© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 71

Problem 5-29 (continued)

3. The major factor would be the sensitivity of the company’s operations to

cyclical movements in the economy. Because the new equipment will

increase the CM ratio, in years of strong economic activity, the company

will be better off with the new equipment. However, in economic

4. No information is given in the problem concerning the new variable

expenses or the new contribution margin ratio. Both of these items must

be determined before the new break-even point can be computed. The

computations are:

New variable expenses:

Profit = (Sales − Variable expenses) − Fixed expenses

New CM ratio:

Sales ………………………….. $585,000 100%

V

ariable expenses …………. 351,000 60%

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

72 Managerial Accounting, 16th Edition

Problem 5-29 (continued)

The greatest risk is that the increases in sales and net operating income

predicted by the marketing manager will not happen and that sales will

remain at their present level. Note that the present level of sales is

It would be a good idea to compare the new marketing strategy to the

current situation more directly. What level of sales would be needed

under the new method to generate at least the $45,000 in profits the

company is currently earning each month? The computations are:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 73

Problem 5-30 (60 minutes)

1. Profit = Unit CM × Q − Fixed expenses

$0 = ($40 − $16) × Q − $60,000

$0 = ($24) × Q − $60,000

Alternative solution:

Fixed expenses $60,000

Unit sales to = = = 2,500 pairs

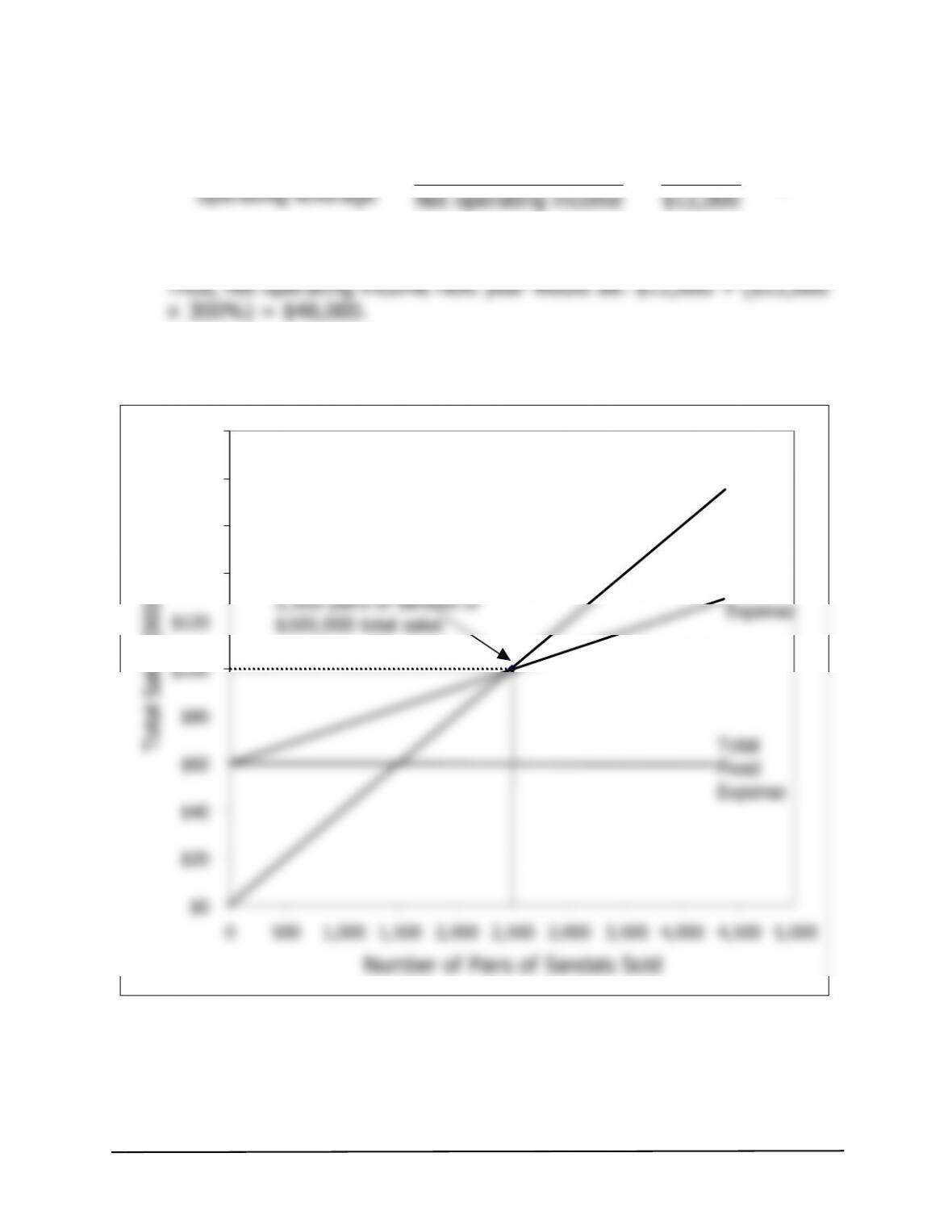

2. See the graphs at the end of this solution.

3. Profit = Unit CM × Q − Fixed expenses

$18,000 = $24 × Q − $60,000

4. Incremental contribution mar

g

in:

$25,000 increased sales × 60% CM ratio …. $15,000

Incremental fixed salary cost …………………… 8,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

74 Managerial Accounting, 16th Edition

Problem 5-30 (continued)

5. a. Contribution margin $72,000

Degree of = = = 6

b. 6 × 50% sales increase = 300%

increase

in net operating income.

2. Cost-volume-profit graph:

$140

$160

$180

$200

Break–even point:

Total Sales

Total

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 75

Problem 5-30 (continued)

