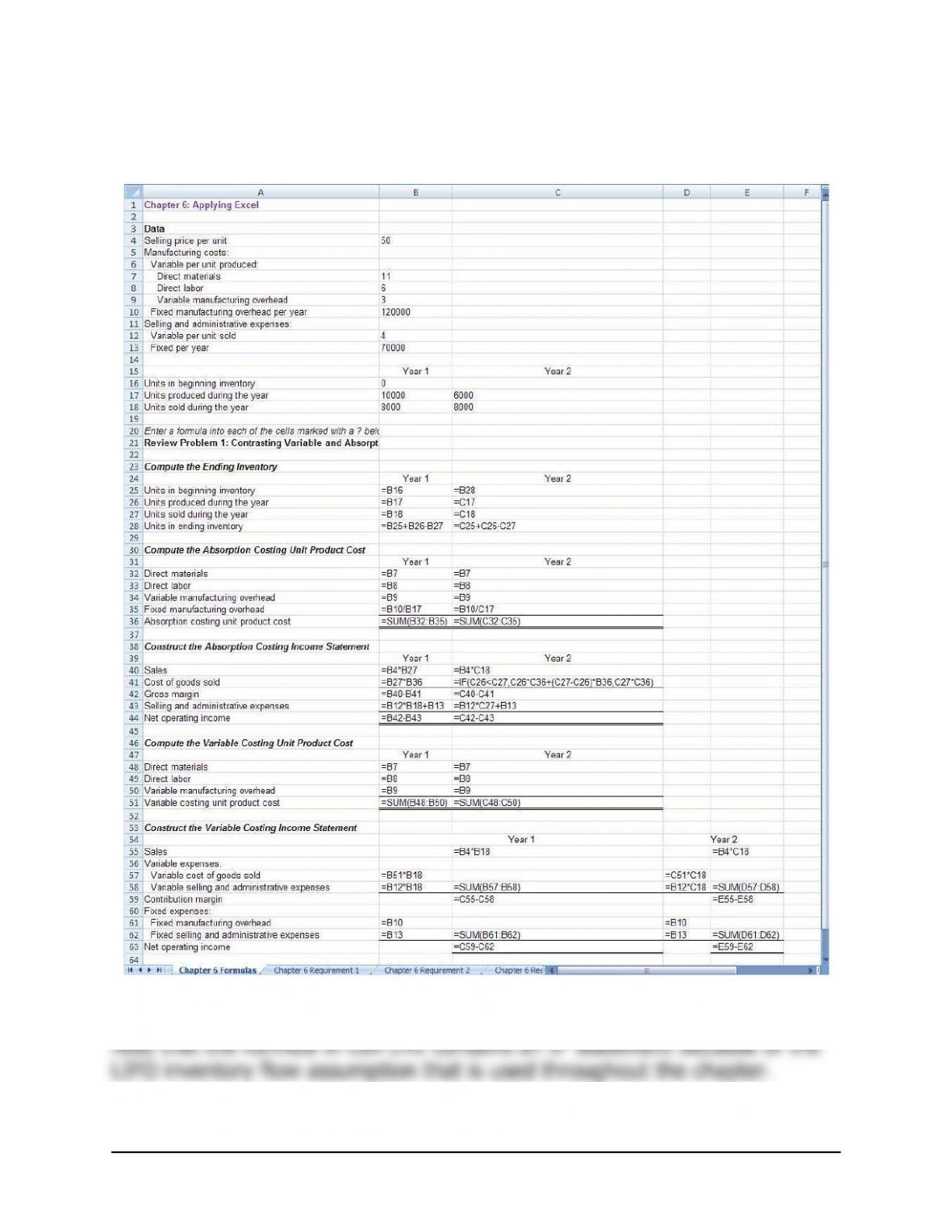

Chapter 6: Applying Excel (continued)

The completed worksheet, with formulas displayed, is shown below.

