© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 61

Problem 5-26 (continued)

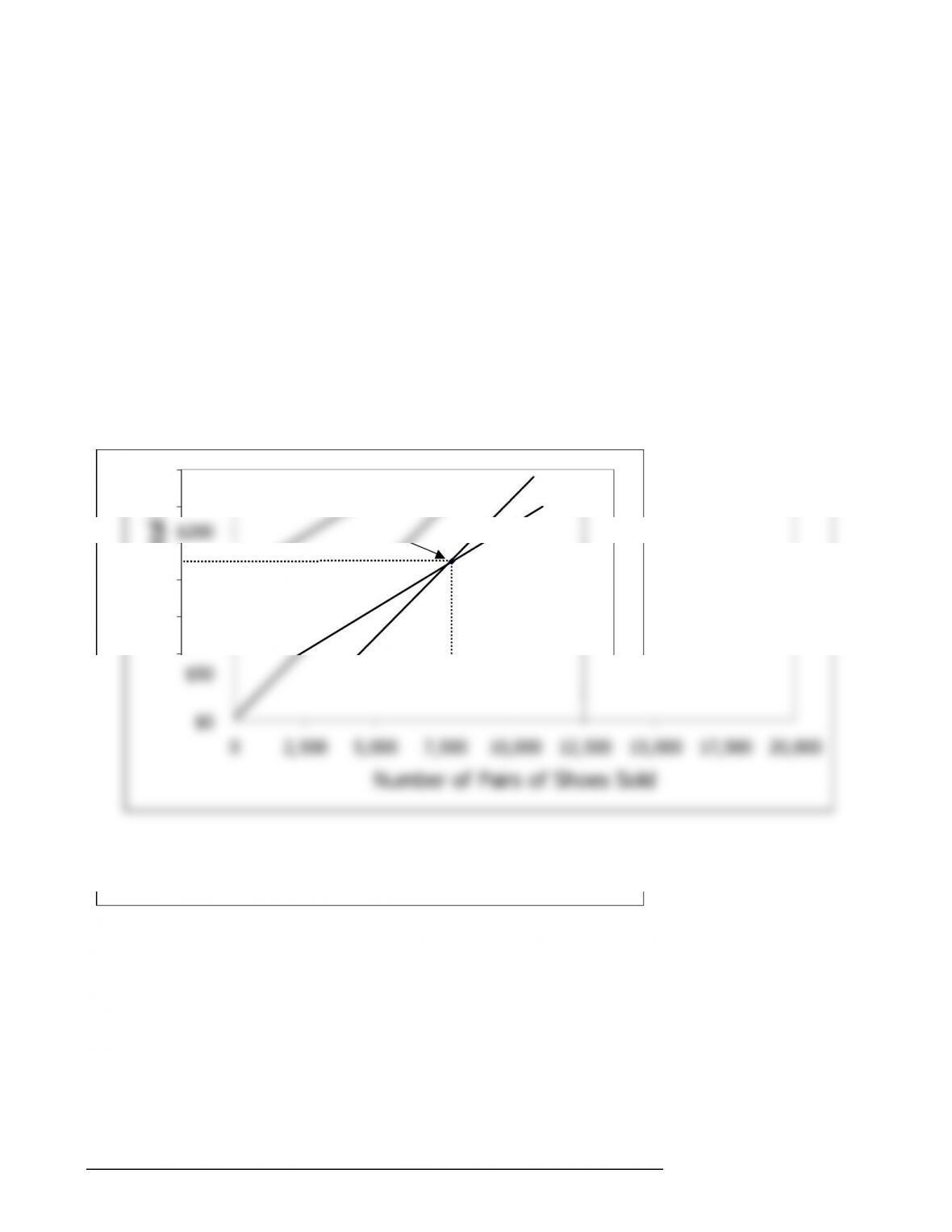

2. Cost-volume-profit graph:

$300

$350

$400

$450

$500

Break–even point:

Total Sales

Total

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

62 Managerial Accounting, 16th Edition

Problem 5-26 (continued)

4. The variable expenses will now be $18.75 per pair, and the contribution

margin will be $11.25 per pair.

