© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 31

Exercise 12-14 (20 minutes)

1.

A

vera

g

e fixed cost per mile ($3,200* ÷ 10,000 miles)….. $0.32

V

ariable operatin

g

cost per mile ……………………………… 0.14

A

vera

g

e cost per mile ………………………………………..…. $0.46

T

2. The variable operating cost is relevant in this situation. The depreciation

is not relevant because it is a sunk cost. However, any decrease in the

resale value of the car due to its use is relevant. The automobile tax and

3. When figuring the incremental cost of the more expensive car, the

relevant costs include the purchase price of the new car (net of the

resale value of the old car) and the increases in the fixed costs of

insurance and automobile tax and license. The original purchase price of

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

32 Managerial Accounting, 16th Edition

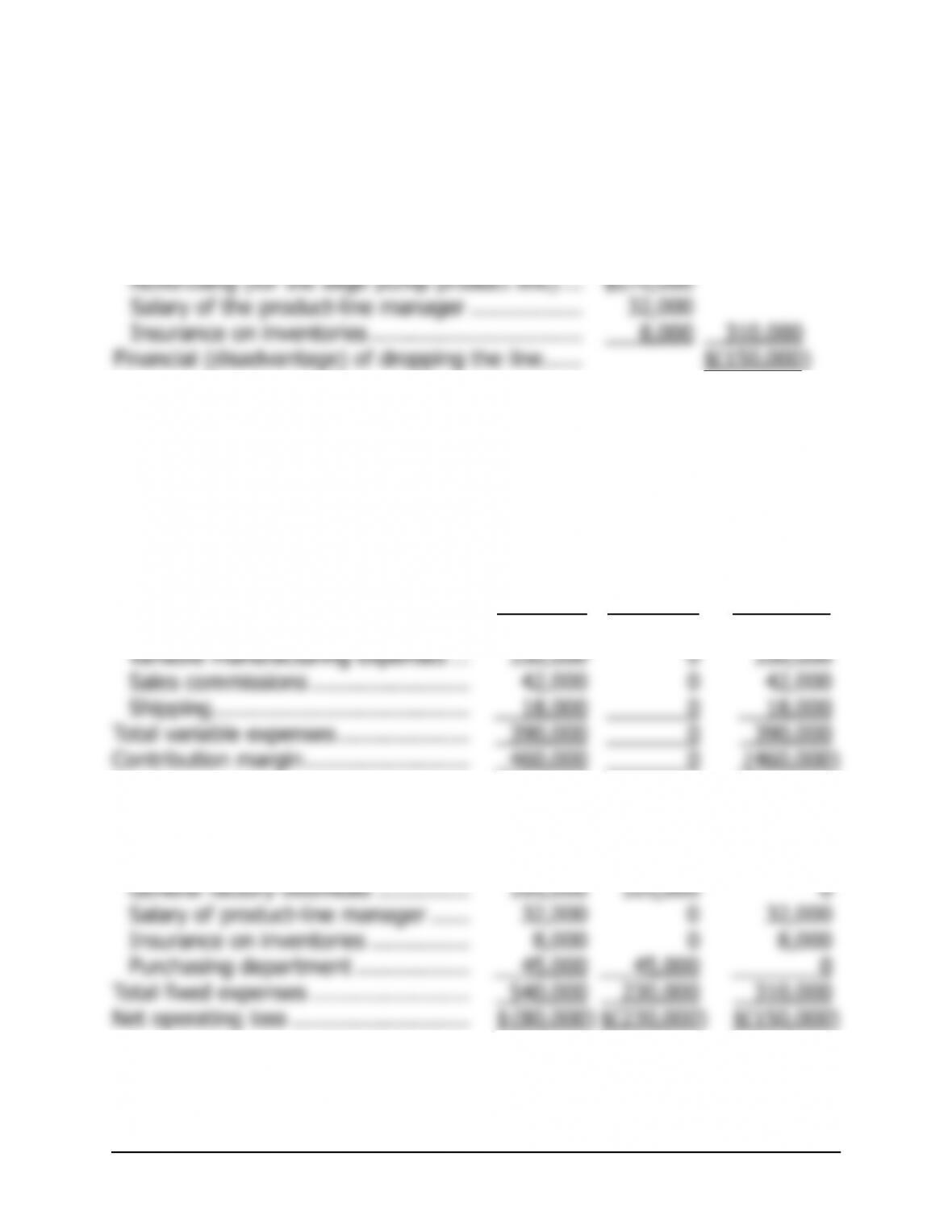

Exercise 12-15 (30 minutes)

The financial (disadvantage) of discontinuing the bilge pump product line is

computed as follows:

Contribution mar

g

in lost if the line is dropped …. $(460,000)

Fixed costs that can be avoided:

A

g

g

g

The same solution can be obtained by preparing comparative income

statements:

Keep

Product

Line

Drop

Product

Line

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sales ………………………………………. $850,000 $ 0 $(850,000)

V

ariable expenses:

T

g

Fixed expenses:

A

dvertisin

g

(for the bil

g

e pump

product line) ………………………… 270,000 0 270,000

Depreciation of equipment…………. 80,000 80,000 0

g

T

$

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 33

Exercise 12-16 (30 minutes)

1. The relevant costs of a hunting trip would be:

T

ravel expense (100 miles @ $0.21 per mile) $21

This answer assumes that Bill would not be drinking the bottle of

The money lost in the poker game is not relevant because Bill would

2. If Bill gets lucky and bags another two ducks, all of his costs are likely to

be the same as they were on his last trip. Therefore, it doesn’t cost him

3. In a decision of whether to give up hunting entirely, more of the costs

listed by John are relevant. If Bill did not hunt, he would not need to

pay for: gas, oil, and tires; shotgun shells; the hunting license; and the

These three requirements illustrate the slippery nature of costs. A cost

that is relevant in one situation can be irrelevant in the next. None of

the costs are relevant when we compute the cost of bagging two

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

34 Managerial Accounting, 16th Edition

Exercise 12-17 (10 minutes)

Contribution mar

g

in lost if the Linens Department is dropped:

Lost from the Linens Department …..……………………………… $(600,000)

Lost from the Hardware Department (10% × $2,100,000) ….. (210,000)

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 35

Problem 12-18 (60 minutes)

1. Sellin

g

price per unit ……………………………………. $32

V

ariable expenses per unit…………………………….. 18 *

Contribution mar

g

in per unit ………………………….. $14

*$10.00 + $4.50 + $2.30 + $1.20 = $18.00

Yes, the increase in fixed selling expenses would be justified.

2.

V

ariable manufacturin

g

cost per unit ……………….. $16.80 *

Import duties per unit ………………………………….. 1.70

3. The relevant cost is $1.20 per unit, which is the variable selling expense

per Dak. Because the irregular units have already been produced, all

production costs (including the variable production costs) are sunk. The

4. If the plant operates at 30% of normal levels, then only 3,000 units will

be produced and sold during the two-month period:

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

36 Managerial Accounting, 16th Edition

Problem 12-18 (continued)

Given this information, the simplest approach to solving 4a, 4b, and 4c

is:

Contribution mar

g

in lost if the plant is closed

(3,000 units × $14 per unit) …..…………………. $(42,000)

Fixed costs that can be avoided if the plant is

closed:

Some students will take a longer approach such as that shown below:

Continue

to

Operate

Close the

Plant

Fixed expenses:

Fixed manufacturin

g

overhead cost:

$300,000 × 2/12 …………………………….. 50,000

$300,000 × 2/12 × 60% ………………….. 30,000

Fixed sellin

g

expense:

4d. The company should not close the plant for two months because it will

g

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 37

Problem 12-18 (continued)

5. The relevant costs are those that can be avoided by purchasing from the

outside supplier. These costs are:

V

ariable manufacturin

g

cost per unit……………………… $16.80

Fixed manufacturin

g

overhead cost ($300,000 × 75%

V

A

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

38 Managerial Accounting, 16th Edition

Problem 12-19 (60 minutes)

1. The financial (disadvantage) of discontinuing the Housekeeping program

is calculated as follows:

Contribution mar

g

in lost if the Housekeepin

g

program is dropped …………………………………… $(80,000)

Depreciation on the van is a sunk cost and the van has no salvage value

since it would be donated to another organization. The general

The same result can be obtained with the alternative analysis below:

Current

Total

Total If

House-

keepin

g

Is

Dropped

Difference:

Net

Operating

Income

Increase or

(Decrease)

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 39

Problem 12-19 (continued)

2. To give the administrator of the entire organization a clearer picture of

the financial viability of each of the organization’s programs, the general

administrative overhead should not be allocated. It is a common cost

that should be deducted from the total program segment margin. A

better income statement would be:

Total

Home

Nursing

Meals On

Wheels

House-

keeping

Revenues ………………….…… $900,000 $260,000 $400,000 $240,000

V

ariable expenses ……………. 490,000 120,000 210,000 160,000

Contribution mar

g

in …………. 410,000 140,000 190,000 80,000

T

raceable fixed expenses:

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

40 Managerial Accounting, 16th Edition

Problem 12-20 (15 minutes)

1.

Per 16-Ounce

T-Bone

Sales from further processin

g

:

Sales price of one filet mi

g

non (6 ounces ×

$12.00 per pound ÷ 16 ounces per pound) … $4.50

Sales price of one New York cut (8 ounces ×

2. The T-bone steaks should be processed further into the filet mignon and

the New York cut. The $4.15 “profit” per pound shown in the text is not