© The McGraw-Hill Companies, Inc., 2018

Solutions Manual, Chapter 13 11

The Foundational 15 (continued)

5. The project profitability index for the project is:

Item

Net Present

Value

(a)

Investment

Required

(b)

Project

Profitability

Index

(a) ÷ (b)

6. The project’s internal rate of return is:

Investment required

Factor of the internal =

rate of return

A

nnual cash inflow

Looking in Exhibit 13B-2, and scanning along the five-period line, we

can see that the factor computed above, 2.975, is closest to 2.991, the

7. The payback period is determined as follows:

Year Investment

Cash

Inflow

Unrecovered

Investment

1 $2,975,000 $1,000,000 $1,975,000

The investment in the project is fully recovered in the 3rd year. To be

© The McGraw-Hill Companies, Inc., 2018

12 Managerial Accounting, 16th Edition

The Foundational 15 (continued)

8. The simple rate of return is computed as follows:

A

nnual incremental net operatin

g

income

Simple rate =

of return Initial investment

9. If the discount rate was 16%, instead of 14%, the project’s net

10. The payback period would be the same because the initial investment

11. The net present value would be higher because a $300,000 salvage

value translates into a larger cash inflow in the fifth year. Although the

12. The simple rate of return would be higher. The salvage value would

© The McGraw-Hill Companies, Inc., 2018

Solutions Manual, Chapter 13 13

The Foundational 15 (continued)

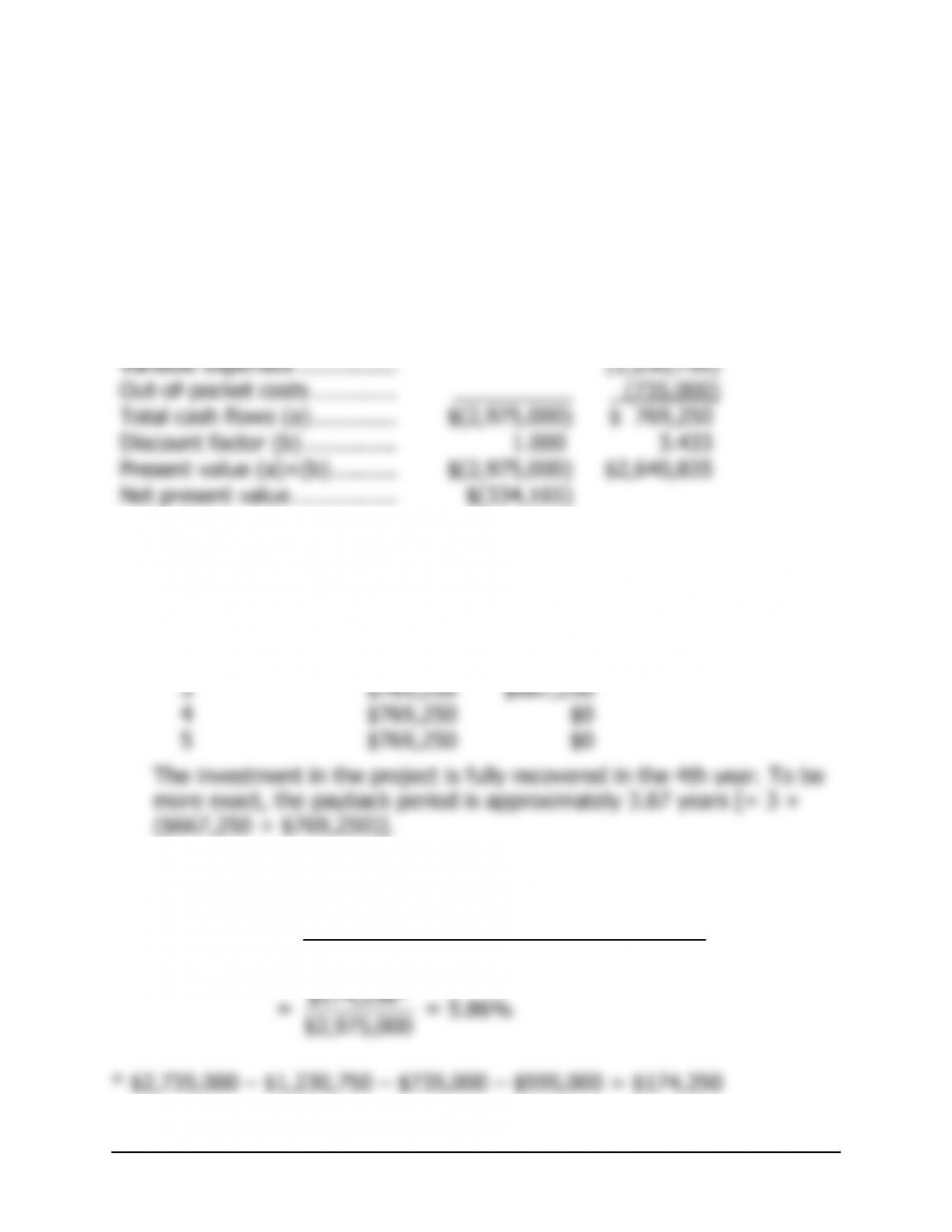

13. The new annual variable expense would be $1,230,750 ($2,735,000 ×

45%). The project’s actual net present value would be computed as

follows:

