© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 51

Problem 12-25 (continued)

5. Because the additional capacity would be used to produce the Mike doll,

6. Additional output could be obtained in a number of ways including

working overtime, adding another shift, expanding the workforce,

Note: Some would argue that direct labor is a fixed cost in this situation

and should be excluded when computing the contribution margin per

unit. However, when deciding which products to emphasize, no harm is

done by misclassifying a fixed cost as a variable cost—providing that the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

52 Managerial Accounting, 16th Edition

Problem 12-26 (60 minutes)

1. and 2.

The avoided employee salaries and employment taxes are computed as

follows:

Sales salaries …………………………………… $70,000

Delivery salaries ……………………………….. 4,000

Store mana

g

ement salaries…………………. 9,000

Salary of new mana

g

er ……………………… 11,000

General office salaries ……………………….. 6,000

T

otal employee salaries avoided……………… 100,000

Employment tax rate …………………………… × 15%

T

otal employment taxes avoided…………….. $15,000

3. The simplest approach to the solution is:

Gross mar

g

in lost if the store is closed………… $(316,800)

Costs that can be avoided:

Employee salaries (see requirement 1) …… $100,000

Employment taxes (see requirement 2) …. $15,000

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 53

Problem 12-26 (continued)

Alternative Solution (Total cost approach):

North

Store

Kept

Open

North

Store

Closed

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sellin

g

and administrative

expenses:

Sellin

g

expenses:

Sales salaries ……………………. 70,000 0 70,000

Direct advertisin

g

………………. 51,000 0 51,000

General advertisin

g

…………….. 10,800 10,800 0

Store rent ………………………… 85,000 0 85,000

T

A

dministrative expenses:

Store mana

g

ement salaries ….. 21,000 12,000 9,000

Salary of new mana

g

er ……….. 11,000 0 11,000

General office salaries …………. 12,000 6,000 6,000

Insurance on fixtures and

—

T

T

*See the computation on the prior page.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

54 Managerial Accounting, 16th Edition

Problem 12-26 (continued)

4. Based on the data in requirement (3), the North Store should not be

closed. The company would be $29,800 worse off per quarter if it closed

the North Store. If the store space cannot be subleased or the lease

5. Under these circumstances, the North Store should be closed. The

computations are as follows:

Gross mar

g

in lost if the North Store is closed (see

requirement 3) ………………………………………………… $(316,800)

Gross mar

g

in

g

ained from the East Store: $720,000 ×

Problem 12-27 (60 minutes)

1. The incremental revenue per jar from further processing of the Grit 337

is:

Sellin

g

price of the silver polish, per

j

ar…………….. $4.00

g

j

2. The incremental contribution margin per jar:

Incremental revenue per

j

ar…………………………… $3.50

Incremental variable costs per

j

ar:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

56 Managerial Accounting, 16th Edition

Problem 12-27 (continued)

3. Only the cost of advertising and the cost of the production supervisor

are avoidable if production of the silver polish is discontinued.

Therefore, the number of jars of silver polish that must be sold each

month to justify continued processing of the Grit 337 into silver polish

is:

If 10,000 jars of silver polish can be sold each month, the company

would be indifferent between selling it or selling all of the Grit 337 as a

cleaning powder. If the sales of the silver polish are greater than 10,000

4. and 5.

The financial advantage (disadvantage) is computed as follows:

9,000

jars

1

1

,50

0

jars

Incremental contribution mar

g

in per

j

ar (a)…

.

$0.70 $0.70

g

Incremental contribution mar

g

in ………………

.

$6,300 $8,050

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 57

Problem 12-28 (60 minutes)

1. The $2.80 per drum general overhead cost is not relevant to the

decision because this cost will be the same regardless of whether the

company decides to make or buy the drums. Also, the present

Differential Costs

Per Drum

Total Differential Costs—

60,000 Drums

Make Buy Make Buy

Outside supplier

’

s price .. $18.00 $1,080,000

Direct materials …………. $10.35 $621,000

Direct labor

($6.00 × 70%) ……….. 4.20 252,000

V

ariable overhead

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

58 Managerial Accounting, 16th Edition

Problem 12-28 (continued)

2. Notice that unit costs for both supervision and equipment rental

decrease with the greater volume because these fixed costs are spread

over more units.

Differential

Cost Per Drum

Total Differential Cost—

75,000 Drums

Make Buy Make Buy

Outside supplier

’

s price …. $18.00 $1,350,000

V

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 59

Problem 12-28 (continued)

3. Again, notice that the unit costs for both supervision and equipment

rental decrease with the greater volume of units.

