© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 41

Problem 12-21 (30 minutes)

1. Contribution mar

g

in lost if the fli

g

ht is

discontinued …………………………………………..… $(12,950)

Fli

g

ht costs that can be avoided if the fli

g

ht is

discontinued:

The following costs are not relevant to the decision:

Cost Reason

Salaries, fli

g

ht crew Fixed annual salaries, which will

not change.

g

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

42 Managerial Accounting, 16th Edition

Problem 12-21 (continued)

Alternative Solution:

Keep the

Flight

Drop the

Flight

Difference:

Net

Operating

Income

Increase or

(Decrease)

T

icket revenue ……………………………….. $14,000 $ 0 $(14,000)

V

ariable expenses …………………………… 1,050 0 1,050

Contribution mar

g

in ………………………… 12,950 0 (12,950)

Less fli

g

ht expenses:

Salaries, fli

g

ht crew ………………………. 1,800 1,800 0

T

2. The goal of increasing the seat occupancy could be obtained by

eliminating flights with a lower-than-average seat occupancy. By

eliminating these flights and keeping the flights with a higher-than-

average seat occupancy, the overall average seat occupancy for the

company as a whole would be improved. This could reduce profits in at

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 43

Problem 12-22 (30 minutes)

1. Because the fixed costs will not change as a result of the order, they are

not relevant to the decision. The cost of the new machine is relevant,

and this cost will have to be recovered by the current order because

there is no assurance of future business from the retail chain.

Unit

Total—

5,000 units

Sales from the order ($50 × 84%) …………………. $42 $210,000

Less costs associated with the order:

Direct materials ……………………………………….. 15 75,000

T

2. Sales from the order:

Reimbursement for costs of production (variable

production costs of $26 plus fixed manufacturing

overhead cost of $9 = $35 per unit; $35 per unit ×

5,000 units) …………………………………………………. $175,000

Fixed fee ($1.80 per unit × 5,000 units)……………….. 9,000

T

—

3. Sales:

From the U.S. Army (above)………………………………. $184,000

From re

g

ular channels ($50 per unit × 5,000 units) … 250,000

Net decrease in revenue ………………………………..……. (66,000)

Less variable sellin

g

expenses avoided if the Army

’

s

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

44 Managerial Accounting, 16th Edition

Problem 12-23 (60 minutes)

1. The starting point for answering requirement 1 is separating the

manufacturing overhead per unit of $1.40 into its variable and fixed

components. The variable manufacturing overhead per box of Chap-Off

would be $0.50, as shown below:

The avoidable manufacturing cost per box of Chap-Off is computed as

follows:

Cost avoided by purchasin

g

the tubes:

2. The financial (disadvantage) per box of Chap-Off is computed as

follows:

Financial (disadvanta

g

e) per box of Chap-Off ……………. $(0.20)

3. The financial (disadvantage) of outsourcing 100,000 boxes of Chap-Off

is computed as follows:

g

g

4. Silven should make the tubes because the price paid to the supplier

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 45

Problem 12-23 (continued)

5. The maximum purchase price would be $1.15 per box. The company

would not be willing to pay more than this amount because the $1.15

6. At a volume of 120,000 boxes, the company should buy the tubes. The

computations are:

Cost of makin

g

120,000 boxes of tubes:

Cost of buyin

g

120,000 boxes of tubes:

7. Under these circumstances, the company should make 100,000 boxes of

tubes and purchase the remaining 20,000 boxes of tubes from the

outside supplier. The costs would be as follows:

g

g

8. Management should take into account at least the following additional

factors:

The ability of the supplier to meet required delivery schedules.

The quality of the tubes purchased from the supplier.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

46 Managerial Accounting, 16th Edition

Problem 12-24 (45 minutes)

1. Product RG-6 has a contribution margin of $8 per unit (= $22 – $14). If

the plant closes, this contribution margin will be lost on the 16,000 units

(= 8,000 units per month × 2 months) that could have been sold during

the two-month period. However, the company will be able to avoid some

fixed costs as a result of closing down. The analysis is:

Contribution mar

g

in lost by closin

g

the plant for

2. No, the company should not close the plant; it should continue to

operate at the reduced level of 8,000 units produced and sold each

month. Closing will result in a $40,000 greater loss over the two-month

Problem 12-24 (continued)

Alternative Solution:

Plant

Kept

Open

Plant

Closed

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sales (8,000 units × $22 per

V

Less fixed costs:

Fixed manufacturin

g

overhead costs ($150,000

× 2) ………………………….. 300,000 210,000 90,000

Fixed sellin

g

costs

($30,000 × 2) ……………… 60,000 54,000 * 6,000

T

otal fixed costs ……………….. 360,000 264,000 96,000

Net operatin

g

loss before

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

48 Managerial Accounting, 16th Edition

Problem 12-24 (continued)

3. Birch Company will be indifferent if it can sell 11,000 units over the two-

month period. The computations are:

Cost avoided by closin

g

the plant for two months

Verification:

Operate at

11,000

Units for

Two

Months

Close for

Two

Months

Sales (11,000 units × $22 per unit) ………. $ 242,000 $ 0

V

ariable expenses (11,000 units × $14

per unit) ………………………………………. 154,000 0

Contribution mar

g

in ………………………….. 88,000 0

Fixed expenses:

