© The McGraw-Hill Companies, Inc., 2018 All rights reserved.

Solutions Manual, Chapter 12 1

Chapter 12

Differential Analysis: The Key to Decision

Making

Solutions to Questions

12-1 A relevant cost is a cost that differs in

12-2 An incremental cost (or benefit) is the

change in cost (or benefit) that will result from

some proposed action. An opportunity cost is

12-3 No. Variable costs are relevant costs

12-5 No. A variable cost is a cost that varies

in total amount in direct proportion to changes

12-6 No. Only those future costs that differ

12-7 Only those costs that would be avoided

12-8 Not necessarily. An apparent loss may

be the result of allocated common costs or of

sunk costs that cannot be avoided if the product

as a result of dropping the product is less than

that situation the product may be retained if it

promotes the sale of other products.

12-9 Allocations of common fixed costs can

12-10 If a company decides to make a part

internally rather than to buy it from an outside

products and get them into the hands of

customers could be a constraint. Some examples

are machine time, direct labor time, floor space,

affected, profits are maximized when the total

contribution margin is maximized. A company

12-13 Joint products are two or more products

that are produced from a common input. Joint

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

2 Managerial Accounting, 16th Edition

among joint products for decision-making

purposes. If joint costs are allocated among the

joint products, then managers may think they

are avoidable costs of the end products.

12-16 Most costs of a flight are either sunk

costs, or costs that do not depend on the

number of passengers on the flight.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 3

