© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 31

Exercise 5-13 (20 minutes)

Total Per Unit

1. Sales (20,000 units × 1.15 = 23,000 units)…. $345,000 $ 15.00

V

ariable expenses …………………………………. 207,000 9.00

2. Sales (20,000 units × 1.25 = 25,000 units)…. $337,500 $13.50

V

ariable expenses …………………………………. 225,000 9.00

3. Sales (20,000 units × 0.95 = 19,000 units)…. $313,500 $16.50

V

ariable expenses …………………………………. 171,000 9.00

4. Sales (20,000 units × 0.90 = 18,000 units)…. $302,400 $16.80

V

ariable expenses …………………………………. 172,800 9.60

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

32 Managerial Accounting, 16th Edition

Exercise 5-14 (30 minutes)

2. The break-even points in unit sales (Q) and dollar sales are computed as

follows:

Sellin

g

price ……………………. $40 100%

V

ariable expenses …………….. 28 70%

Alternative solution:

Profit = CM ratio × Sales − Fixed expenses

$0 = 0.30 × Sales − $180,000

3. The unit sales and dollar sales needed to attain the target profit are

computed as follows:

Profit = Unit CM × Q − Fixed expenses

$60,000 = $12 × Q − $180,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 33

Exercise 5-14 (continued)

Alternative solution:

Profit = CM ratio × Sales − Fixed expenses

$60,000 = 0.30 × Sales − $180,000

4. The new break-even points in unit sales and dollar sales are computed

as follows:

The company’s new cost/revenue relation will be:

Sellin

g

price ………………………… $40 100%

V

ariable expenses ($28

–

$4) ….. 24 60%

Contribution mar

g

in ………………. $16 40%

Alternative solution:

Profit = CM ratio × Sales − Fixed expenses

$0 = 0.40 × Sales − $180,000

0.40 × Sales = $180,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

34 Managerial Accounting, 16th Edition

Exercise 5-14 (continued)

4. The dollar sales required to attain the target profit is computed as

follows:

Profit = CM ratio × Sales − Fixed expenses

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 35

Exercise 5-15 (15 minutes)

1.

Total

Per

Unit

Sales (15,000

g

ames) ……… $300,000 $20

V

ariable expenses ………….. 90,000 6

Contribution mar

g

in ……….. 210,000 $14

2. a. Sales of 18,000 games represent a 20% increase over last year’s

b. The expected total dollar amount of net operating income for next

year would be:

Last year’s net operatin

g

income …………………. $28,000

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

36 Managerial Accounting, 16th Edition

Exercise 5-16 (30 minutes)

1. The contribution margin per person would be:

Price per ticket ………………………………. $35

V

ariable expenses:

+ $1,000 + $1,300). The break-even point would be:

Profit = Unit CM × Q − Fixed expenses

$0 = ($35 − $20) × Q − $6,000

Alternative solution:

Fixed expenses

Unit sales to=

break even Unit contribution margin

2.

V

ariable cost per person ($18 + $2)…………….. $20

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 37

Exercise 5-16 (continued)

