© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 5A 99

Problem 5A-9 (continued)

2. Milden Company

Budgeted Contribution Format Income Statement

For the First Quarter, Year 3

Sales (12,000 units × $100 per unit) ……….. $1,200,000

V

ariable expenses:

Cost of

g

oods sold

T

otal variable expenses ………………………… 601,200

Contribution mar

g

in …………………………….. 598,800

Fixed expenses:

A

dvertisin

g

expense ………………………….. 210,000

Shippin

g

expense ……………………………… 28,000

A

T

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

100 Managerial Accounting, 16th Edition

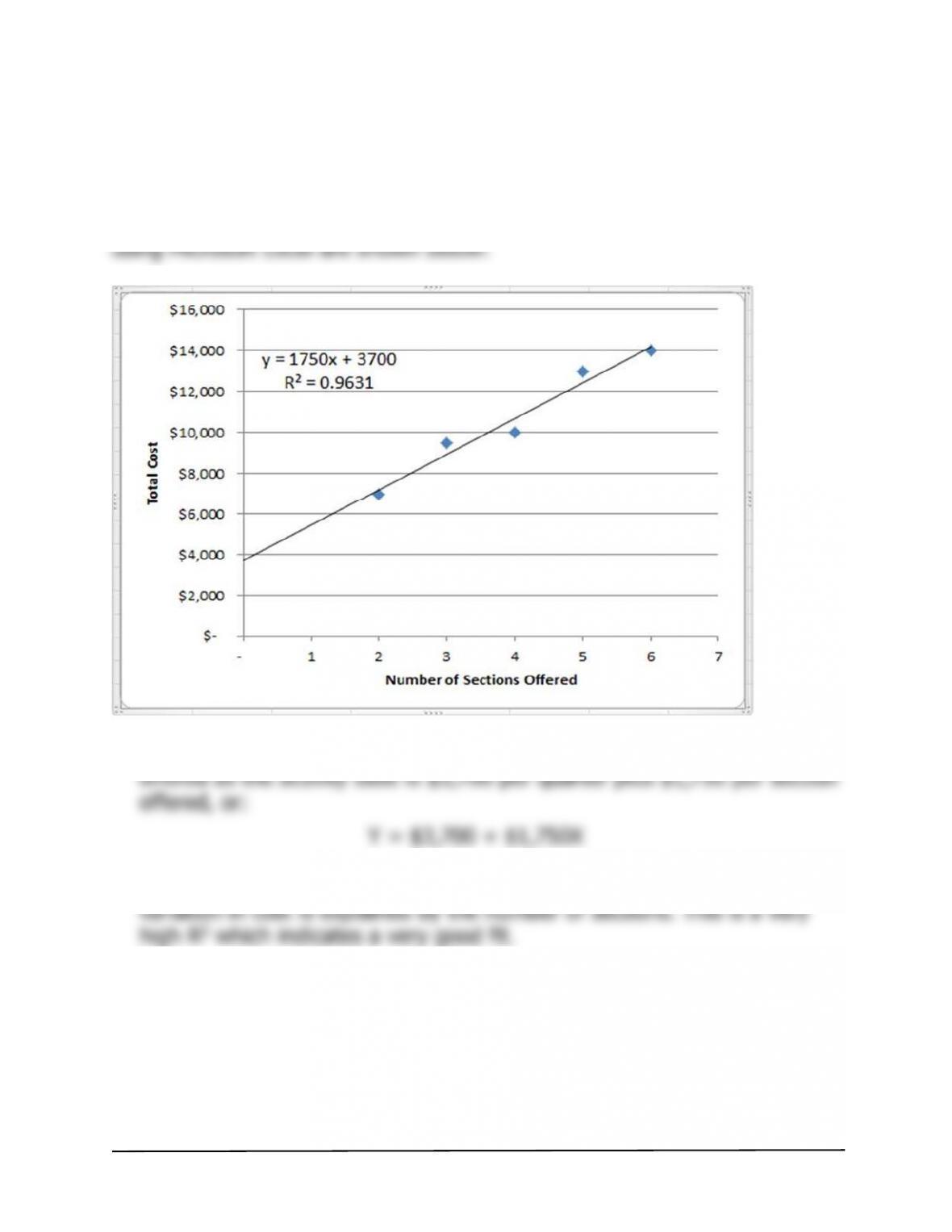

Problem 5A-10 (30 minutes)

1. and 2.