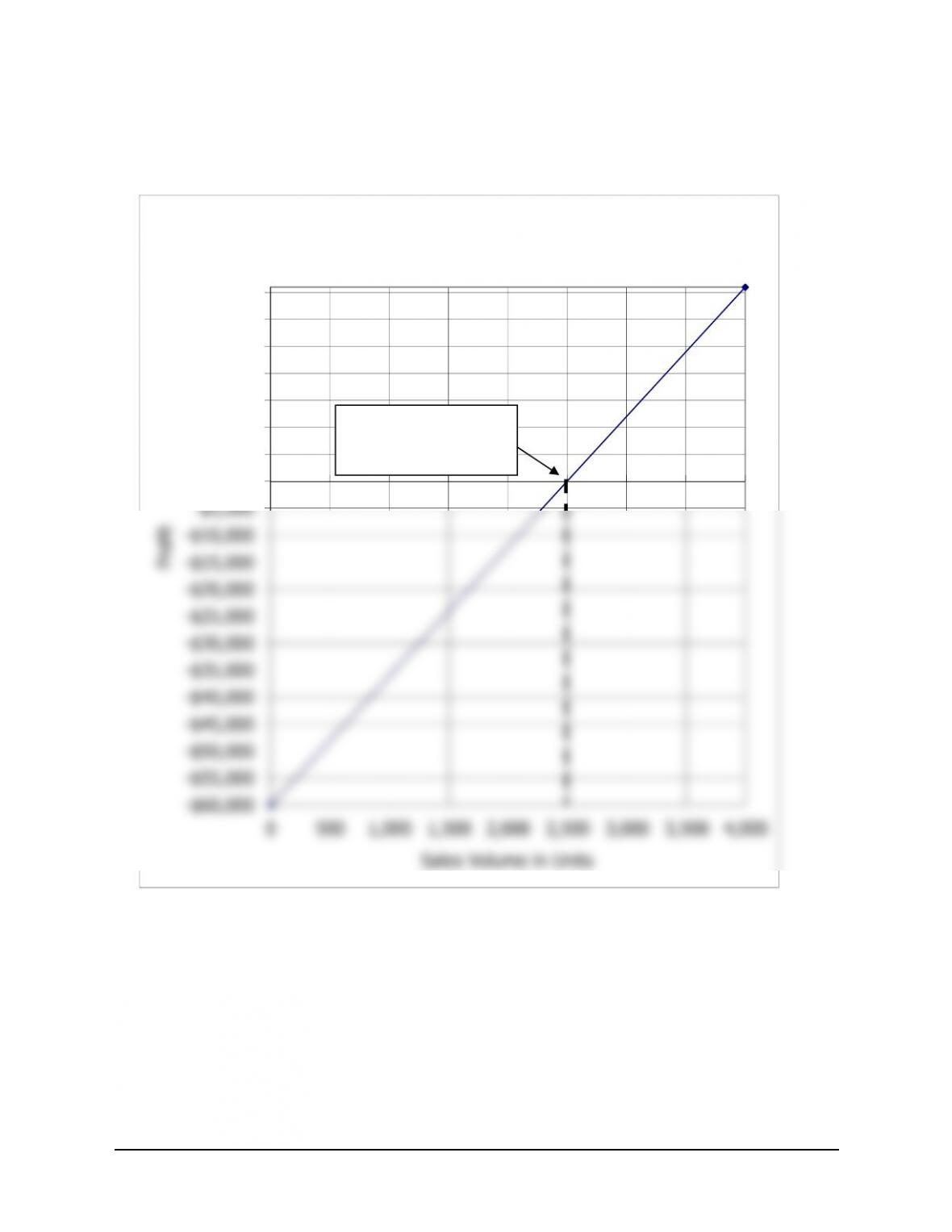

Profit graph:

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Profit Graph

Break-even point:

2,500 sandals

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

76 Managerial Accounting, 16th Edition

Problem 5-31 (30 minutes)

1. (1) Dollars

(2)

V

olume of output, expressed in units, % of capacity, sales,

or some other measure

(3)

T

otal expense line

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 77

Problem 5-31 (continued)

2. a. Line 3: Remain unchan

g

ed.

b. Line 3: Have a flatter slope.

g

c. Line 3: Shift upward.

g

d. Line 3: Remain unchan

g

ed.

g

g

e. Line 3: Shift downward and have a steeper slope.

g

f. Line 3: Have a steeper slope.

g

g

. Line 3: Shift upward.

Line 9: Remain unchan

g

ed.

h. Line 3: Shift upward and have a flatter slope.

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

78 Managerial Accounting, 16th Edition

Case 5-32 (60 minutes)

Note: This is a problem that will challenge the very best students’ conceptual

and analytical skills. However, working through this case will yield substantial

dividends in terms of a much deeper understanding of critical management

accounting concepts.

1. The overall break-even sales can be determined using the CM ratio.

Velcro Metal Nylon Total

Sales……………………….. $165,000 $300,000 $340,000 $805,000

V

ariable expenses ………. 125,000 140,000 100,000 365,000

Contribution mar

g

in ..….. $ 40,000 $160,000 $240,000 440,000

2. The issue is what to do with the common fixed cost when computing

the break-evens for the individual products. The correct approach is to

a. The break-even points for each product can be computed using the

contribution margin approach as follows:

Velcro Metal Nylon

Unit sellin

g

price ……………………………. $1.65 $1.50 $0.85

V

ariable cost per unit ……………………… 1.25 0.70 0.25