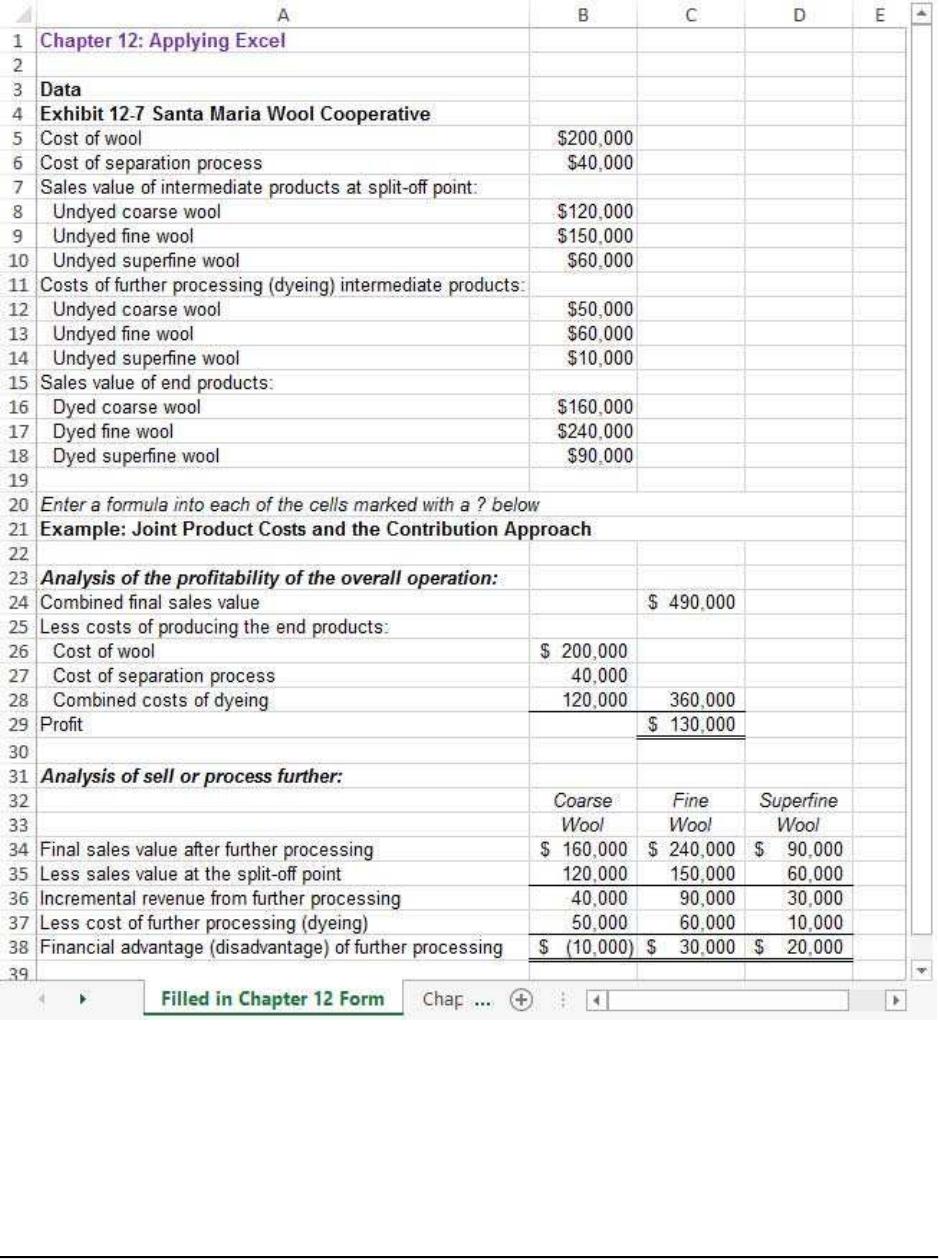

Chapter 12: Applying Excel

The completed worksheet is shown below.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

