© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 61

Case 12-29 (45 minutes)

1. As much yarn as possible should be processed into sweaters. Products

should be processed further so long as the added revenues from further

processing are greater than the added costs. In this case, the added

revenues and costs are:

Per Sweater

A

–

A

2. The company should process the wool yarn into sweaters because the

company will gain $2.20 in contribution margin for each spindle of yarn

that is further processed into a sweater. The fixed manufacturing

3. The lowest price the company should accept is $27.80 per sweater. The

simplest approach to this answer is:

A more involved approach to the same answer is to reason as follows:

If the wool yarn is sold outright, then the company will realize a

contribution margin of $9.40 per spindle:

Per Spindle

Sellin

g

price …………………….. $20.00

V

ariable expenses:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

62 Managerial Accounting, 16th Edition

Case 12-29 (continued)

This $9.40 is an opportunity cost. The price of the sweaters must be

high enough to cover this opportunity cost. In addition, the company

must be able to cover all of its variable costs from the time the raw wool

is purchased until the sweater is completed. Therefore, the minimum

price is:

V

ariable costs of producin

g

a spindle of yarn:

A

T

—

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 63

Case 12-30 (90 minutes)

1. The original cost of the facilities at Clayton is a sunk cost and should be

ignored in any decision. The decision being considered here is whether to

continue operations at Clayton. The only relevant costs are the future

facility costs that would be affected by this decision. If the facility were

shut down, the Clayton facility has no resale value. In addition, if the

Clayton facility were sold, the company would have to rent additional

space at the remaining processing centers. On the other hand, if the

The costs that are relevant in the decision to shut down the Clayton

facility are:

In addition, there would be costs of moving the equipment from Clayton

and there might be some loss of sales due to disruption of services. In

2. Haley’s self-interest is to focus on the performance report that probably

plays an instrumental role in how her boss evaluates her performance.

So, even though closing down the Clayton facility would result in a

decline in overall company profits, from Haley’s standpoint it would

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

64 Managerial Accounting, 16th Edition

Case 12-30 (continued)

Financial Performance

After Shutting Down the Clayton Facility

Rocky Mountain Region

Total

Sales …………………………………………………… $50,000,000

Sellin

g

and administrative expenses:

Direct labor ………………………………………… 32,000,000

Variable overhead ………………………………… 850,000

Equipment depreciation …………………………. 3,900,000

If the Clayton facility is shut down, BSC’s profits will decline, employees

will lose their jobs, and customers will at least temporarily suffer some

While Romeros is not a management accountant, the Standards of

Ethical Conduct for Management Accountants still provide useful

guidelines. By recommending closing the Clayton facility, Romeros will

have to violate the Credibility Standard, which requires the disclosure of

In sum, it is difficult to describe the recommendation to close the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 65

Case 12-30 (continued)

It should be noted that the performance report required by corporate

headquarters is likely to lead to other problems such as the one

illustrated here. The arbitrary allocations of corporate and regional

3. Prices should be set ignoring the depreciation on the Clayton facility. As

argued in part (1) above, the real cost of using the Clayton facility is

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

66 Managerial Accounting, 16th Edition

Case 12-31 (90 minutes)

1. The lowest price Wesco could bid for the one-time special order of

20,000 pounds (20 lots) and still exactly cover its incremental

manufacturing costs is calculated as follows:

Direct materials:

A

G-5: 300 pounds per lot × 20 lots = 6,000 pounds.

Substitute BH-3 on a one-for-one basis to its total of 3,500

pounds. If BH-3 is not used in this order, it will be salvaged

DF-6: 175 pounds per lot × 20 lots = 3,500 pounds. Use

3,000 pounds in inventory at $0.60 per pound ($0.70

market price – $0.10 handling charge), and purchase the

remaining 500 pounds (= 3,500 pounds – 3,000 pounds)

T

would have to be used for the remaining 100 hours.

400 DLHs × $14.00 per DLH…………………….………………… 5,600

T

Overhead: This special order will not increase fixed overhead costs.

Therefore, only the variable overhead is relevant.

T

T

–

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 67

Case 12-31 (continued)

2. In this part, we calculate the price for recurring orders of 20,000 pounds

Direct materials: Because the initial order will exhaust existing

inventories of BH-3 and DF-6 and new supplies would have to be

purchased, all raw materials should be charged at their expected

future cost, which is the current market price.

Direct labor: 90% (i.e., 450 DLHs) of the production of a batch can be

done on regular time; but the remaining production (i.e., 50 DLHs) must

be done on overtime.

Overhead: The full manufacturing cost includes both fixed and variable

manufacturing overhead.

