Learning

and

Growth

Internal

Business

Customer

Financial

Case 11-23 (60 minutes)

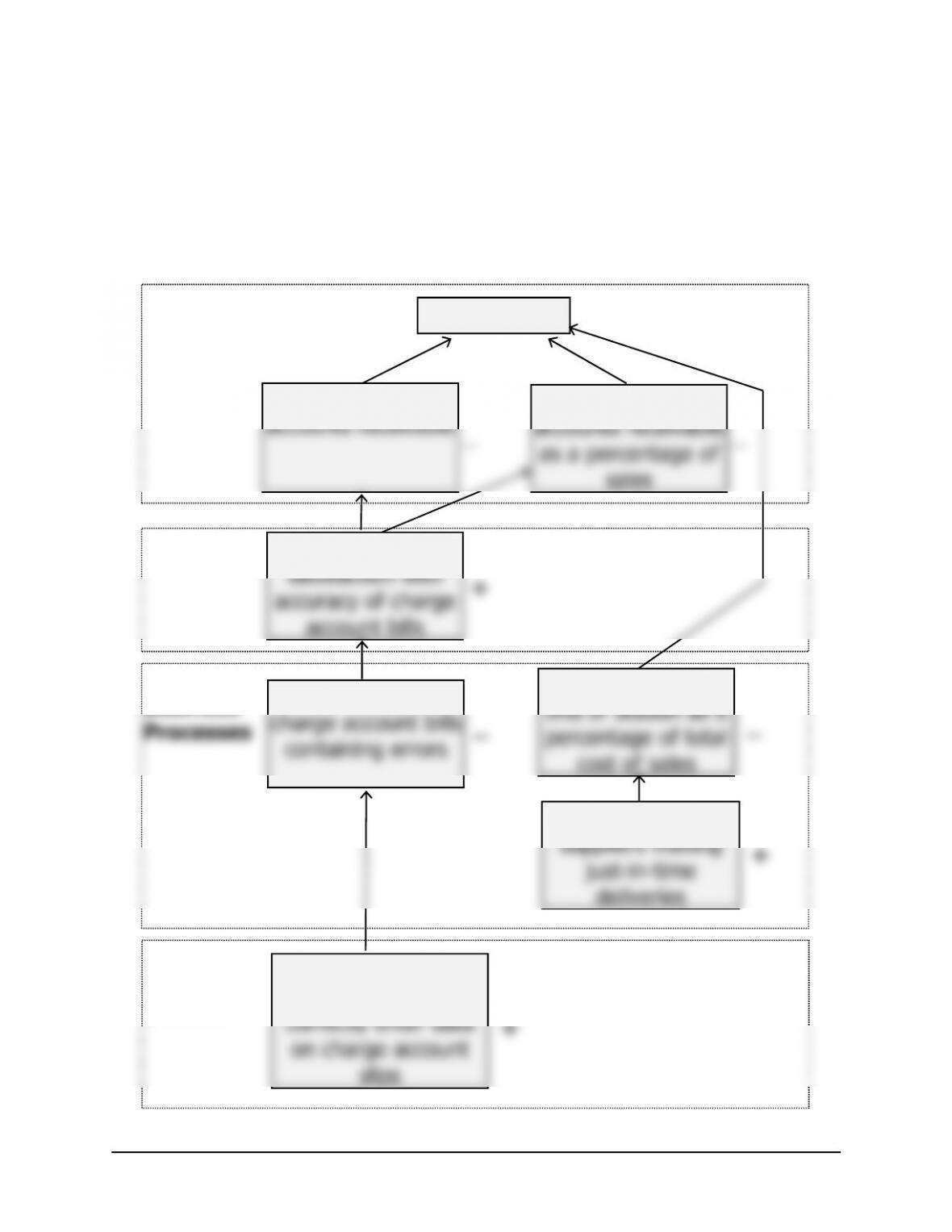

1. Student answers may differ concerning which category—learning and

growth, internal business processes, customers, or financial—a

particular performance measure belongs to.

Total profit

Average age of

Written-off

Customer

Percentage of

Unsold inventory at

Percentage of

Percentage of sales

clerks trained to

+

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

52 Managerial Accounting, 16th Edition

Case 11-23 (continued)

A number of the performance measures suggested by managers have

not been included in the above balanced scorecard. The excluded

performance measures may have an impact on total profit, but they are

2. The results of operations can be exploited for information about the

company’s strategy. Each link in the balanced scorecard should be

regarded as a hypothesis of the form “If …, then …”. For example, the

balanced scorecard on the previous page contains the hypothesis “If

customers express greater satisfaction with the accuracy of their charge

In general, the most important results are those that provide evidence

inconsistent with the hypotheses embedded in the balanced scorecard.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Chapter 11 53

