© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 51

Problem 5-22 (60 minutes)

1. The CM ratio is 30%.

Total Per Unit Percent of Sales

Sales (19,500 units) …….. $585,000 $30.00 100%

The break-even point is:

Profit = Unit CM × Q − Fixed expenses

$0 = ($30 − $21) × Q − $180,000

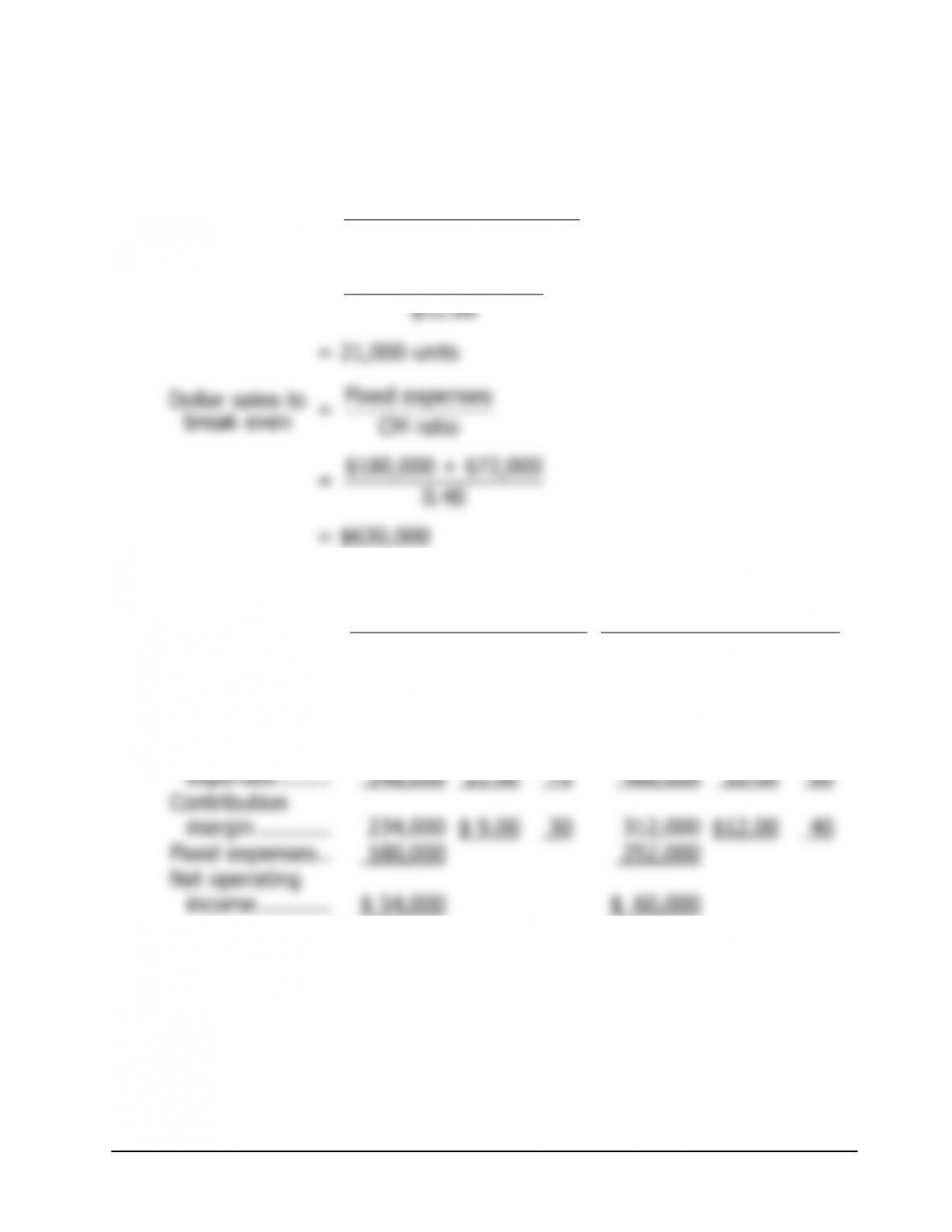

20,000 units × $30 per unit = $600,000 in sales

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution margin

2. Incremental contribution mar

g

in:

Less increased advertisin

g

cost ………………………. 16,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

52 Managerial Accounting, 16th Edition

Problem 5-22 (continued)