Manufacturin

g

overhead applied:

500 DLHs × $13.50 per DLH ……………………………….…. 6,750

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

68 Managerial Accounting, 16th Edition

Case 12-32 (120 minutes)

1. The product margins computed by the accounting department for the

drums and bike frames should not be used in the decision of which

product to make. The product margins are lower than they should be

due to the presence of allocated fixed common costs that are irrelevant

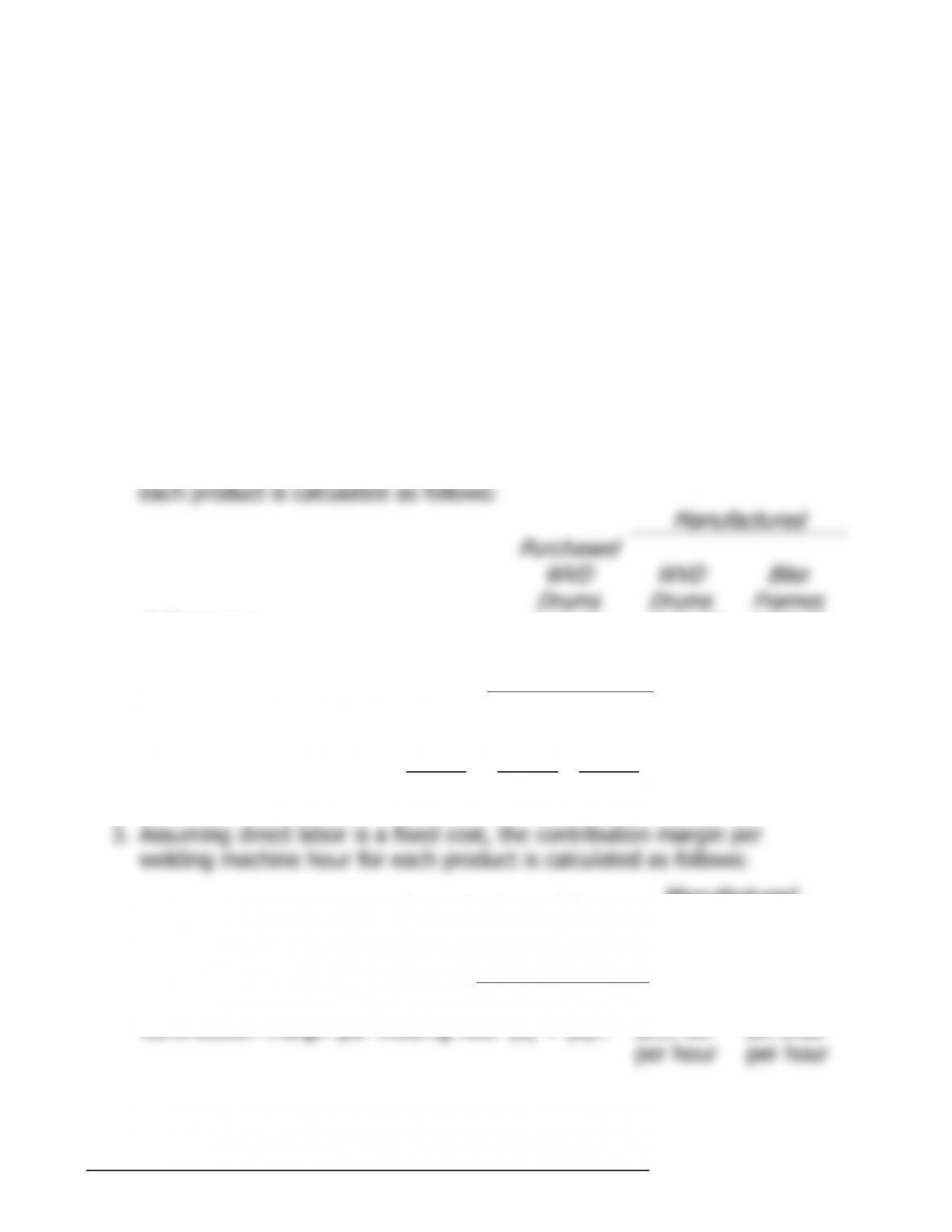

2. Assuming direct labor is a fixed cost, the contribution margin per unit for

each product is calculated as follows:

Manufactured

Purchased

WVD

Drums

WVD

Drums

Bike

Frames

Sellin

g

price ………………………………. $149.00 $149.00 $239.00

V

ariable costs:

Direct materials ……………………….. 138.00 52.10 99.40

T

3. Assuming direct labor is a fixed cost, the contribution margin per

welding machine hour for each product is calculated as follows:

Manufactured

WVD

Drums

Bike

Frames

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 69

Case 12-32 (continued)