Now

Years

1-5

Purchase of equipment …….. $(2,975,000)

Sales ……………………………. $2,735,000

14. The payback period is computed as follows:

Year Investment

Cash

Inflow

Unrecovered

Investment

1 $2,975,000 $769,250 $2,205,750

2 $769,250 $1,436,500

15. The simple rate of return is computed as follows:

A

nnual incremental net operatin

g

income

Simple rate =

of return Initial investment

© The McGraw-Hill Companies, Inc., 2018

14 Managerial Accounting, 16th Edition

Exercise 13-1 (10 minutes)

1. The payback period is determined as follows:

Year Investment Cash Inflow

Unrecovered

Investment

1 $15,000 $1,000 $14,000

2 $8,000 $2,000 $20,000

3 $2,500 $17,500

2. Because the investment is recovered prior to the last year, the amount

© The McGraw-Hill Companies, Inc., 2018

Solutions Manual, Chapter 13 15

Exercise 13-2 (10 minutes)

1.

Now

Years

1-5

Purchase of machine ………………… $(27,000)

Reduced operating costs ……………. ________ $7,000

2.

Item

Cash

Flow Years

Total

Cash

Flows

© The McGraw-Hill Companies, Inc., 2018

16 Managerial Accounting, 16th Edition

Exercise 13-3 (20 minutes)

1.

A

nnual savin

g

s in part-time help ………………………. $3,800

A

dded contribution mar

g

in from expanded sales

2. Investment required

Factor of the internal =

rate of return

A

nnual cash inflow

3. Looking in Exhibit 13B-2, and scanning along the six-period line, we can

4. The cash flows will not be even over the six-year life of the machine

because of the extra $9,125 inflow in the sixth year. Therefore, the

rate of is 22%:

Now Years

1-6

Year

6

Purchase of machine …………………… $(18,600)

Reduced part-time help ……………….. $3,800

Added contribution margin ……………. 1,200

A

© The McGraw-Hill Companies, Inc., 2018

Solutions Manual, Chapter 13 17

Exercise 13-4 (15 minutes)

The equipment’s net present value without considering the intangible

benefits would be:

Item Year(s)

Amount of

Cash Flows

20%

Factor

Present Value

of Cash Flows

The annual value of the intangible benefits would have to be great enough

to offset a $630,000 negative present value for the equipment. This annual

value can be computed as follows:

© The McGraw-Hill Companies, Inc., 2018

18 Managerial Accounting, 16th Edition

Exercise 13-5 (10 minutes)

1. The project profitability index for each proposal is:

Proposal

Number

Net Present

Value

(a)

Investment

Required

(b)

Project Profitability

Index

(a) (b)

A

$36,000 $90,000 0.40

2. The ranking is:

Proposal

Number

Project Profitability

Index

C 0.50

A

Note that proposal D has the highest net present value, but it ranks

lowest in terms of the project profitability index.

© The McGraw-Hill Companies, Inc., 2018

Solutions Manual, Chapter 13 19

Exercise 13-6 (10 minutes)

1. The annual depreciation expense is computed as follows:

Cost of the new machine (a)…………………. $120,000

2. The annual incremental net operating income is computed as follows:

Operatin

g

cost of old machine……………….. $ 30,000

Less operatin

g

cost of new machine ……….. 12,000

3. The initial investment is computed as follows:

Cost of the new machine ……………………… $120,000

4. The simple rate of return is computed as follows:

A

nnual incremental net operatin

g

income

Simple rate =

of return Initial investment

© The McGraw-Hill Companies, Inc., 2018

20 Managerial Accounting, 16th Edition

Exercise 13-7 (15 minutes)

1. Project A:

Now

Years

1-6

Year

6

Purchase of equipment …….. $(100,000)

Annual cash inflows …………. $21,000

Salvage value ………………… _______ ______ $8,000

2. Project B:

Now

Years

1-6

Year

6

Working capital invested …… $(100,000)

Annual cash inflows …………. $16,000

Working capital released …… _______ ______ $100,000

3. The $100,000 should be invested in Project B rather than in Project A.