© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 81

Exercise 12A-5 (30 minutes)

1. The profit at a price of $24.00 is computed as follows:

Profit = (P

–

V) × Q − Fixed expenses

2. Northport would need to sell 76,364 units computed as follows:

Profit = (P

–

V) × Q − Fixed expenses

$40,000 = ($24.00 − $13.00) × Q − $800,000

3. The percentage decrease is computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

82 Managerial Accounting, 16th Edition

Exercise 12A-5 (continued)

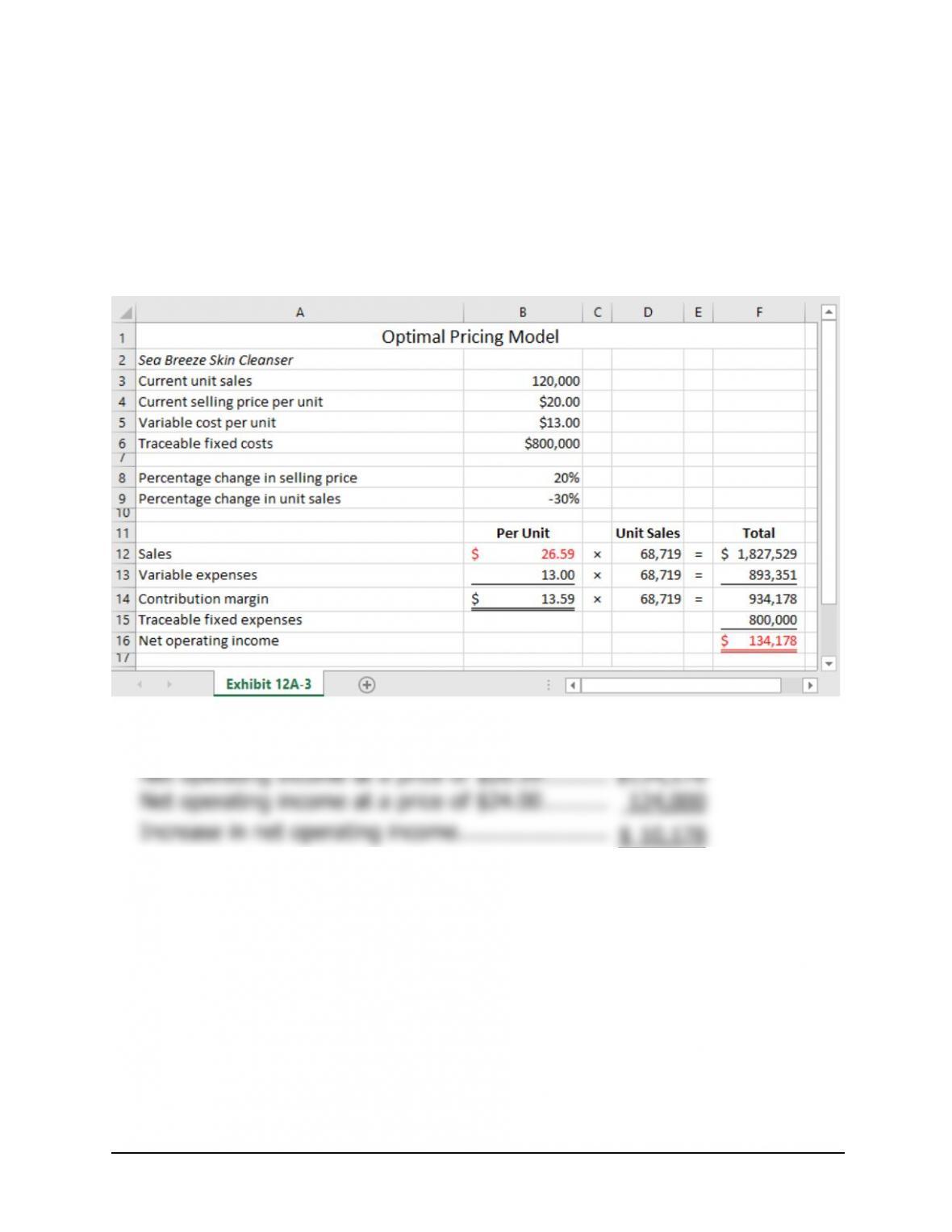

4a and 4b.

The optimal selling price ($26.59) and the optimal profit ($134,178) are as

shown below:

4c. The additional profit is computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 83

