© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 91

Problem 12A-10 (45 minutes)

1. The unit product cost is computed as follows:

Direct materials …………………………………………….. $ 4.00

Direct labor ………………………………………………….. 3.00

2. The markup percentage is computed as follows:

(

)

Required ROI Selling and administraive

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

3. The selling price is computed as follows:

Unit product cost ………………… $13.50

4. The revised unit product cost is computed as follows:

Direct materials …………………………………………….. $ 4.00

Direct labor ………………………………………………….. 3.00

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

92 Managerial Accounting, 16th Edition

Problem 12A-10 (continued)

4. continued

The net operating income at a sales volume of 10,000 units is computed

as follows:

Sales (10,000 units × $20.25 per unit)…………. $202,500

Cost of

g

oods sold (10,000 units × $14.60 per

unit) ………………………………………………….. 146,000

The return on investment (ROI) at a sales volume of 10,000 units is

computed as follows:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 93

Problem 12A-10 (continued)

5. The revised markup percentage would be computed as follows:

(

)

Required ROI Selling and administraive

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

The revised selling price would be computed as follows:

It is quite possible that customers will be displeased with the price

increase of $2.25 per unit (= $22.50 per unit – $20.25 per unit). This

may cause sales volume to drop below 10,000 units, thereby further

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

94 Managerial Accounting, 16th Edition

Problem 12A-11 (45 minutes)

1. Pro

j

ected sales (100 machines × $4,950 per machine) . $495,000

T

ar

g

et cost per machine ($405,000 ÷ 100 machines) … $4,050

Less National Restaurant Supply’s variable sellin

g

cost

2. The relation between the purchase price of the machine and ROI can

be developed as follows:

Total projected sales – Total cost

ROI = Investment

The above formula can be used to compute the ROI for purchase prices

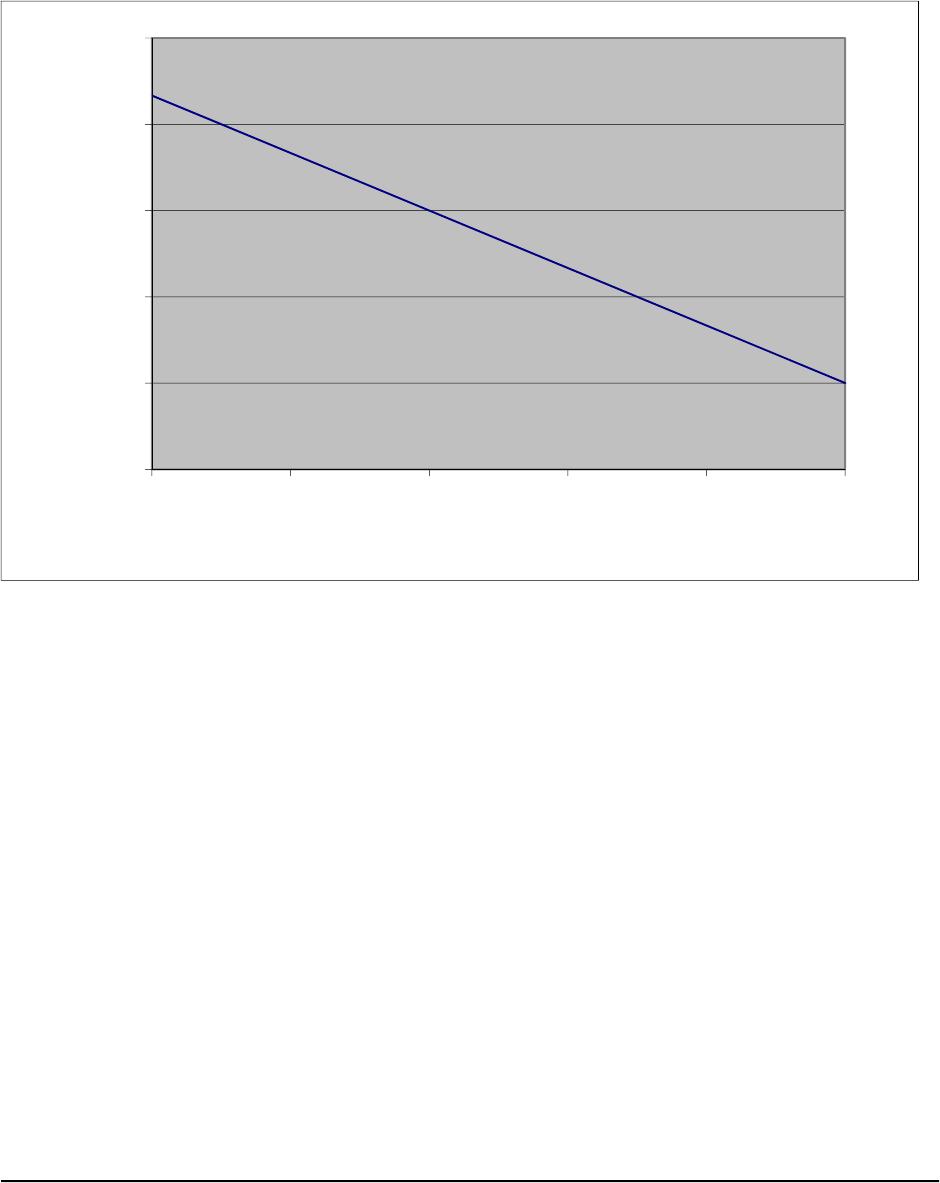

between $3,000 and $4,000 (in increments of $100) as follows:

Purchase price ROI

$3,000 21.7%

$3,100 20.0%

$3,200 18.3%

$3,300 16.7%

T

g

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 95

Problem 12A-11 (continued)

Using the above data, the relation between purchase price and ROI can

be plotted as follows:

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

$3,000 $3,200 $3,400 $3,600 $3,800 $4,000

Realized ROI

Purchase price

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

96 Managerial Accounting, 16th Edition

Problem 12A-11 (continued)

3. A number of options are available in addition to simply giving up on

adding the new sorbet machines to the company’s product lines. These

options include:

• Check the projected unit sales figures. Perhaps more units could be

• Modify the selling price. This does not necessarily mean increasing the

• Improve the selling process to decrease the variable selling costs.

• Rethink the investment that would be required to carry this new

• Does the company really need a 15% ROI? Does it cost the company