Profit = Unit CM × Q − Fixed expenses

$0 = ($30.00 − $18.75) × Q − $150,000

Alternative solution:

Fixed expenses

Unit sales to =

break even CM per unit

$150,000

= = 13,333 pairs

0.375

5. The simplest approach is:

A

ctual sales ………………………….. 15,000 pairs

Brea

k

-even sales …………………… 12,500 pairs

–

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 63

Problem 5-26 (continued)

6. The new variable expenses will be $13.50 per pair.

Profit = Unit CM × Q − Fixed expenses

$0 = ($30.00 − $13.50) × Q

–

($150,000 + $31,500)

Although the change will lower the break-even point from 12,500 pairs

to 11,000 pairs, the company must consider whether this reduction in

the break-even point is more than offset by the possible loss in sales

arising from having the sales staff on a salaried basis. Under a salary

arrangement, the sales staff has less incentive to sell than under the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

64 Managerial Accounting, 16th Edition

Problem 5-27 (45 minutes)

1. a.

Hawaiian

Fantasy

(20,000 units)

Tahitian

Joy

(5,000 units) Total

Amount % Amount % Amount %

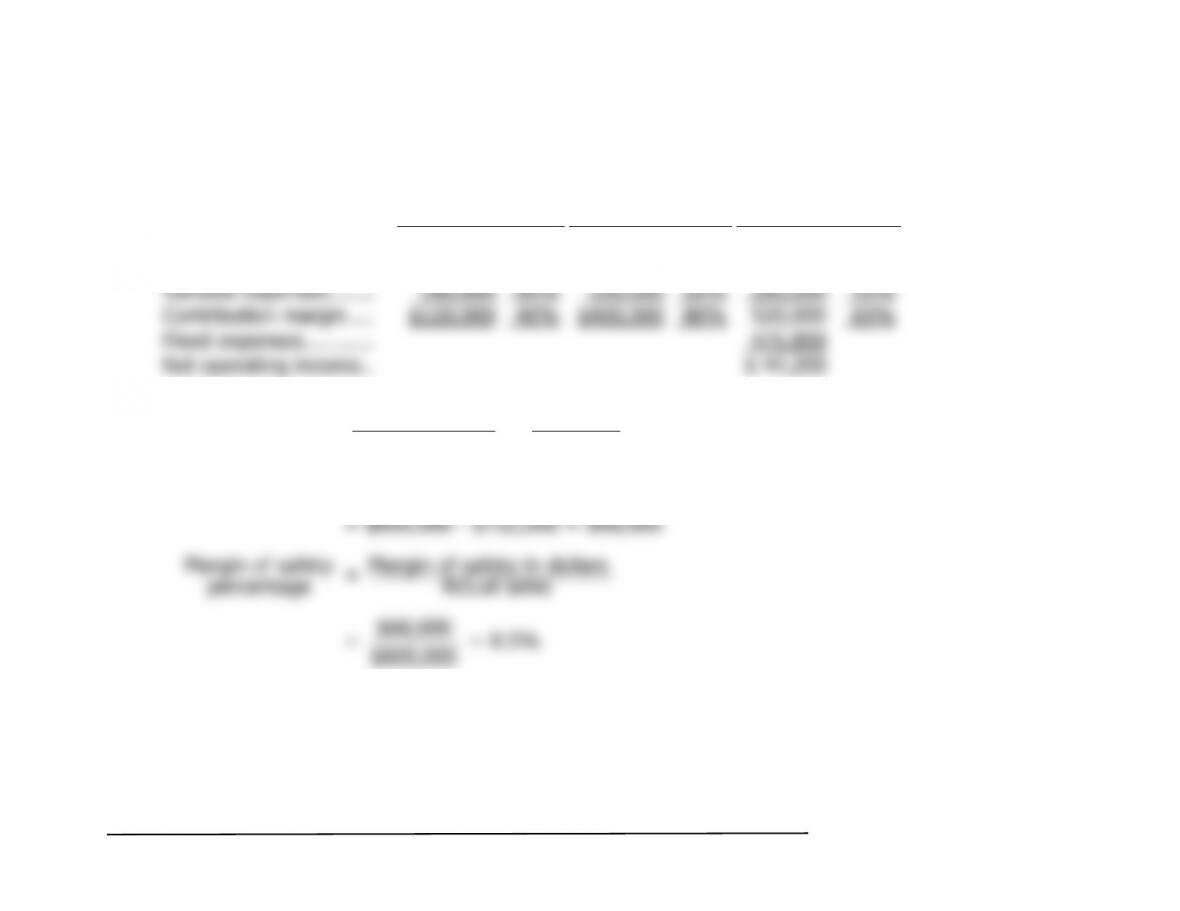

Sales ……………………. $300,000 100% $500,000 100% $800,000 100%

b. Fixed expenses $475,800

Dollar sales to = = = $732,000

break even CM ratio 0.65

Mar

g

in of safety = Actual sales – Break-even sales

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 65

Problem 5-27 (continued)

2. a.

Hawaiian

Fantasy

(20,000 units)

Tahitian

Joy

(5,000 units)

Samoan

Delight

(10,000 units)

Total

Amount % Amount % Amount % Amount %

Sales ……………. $300,000 100% $500,000 100% $450,000 100% $1,250,000 100.0%

V

ariable

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

66 Managerial Accounting, 16th Edition

Problem 5-27 (continued)

b. Fixed expenses $475,800

Dollar sales to = = = $975,000

break even CM ratio 0.488

Mar

g

in of safety = Actual sales – Break-even sales

3. The reason for the increase in the break-even point can be traced to the

decrease in the company’s overall contribution margin ratio when the

third product is added. Note from the income statements above that this

This problem shows the somewhat tenuous nature of break-even

analysis when the company has more than one product. The analyst

It should be pointed out to the president that even though the break-