4 Managerial Accounting, 16th Edition

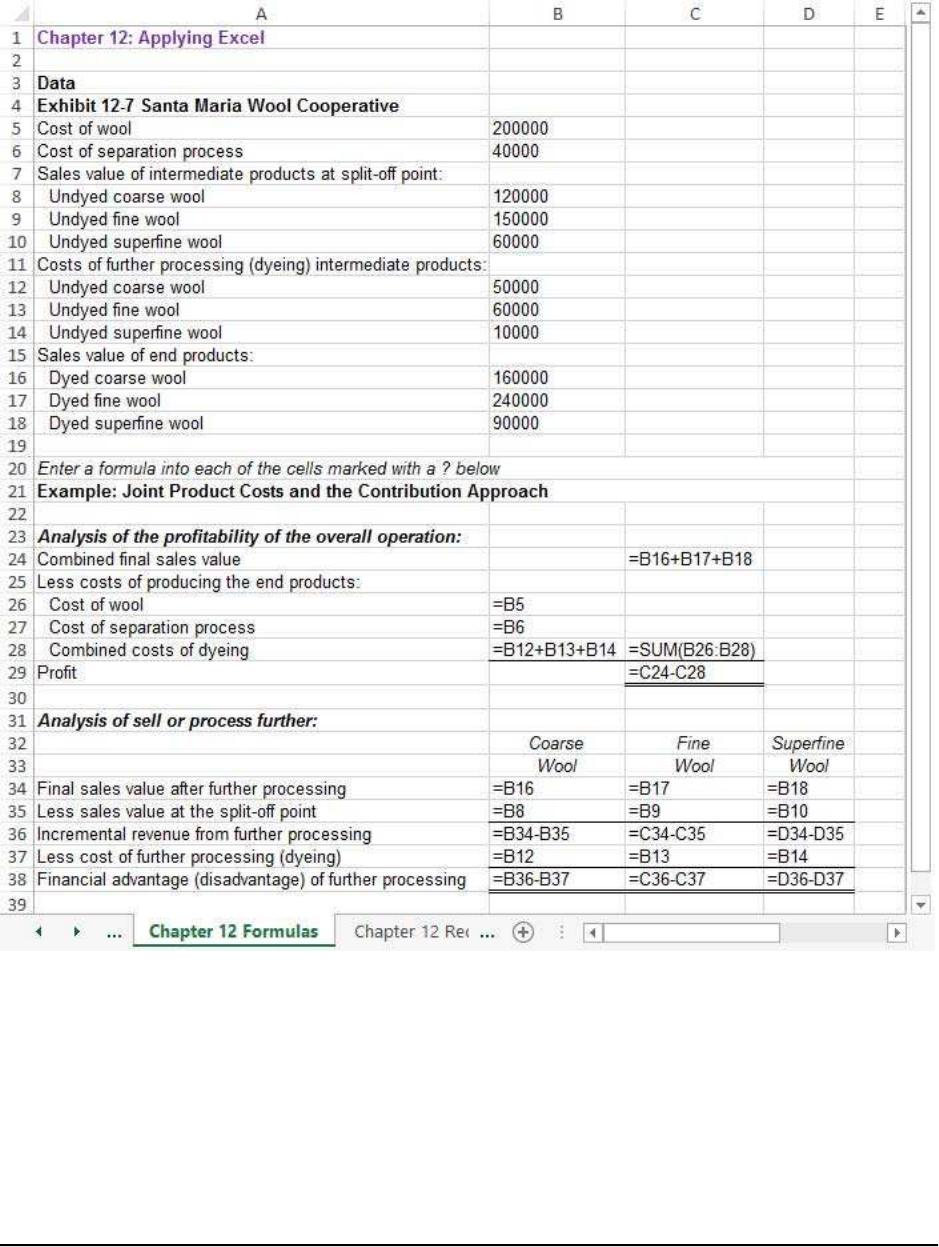

Chapter 12: Applying Excel (continued)

The completed worksheet, with formulas displayed, is shown below.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 5

Chapter 12: Applying Excel (continued)