The scattergraph plot and regression estimates of fixed and variable costs

The cost formula, in the form

Y

=

a

+

bX

, using number of sections

Note that the R

2

is approximately 0.96, which means that 96% of the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 5A 101

Problem 5A-10 (continued)

3. Expected total cost would be:

The problem with using the cost formula from (2) to derive total cost is

that an activity level of 8 sections may lie outside the relevant range—

the range of activity within which the fixed cost is approximately $3,700

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

102 Managerial Accounting, 16th Edition

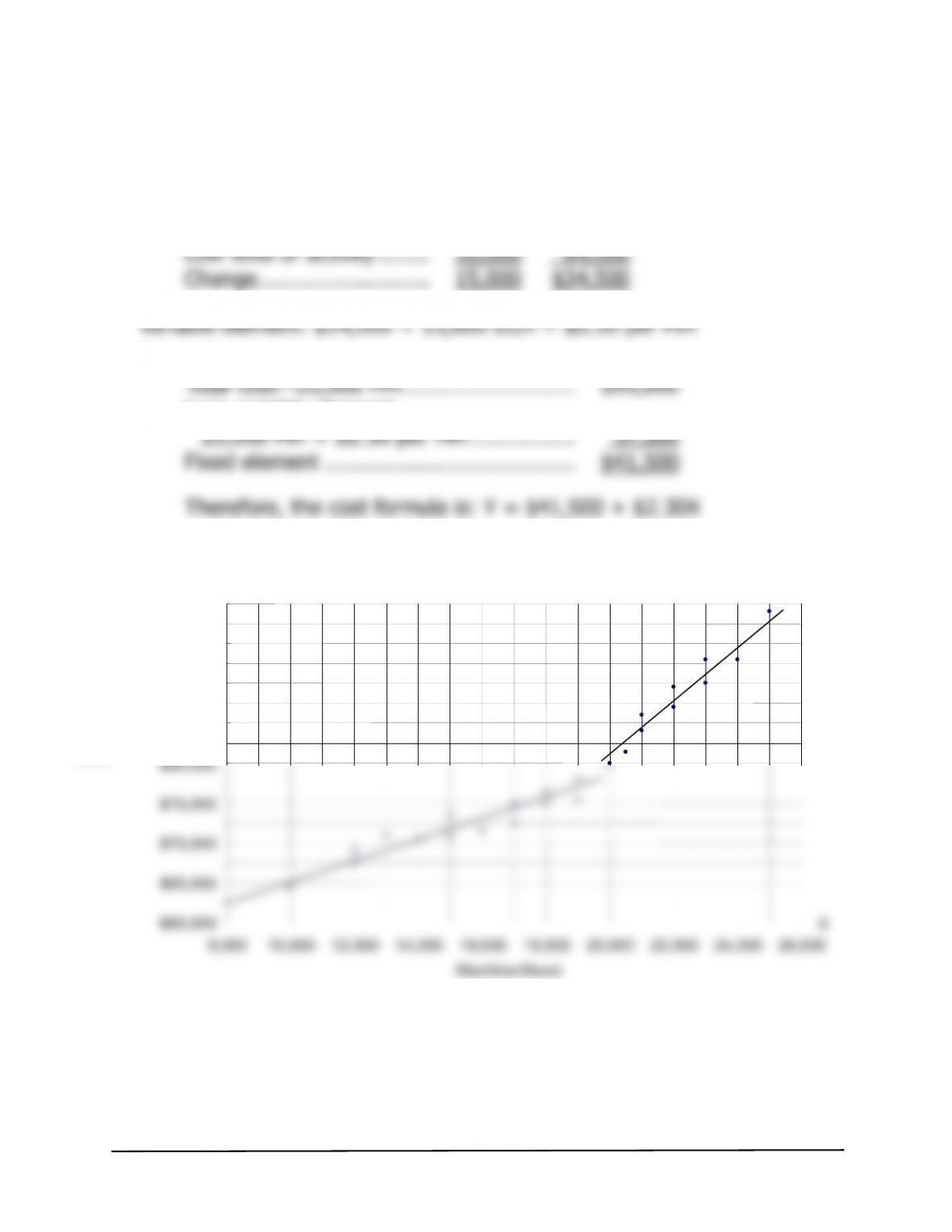

Case 5A-11 (60 minutes)

1. High-low method:

Hours Cost

Hi

g

h level of activity ……. 25,000 $99,000

Fixed element:

Less variable element:

2. The scattergraph is shown below:

$85,000

$90,000

$95,000

$100,000

Y

Overhead

Costs

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 5A 103

Case 5A-11 (continued)

2. The scattergraph shows that there are two relevant ranges—one below

19,500 MH and one above 19,500 MH. The change in equipment lease

3. The cost formulas computed with the high-low and regression methods

are faulty since they are based on the assumption that a single straight

4. High-low method:

Hours Cost

Hi

g

h level of activity ……. 25,000 $99,000

Variable element: $19,000 ÷ 5,000 MH = $3.80 per MH

Fixed element:

T

otal cost

—

25,000 MH …………………….. $99,000

Less variable element:

V

T

5. The high-low estimate of fixed costs is $6,090 (= $10,090 – $4,000)

lower than the estimate provided by least-squares regression. The high-

low estimate of the variable cost per machine hour is $0.27 (= $3.80 –

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

104 Managerial Accounting, 16th Edition

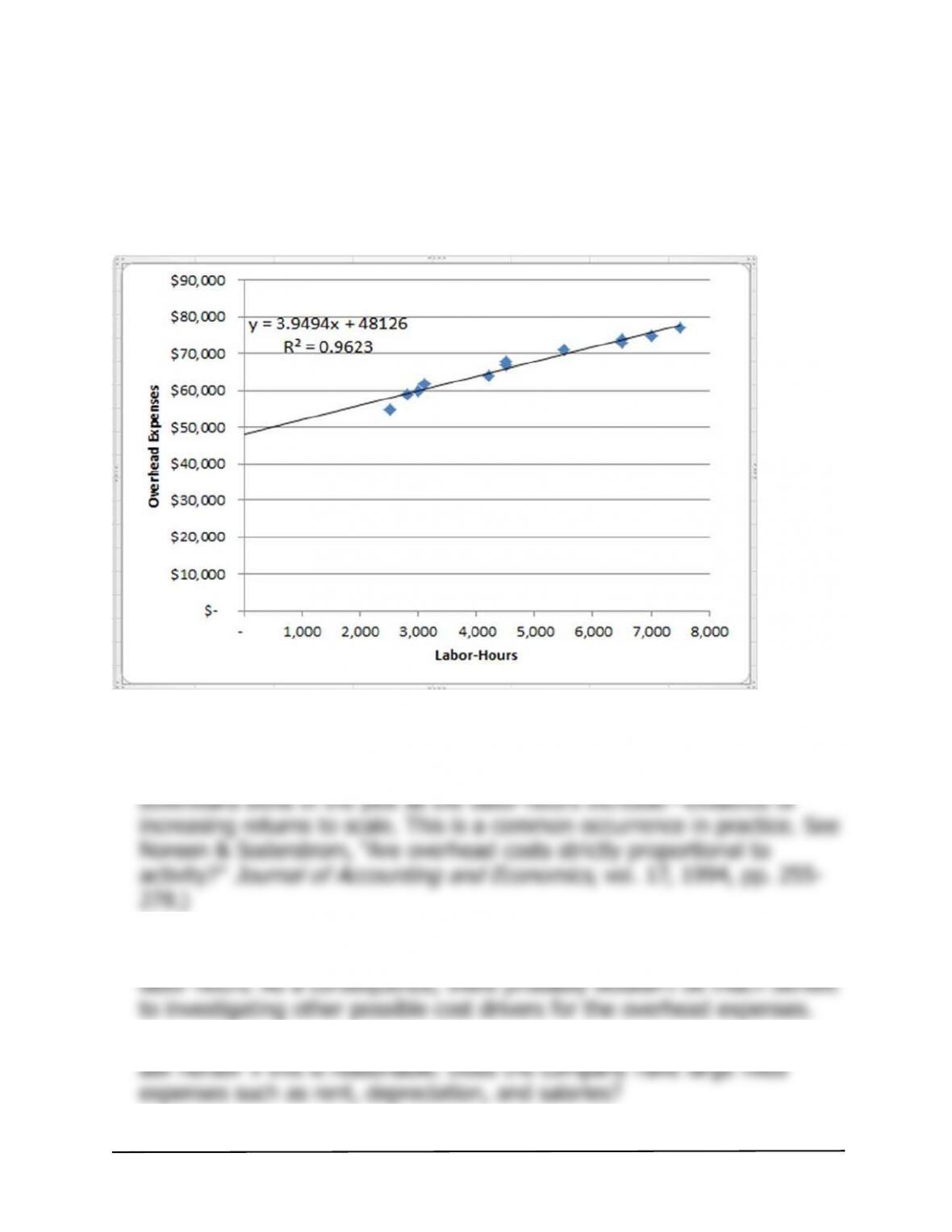

Case 5A-12 (45 minutes)

1. and 2.

The scattergraph plot and regression estimates of fixed and variable

costs using Microsoft Excel are shown below:

The scattergraph reveals three interesting findings. First, it indicates the

relation between overhead expense and labor hours is approximated

reasonably well by a straight line. (However, there appears to be a slight

Second, the data points are all fairly close to the straight line. This

indicates that most of the variation in overhead expenses is explained by

Third, most of the overhead expense appears to be fixed. Maria should

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 5A 105

CASE 5A-12 (continued)

The cost formula, in the form

Y

=

a

+

bX

, using labor-hours as the

activity base is $48,126 per month plus $3.95 per labor-hour, or:

3. Using the least-squares regression estimate of the variable overhead

cost, the total variable cost per guest is computed as follows:

Food and bevera

g

es ………………………. $15.00

T

The total contribution from 180 guests paying $31 each is computed as

follows:

Sales (180

g

uests @ $31.00 per

g

uest) ………….. $5,580.00

V

g

g

4. Assuming that no additional fixed costs are incurred as a result of

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

106 Managerial Accounting, 16th Edition

CASE 5A-12 (continued)

5. We would favor bidding slightly less than $30 to get the contract. Any

bid above $22 would contribute to profits and a bid at the normal price

of $31 is unlikely to land the contract. And apart from the contribution

to profit, catering the event would show off the company’s capabilities

to potential clients. The danger is that a price that is lower than the

normal bid of $31 might set a precedent for the future or it might