3. Sales (39,000 units @ $27.00 per unit*)…….. $1,053,000

V

ariable expenses

(39,000 units @ $21.00 per unit) ……………. 819,000

4. Profit = Unit CM × Q − Fixed expenses

$9,750 = ($30.00 − $21.75) × Q − $180,000

$9,750 = ($8.25) × Q − $180,000

Alternative solution:

T

ar

g

et profit + Fixed expenses

Unit sales to attain =

target profit CM per unit

5. a. The new CM ratio would be:

Per Unit Percent of Sales

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 53

Problem 5-22 (continued)

The new break-even point would be:

Fixed expenses

Unit sales to =

break even Unit contribution mar

g

in

$180,000 + $72,000

=

b. Comparative income statements follow:

Not Automated Automated

Total

Per

Unit % Total

Per

Unit %

Sales (26,000

units) …………. $780,000 $30.00 100 $780,000 $30.00 100

V

ariable

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

54 Managerial Accounting, 16th Edition

Problem 5-22 (continued)

c. Whether or not the company should automate its operations depends

on how much risk the company is willing to take and on prospects for

future sales. The proposed changes would increase the company’s

fixed costs and its break-even point. However, the changes would

The greatest risk of automating is that future sales may drop back

down to present levels (only 19,500 units per month), and as a

result, losses will be even larger than at present due to the

Note to the Instructor: Although it is not asked for in the problem,

if time permits you may want to compute the point of indifference

between the two alternatives in terms of units sold; i.e., the point

where profits will be the same under either alternative. At this point,

total revenue will be the same; hence, we include only costs in our

equation:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 55

Problem 5-23 (60 minutes)

1. The CM ratio is 60%:

2. Fixed expenses

Dollar sales to =

break even CM ratio

3. $75,000 increased sales × 0.60 CM ratio = $45,000 increased

4a. The degree of operating leverage is calculated as follows:

4. Contribution mar

g

in

Degree of

=

operating leverage Net operatin

g

income

4b. 4 × 20% = 80% increase in net operating income. In dollars, this

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

56 Managerial Accounting, 16th Edition

Problem 5-23 (continued)

5. This year’s net operating income is computed as follows:

Sales (25,000 units × $18 per unit)……………….. $450,000

V

ariable expenses (25,000 units × $8 per unit) … 200,000

6. Expected total contribution mar

g

in:

20,000 units × 1.25 × $11.00 per unit* …………………… $275,000

Present total contribution mar

g

in ……………………………… 240,000

–

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 57

Problem 5-24 (30 minutes)

1. The contribution margin per sweatshirt would be:

Sellin

g

price …………………………………….. $13.50

V

ariable expenses:

Purchase cost of the sweatshirts…………. $8.00

2. Since an order has been placed, there is now a “fixed” cost associated

with the purchase price of the sweatshirts (i.e., the sweatshirts can’t be

returned). For example, an order of 75 sweatshirts requires a “fixed”

g

V

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

58 Managerial Accounting, 16th Edition

Problem 5-25 (45 minutes)

1. The contribution margin per unit on the first 16,000 units is:

Per Unit

Sales price …………………….. $3.00

The contribution margin per unit on anything over 16,000 units is:

Per Unit

Sales price …………………….. $3.00

Thus, for the first 16,000 units sold, the total amount of contribution

margin generated would be:

16,000 units × $1.75 per unit = $28,000

Since the fixed costs on the first 16,000 units total $35,000, the $28,000

contribution margin above is not enough to permit the company to

Fixed costs on the first 16,000 units ………………….. $35,000

Less contribution mar

g

in from the first 16,000 units 28,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 59

Problem 5-25 (continued)

The additional sales of units required to cover these fixed costs would

be:

Total remaining fixed costs $8,000

= = 5,000 units

Unit CM on added units $1.60

Thus, the company must sell 7,500 units above the break-even point to

earn a profit of $12,000 each month. These units, added to the 21,000

3. If a bonus of $0.10 per unit is paid for each unit sold in excess of the

break-even point, then the contribution margin on these units would

drop from $1.60 to $1.50 per unit.

The desired monthly profit would be:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

60 Managerial Accounting, 16th Edition

Problem 5-26 (60 minutes)

1. Profit = Unit CM × Q − Fixed expenses

$0 = ($30 − $18) × Q − $150,000

$0 = ($12) × Q − $150,000

2. See the graph on the following page.

3. The simplest approach is:

Brea

k

-even sales ………………….. 12,500 pairs

A

Alternative solution:

Sales (12,000 pairs × $30.00 per pair) …. $360,000

V

ariable expenses