Note: This worksheet assumes that the beginning inventory in Year 1 is

zero. If this were not true, the worksheet would have to be modified. Also

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 5

Chapter 6: Applying Excel (continued)

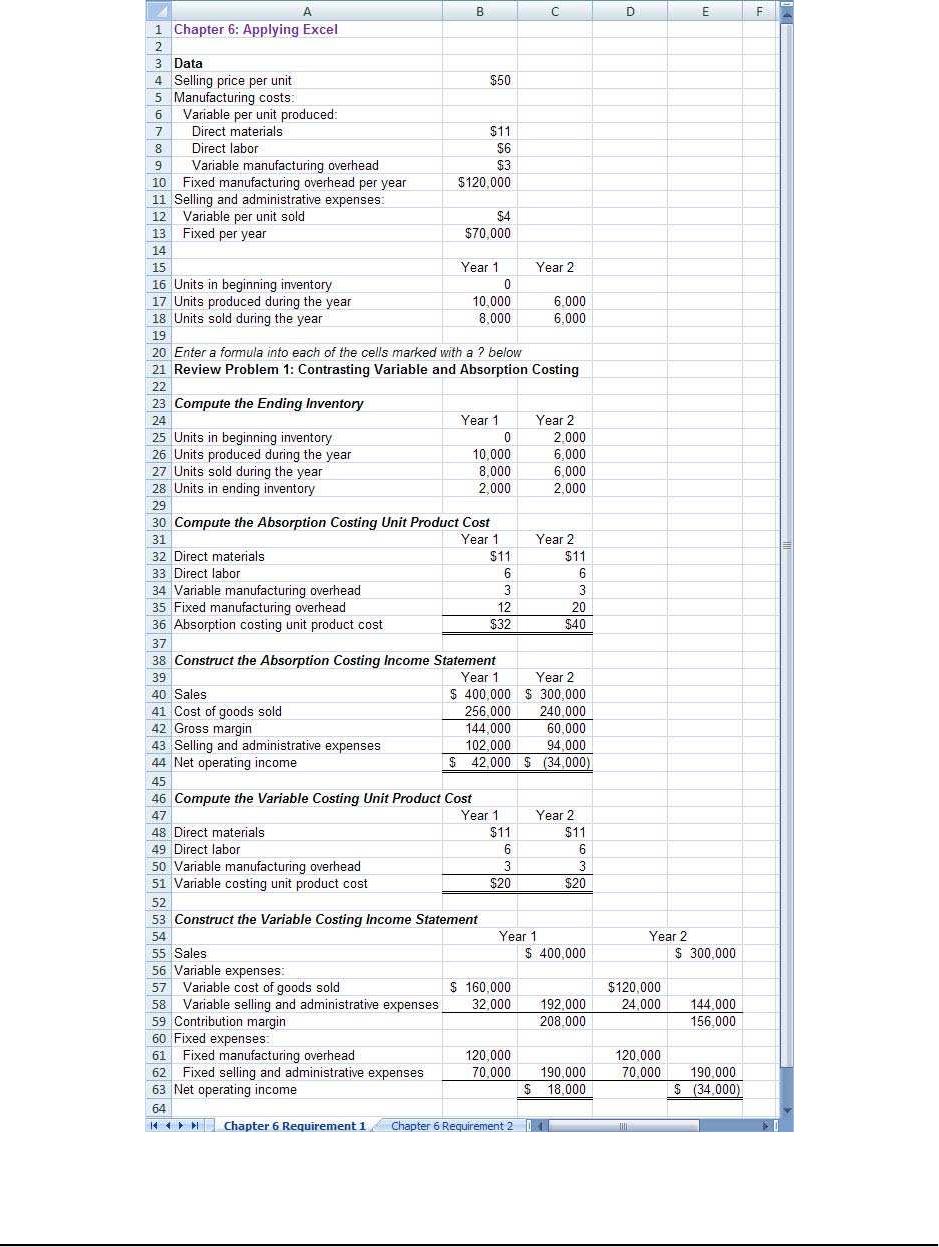

1. When the units sold in Year 2 are changed to 6,000, the result is:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

6 Managerial Accounting, 16th Edition

Chapter 6: Applying Excel (continued)

If the units produced equals the units sold, under the LIFO assumption,

all of the fixed manufacturing overhead from Year 2 flows to the income

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 7

Chapter 6: Applying Excel (continued)