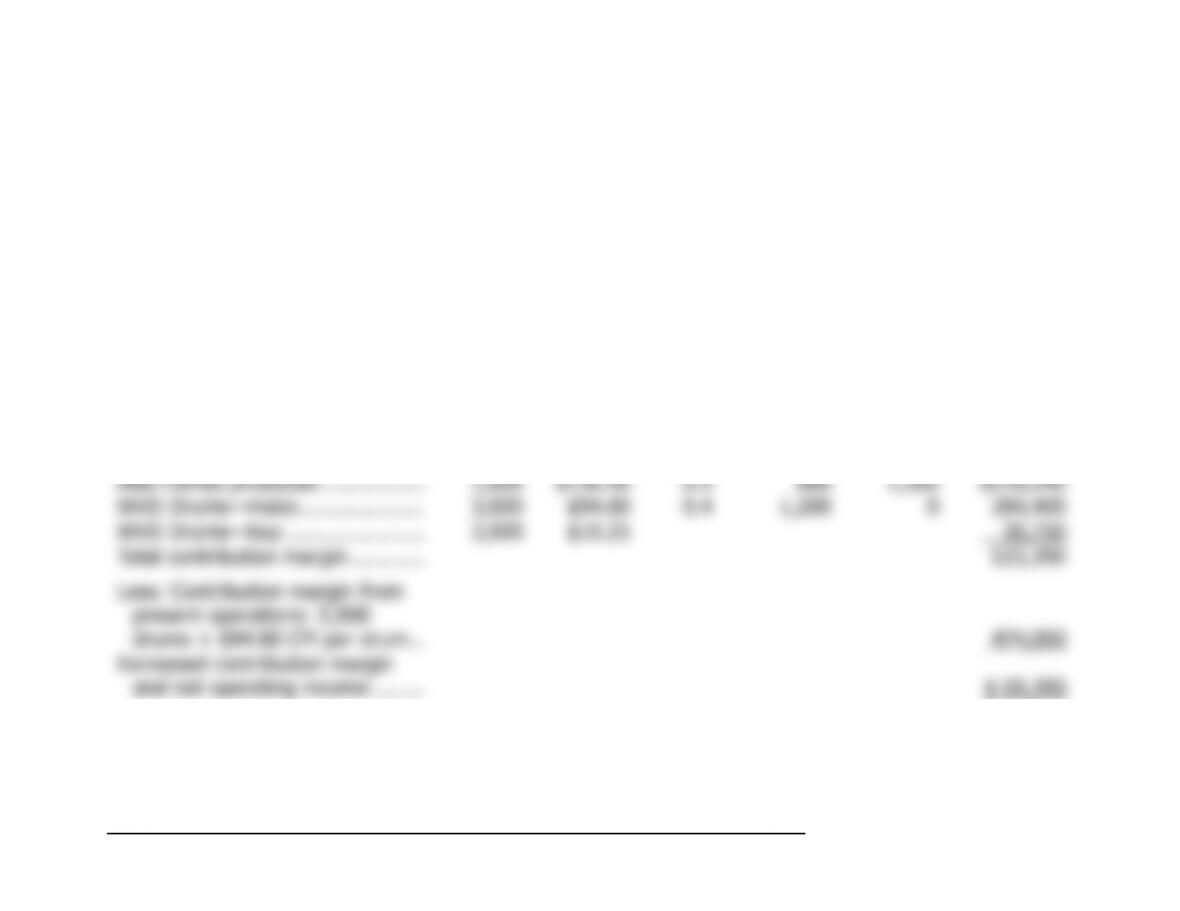

4. Because the contribution margin per unit of the constrained resource (i.e., welding time) is larger

for the bike frames than for the WVD drums, the frames make the most profitable use of the

welding machine (assuming direct labor is a fixed cost). Consequently, the company should

manufacture as many bike frames as possible up to demand and then use any leftover capacity to

produce WVD drums. Buying the drums from the outside supplier can fill any remaining unsatisfied

demand for WVD drums. The necessary calculations are carried out below.

(a) (b) (c) (a) × (c) (a) × (b)

Quantity

Unit

Contri-

bution

Margin

Welding

Time

per Unit

Total

Welding

Time

Balance

of

Welding

Time

Total

Contri-

bution

T

otal hours available ……………… 2,000

—

T

—

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

70 Managerial Accounting, 16th Edition

Case 12-32 (continued)

5. Assuming direct labor is a variable cost, the contribution margin per unit

for each product is calculated as follows:

Manufactured

Purchased

WVD

Drums

WVD

Drums

Bike

Frames

Sellin

g

price ……………………………. $149.00 $149.00 $239.00

V

ariable costs:

g

6.

Assuming direct labor is a variable cost, the contribution margin per

welding hour for each product is calculated as follows:

Manufactured

WVD

Drums

Bike

Frames

Contribution mar

g

in per unit (above) (a)………. $91.20 $107.60

g

T