Case 11-23 (continued)

3. a. This evidence is inconsistent with two of the hypotheses underlying

the balanced scorecard. The first of these hypotheses is “If customers

express greater satisfaction with the accuracy of their charge account

bills, then the average age of accounts receivable will improve.” The

second of these hypotheses is “If customers express greater

satisfaction with the accuracy of their charge account bills, then there

will be improvement in bad debts.” There are a number of possible

b. This evidence is inconsistent with three hypotheses. The first of these

is “If the average age of receivables declines, then profits will

increase.” The second hypothesis is “If the written-off accounts

Again, there are a number of possible explanations for the lack of

results consistent with the hypotheses. Managers may have

decreased the average age of receivables by simply writing off old

accounts earlier than was done previously. This would actually

decrease reported profits in the short term. Bad debts as a

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

54 Managerial Accounting, 16th Edition

Case 11-23 (continued)

The reduction in unsold inventories at the end of the season as a

percentage of cost of sales could have occurred for a number of

reasons that are not necessarily good for profits. For example,

managers may have been too cautious about ordering goods to

restock low inventories—creating stockouts and lost sales. Or,

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 11A 55

Appendix 11A

Transfer Pricing

Exercise 11A-1 (30 minutes)

1. a. The lowest acceptable transfer price from the perspective of the

selling division is given by the following formula:

T

otal contribution mar

g

in

on lost sales

Variable cost

Transfer price +

³

b. The Hi-Fi division can buy a similar speaker from an outside supplier

for $57. Therefore, the Hi-Fi Division would be unwilling to pay more

c. Combining the requirements of both the selling division and the

Assuming that the managers understand their own businesses and

d. From the standpoint of the entire company, the transfer should take

place. The cost of the speakers transferred is only $42 and the

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

56 Managerial Accounting, 16th Edition

Exercise 11A-1 (continued)

2. a. Each of the 5,000 units transferred to the Hi-Fi Division must displace

a sale to an outsider at a price of $60. Therefore, the selling division

would demand a transfer price of at least $60. This can also be

computed using the formula for the lowest acceptable transfer price

b. As before, the Hi-Fi Division would be unwilling to pay more than $57

c. The requirements of the selling and buying divisions in this instance

are incompatible. The selling division must have a price of at least

d. From the standpoint of the entire company, the transfer should not

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 11A 57

Exercise 11A-2 (20 minutes)

1.

Division A Division B

Total

Company

Sales ……………………… $2,500,0001$1,200,0002$3,200,0003

Expenses:

A

dded by the division . 1,800,000 400,000 2,200,000

T

ransfer price paid …… 500,000

3Division A outside sales

(16,000 units × $125 per unit) ………………. $2,000,000

Division B outside sales

T

2. Division A should transfer the 1,000 additional circuit boards to Division

B. Note that Division B’s processing adds $175 to each unit’s selling

price (B’s $300 selling price – A’s $125 selling price = $175 increase),

but it adds only $100 in cost. Therefore, each board transferred to

T

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

58 Managerial Accounting, 16th Edition

Exercise 11A-3 (20 minutes)

1a. The lowest acceptable transfer price from the perspective of the selling

division is given by the following formula:

T

otal contribution mar

g

in

on lost sales

Variable cost

1b. The buying division, Division Y, can buy a similar unit from an outside

1c. There is no range of acceptable transfer prices. The requirements of

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

Solutions Manual, Appendix 11A 59

Exercise 11A-3 (continued)

2a. In this case, Division X has enough idle capacity to satisfy Division Y’s

demand. Therefore, there are no lost sales and the lowest acceptable

2b. The buying division, Division Y, can buy a similar unit from an outside

supplier for $74. Therefore, Division Y would be unwilling to pay more

2c. As shown below, the range of acceptable transfer prices is $60 to $74.

© The McGraw-Hill Companies, Inc., 2018. All rights reserved.

60 Managerial Accounting, 16th Edition

Problem 11A-4 (60 minutes)

1. The lowest acceptable transfer price from the perspective of the selling

division is given by the following formula:

Variable cost

The Pulp Division has no idle capacity, so transfers from the Pulp

Division to the Carton Division would cut directly into normal sales of

pulp to outsiders. The costs are the same whether the pulp is

Therefore, the Pulp Division will refuse to transfer at a price less than

$70 a ton.

The Carton Division can buy pulp from an outside supplier for $70 a ton,

less a 10% quantity discount of $7, or $63 a ton. Therefore, the Division

The requirements of the two divisions are incompatible. The Carton

2. The price being paid to the outside supplier, net of the quantity

discount, is only $63. If the Pulp Division meets this price, then profits in

the Pulp Division and in the company as a whole will drop by $35,000

per year:

Lost revenue per ton ………………………. $70