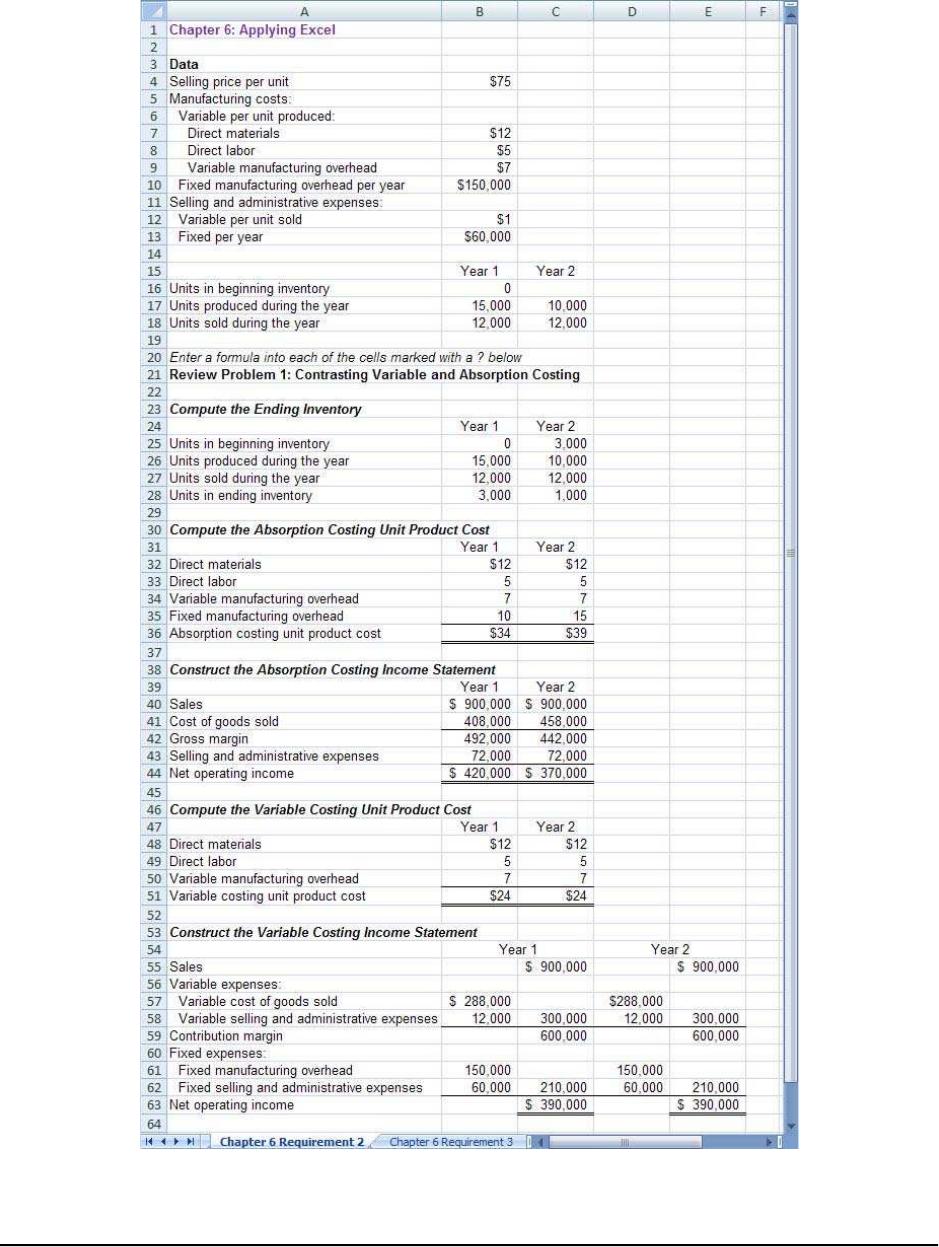

2. With the changes in the data, the worksheet should look like this:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

8 Managerial Accounting, 16th Edition

Chapter 6: Applying Excel (continued)

The variable costing net operating income is the same in Year 1 and

Year 2 because the sales are the same in the two years—12,000 units.

Absorption costing net operating income exceeds variable costing net

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 6 9

Chapter 6: Applying Excel (continued)

3. With the increase in units produced in Year 2, the result is:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

10 Managerial Accounting, 16th Edition

Chapter 6: Applying Excel (continued)

Increasing the production in Year 2 to 50,000 units while keeping

everything else the same—including the unit sales—would result in

absorption costing net operating income of $504,000 and payment of

the bonus. However, it would also result in huge ending inventories that

exceed the normal sales by several times. These huge inventories are