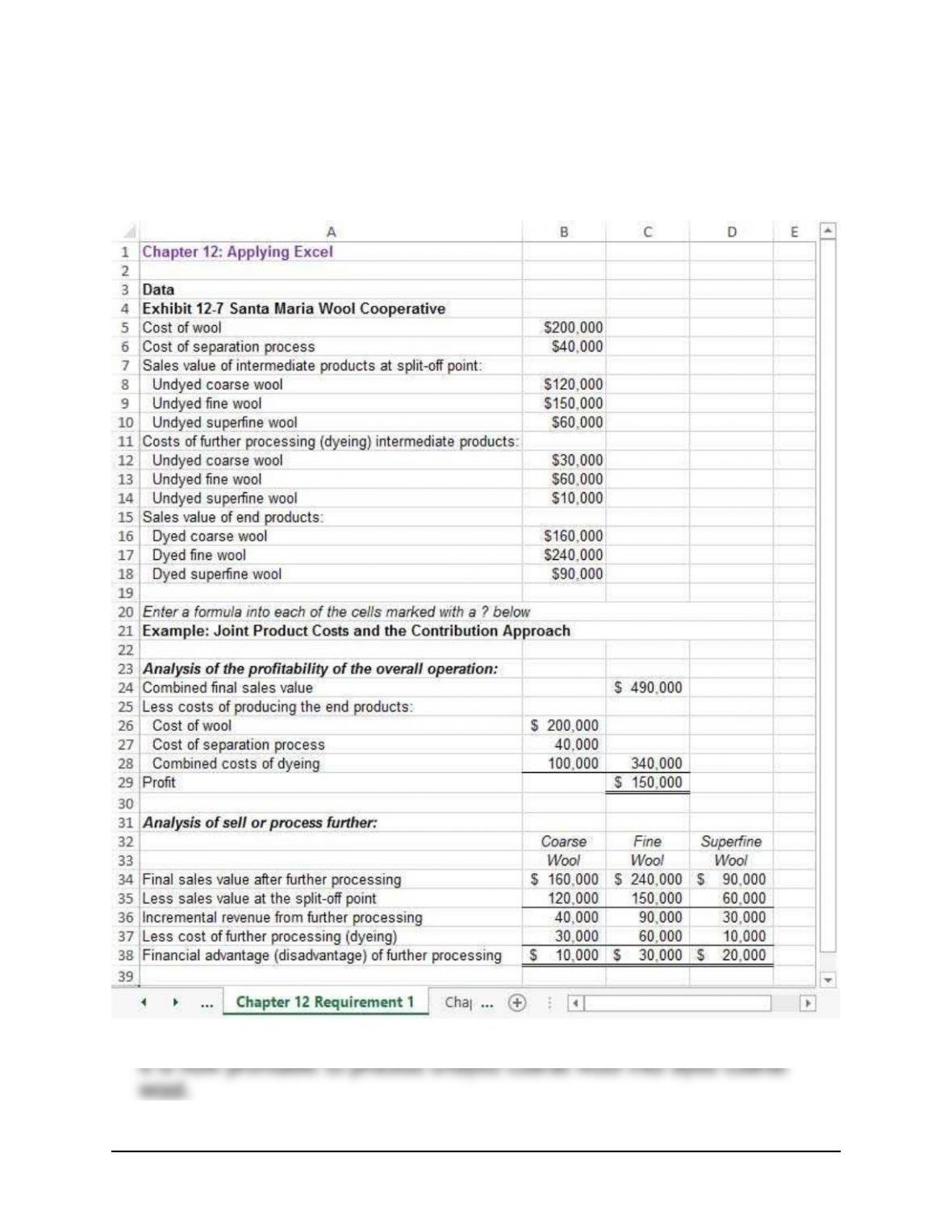

1. With the change in the cost of further processing undyed course wool,

the result is:

With the reduction in the cost of further processing undyed coarse wool,

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

6 Managerial Accounting, 16th Edition

Chapter 12: Applying Excel (continued)