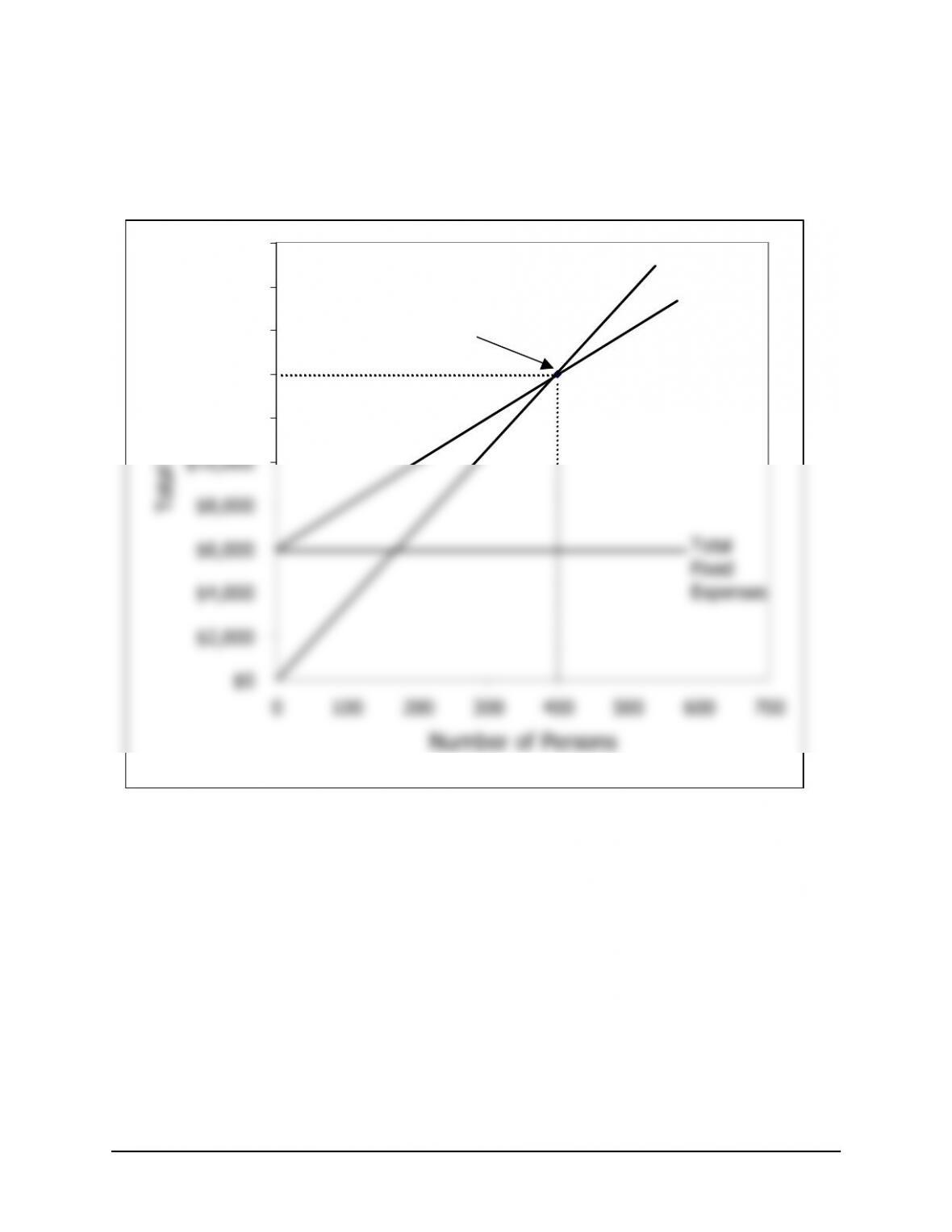

3. Cost-volume-profit graph:

$12,000

$14,000

$16,000

$18,000

$20,000

Total

Expenses

Total Sales

Break–even point:

400 persons or

$14,000 total sales

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

38 Managerial Accounting, 16th Edition

Exercise 5-17 (30 minutes)

1. Profit = Unit CM × Q − Fixed expenses

$0 = ($50 − $32) × Q − $108,000

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution margin

2. An increase in variable expenses as a percentage of the selling price

would result in a higher break-even point. If variable expenses increase

3.

Present:

8,000 Stoves

Proposed:

10,000 Stoves*

Total Per Unit Total Per Unit

Sales ………………………. $400,000 $50 $450,000 $45 **

V

ariable expenses ……… 256,000 32 320,000 32

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 5 39

Exercise 5-17 (continued)

4. Profit = Unit CM × Q − Fixed expenses

$35,000 = ($45 − $32) × Q − $108,000

Alternative solution:

Tar

g

et profit + Fixed expenses

Unit sales to attain =

target profit Unit contribution margin

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

40 Managerial Accounting, 16th Edition

Exercise 5-18 (30 minutes)

1. Profit = Unit CM × Q − Fixed expenses

$0 = ($30 − $12) × Q − $216,000

Alternative solution:

Fixed expenses

Unit sales

=

to break even Unit contribution margin

2. The contribution margin is $216,000 because the contribution margin is

3.

T

ar

g

et profit + Fixed expenses

Units sold to attain

=

target profit Unit contribution margin

Total Unit

Sales (17,000 units × $30 per unit)……. $510,000 $30

V

ariable expenses