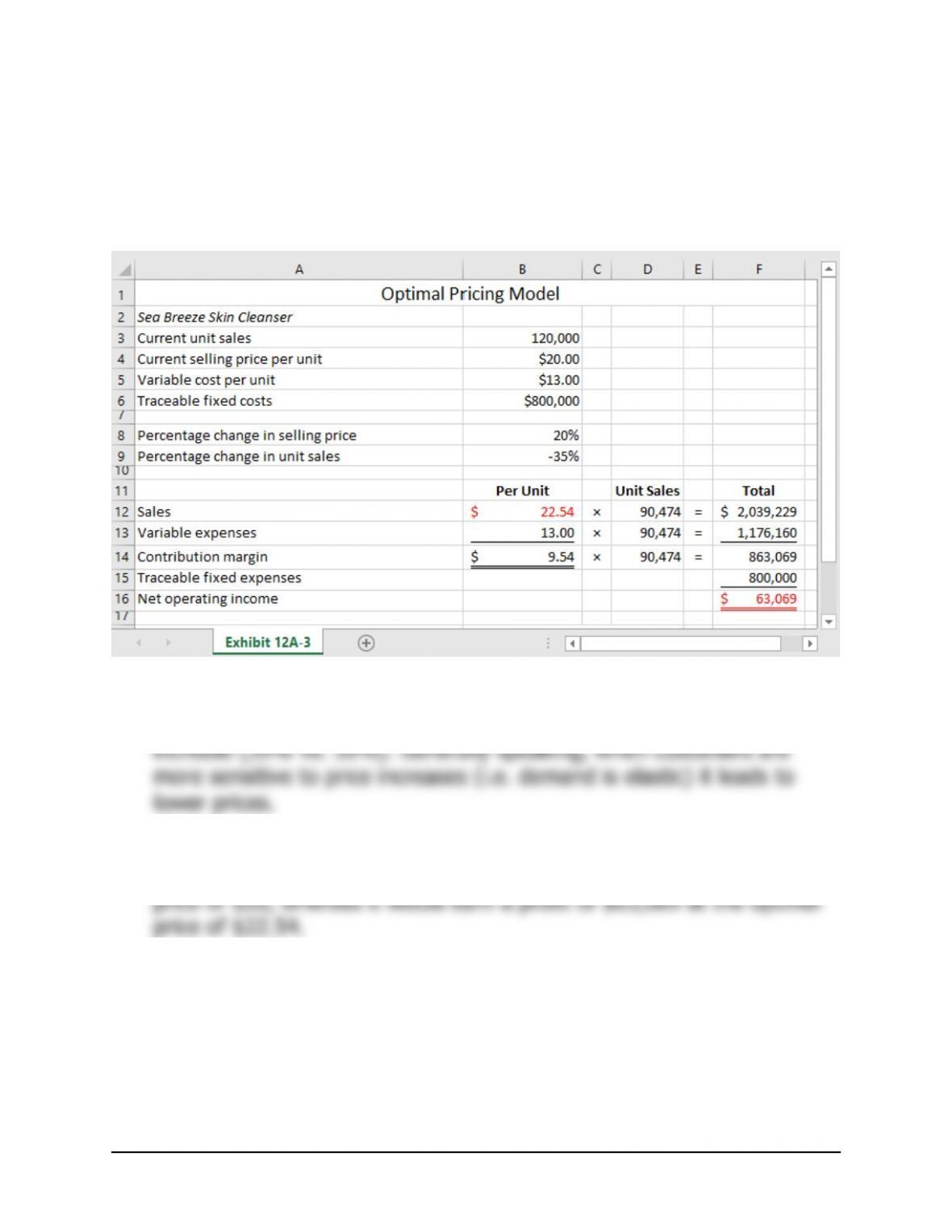

Exercise 12A-5 (continued)

5a. The optimal selling price ($22.54) and optimal profit ($63,069) are as

shown below:

5b. The optimal price in requirement 5a is lower than the price in

requirement 4a because the customers are more sensitive to the price

5c. If unit sales decrease by 35% instead of 30%, the price increase is still

a good idea. The company is currently earning a profit of $40,000 at a

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

84 Managerial Accounting, 16th Edition

Exercise 12A-6 (30 minutes)

1. The absorption cost-plus price of $15,540 is computed as follows:

2. The economic value to the customer (EVC) is computed as follows:

EVC = Reference value + Differentiation value

The differentiation value shown above ($18,400) includes three

components. First, customers who purchase an XP-200 rather than the

competing alternative would avoid the need to buy a second piece of

a 20,000-hour period, computed as follows:

Competin

g

Equipment XP-200

Preventive maintenance cost for 20,000 hours:

Third, customers who purchase an XP-200 rather than the competing

period, computed as follows:

Competin

g

Equipment XP-200

Electricity cost for 20,000 hours:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 85

Exercise 12A-6 (continued)

3. The range of possible prices is as follows:

4. The absorption approach to cost-plus pricing ignores the value that XP-200

offers customers relative to the best available alternative. It is quite possible

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

86 Managerial Accounting, 16th Edition

Exercise 12A-7 (30 minutes)

1. The postal service’s contribution margin (CM) at a price of $8.00 is

computed as follows:

2. The percentage decrease in the selling price and the percentage

increase in unit sales are computed as follows:

Pric

e

V

olum

e

3. The postal service’s contribution margin at a price of $7.00 is computed

as follows:

4. The increase in contribution margin is computed as follows:

5. The postal service would have to sell 92,904 sheets computed as

follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 87

Exercise 12A-7 (continued)

6. The percentage increase is computed as follows:

7. The postal service should not allocate a portion of its common fixed

costs to these two pricing alternatives. Using sales dollars as the

allocation base would cause differing amounts of common fixed costs to

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

88 Managerial Accounting, 16th Edition

Problem 12A-8 (45 minutes)

1. a. Number of pads manufactured each year:

38,400 labor-hours ÷ 2.4 labor-hours per pad = 16,000 pads.

Selling and administrative expenses:

(

)

Required ROI Selling and administrative

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

b. Direct materials ………………………………. $ 10.80

Direct labor ……………………………………. 19.20

Manufacturin

g

overhead ……………………. 30.00

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 89

Problem 12A-8 (continued)

c. The income statement is:

Sales (16,000 pads × $135 per pad) …………. $2,160,000

Cost of

g

oods sold

The company’s ROI computation for the pads will be:

Net Operating Income

ROI =

A

verage Operating Assets

$324,000

=

$1,350,000

= 24%

2. Variable cost per unit:

Direct materials ………………………………………. $10.80

If the company has idle capacity and sales to the retail outlet would not

affect regular sales, any price above the variable cost of $45 per pad

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

90 Managerial Accounting, 16th Edition

Problem 12A-9 (10 minutes)

1. The unit product cost is computed as follows:

Direct materials ………………………………………. $ 7.00

2. The markup percentage is computed as follows:

(

)

Required ROI Selling and administraive

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

3. The selling price is computed as follows:

Unit product cost ………………… $21.25