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 79

Case 5-32 (continued)

b. If the company were to sell exactly the break-even quantities

computed above, the company would lose $240,000—the amount of

the common fixed cost. This can be verified as follows:

Velcro Metal Nylon Total

Unit sales ………………. 50,000 100,000 100,000

Sales ……………………. $82,500 $150,000 $85,000 $317,500

At this point, many students conclude that something is wrong with

their answer to part (a) because a result in which the company loses

money operating at the break-evens for the individual products does not

Many students (and managers, for that matter) attempt to resolve this

apparent paradox by allocating the common fixed costs among the

products prior to computing the break-evens for individual products. Any

of a number of allocation bases could be used for this purpose—sales,

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

80 Managerial Accounting, 16th Edition

Case 5-32 (continued)

Allocation of common fixed expenses on the basis of sales revenue:

Velcro Metal Nylon Total

Sales ……….…………………… $165,000 $300,000 $340,000 $805,000

Percenta

g

e of total sales …… 20.497% 37.267% 42.236% 100.0%

A

llocated common fixed

expense* ……………………. $49,193 $ 89,441 $101,366 $240,000

A

“

If the company sells 172,983 units of the Velcro product, 211,801 units of

the Metal product, and 268,943 units of the Nylon product, the company

will indeed break even overall. However, the apparent break-evens for two

of the products are higher than their normal annual sales.

Velcro Metal Nylon

“

“

It would be natural for managers to interpret a break-even for a product as

the level of sales below which the company would be financially better off

dropping the product. Therefore, we should not be surprised if managers,