© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 41

Exercise 5-18 (continued)

4. Margin of safety in dollar terms:

Margin of safety = Total sales – Break-even sales

in dollars

5. The CM ratio is 60% [= ($30 – $12) ÷ $30].

Expected total contribution mar

g

in: ($500,000 × 60%) .. $300,000

Alternative solution:

$50,000 incremental sales × 60% CM ratio = $30,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

42 Managerial Accounting, 16th Edition

Problem 5-19 (45 minutes)

1. Sales (15,000 units × $70 per unit)…………………. $1,050,000

V

ariable expenses (15,000 units × $40 per unit) … 600,000

Contribution mar

g

in …………………………………….. 450,000

Fixed expenses ………………………………………..…. 540,000

Net operatin

g

loss ……………………………………….. $ (90,000)

2. Fixed expenses

Unit sales to=

break even Unit contribution margin

$540,000

3. See the next page.

4. At a selling price of $58 per unit, the contribution margin is $18 per unit.

Therefore:

Fixed expenses

Unit sales to =

break even Unit contribution mar

g

in

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 43

Problem 5-19 (continued)

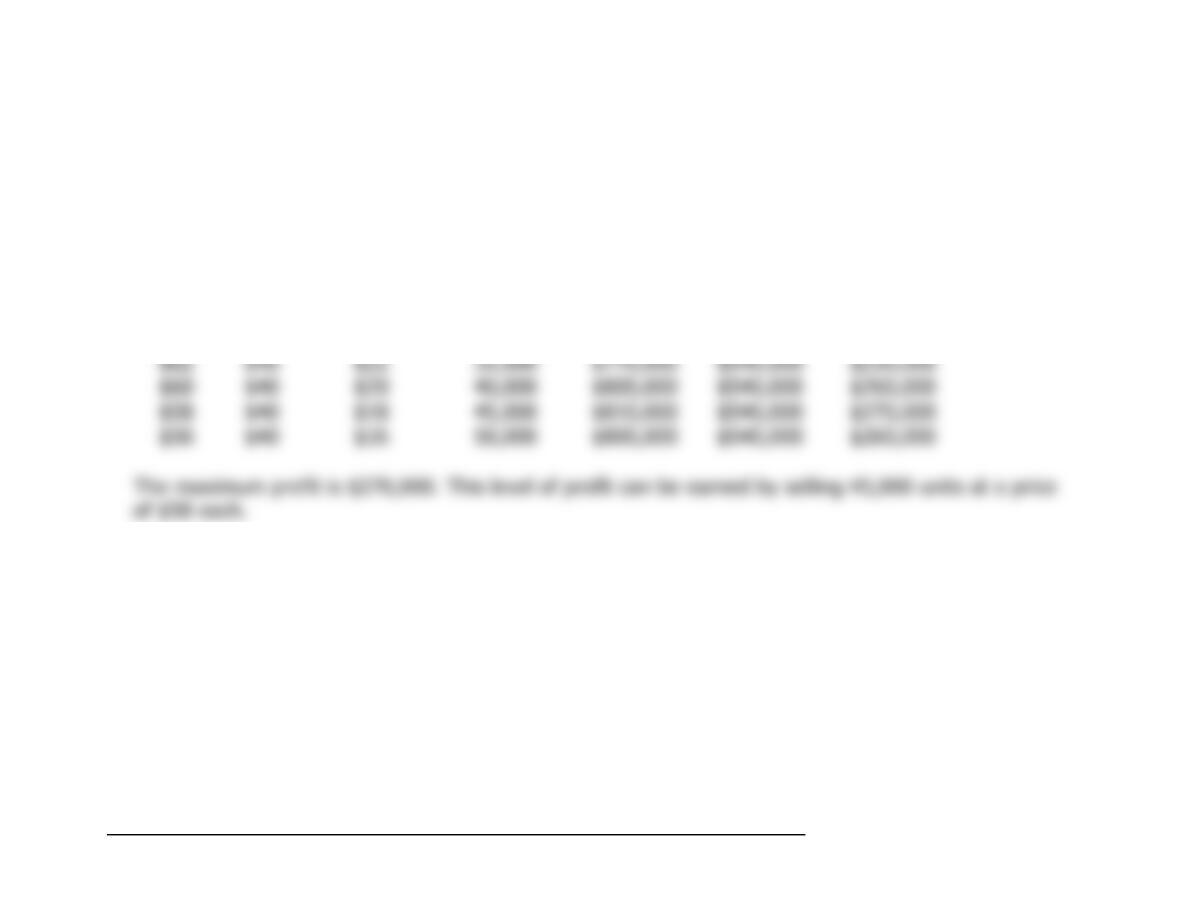

3.