Manufacturin

g

overhead ($150,000 and

T

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 49

Problem 12-25 (60 minutes)

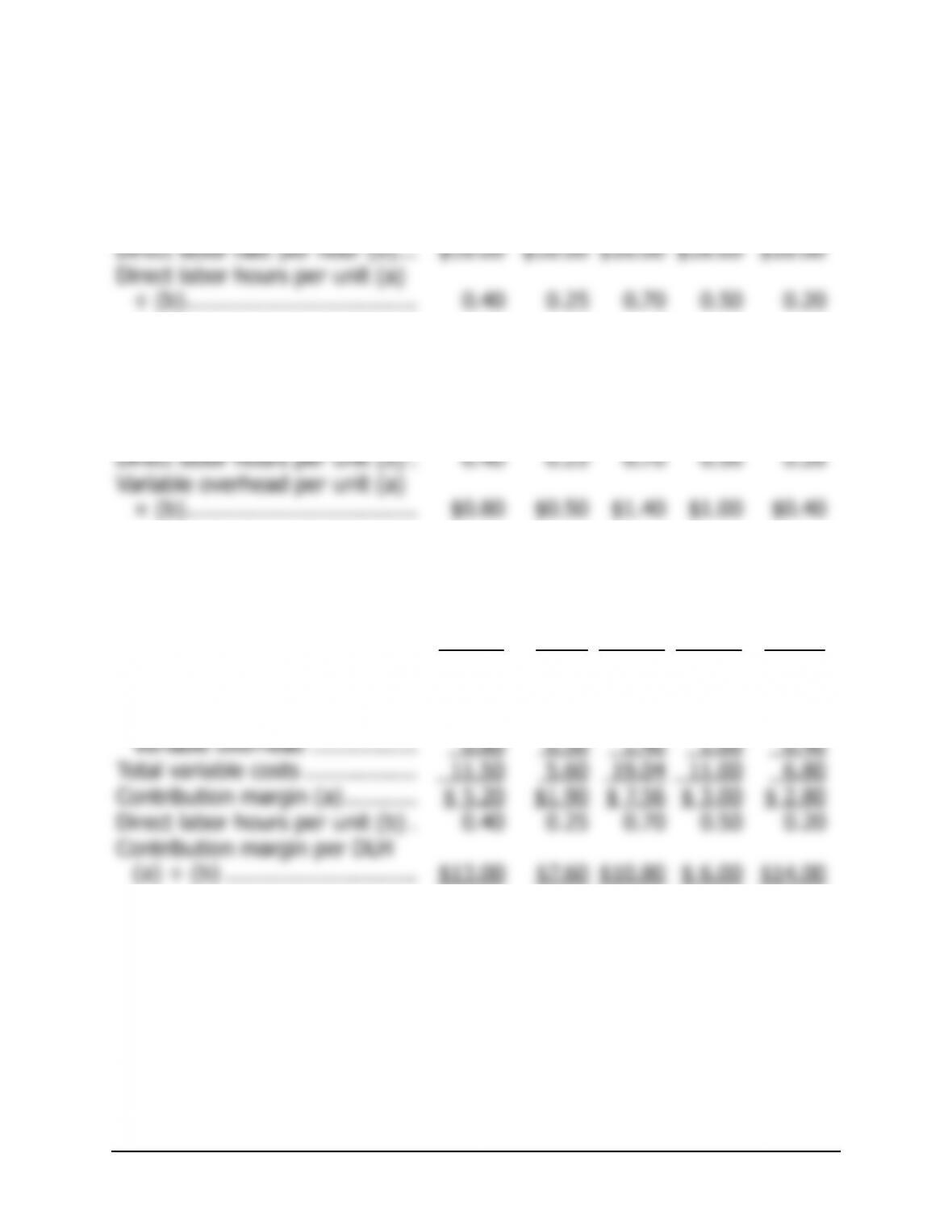

1.

Debbie Trish Sarah Mike

Sewin

g

Kit

Direct labor cost per unit (a)…. $6.40 $4.00 $11.20 $8.00 $3.20

2 .

Debbie Trish Sarah Mike

Sewin

g

Kit

V

ariable overhead per hour (a) $2.00 $2.00 $2.00 $2.00 $2.00

V

3 .

Debbie Trish Sarah Mike

Sewin

g

Kit

Sellin

g

price ……………………… $16.70 $7.50 $26.60 $14.00 $9.60

V

ariable costs:

Direct materials ……………….. 4.30 1.10 6.44 2.00 3.20

Direct labor …………………….. 6.40 4.00 11.20 8.00 3.20

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

50 Managerial Accounting, 16th Edition

Problem 12-25 (continued)

4. The first step is to compute how many direct labor-hours would be

committed to each of the five products as follows:

A

mount of constrained resource available…………….. 130,000 hours

Less: Hours required for production of 325,000 units

of the Sewing Kit @0.20 hours per unit ……………. 65,000 hours

Remainin

g

constrained resource available…………….. 65,000 hours

Less: Hours required for production of 50,000 units

g

g

g

The second step is to multiple the direct labor-hours committed to each

product by its respective contribution margin per direct labor–hour as

shown below:

Sewin

g

Kit Debbie Sarah Trish Mike

Contribution

margin per DLH

T

The highest total contribution margin that the company can earn is

g