Differential

Costs Per Drum

Total Differential Cost—

90,000 Drums

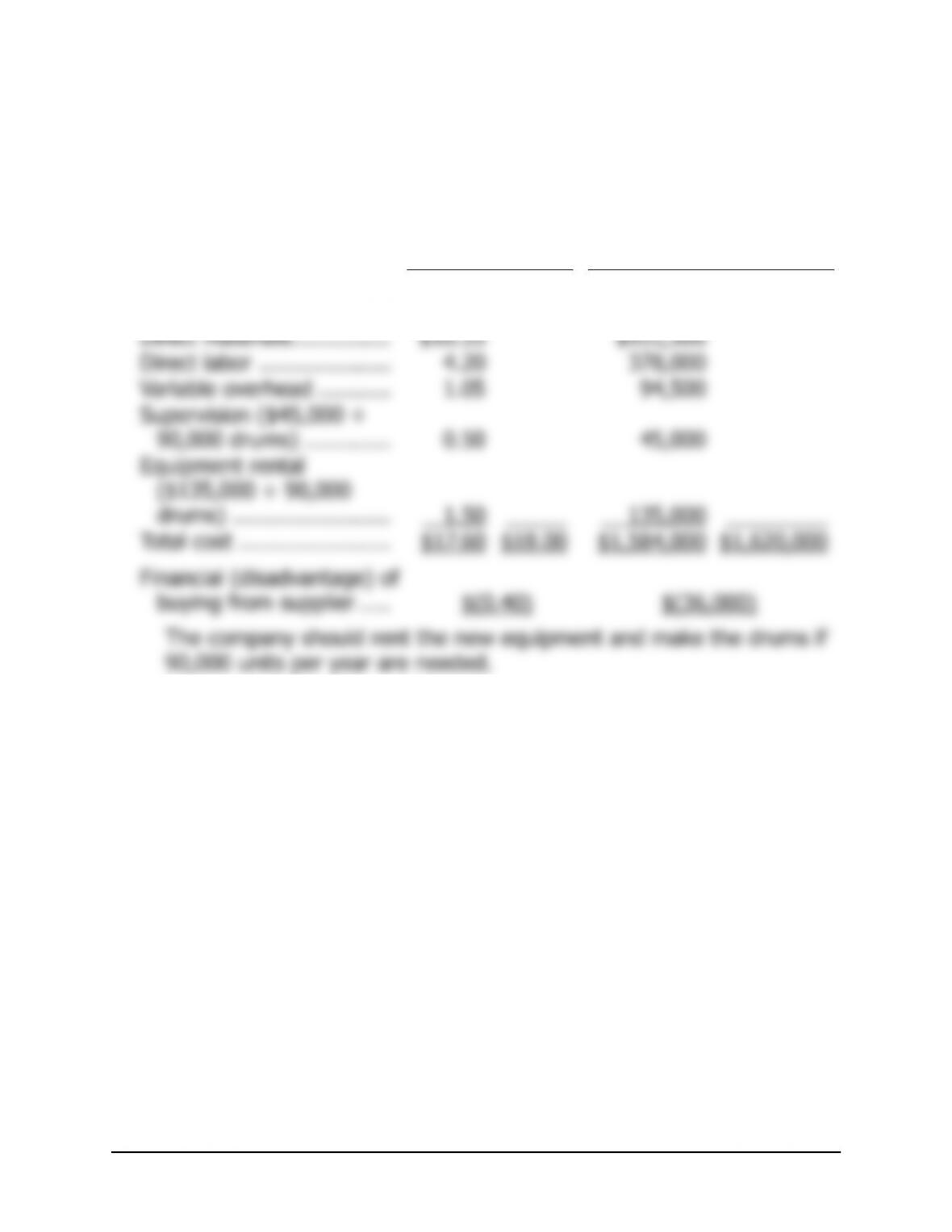

Make Buy Make Buy

Outside supplier

’

s price …. $18.00 $1,620,000

V

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

60 Managerial Accounting, 16th Edition

Problem 12-28 (continued)

4. Other factors that the company should consider include:

Will volume in future years increase, or will it remain constant at

Can quality control be maintained if the drums are purchased from

Can the company begin making the drums again if the supplier

What is the labor outlook in the supplier’s industry (e.g., are frequent

If the outside supplier’s offer is accepted and the need for drums