Unit

Selling

Price

Unit

Variable

Expense

Unit

Contribution

Margin

Volume

(Units)

Total

Contribution

Margin

Fixed

Expenses

Net operating

income (loss)

$70 $40 $30 15,000 $450,000 $540,000 $ (90,000)

$68 $40 $28 20,000 $560,000 $540,000 $ 20,000

$66 $40 $26 25,000 $650,000 $540,000 $110,000

$64 $40 $24 30,000 $720,000 $540,000 $180,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

44 Managerial Accounting, 16th Edition

Problem 5-20 (75 minutes)

1. a. Sellin

g

price ……………….. $25 100%

V

ariable expenses ………… 15 60%

Contribution mar

g

in ……… $10 40%

Profit = Unit CM × Q − Fixed expenses

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution mar

g

in

b. The degree of operating leverage is:

Contribution margin

Degree of =

operating leverage Net operating income

2. The new CM ratio will be:

Sellin

g

price ……………….. $25 100%

V

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 45

Problem 5-20 (continued)

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution mar

g

in

3. Profit = Unit CM × Q − Fixed expenses

$90,000 = $7 × Q − $210,000

Thus, sales will have to increase by 12,857 balls (= 42,857 balls –

30,000 balls = 12,857 balls) to earn the same amount of net operating

income as last year. The computations above and in part (2) show the

dramatic effect that increases in variable costs can have on an

organization. The effects on Northwood Company are summarized

below:

Present Expected

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

46 Managerial Accounting, 16th Edition

Problem 5-20 (continued)

4. The contribution margin ratio last year was 40%. If we let P equal the

new selling price, then:

P = $18 + 0.40P

0.60P = $18

V

Therefore, to maintain a 40% CM ratio, a $3 increase in variable costs

would require a $5 increase in the selling price.

5. The new CM ratio would be:

Sellin

g

price …………………… $25 100%

V

ariable expenses …………… 9* 36%

–

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution margin

Although this new break-even point is greater than the company’s

present break-even point of 21,000 balls [see Part (1) above], it is less

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 47

Problem 5-20 (continued)

6. a. Profit = Unit CM × Q − Fixed expenses

$90,000 = $16 × Q − $420,000

Alternative solution:

Unit sales to attain

T

arget profit + Fixed expenses

=

target profit Unit contribution margin

$90,000 + $420,000

=

b. The contribution income statement would be:

Sales (30,000 balls × $25 per ball) ……………….. $750,000

V

ariable expenses (30,000 balls × $9 per ball)…. 270,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

48 Managerial Accounting, 16th Edition

Problem 5-20 (continued)

c. This problem illustrates the difficulty faced by some companies. When

variable labor costs increase, it is often difficult to pass these cost

increases along to customers in the form of higher prices. Thus,

There is no clear answer as to whether one should have been in favor

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 49

Problem 5-21 (30 minutes)

1.

Product

White Fragrant Loonzain Total

Percenta

g

e of total

sales ……………….. 40% 24% 36% 100%

Sales ………………….. $300,000 100% $180,000 100% $270,000 100% $750,000 100%

2. Break-even sales would be:

Fixed expenses

Dollar sales to =

break even CM ratio

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

50 Managerial Accounting, 16th Edition

Problem 5-21 (continued)

3. Memo to the president:

Although the company met its sales budget of $750,000 for the month,

the mix of products changed substantially from that budgeted. This is

the reason the budgeted net operating income was not met, and the

As shown by these data, sales shifted away from Fragrant Rice, which

provides our greatest contribution per dollar of sales, and shifted toward

White Rice, which provides our least contribution per dollar of sales.

Although the company met its budgeted level of sales, these sales

provided considerably less contribution margin than we had planned,