even point is higher with the addition of the third product, the

company’s margin of safety is also greater. Notice that the margin of

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 67

Problem 5-28 (60 minutes)

1.

Carbex, Inc.

Income Statement For

A

pril

Standard Deluxe Total

Amount % Amount % Amount %

Sales ……………………… $240,000 100 $150,000 100 $390,000 100.0

V

ariable expenses:

Production ……………. 60,000 25 60,000 40 120,000 30.8

Sales commission …… 36,000 15 22,500 15 58,500 15.0

T

A

A

T

Carbex, Inc.

Income Statement For May

Standard Deluxe Total

Amount % Amount % Amount %

Sales ……………………… $60,000 100 $375,000 100 $435,000 100.0

V

ariable expenses:

Production ……………. 15,000 25 150,000 40 165,000 37.9

Sales commission …… 9,000 15 56,250 15 65,250 15.0

T

otal variable expenses . 24,000 40 206,250 55 230,250 52.9

A

A

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

68 Managerial Accounting, 16th Edition

Problem 5-28 (continued)

2. The sales mix has shifted over the last year from Standard sets to

Deluxe sets. This shift has caused a decrease in the company’s overall

3. Sales commissions could be based on contribution margin rather than

on sales price. A flat rate on total contribution margin, as the text

a. The break-even in dollar sales can be computed as follows:

Dollar sales to = = = $350,000

b. The break-even point in May would be higher than the break-even

point in April. This occurs because the sales mix has shifted from the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 69

Problem 5-29 (60 minutes)

1. The income statements would be:

Present

Amount Per Unit %

Sales ……………………. $450,000 $30 100%

V

ariable expenses ……. 315,000 21 70%

Proposed

Amount Per Unit %

Sales ……………………. $450,000 $30 100%

V

ariable expenses* ….. 180,000 12 40%

2. a. Degree of operating leverage:

Present:

Contribution margin

Degree of

=

operating leverage Net operating income

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

70 Managerial Accounting, 16th Edition

Problem 5-29 (continued)

b. Dollar sales to break even:

Present:

Fixed expenses

Dollar sales to =

break even CM ratio

c. Margin of safety:

Present:

Mar

g

in of safety = Actual sales – Break-even sales

= $450,000 – $300,000 = $150,000

Proposed:

Mar

g

in of safety = Actual sales – Break-even sales

= $450,000 – $375,000 = $75,000