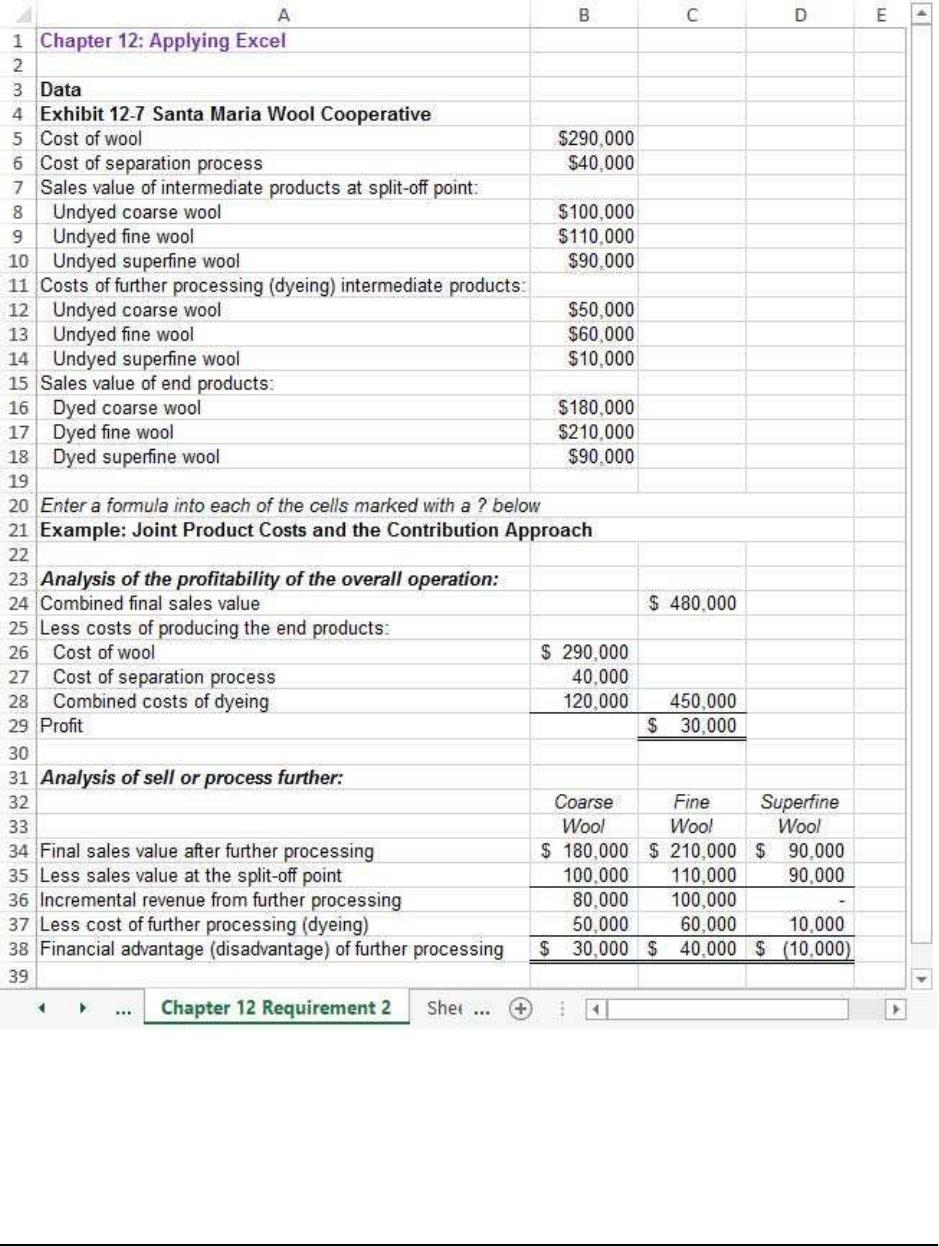

2. With the revised data, the worksheet should look like this:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 7

Chapter 12: Applying Excel (continued)

a. The profit of the overall operation is now $30,000 if all intermediate

b. The financial advantage (disadvantage) from further processing each

c. To maximize profit, the company should process undyed coarse wool

into dyed coarse wool and undyed fine wool into dyed fine wool.

However, undyed superfine wool should be sold as is rather than

processed into dyed superfine wool. If this plan is followed, the

overall profit of the company should be $40,000 as shown below:

Combined sales value

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

8 Managerial Accounting, 16th Edition

The Foundational 15

1. The total traceable fixed manufacturing overhead for Alpha and Beta is

computed as follows:

A

lph

a

Bet

a

2. The total common fixed expenses is computed as follows:

A

lph

a

Bet

a

Common fixed expenses per unit (a) ……… $15 $10

3. The financial advantage of accepting the order is computed as follows:

Per Total

Unit 10,000 units

Incremental revenue ………………………. $80 $800,000

Incremental costs:

Variable costs:

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 12 9

The Foundational 15 (continued)

4. The financial (disadvantage) is computed as follows:

Per Total

Unit 5,000 units

Incremental revenue ………………………. $39 $195,000

Incremental costs:

Variable costs:

5. The financial (disadvantage) is computed as follows:

Incremental revenue

(10,000 units × $80 per unit) (a) …………

.

$800,000

Incremental variable costs:

Direct materials (5,000 units × $30

.

Note to instructors: There will be additional sales of 10,000 units to the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

10 Managerial Accounting, 16th Edition

The Foundational 15 (continued)

6. The financial (disadvantage) of dropping the Beta product line is

computed as follows:

Contribution mar

g

in lost if the Beta product line is

dropped* ……………………………………………………….. $(3,600,000)

T

raceable fixed manufacturin

g

overhead ………………….. 1,800,000

7. The financial advantage of dropping the Beta product line is computed

as follows:

Contribution mar

g

in lost if the Beta product line is

dropped* ……………………………………………………….

.

$(1,600,000)

T

g

.

8. The financial advantage of dropping the Beta product line is computed

as follows:

Contribution mar

g

in lost if the Beta product line is

dropped* ……………………………………………………….

.

$(2,400,000)

T

raceable fixed manufacturin

g

overhead ………………….

.

1,800,000

g